Problem E-1B (Continued)

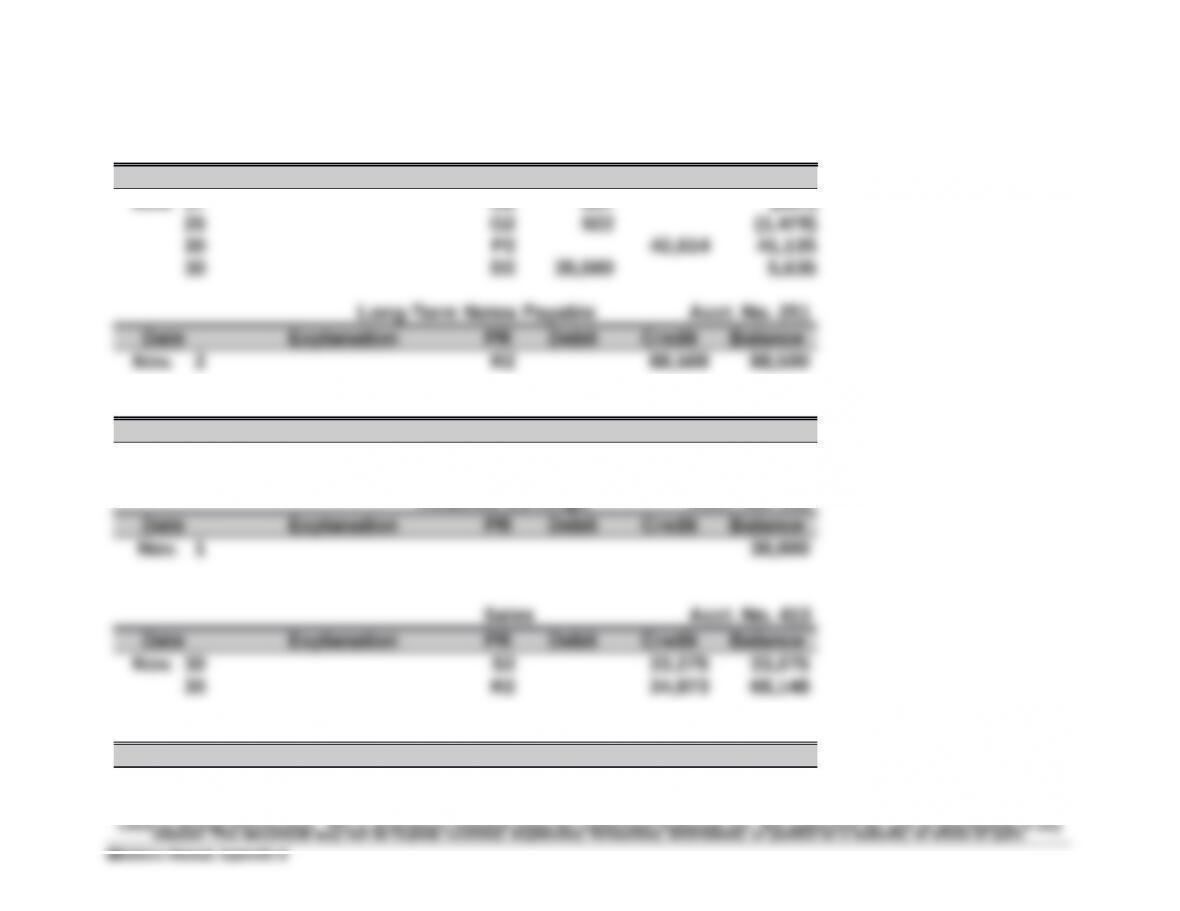

Accounts Payable Acct. No. 201

Date Explanation PR Debit Credit Balance

Nov. 17 G2 557 (557)

Common Stock Acct. No. 307

Date Explanation PR Debit Credit Balance

Nov. 1 10,000

Retained Earnings Acct. No. 318

Sales Discounts Acct. No. 415

Date Explanation PR Debit Credit Balance

Nov. 30 R2 506 506

Costs of Goods Sold Acct. No. 502

Date Explanation PR Debit Credit Balance

Nov. 30 S2 19,050 19,050

30 R2 19,200 38,250

30 D2 6,585 13,170

Problem E-1B (Continued)

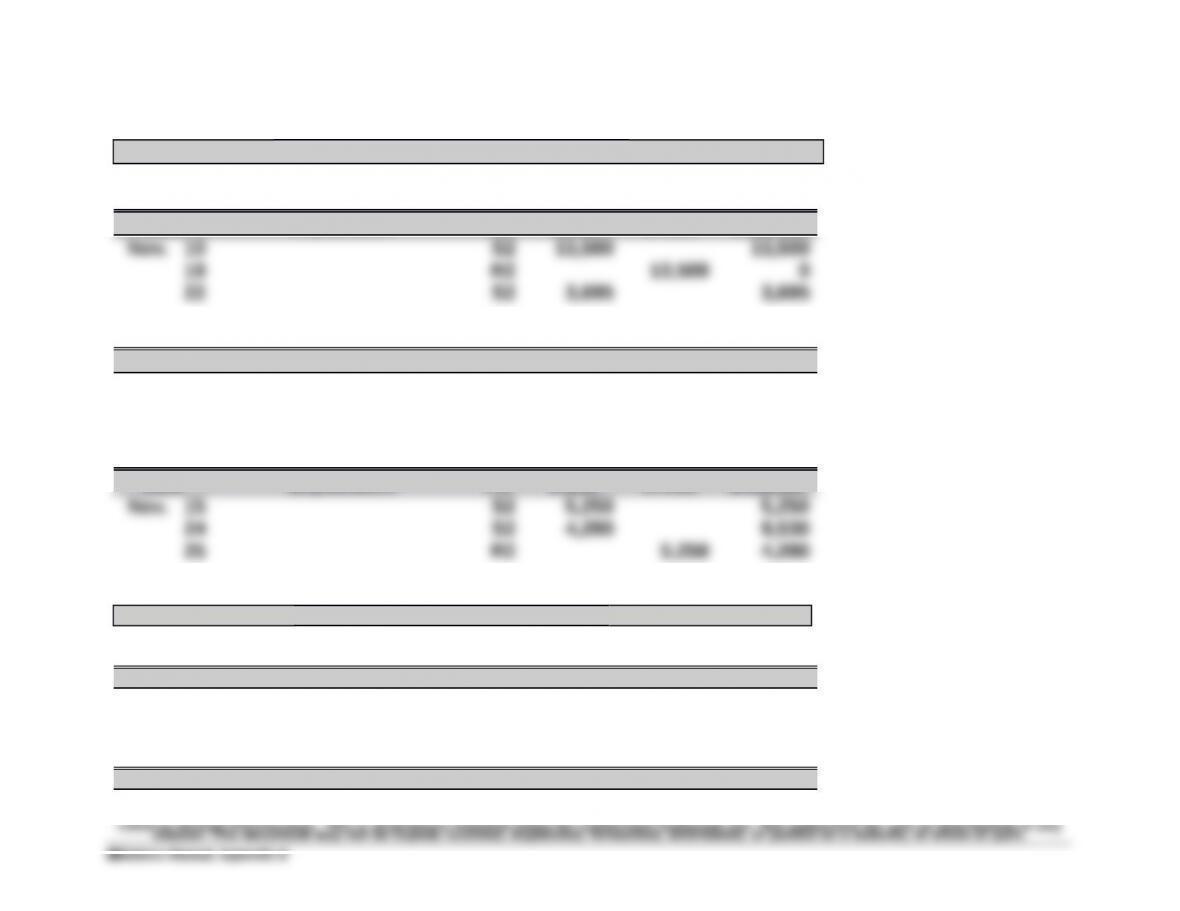

ACCOUNTS RECEIVABLE LEDGER

Carlos Mantel

Date Explanation PR Debit Credit Balance

Cyd Rounder

Date Explanation PR Debit Credit Balance

Nov. 8 S2 6,550 6,550

18 R2 6,550 0

Tori Tripp

Date Explanation PR Debit Credit Balance

ACCOUNTS PAYABLE LEDGER

BLR Industries

Date Explanation PR Debit Credit Balance

Nov. 4 P2 33,500 33,500

12 D2 33,500 0

Brun Supply

Date Explanation PR Debit Credit Balance

Nov. 1 P2 5,058 5,058

26 G2 922 4,136

Grebe Company

Date Explanation PR Debit Credit Balance

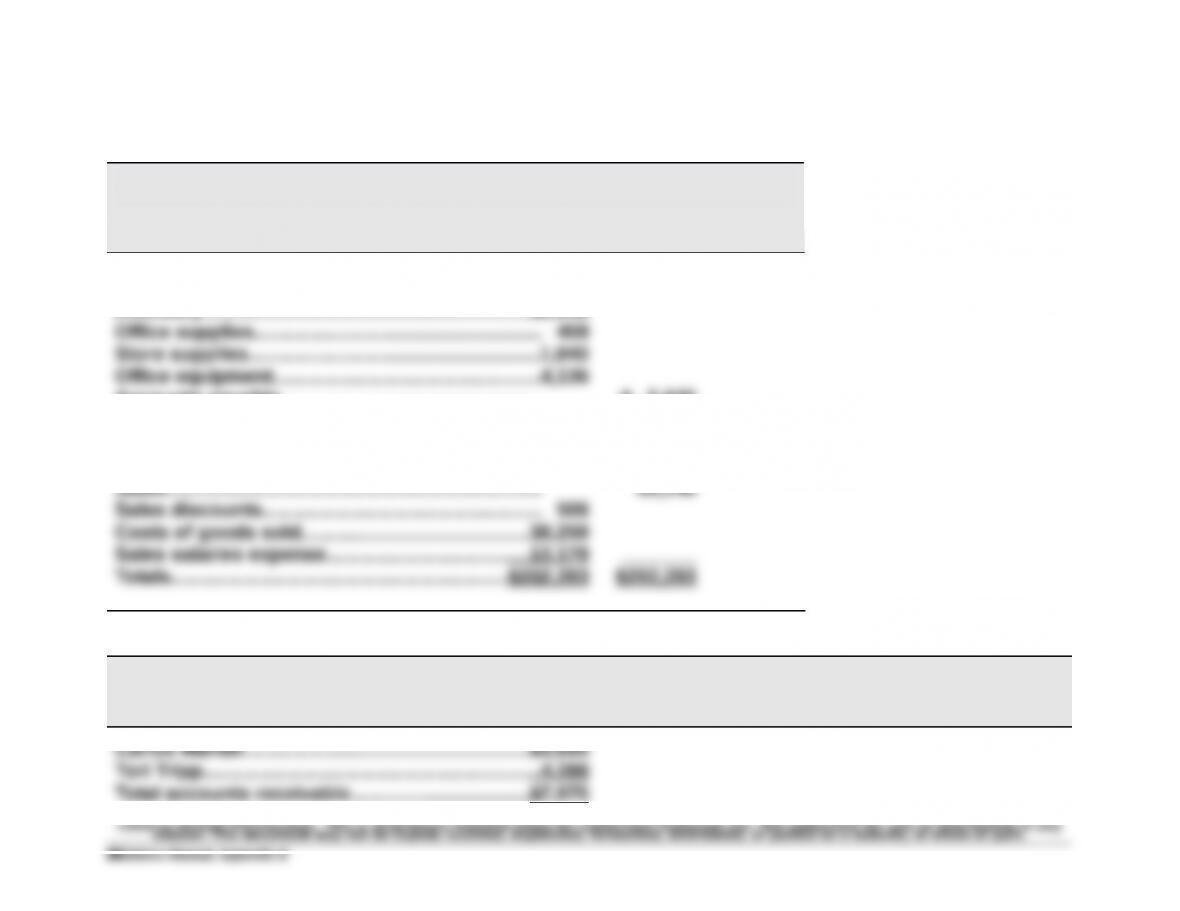

Problem E-1B (Concluded)

Part 3

GRASSLEY COMPANY

Trial Balance

November 30

Debit Credit

Cash……………………………………….…..….….….….…$100,207

Accounts receivable……….……………….…..….…... 7,975

Inventory………….…………………….……………….…... 36,540

Accounts payable……………….…..….….….….….…. $ 5,635

Long-term notes payable……………….….….….….. 88,500

Common stock…………..…………………..…..….….… 10,000

Retained earnings…………………………….….….…... 30,000

GRASSLEY COMPANY

Schedule of Accounts Receivable

November 30

GRASSLEY COMPANY

Schedule of Accounts Payable

November 30

Brun Supply……………..…………………..………….…..$4,136

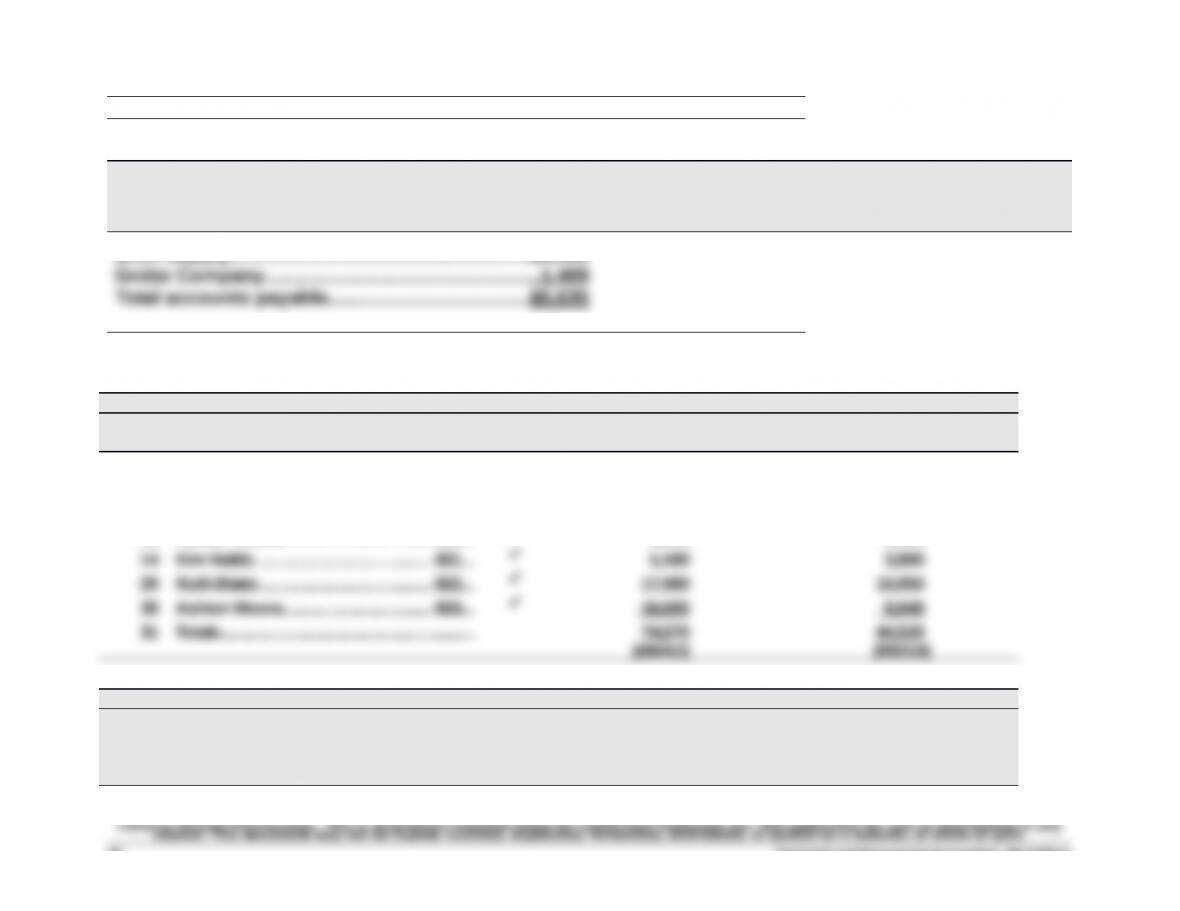

Problem E-2B (70 minutes)

Parts 1 and 2

SALES JOURNAL Page 3

Date Account Debited

Invoice

Number PR

Accounts Receivable Dr.

Sales Cr.

Cost of Goods Sold Dr.

Inventory Cr.

July

5

Kim Nettle………………………..….……….…

918 19,200 10,500

6 Ruth Blake……………………….…….…….…

919 7,500 4,300

13 Ashton Moore……………………….………...

920 8,550 5,230

CASH RECEIPTS JOURNAL Page 3

Date Account Credited Explanation PR

Cash

Dr.

Sales

Discoun

t

Dr.

Accounts

Receivable

Cr.

Sales

Cr.

Other

Accts.

Cr.

Cost of Goods

Sold Dr.

Inventory Cr.

Financial and Managerial Accounting, 6th Edition

46

21 L.T. Notes Pay…………………………………..Note to bank……………………………………………….……….………

251 15,000 15,000

23 Ashton Moore…………………….….………..Sale of 7/13…………………………………………………………….……

8,379 171 8,550

Problem E-2B (Continued)

Parts 2 and 3

GENERAL LEDGER

Cash Acct. No. 101

Date Explanation PR Debit Credit Balance

July 31 R3 253,137 353,137

Accounts Receivable Acct. No. 106

Date Explanation PR Debit Credit Balance

July 31 S3 74,670 74,670

31 R3 40,350 34,320

Inventory Acct. No. 119

Date Explanation PR Debit Credit Balance

Long-Term Notes Payable Acct. No. 251

Date Explanation PR Debit Credit Balance

June 30 200,000

July 21 R3 15,000 215,000

Common Stock Acct. No. 307

Sales Acct. No. 413

Date Explanation PR Debit Credit Balance

July 31 S3 74,670 74,670

31 R3 198,594 273,264

Problem E-2B (Continued)

Parts 2 and 3 (continued)

ACCOUNTS RECEIVABLE LEDGER

Ruth Blake

Ashton Moore

Date Explanation PR Debit Credit Balance

July 13 S3 8,550 8,550

23 R3 8,550 0

30 S3 16,820 16,820

Part 4

ACORN INDUSTRIES

Trial Balance

July 31

Debit Credit

Cash……………………………………….…..….….….….…

$353,137

Accounts receivable……….……………….…..….…...

34,320

Inventory………….…………………….……………….…...

25,295

Long-term notes payable……………….….….….….. $215,000