Problem C-3A (Continued)

2017

June 21 Cash …………..…………………..…………….…………………………….…56,720

Gain on Sale of Investments …….……………………………….. 1,055

Long-Term Investments—AFS (Sony)………………………….. 55,665

Sold Sony shares [(1,200 x $48.00) – $880].

June 30 Long-Term Investments—AFS (Black & Decker)…….…..…….……50,835

Aug. 3 Cash …………..……………………………………………………………….…9,315

[(600 x $16.25) – $435].

Nov. 1 Cash …………..………………………………….…………………..……….…19,850

Gain on Sale of Investments …….……………….….…….……. 4,352

Dec. 31 Fair Value Adjustment—AFS (LT)*..…..………………………………21,858

Unrealized Loss—Equity……………………………….…….……. 13,818

Unrealized Gain—Equity……….……………..……………………. 8,040

Annual adjustment to fair values.

* Cost Fair Value

Black & Decker: 1,400 x $39.00 = $ 54,600

Microsoft: 2,400 x $69.00 = $165,600

$212,160 – $220,200 = $8,040 (fair value exceeds cost)

Problem C-3A (Concluded)

Part 2

12/31/2015 12/31/2016 12/31/2017

Long-Term AFS Securities (cost)……….………. $117,100 $85,143 $212,160

Part 3

2015 2016 2017

Realized gains (losses)

Sale of Johnson & Johnson shares....... $ 2,235

Sale of Mattel shares……………….…………. (5,080)

Sale of Sara Lee shares…………….….……. $(4,665)

Sale of Sony shares…………..…….…….….. 1,055

Problem C-4A (30 minutes)

Part 1

1. Journal entries (assuming significant influence)

2015

Jan. 5 Long-Term Investments—Kildaire…….……………………….…….….1,560,000

Oct. 23 Cash………………………………….……………………………………………192,000

Long-Term Investments—Kildaire…………………………..……..192,000

Received cash dividend (60,000 x $3.20).

Dec. 31 Long-Term Investments—Kildaire……..………………………………..232,800

2016

Oct. 15 Cash………………………………….……………………………………………156,000

Long-Term Investments—Kildaire…………………………..……..156,000

Record cash dividend (60,000 x $2.60).

Dec. 31 Long-Term Investments—Kildaire……..………………………………..295,200

($1,476,000 x 20%).

2017

Jan. 2 Cash…………………………………………………………………………….…1,894,000

Gain on Sale of Investments……..………………………………..154,000

Long-Term Investments—Kildaire*………………………………..1,740,000

Sold Kildaire shares.

* Investment carrying value, January 2, 2017

Original cost…….…………………………….…. $1,560,000

Problem C-4A (Continued)

2. Carrying value per share, January 1, 2017 (see computations in part 1)

3. Change in Selk’s equity due to stock investment

Earnings from Kildaire (2015)………….……..….….…….…$232,800

Net increase………………….……………..…………………….….$682 ,000

Part 2

1. Journal entries (assuming NO significant influence)

2015

Jan. 5 Long-Term Investments—AFS (Kildaire)………………….…….……1,560,000

Cash…………………………..……………………………………………..1,560,000

Purchased Kildaire shares.

2016

Oct. 15 Cash…………………..…………………………………………………………..156,000

Dividend Revenue……..…………………………….…….…….……156,000

Received cash dividends (60,000 x $2.60).

Dec. 31 Fair Value Adjustment—AFS (LT)*……….………………….….……120,000

$360,000 – $240,000 = $120,000

Problem C-4A (Concluded)

2017

Jan. 2 Cash……………………………………………………………………………….1,894,000

Sold Kildaire shares.

Jan. 2 Unrealized Gain—Equity……………..…………………………………..360,000

2. Investment cost per share, January 1, 2017

$1,560,000 / 60,000 shares = $26

3. Change in Selk’s equity due to stock investment

Dividend Revenue (2015)…..…….…….….…….. $192,000

Financial and Managerial Accounting, 6th Edition

36

Problem C-5A (40 minutes)

Part 1

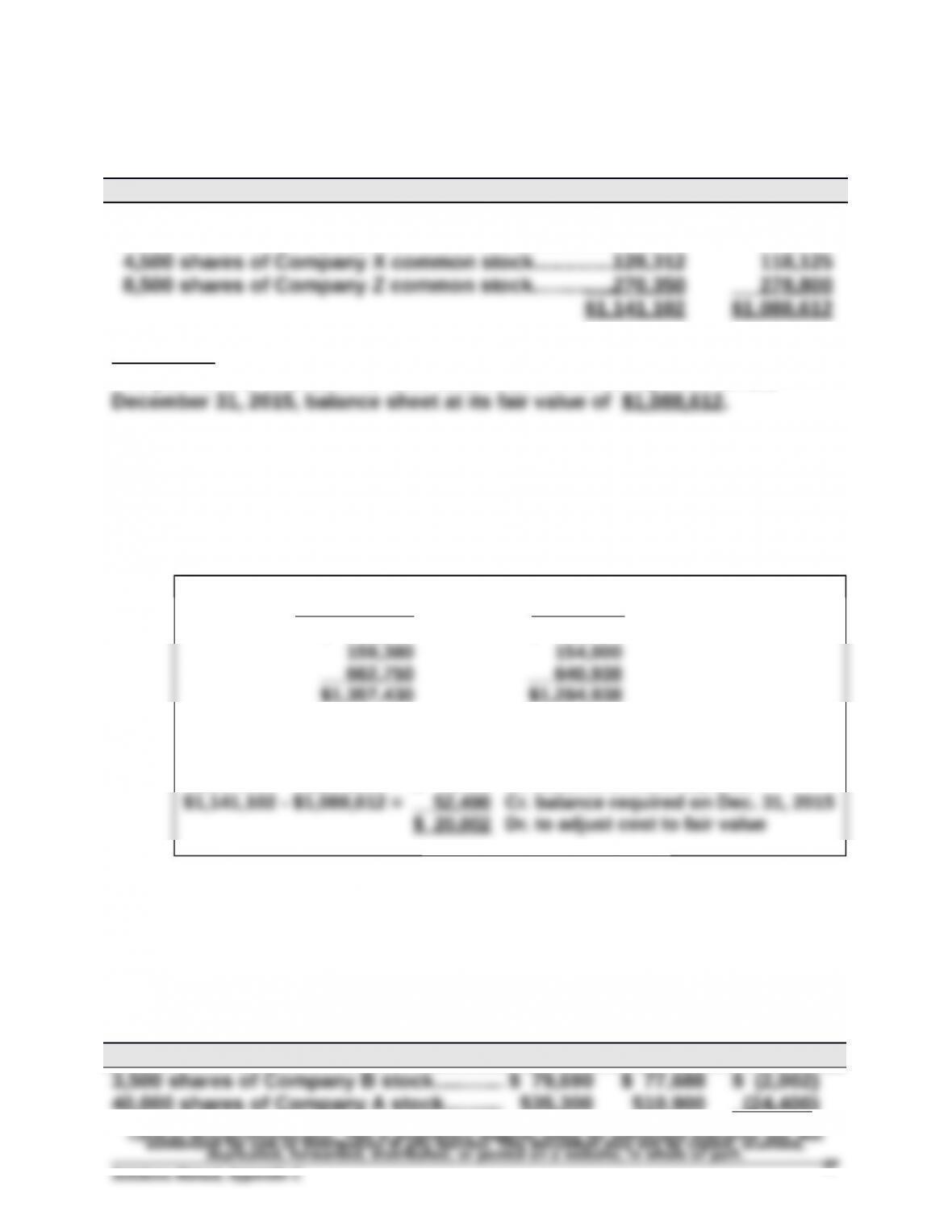

Available-for-sale securities on December 31, 2015

Security Cost Fair Value

3,500 shares of Company B common stock…………..$ 79,690 $ 81,375

17,500 shares of Company C common stock…………..662,750 610,312

Disclosure

The portfolio of available-for-sale securities would be reported on the

Part 2

Dec. 31 Fair Value Adjustment—AFS*…………….….….…….….…….…….20,002

Unrealized Loss—Equity…………..………………….…….……. 20,002

Adjustment to fair value for AFS securities..

* December 31, 2014, available-for-sale securities

Cost _ Fair Value

$ 535,300 $ 490,000

December 31, 2015, adjustment to the Fair Value Adjustment account:

$1,357,430 – $1,284,938 = $ 72,492 Cr. balance on Dec. 31, 2014

Part 3

Only gains or losses realized on the sale of available-for-sale securities

appear on the 2015 income statement. Unrealized gains or losses appear

in the equity section of the balance sheet.

Year 2015 realized gains (losses)

Stock Sold Cost Sale Gain (Loss)

40,000 shares of Company A stock.......... 535,300 510,900 (24,400)

Problem C-6AA (60 minutes)

Part 1

2015

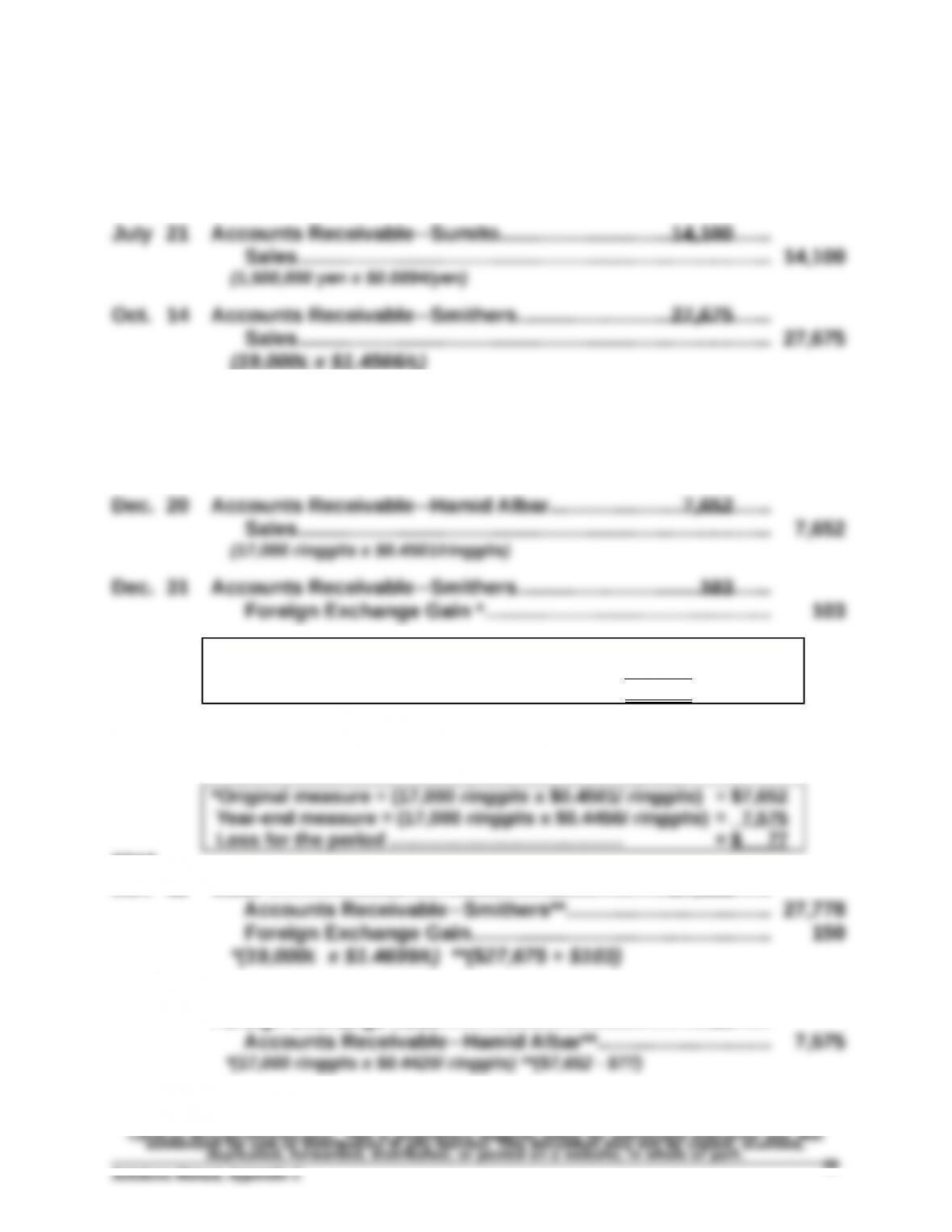

Apr. 8 Cash……………………………………………………………………………....5,938

Sales……….…………………………………………………..…….…….. 5,938

Nov. 18 Cash………………………………………….…………………………………...13,800

Foreign Exchange Loss……….………………..…………………….….300

Accounts ReceivableSumito…………………..….…….….…. 14,100

(1,500,000 yen x $0.0092/yen)

*Original measure = (19,000£ x $1.4566/£) = $27,675

Year-end measure = (19,000£ x $1.4620/£) = 27,778

Gain for the period ……………………… = $ 103

Dec. 31 Foreign Exchange Loss*…………………………..…….…….…….….77

Accounts ReceivableHamid Albar….……………………….. 77

2016

Jan. 12 Cash*……………………………………………………….…….….…….…….27,928

Jan. 19 Cash*……………………………………………………….…….….…….…….7,514

Foreign Exchange Loss……….………………..…………………….….61

Problem C-6AA (Continued)

Part 2

Foreign exchange loss reported on the 2015 income statement

November 18……….…….….…….…….….. $(300)

Part 3

To reduce the risk of foreign exchange gain or loss, Doering could attempt

to negotiate foreign customer sales that are denominated in U.S. dollars.

To accomplish this, Doering might be willing to offer favorable terms, such

NOTE: A few students may also understand Doering’s opportunity for hedging.