Chapter 09 – Behavioral Finance and Technical Analysis

CHAPTER NINE

BEHAVIORAL FINANCE AND TECHNICAL ANALYSIS

CHAPTER OVERVIEW

1. The Behavioral Critique

PPT 9-2 through PPT 9-13

The area of behavioral finance is relatively new but has been growing in popularity. The

behavioralists offer explanations of asset pricing that may perhaps explain some of the observed

anomalies in efficient markets, although other explanations are possible. The purpose of

research has been the dot-com and the housing bubbles. Whether behavioralism will remain as

popular in today’s environment remains to be seen. Extrapolation bias and overconfidence can

occur if an analyst or investor places too much confidence in historical statistical behavior. For

instance, believing that earnings will continue to rise simply because they have for the last eight

quarters will lead to underestimating volatility and overestimating value. Some of these problems

fundamentals change. Anchoring bias, or conservatism, as the text calls it, is a similar

phenomenon. The PPT refers to framing errors. This term refers to a person’s tendency make a

different decision with same set of facts if they are framed differently. Regret avoidance and loss

aversion are examples of framing decisions. Some individuals tend to increase risk if they believe

they are facing a loss anyway in an attempt to avoid the loss. They may choose to do this even if

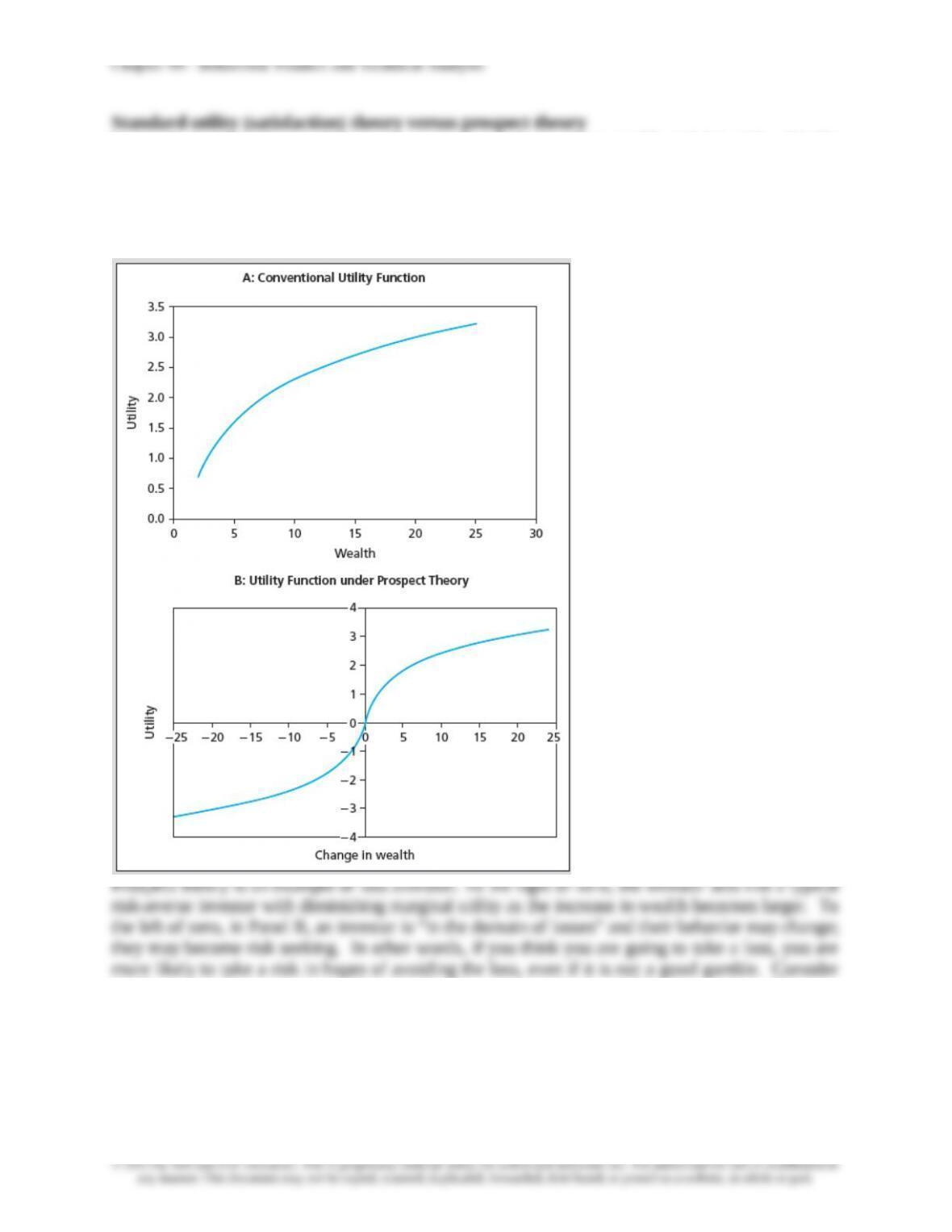

In standard utility theory of investments, investors desire more wealth and less risk. Wealth

provides diminishing marginal utility; thus a gain of $1,000 provides less utility than the utility loss

from losing $1,000. This gives rise to risk aversion. Prospect theory is an alternative behavioral-

based theory that asserts that investor utility depends on the change in wealth from the start of the

investment rather than on the starting level of wealth.

conducting a class exercise to demonstrate that some people do exhibit loss aversion. This may

explain why people are reluctant to sell losers in their portfolio, holding on to them during periods

of declining performance.

9-2

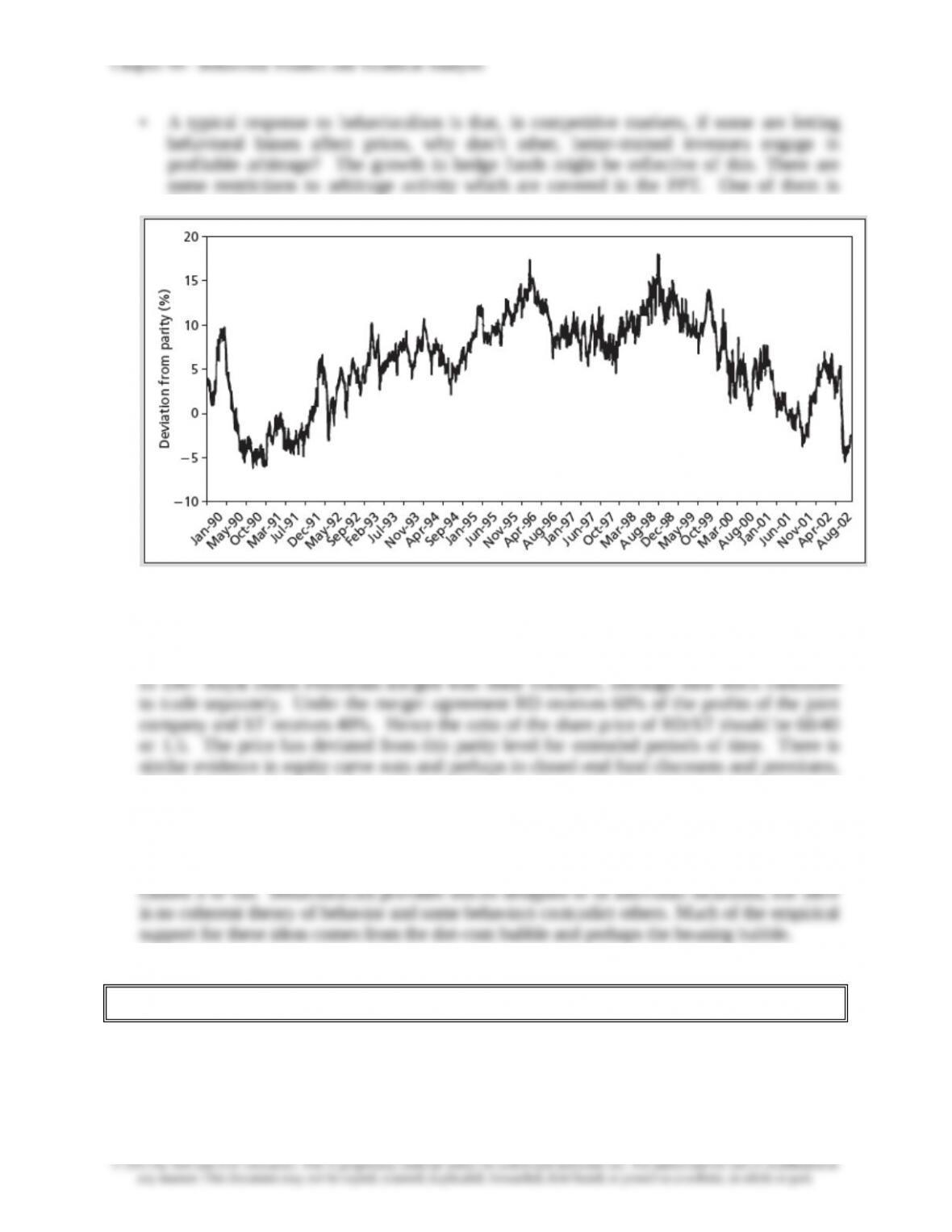

illustrated below:

60:40 split of profits from merger between RD and Shell

Stock price ratio RD/Shell should = 60/40 = 1.5

If RD/Shell > 1.5, then short RD and buy Shell

If you had done this in 1993, you would have LOST money until 1999.

although both of these may have other explanations. Remember Keynes’ quote, “Markets can

remain irrational longer than you can remain solvent.” What if prices don’t conform to your

models in the near term? This can be disastrous if you are levered. Ultimately this is why

Long Term Capital Management Hedge Fund failed. In the long run, their bets were correct,

but the markets did not return to ‘normal’ levels immediately and the fund’s excessive leverage

2. Technical Analysis and Behavioral Finance

PPT 9-14 through PPT 9-30

9-3

Chapter 09 – Behavioral Finance and Technical Analysis

TA belief. Under the disposition effect investors exhibit loss aversion so that they are reluctant to

sell on bad news and price converges slowly to its new fundamental value. While some investors

undoubtedly behave this way, this seems unlikely to be a true description of market prices

behavior.

The PPT covers various simple technical analysis rules. There are a vast number of TA rules that

buy signal is said to occur. A sell signal occurs when the stock price falls below the moving

average. Some of the more popular charting methods used are defined.

Several sentiment indicators are displayed in the PPT.

The Trin statistic measures the number and trading volume on stocks that are advancing and

declining. If the Trin statistic exceeds one, a bearish signal occurs. For many indicators, both

For a contrarian, a rise in the put/call ratio is bullish.

As a final word of warning—the ability to discern apparent patterns with stock market prices

means it is often possible to perceive patterns that may not exist. This is aptly illustrated in the

PPT using the associated figures in the text.

9-4