Chapter 08 – The Efficient Market Hypothesis

CHAPTER EIGHT

THE EFFICIENT MARKET HYPOTHESIS

CHAPTER OVERVIEW

This chapter examines the concept of market efficiency. We are asking whether securities are, on

concerned. However we may also ask a related question, “Are the markets efficient allocators of

capital?” In other words do market prices accurately reflect the current value of risk-adjusted-

expected-future cash flows? If they do then the markets are allocationally efficient. Markets

could be allocationally inefficient, but still be informationally efficient. This may arise due to

behavioral problems discussed in Chapter 9 or due to structural market problems. We will have

of market efficiency, the forms of market efficiency, and observed market anomalies. Market

efficiency is akin to the perfect competition model to which it is related. Like perfect

competition, it should be interpreted as an ideal that markets move toward but will probably

never completely and consistently achieve. Nevertheless the financial markets are highly

competitive and it is likely that markets will closely approach efficiency, the occasional bubbles

1. Random Walks and the Efficient Market Hypothesis

PPT 8-2 through PPT 8-6

Chapter 08 – The Efficient Market Hypothesis

Definitions of informational and allocational efficiency are provided. Implications of efficiency

are then discussed and the idea of random walk is introduced and illustrated. Note that we

actually expect there to be a positive trend in stock prices albeit with random movements around

those positive trends. The reason that we would expect to see price changes that are random is

related to efficiency. If information that has importance for stock values arrives or occurs in a

random fashion, price changes will occur randomly. If the market is efficient in its analysis, the

change in prices will reflect that information in a timely basis. The result will be random price

changes. The concept of market efficiency is related to the concept of competition. In efficient

markets, once information becomes available, participants will trade quickly on that information.

Competition assures that prices will reflect that information very quickly. If the information

does not become incorporated into price very quickly, market participants would act to eliminate

the inefficiency.

Questions arise about efficiency due to possible unequal access to information, structural market

problems and the psychology of investors (behavioralism). Structural market problems refer to

market imperfections. These include transaction costs limiting arbitrage, constraints on short

sales doing the same and recognizing that in volatile markets, most arbitrage strategies are really

risky arbitrage, not riskless arbitrage. We will have more to say on this later.

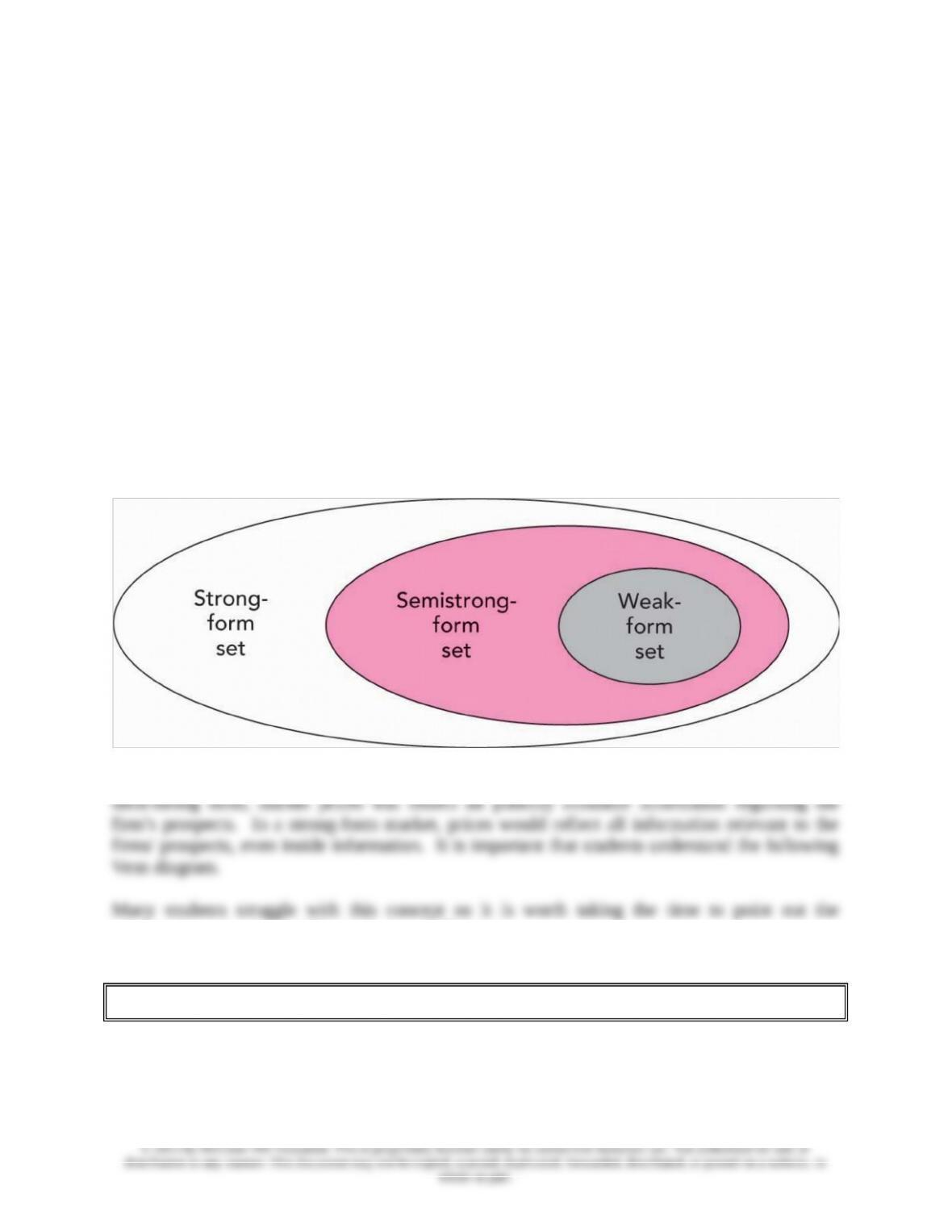

The forms of the efficient market are presented. In a weak-form efficient market, prices will

reflect all information that can be derived from trading data such as prices and volumes. In a

relationships among the different forms of efficiency.

2. Implications of the EMH (for Security Analysis)

PPT 8-7 through PPT 8-10

8-2

employment-related risk.

3. Are Markets Efficient?

PPT 8-11 through PPT 8-22

Over time stock prices tend to follow a submartingale. This has nothing to do with efficiency,

per se. It does however have serious implications for tests of efficiency. This implies that a

randomly chosen portfolio of stocks can be expected to have a positive return. In practice this

investor or an investment rule earns excess return, tests of market efficiency are joint tests of the

model used to estimate expected returns and market efficiency. Therefore, even when an

anomaly is discovered, we have to be careful in interpreting the results. Some apparent

anomalies are discussed including the Fama-French results, the Keim and Stambaugh findings

and the Campbell and Shiller work. Note that each of these results may also be consistent with

It is very difficult to predict if you are in a bubble and when the bubble will burst. Stock

prices are estimates of future economic performance of the firm and these estimates can

change rapidly.

Risk premiums can change rapidly and dramatically.

Nevertheless, with hindsight there appear to be times when stock prices decouple from intrinsic

• Prices eventually conform once more to intrinsic value. Many who don’t believe in

efficient markets anyway have jumped on this result to pronounce the death of market

efficiency. However, the bubbles bring into question the allocational efficiency of the

markets more than the informational efficiency. Very few people will be able to

consistently predict the extent and duration of a bubble.

2) during periods of cheap capital when interest rates are low for extended periods. In the

first case, values will be more heavily determined by future growth prospects rather than

the value of assets in place. During periods of cheap capital, new investments will be

undertaken based on future growth prospects as well. In both situations, new investors

with less investment knowledge and experience are likely to enter the markets, making a

values in price setting.

Some of the major types of tests that researchers have done on market efficiency are described. If

markets are inefficient, then professionals who spend considerable resources in investment

should secure superior performance. The tests are broken down in terms tests of the forms of

efficiency. Tests have uncovered some inefficiency in pricing but many possible interpretations

competitive markets. People rush to buy recent winners and in so doing drive up the price

enough so that future returns are not abnormal. This does not imply inefficiency unless the same

investors can consistently do this. Attempting to interpret the results of efficiency tests has led to

various explanations ranging from model misspecification to data mining.

4. Mutual Fund and Analyst Performance

PPT 8-23 through PPT 8-30

Some recent studies on mutual funds have documented some persistence in positive and negative