Chapter 05 – Risk and Return: Past and Prologue

1. The 1% VaR will be less than –30%. As percentile or probability of a return declines so

2. The geometric return represents a compounding growth number and will artificially

inflate the annual performance of the portfolio.

3. No. Since all items are presented in nominal figures, the input should also use nominal

data.

4. Decrease. Typically, standard deviation exceeds return. Thus, an underestimation of 4%

5. Using Equation 5.6, we can calculate the mean of the HPR as:

E(r) =

∑

s=1

S

p (s) r (s)

= (0.3 0.44) + (0.4 0.14) + [0.3 (–0.16)] = 0.14 or

14%

6. We use the below equation to calculate the holding period return of each scenario:

HPR =

Ending Price - Beginning Price + Cash Dividend

Be ginning Price

Chapter 05 – Risk and Return: Past and Prologue

7.

a. Time-weighted average returns are based on year-by-year rates of return.

Year Return = [(Capital gains + Dividend)/Price]

2010-2011 (110 – 100 + 4)/100 = 0.14 or 14.00%

2011-2012 (90 – 110 + 4)/110 = –0.1455 or –14.55%

2012-2013 (95 – 90 + 4)/90 = 0.10 or 10.00%

Chapter 05 – Risk and Return: Past and Prologue

3 396 Dividends on four shares,

plus sale of four shares at $95 per share

8.

a. Given that A = 4 and the projected standard deviation of the market return =

20%, we can use the below equation to solve for the expected market risk

premium:

Average( r M ) - r f

Average( r M ) - r f

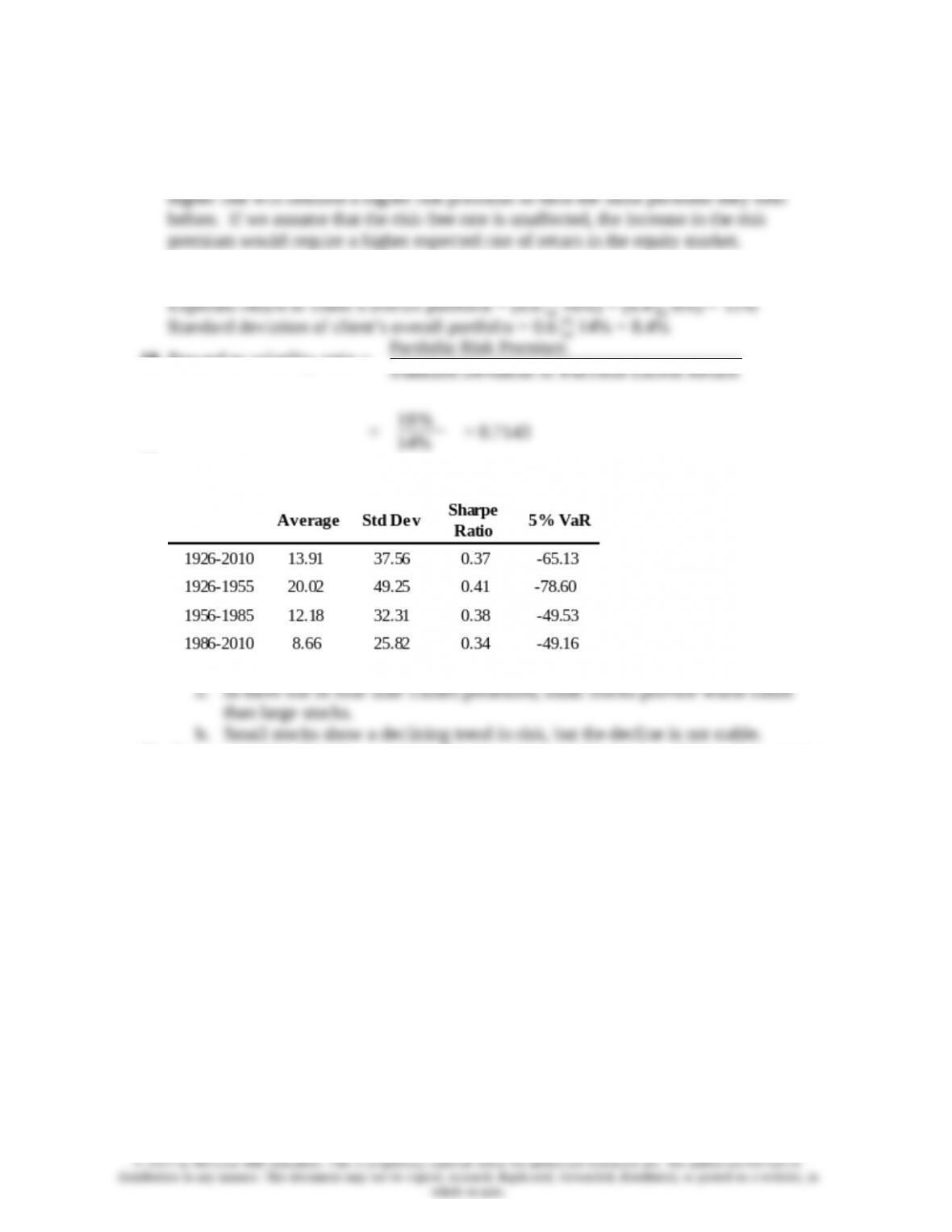

9. From Table 5.4, we find that for the period 1926 – 2010, the mean excess return for

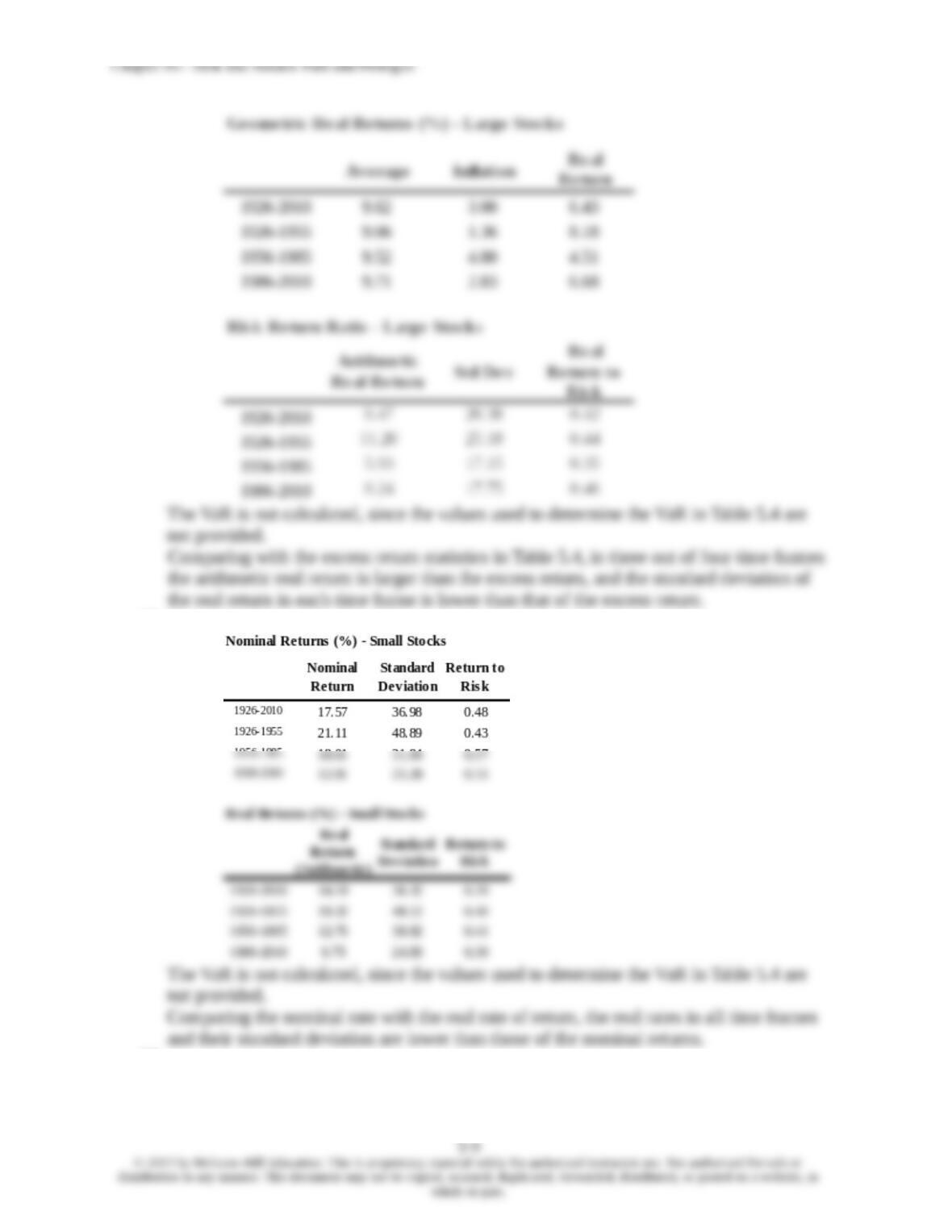

10. To answer this question with the data provided in the textbook, we look up the real

returns of the large stocks, small stocks, and Treasury Bonds for 1926-2010 from Table

5.2, and the real rate of return of T–Bills in the same period from Table 5.3:

Total Real Return – Geometric Average

Large Stocks: 6.43%

11.

a. The expected cash flow is: (0.5 $50,000) + (0.5 $150,000) = $100,000

With a risk premium of 10%, the required rate of return is 15%. Therefore, if

the value of the portfolio is X, then, in order to earn a 15% expected return:

5-3

must sell at lower prices. The extra discount in the purchase price from the expected

value is to compensate the investor for bearing additional risk.

12.

a. Allocating 70% of the capital in the risky portfolio P, and 30% in risk-free

asset, the client has an expected return on the complete portfolio calculated by

adding up the expected return of the risky proportion (y) and the expected return

of the proportion (1 – y) of the risk-free investment:

E(rC) = y E(rP) + (1 – y) rf

Security

Investment

Proportions

T-Bills

30.0%

Chapter 05 – Risk and Return: Past and Prologue

Portfolio Risk Premium

S tandard Deviation of Portfolio Excess Return

0. 27

E( rC ) - r f

0. 14 - 0.0 7

E( r P) - r f

0. 17 - 0.0 7

C

0. 189

E(r)

s

7

27

14

17

P

CAL ( slope=.3704)

%

%

18.9

client

13.

a. E(rC) = y E(rP) + (1 – y) rf

= y 0.17 + (1 – y) 0.07 = 0.15 or 15% per year

Solving for y, we get y =

0. 15 - 0.0 7

0. 10

= 0.8

14.

a. Standard deviation of the complete portfolio= C = y 0.27

If the client wants the standard deviation to be equal or less than 20%, then:

15.

a. Slope of the CML =

E( r M) - r f

M

=

0. 13 - 0.0 7

0. 25

= 0.24

16.

a. With 70% of his money in your fund’s portfolio, the client has an expected rate

of return of 14% per year and a standard deviation of 18.9% per year. If he

shifts that money to the passive portfolio (which has an expected rate of return

of 13% and standard deviation of 25%), his overall expected return and standard

5-6

return with a lower standard deviation using your fund portfolio rather than the

passive portfolio. To achieve a target mean of 11.2%, we first write the mean of

the complete portfolio as a function of the proportions invested in your fund

portfolio, y:

11.2% = 7% + 10% y y =

11.2% - 7%

10%

= 0.42

The standard deviation of the portfolio would be:

C = y 27% = 0.42 27% = 11.34%

Thus, by using your portfolio, the same 11.2% expected rate of return can be

17% - 7% - f

10 % - f

27%

27%

13 % - 7 %

25%

Chapter 05 – Risk and Return: Past and Prologue

10% – f = 27% 0.24 = 6.48%

f = 10% 6.48% = 3.52% per year

17. Assuming no change in tastes, that is, an unchanged risk aversion, investors perceiving

18. Expected return for your fund = T–bill rate + risk premium = 6% + 10% = 16%

19. Reward to volatility ratio =

Portfolio Risk Premium

S tandard Deviation of Portfolio Excess Return

=

10 %

14%

= 0.7143

20.

Excess Return (%)

21. For geometric real returns, we take the geometric average return and the real geometric

return data from Table 5.2 and then calculate the inflation in each time frame using the

equation: Inflation rate = (1 + Nominal rate)/(1 + Real rate) – 1.

5-8

22.

23.

Chapter 05 – Risk and Return: Past and Prologue

CFA 1 Answer: V(12/31/2011) = V(1/1/2005) (1 + g)7 = $100,000 (1.05)7 = $140,710.0

CFA 2 Answer: a. and b. are true. The standard deviation is non-negative.

CFA 3Answer: c. Determines most of the portfolio’s return and volatility over time.

CFA 5

Chapter 05 – Risk and Return: Past and Prologue

CFA 8

Answer:

Answer:

Answer:

CFA 11