Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 21 - Taxes, Inflation, and Investment Strategy

CHAPTER 21

TAXES, INFLATION, AND INVESTMENT STRATEGY

2. The owner will suffer from adverse selection. The owner will attract cargo that

would normally cost more than the flat fee being charged.

3. Passive investors who are not sophisticated and looking for reduced fees. These

4. The social security annuity is paid out for the balance of your life, regardless of

how long you live. The amount is determined based on the calculation of a

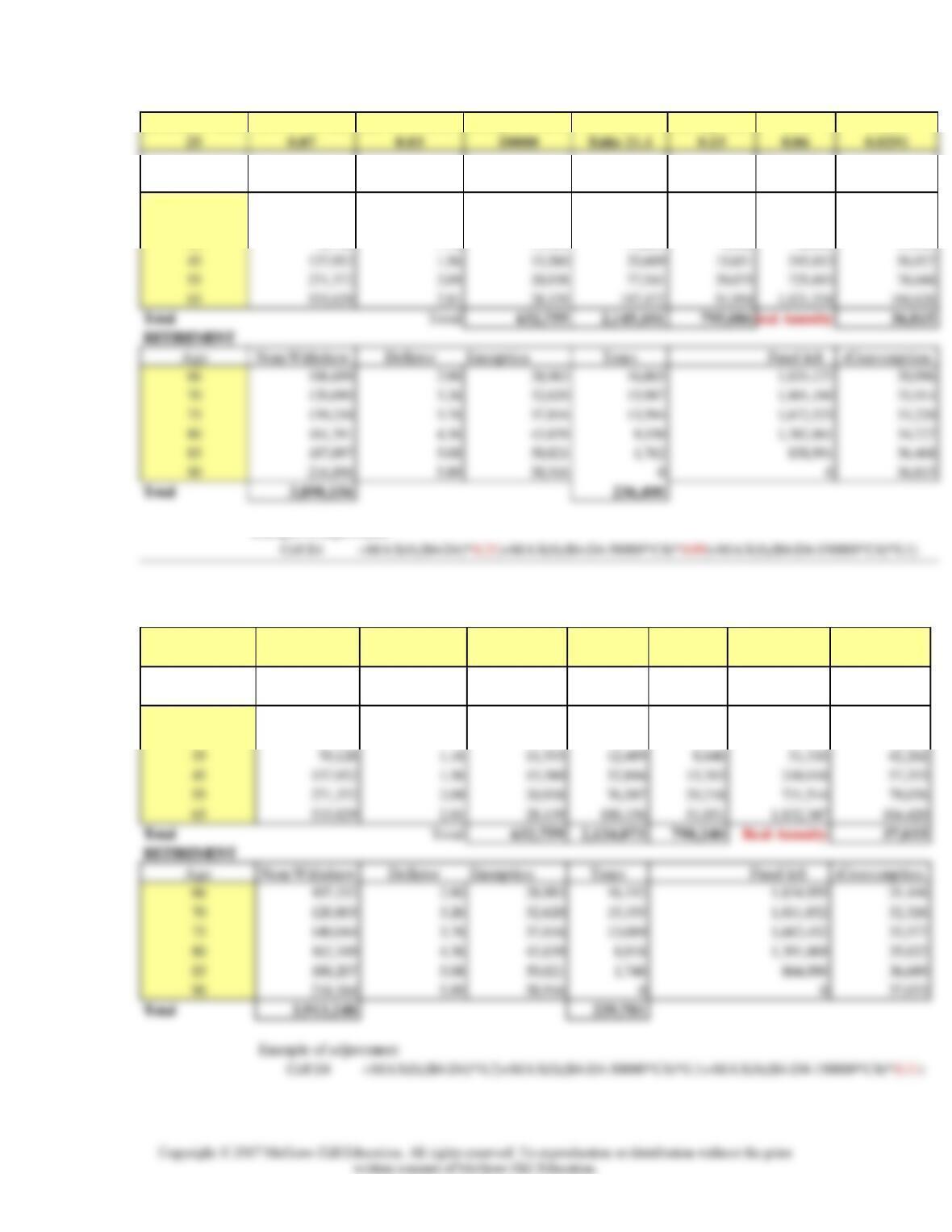

5. The progressive tax code sharpens the importance of taxes during the retirement

years. High tax rates during retirement reduce the effectiveness of a tax shelter. In

6. With a savings rate of 16%, the retirement annuity would be $205,060 (compared

to $192,244 with the 15% savings rate).

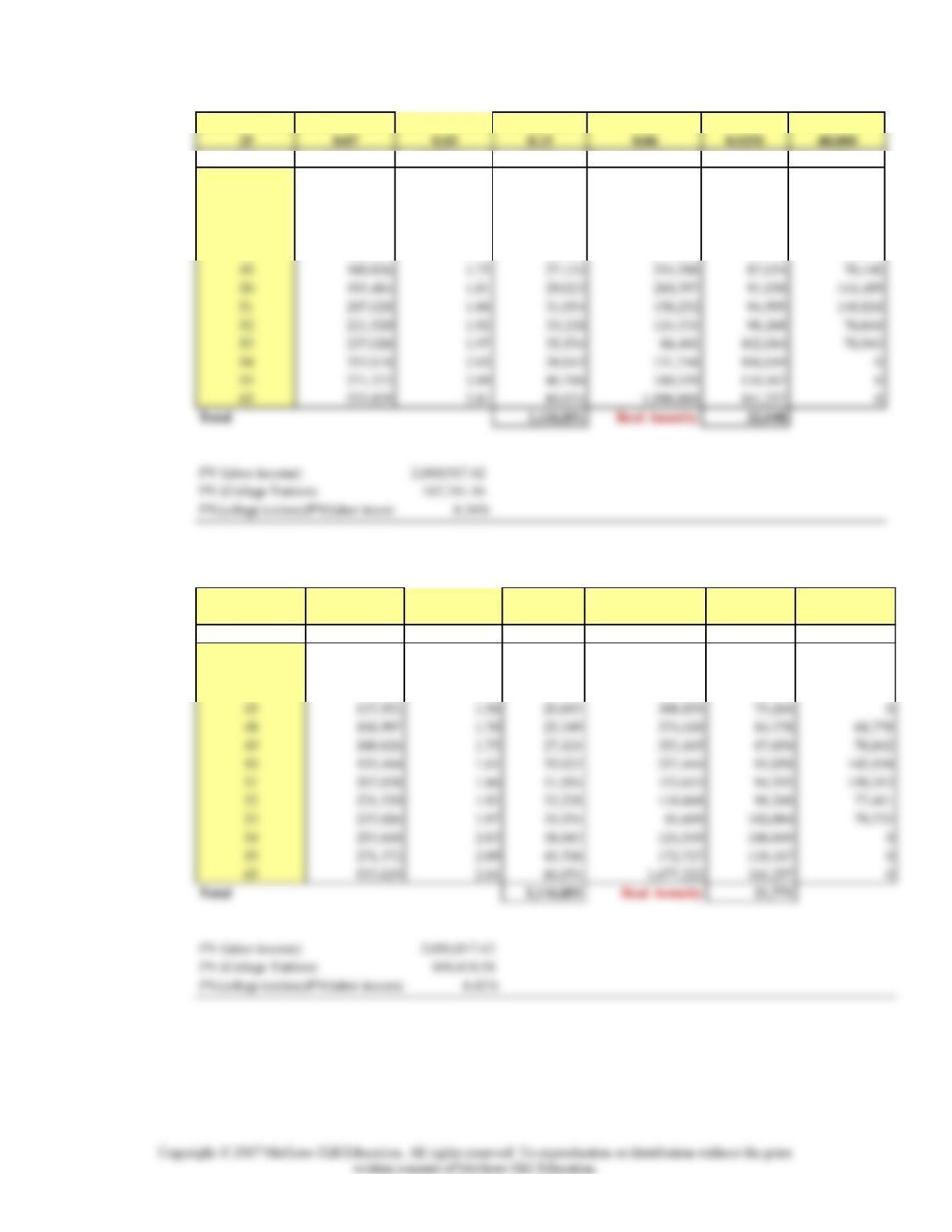

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement Years Income Growth Savings Rate ROR

Age Income Saving Cumulative Savings Consumption

30 50,000 8,000 8,000 42,000

7. With a savings rate of 16%, the retirement annuity will be $52,979 (vs. $49,668).

The growth in the real retirement annuity (6.67%) is the same as with the case of

no inflation.

Spreadsheet 21.2: Adjusted for Change in Savings Rate

Retirement Years Income Growth Rate of Inflation Savings Rate ROR rROR

Age Income Deflator Saving Cumulative Savings rConsumption

30 50,000 1.00 8,000 8,000 42,000

8. The objective is to obtain a real retirement annuity of $49,668, as in Spreadsheet

21.2. In Spreadsheet 21.3: Backloading the Real Savings Plan, select Data/Solver

from the menu bar. Set the objective value of Real Annuity to 49,668; Assign the

25 0.07 0.03 0.083 0.06 0.0291

Age Income Deflator Saving Cumulative Savings rConsumption

30 50,000 1.00 4,145 4,145 45,855

9. Because of the exemption from taxable income, only part of income is subject to

tax, while a change in ROR affects all savings.

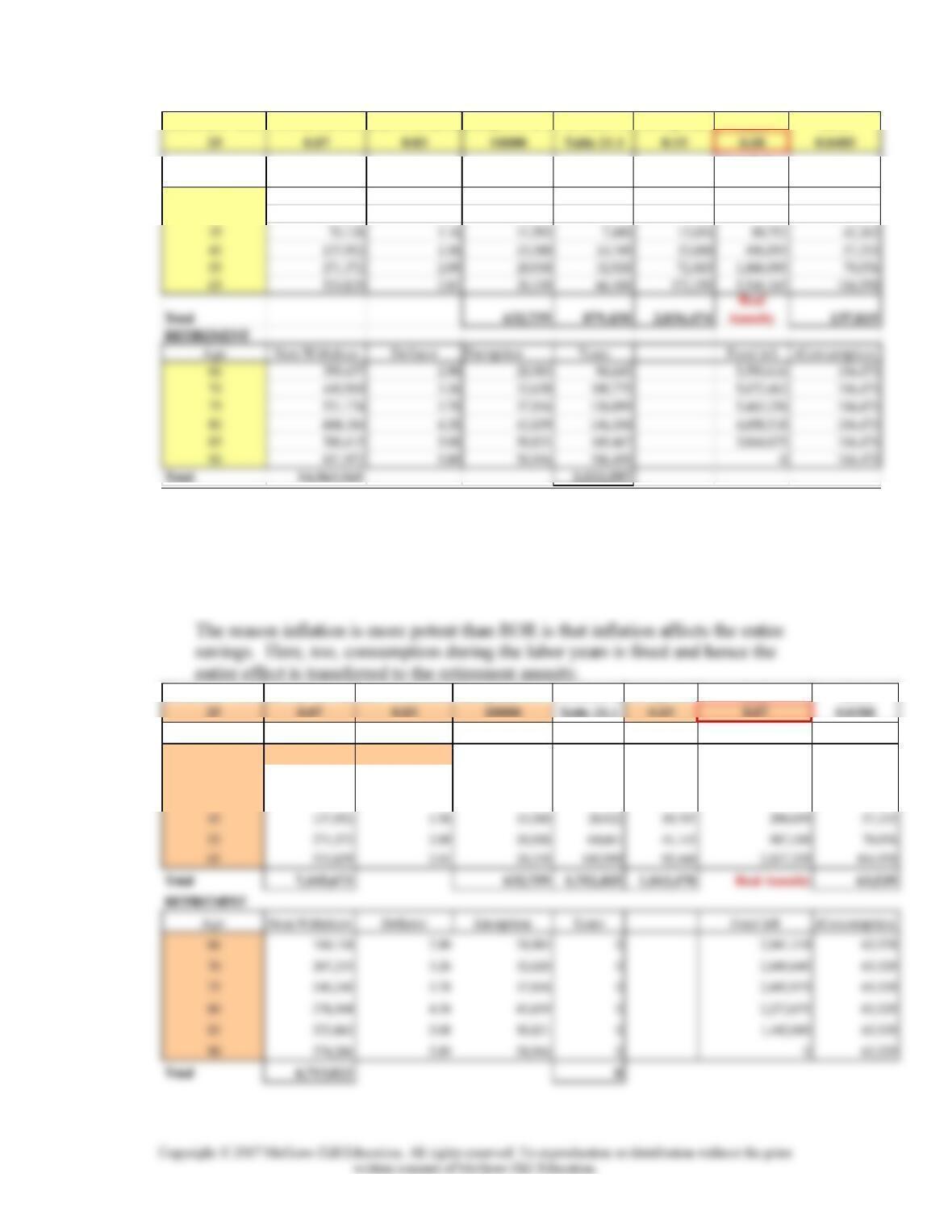

10. In the original Spreadsheet 21.5, real consumption during retirement is $60,789.

A 1% increase in the rate of inflation will reduce real consumption during

retirement to $15,780.

A 1% increase in the flat-tax rate reduces real consumption during retirement to

Chapter 21 - Taxes, Inflation, and Investment Strategy

Spreadsheet 21.5: Adjusted for Higher Rate of Inflation

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rate Saving Rate ROR rROR

25 0.07 0.04 15000 0.25 0.15 0.06 0.0192

Age Income Deflator Exemption Taxes Savings

Cumulative

Savings

rConsumption

30 50,000 1.00 15,000 5,016 9,922 9,922 35,063

31 53,500 1.04 15,600 5,518 10,309 20,826 36,224

RETIREMENT

Age Nom Withdraw Deflator Exemption Taxes Fund left rConsumption

66 65,827 4.10 61,559 1,067 1,255,966 15,780

70 77,008 4.80 72,015 1,248 1,268,594 15,780

11. In Spreadsheet 21.6, the real retirement annuity is $37,059.

A 1% increase in the lowest tax bracket reduces the real retirement annuity to $36,815.

A 1% increase in the highest tax bracket reduces the real retirement annuity to

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rates in Saving Rate ROR rROR

Age Income Deflator Exemption Taxes Savings

Cumulative

Savings

rConsumption

30 50,000 1.00 10,000 8,400 6,240 6,240 35,360

31 53,500 1.03 10,300 9,151 6,652 13,267 36,599

35 70,128 1.16 11,593 13,061 8,560 50,802 41,842

Example of adjustment

Retirement Years Income Growth Rate of Inflation

Exemption Now

Tax Rates in Saving Rate ROR rROR

25 0.07 0.03 10000 Table 21.1 0.15 0.06 0.0291

Age Income Deflator Exemption Taxes Savings

Cumulative

Savings

rConsumption

30 50,000 1.00 10,000 8,000 6,300 6,300 35,700

31 53,500 1.03 10,300 8,716 6,718 13,396 36,958

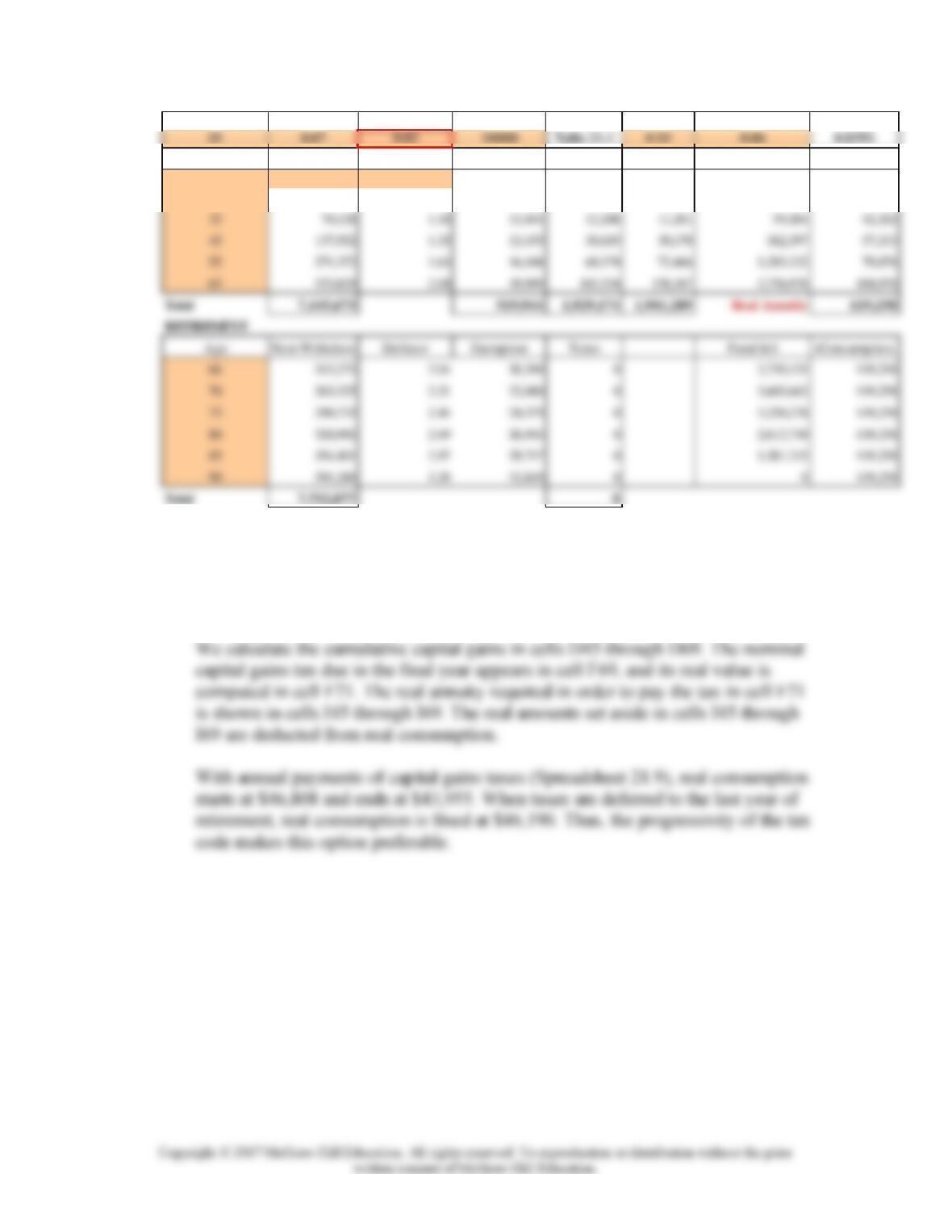

12. The real retirement annuity in Spreadsheet 21.7 is $83,380.

A decrease of 2% in the ROR reduces the real retirement annuity to $50,900.

An increase of 2% in the ROR increases the real retirement annuity to $137,819.

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rates in Saving Rate ROR rROR

25 0.07 0.03 10000 Table 21.1 0.15 0.04 0.0097

Age Income Deflator Exemption Taxes Savings

Cumulative

Savings

rConsumption

30 50,000 1.00 10,000 5,140 9,160 9,160 35,700

31 53,500 1.03 10,300 5,553 9,880 19,406 36,958

35 70,128 1.16 11,593 7,480 13,654 73,648 42,262

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rates in Saving Rate ROR rROR

Age Income Deflator Exemption Taxes Savings

Cumulative

Savings

rConsumption

30 50,000 1.00 10,000 5,140 9,160 9,160 35,700

31 53,500 1.03 10,300 5,553 9,880 19,773 36,958

13. The real retirement annuity in Spreadsheet 21.8 is $ 49,153.

A 1% increase in ROR increases the real retirement annuity to $63,529.

A 1% decrease in the rate of inflation increases the real retirement annuity to $119,258.

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rates in Saving Rate ROR rROR

Age Income Deflator Exemption Taxes Savings Cumulative Savings rConsumption

30 50,000 1.00 10,000 8,000 6,300 6,300 35,700

31 53,500 1.03 10,300 8,640 6,793 13,534 36,958

35 70,128 1.16 11,593 11,764 9,370 54,231 42,262

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement Years Income Growth Rate of Inflation Exemption Now Tax Rates in Saving Rate ROR rROR

Age Income Deflator Exemption Taxes Savings Cumulative Savings rConsumption

30 50,000 1.00 10,000 8,000 6,300 6,300 35,700

31 53,500 1.02 10,200 8,660 7,143 13,821 36,958

14. When deferring taxes to the last year of retirement, you must set money aside

every year in order to accumulate a fund sufficient to pay the capital gains tax in a

lump sum. To leave consumption fixed in real terms, a fixed real amount is set

aside each year.

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement

Years

Income

Growth

Rate of

Inflation

Exemption

Now

Tax Rates in Saving Rate ROR rROR

25 0.07 0.03 10000 Table 21.1 0.15 0.06 0.0291

Age Income Deflator Exemption Taxes Savings

Cumulative Savings

rConsumption

30 50,000 1.00 10,000 8,000 6,300 6,300 35,700

35 70,128 1.16 11,593 11,764 9,370 52,995 42,262

45 137,952 1.56 15,580 28,922 19,707 278,528 57,333

15. Answers will vary.

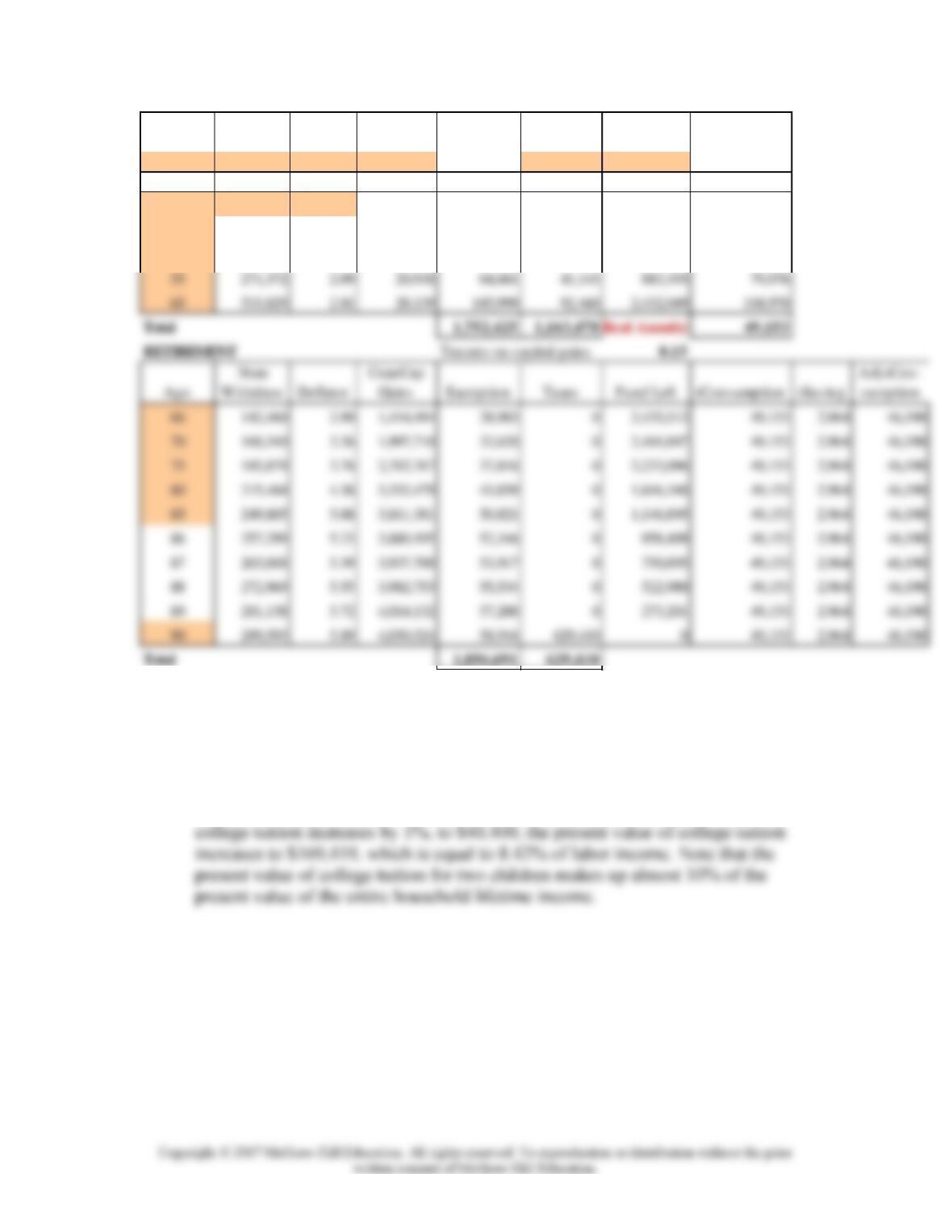

16. The present value of labor income is $ 2,010,917 (at the rate of the applicable

ROR). The present value of college tuition is $167,741. This is equal to:

($167,741/$2,010,917) = 8.34% of the present value of labor income. When

Chapter 21 - Taxes, Inflation, and Investment Strategy

Retirement Years

Income Growth Rate of Inflation Savings Rate ROR rROR Extra-Cons

Age Income Deflator Saving Cumulative Savings rConsumption Expenditures

30 50,000 1.00 7,500 7,500 42,500 0

31 53,500 1.03 8,025 15,975 44,150 0

35 70,128 1.16 10,519 61,658 51,419 0

45 137,952 1.56 20,693 308,859 75,264 0

48 168,997 1.70 25,349 375,099 84,378 68,097

Retirement Years Income Growth Rate of Inflation Savings Rate ROR rROR Extra-Cons

25 0.07 0.03 0.15 0.06 0.0291 40,400

Age Income Deflator Saving Cumulative Savings rConsumption Expenditures

30 50,000 1.00 7,500 7,500 42,500 0

31 53,500 1.03 8,025 15,975 44,150 0

35 70,128 1.16 10,519 61,658 51,419 0

17. Adverse selection is a concept that is generally associated with insurance; however,

in a broader sense, adverse selection is a potential issue in any contract where one

party has more complete information about the transaction than the other. In

insurance, the insured has more information about one’s own health (e.g., in life

insurance and health insurance) or, in general, the risk of loss (e.g., one’s driving

19. In general, moral hazard is a term associated with insurance contracts and with

government programs that essentially function as insurance. When an individual

or a business entity insures against loss of property due to fire, theft or other

hazard, the insured may have a tendency to take greater risks than one would in