Chapter 19 – Globalization and International Investing

CHAPTER NINETEEN

GLOBALIZATION AND INTERNATIONAL INVESTING

CHAPTER OVERVIEW

This chapter notes that the United States offers a relatively small portion of the entire assets

available for investment purposes. In addition, the benefits of increased diversification as a result

of international investing are presented. International indexes are available for passive investing

purposes. Although exchange rate risk is present in international investing, exchange rate futures

allow a much of this risk to be hedged. This edition has a plethora of updated results concerning

the efficacy of passive international diversification. The results indicate that the benefits of

internationally diversifying are declining and are now rather modest. Moreover, the recent

financial crisis show once more that correlations increase in a market panic and it is very difficult

if not impossible to diversify away from U.S. market crash.

LEARNING OBJECTIVES

After studying this chapter, the student should understand the potential and real advantages of

international diversification, and be able to devise hedge strategies to offset currency risk involved

in international investing. The student should have a basic idea of how to decompose investment

returns into contributing factors such as country, currency, and stock selections.

CHAPTER OUTLINE

1. Global Markets for Equities

PPT 19-2 through PPT 19-6

This section presents some background and focuses on growth in international investing and

begins exploring the tie between market capitalization and growth. The growth of international

2. Risk Factors in International Investing

PPT 19-7 through PPT 19-20

One of the key elements of risk that is presented in the chapter is foreign exchange risk. It is not

possible to completely hedge for foreign exchange risk for equities because the returns that an

investor gets in foreign markets are not completely predictable. The emphasis on the material in

19–1

0

1

E

E

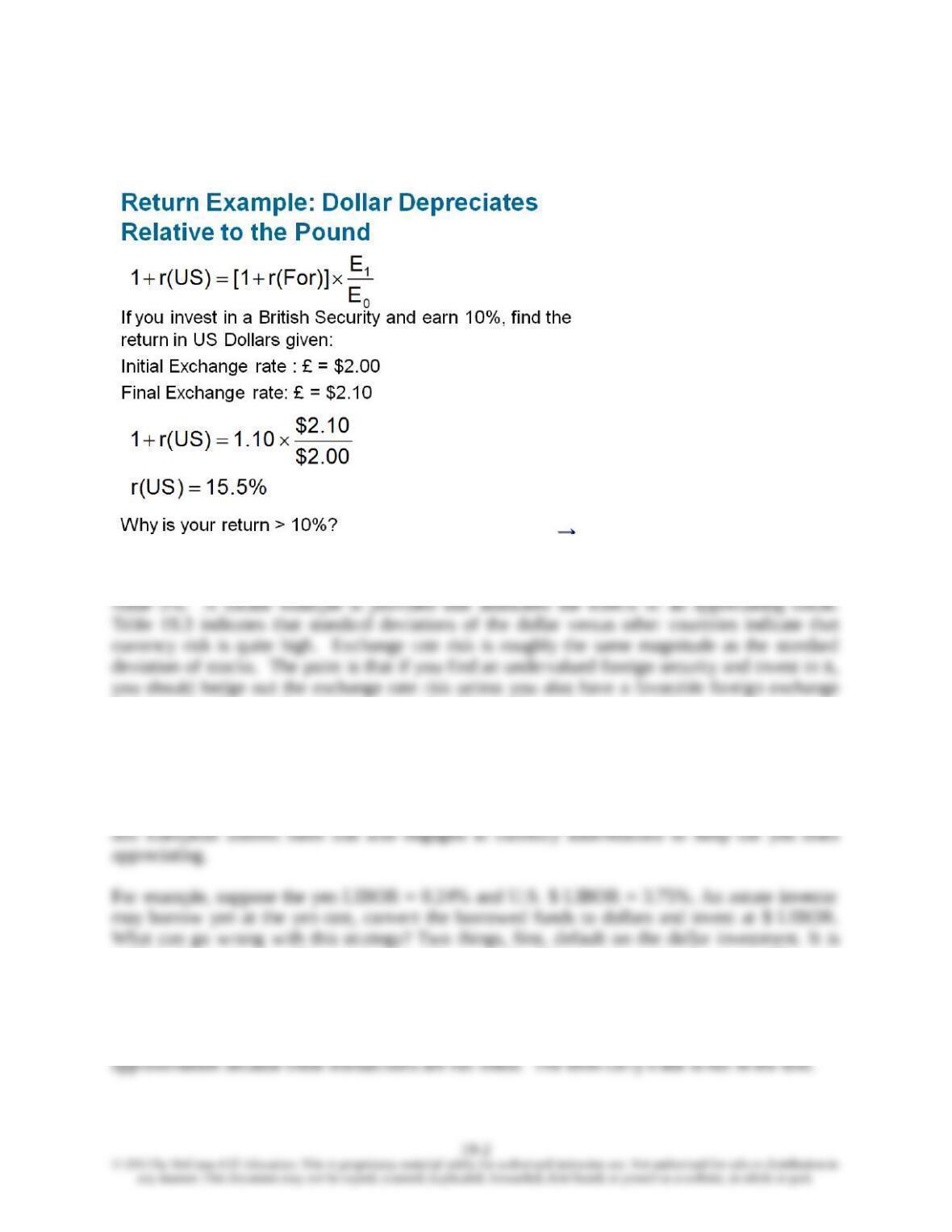

r(For)][1r(US)1

Chapter 19 – Globalization and International Investing

A simple example illustrates this point:

The return is better because while the investor held the British investment, the pound increased in

forecast. In other words active managers should consider exchange rate risk.

Figure 19.2 displays information on how actual security returns for US investors have been

impacted by foreign exchange rates. Exchange rate movements have material affects on dollar

returns in some countries. The Carry Trade

The carry trade was very popular for a few years when Japan kept interest rates lower than U.S

unlikely that investors will invest in very risky assets for this type transaction however. The main

risk is that the yen increases in value by 3.75% – 0.24% = 3.51% or more. Even individual

investors in Japan were exploiting this risky arbitrage opportunity and many were hurt when the

yen rose during the financial crisis as for a time investors believed the yen was safer than the

dollar. The weakening of Japan’s economy in 2009 brought the yen back down. The 3.51% is an

The covered interest parity formula presents the no arbitrage condition required to eliminate

covered interest arbitrage:

Covered interest parity formula

transaction makes the process more transparent. This strategy works because the currency %

change is ($1.95 – $2.00) / $2.00 = -2.5% (pound depreciation) is not enough to offset the higher

British interest rate. In doing so one gains 10% – 6.15% = 3.85% on the interest rates and one

loses on 2.5% on the currency depreciation. It is riskless if steps 3 and 4 can be done

simultaneously. This is a violation of covered interest parity and it should not persist. Borrowing

countries from 0 (most risky) to 100 (least risky) are provided. Variables that are used in the

political risk scores are shown. Current ratings and the breakdown of political, financial and

economic risk scores are presented.

3. International Investing: Risk, Return, and Benefits from Diversification

PPT 19-21 through PPT 19-39

19–3

0

1

E

F

r(For)1

r(US)1

Chapter 19 – Globalization and International Investing

Funds labeled “World” usually include U.S. investments; those labeled “International” exclude

U.S. investments. WEBS are low cost tradable investment alternatives that track performance in

an index in a country or region.

Several important questions concerning international investments are addressed in the text. The

central questions asked are;

standard deviation. The figure reveals imperfect correlations between standard deviation and beta.

The evidence of lower betas indicates that there may be diversification benefits from including

international investments into a U.S. portfolio. Are average returns higher in emerging markets?

Figure 19.5 indicates that Emerging markets generally have higher excess returns. Since some

had returns below the risk free rate we can reaffirm that risky returns may fall short of

Hedging currency risk can materially affect returns, particularly if a currency is over or

undervalued against many other currencies. The choice to hedge or not now becomes one of the

decision variables for an active manager but a well diversified passive portfolio may not need to

hedge.

Are there significant benefits to international diversification?

19.10, Hedged & Unhedged Correlations, indicate that international diversification benefits will be

19.13 and 19.14A contain the efficient frontier for two different levels of expected excess returns

consistent with historical results. Changing the expected excess return by varying the expected

excess return makes the slope of the CML larger because a higher excess return simply shifts the

curve upward. This graph also indicates only modest benefits from international diversification

from including developed markets.

19–4

several studies as well. If this is so then diversification fails just when you need it most. This was

certainly true for the hedge fund Long Term Capital Management.

Conclusions:

A passive investment in all countries would not have lowered risk at all during the recent

crisis. This isn’t particularly surprising. We have always known that you could not

Hedging currencies has little effect either.

A U.S. stock market crash appears to be a systemic factor that cannot be diversified away

from in a crisis. (See the first bullet in this list.)

Correlations are on the increase due to globalization; nevertheless we still expect modest

international diversification benefits in normal markets.

Second level:

Optimize allocations across country portfolios to maximize diversification.

4. International Investing and Performance Attribution

PPT 19-40 through PPT 19-41

When assessing the performance of managers of international investment portfolios variations in

performance attribution discussed in Chapter 18 can be used:

An Excel model that allows a student to construct an efficient frontier for international

investments is available. It demonstrates the potential benefits of diversification.

19–6