Chapter 16 – Option Valuation

CHAPTER SIXTEEN

OPTION VALUATION

CHAPTER OVERVIEW

This chapter discusses factors affecting the value of an option and presents analytical and

spreadsheet models of option pricing. Put call parity is introduced, manipulating hedge ratios and

portfolio insurance techniques are also presented.

LEARNING OBJECTIVES

After studying this chapter, the student should be able to identify the characteristics that determine

an option’s value and should understand how different values for these variables affect option

prices. The reader should be able to calculate option prices in a two state world (via a simplified

binomial model) and should know how to calculate Black-Scholes put and call option values when

there is no early exercise. Students should be able to calculate put prices from put call parity and

know how to arbitrage a mispriced option. The chapter demonstrates how to calculate the hedge

ratio for an option and students should have a basic understanding of portfolio insurance.

CHAPTER OUTLINE

1. Option Valuation: Introduction

PPT 16-2 through PPT 16-5

When describing options, intrinsic value refers to the value if the option were immediately

helped students understand basic option strategy payoffs. A review is provided below:

Ct = Price paid for a call option at time t. t = 0 is today,

T = Immediately before the option‘s expiration.

Pt = Price paid for a put option at time t.

St = Stock price at time t.

X = Exercise or Strike Price (X or E)

Chapter 16 – Option Valuation

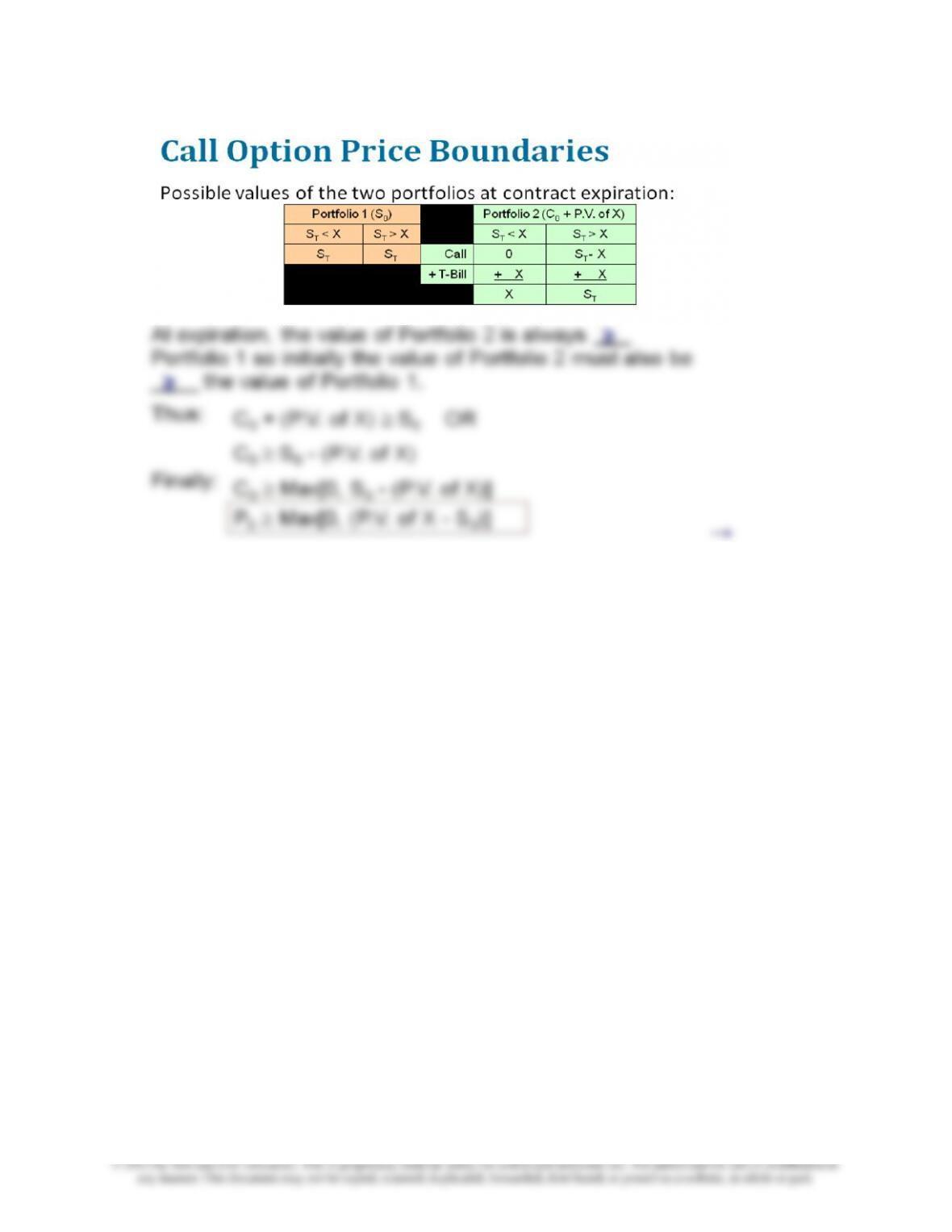

From here we can present the value of a call option at expiration and prior to expiration as

follows:

16–2

(Writing an option will be a + Theta position.) Going long or buying an option is a play that the

price will move enough before you run out of time value.

The time value of a call incorporates the probability that S will be in the money at period T given

S0, time to T, s2stock ,X, and the level of interest rates. The benefit of time value is the chance

that the option will wind up further in the money. Of course, it might not wind up further in the

receive the dividend. If the dividend is greater than the time value on the call, you would want to

early exercise right before the stock went ex-dividend.

2. Binomial Option Pricing

PPT 16-6 through PPT 16-12

A binomial pricing example is developed in the PPT. The example assumes the stock is currently

priced at $100 and will have a value of either $115or $85 at the end of the period. A call that has

Time value of the call = $ 8.94

While the two-state approach is simplistic, the approach is easily generalized. Expansion of the

two-state approach shows how the probability distributions will approach the familiar bell shaped

curve as the number sub-periods increases.

3. Black-Scholes Option Valuation

PPT 16-13 through PPT 16-24

16–4

T = Time until expiration (not a point in time) in years,

σ = Annual standard deviation of continuously compounded stock returns

N(d) = probability that a random draw from a normal distribution will be less than d.

Including the annual dividend yield is an approximation of a discrete payment, (also technically the

dividend can’t be stochastic). It assumes no early exercise due to the dividend.

E(r) = (r + σ2/2)T when returns are lognormally distributed1

Ln (S0 / X) measures the continuous return needed for the stock to finish in the money

Roughly speaking the d1 numerator is a measure of the return needed to finish in the

money, the denominator measures this relative to the standard deviation of the returns.

N(d) is cumulative normal probability. It can be calculated in Excel using the

model:

1The non continuously compounded returns are lognormally distributed. When we convert them to continuously compounded

returns rcont = Ln(1+rsimple), the rcont are normally distributed. If you have simple stock return series for monthly data or

shorter, you don’t need to do the conversion to continuous compounding because they will give you approximately the same

numbers (albeit this is a rule of thumb heuristic).

16–5

the probability that the option will wind up (deeper) in the money by expiration. Higher volatility

also indicates that the stock may not wind up in the money even if it currently is. However, due

to the asymmetric nature of options (one don’t use them if they don’t help) volatility increases

value. An extreme example might help here. Suppose one has a stock priced at $30 and a call

option on the stock with an exercise price of $50. Would one pay more for the option if the

value. Likewise since the option is the right to buy at the fixed value X, a higher S results in a

higher call value. Note that X would change if a stock split or stock dividend occurred, but not

otherwise. For instance, in a 2 for 1 stock split the exercise price would be halved. No adjustment

is made to X for a cash dividend.

As noted previously, a call option should not be exercised prior to maturity unless a stock is about

decline in stock price, and in such cases early exercise is desirable.

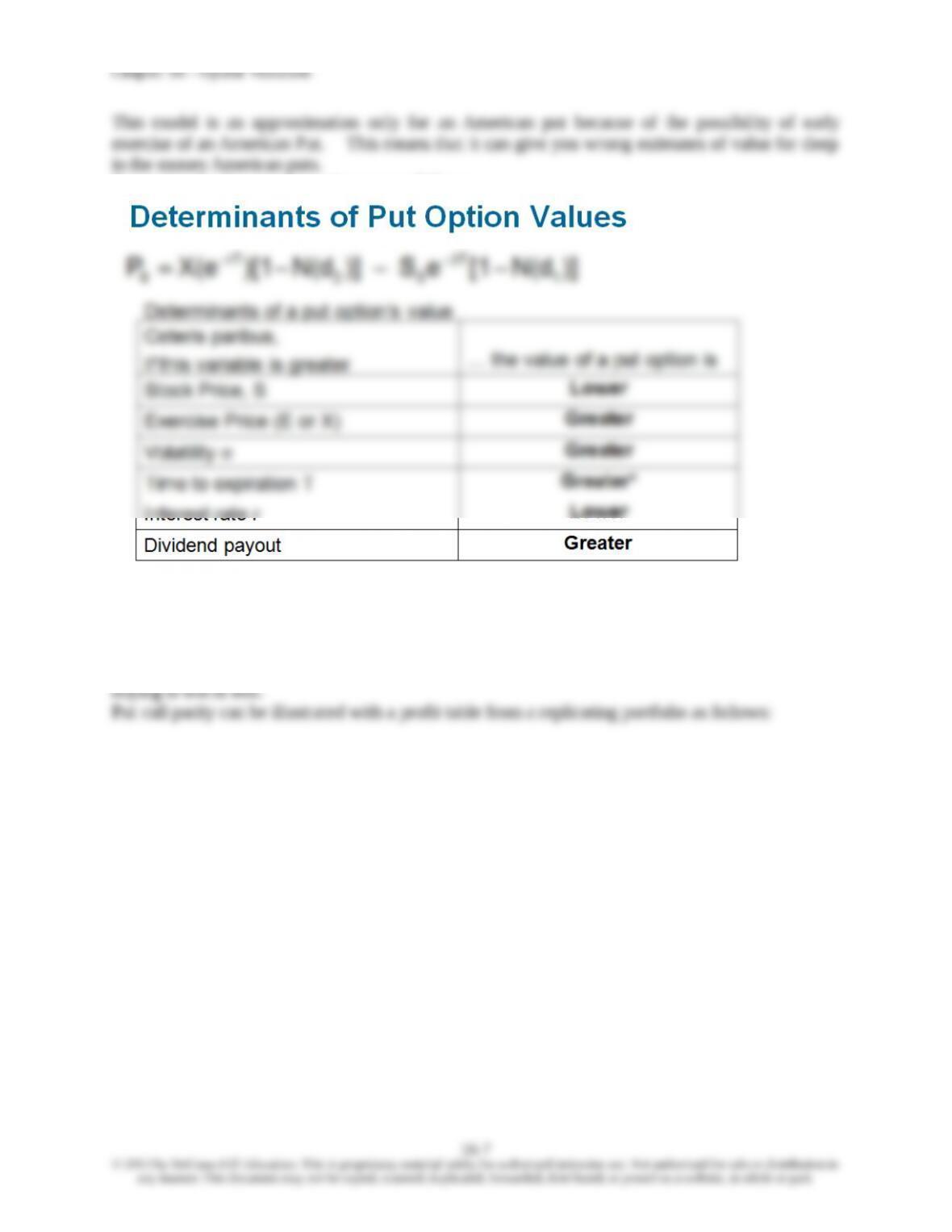

A version of the BS model is available for puts:

16–6

)]N(d [1eS )]N(d)[1X(e P 1

T

02

rT

0

Determinants of put option values are as follows:

The interest rate variable probably requires some explanation. A higher interest rate lowers the PV

of X, thereby lowering the put value. In concept, the most you can get from a put is X, and the

lower the PV of X the lower the value of the put. Buying a put is conceptually equivalent to

shorting the stock and investing the proceeds in X. With a higher interest rate the bond one is

This combination will always result in a zero payoff at expiration so its initial cost must be zero as

well. This establishes the time zero value of 0 = C0-P0-S0 + X(e-rT). Knowing the call value and

the other variables one can find the implied put value. Using the BS model for puts will give the

same value. Both are correct only for European puts if there is a possibility of early exercise.

4. Using the Black-Scholes Formula

PPT 16-25 through PPT 16-32

The BS hedge ratio H can be found for a call option on a non-dividend paying stock as:

0. The sensitivity of a position’s value to a change in stock price is sometimes called the position’s

Delta.

If the position is not affected by a change in stock price the position has a delta of zero and is said

to be delta neutral.

If a position increases in value when stock price increases (and vice versa) it is positive

)d(N

S

C

H 1

0

0

Chapter 16 – Option Valuation

The position delta can be strategically manipulated as market conditions change and this idea is

the basis for portfolio insurance strategies accomplished through dynamic hedging. The basic

concept of portfolio insurance involves the purchase of protective puts. Purchase of protective

puts is a relatively easy concept but there are some limitations to the implementation of portfolio

option price per 1% change in stock price would not be atypical. Further out of the money

options have greater elasticity, deep out options may have elasticities of 25% or more. Deep in

the money options may have elasticities as low as 2-3% but they have to be deep in.

The stock’s standard deviation is the one variable in the BS model that is not easily observable.

The BS model can be used to find the implied volatility of the underlying stock, IF one is willing

5. Empirical Evidence

PPT 33

The B-S model has been heavily tested with the general conclusion that the model generates

option values that are very close to actual market prices. However, there are some problems with