Chapter 15 – Options Markets

1.

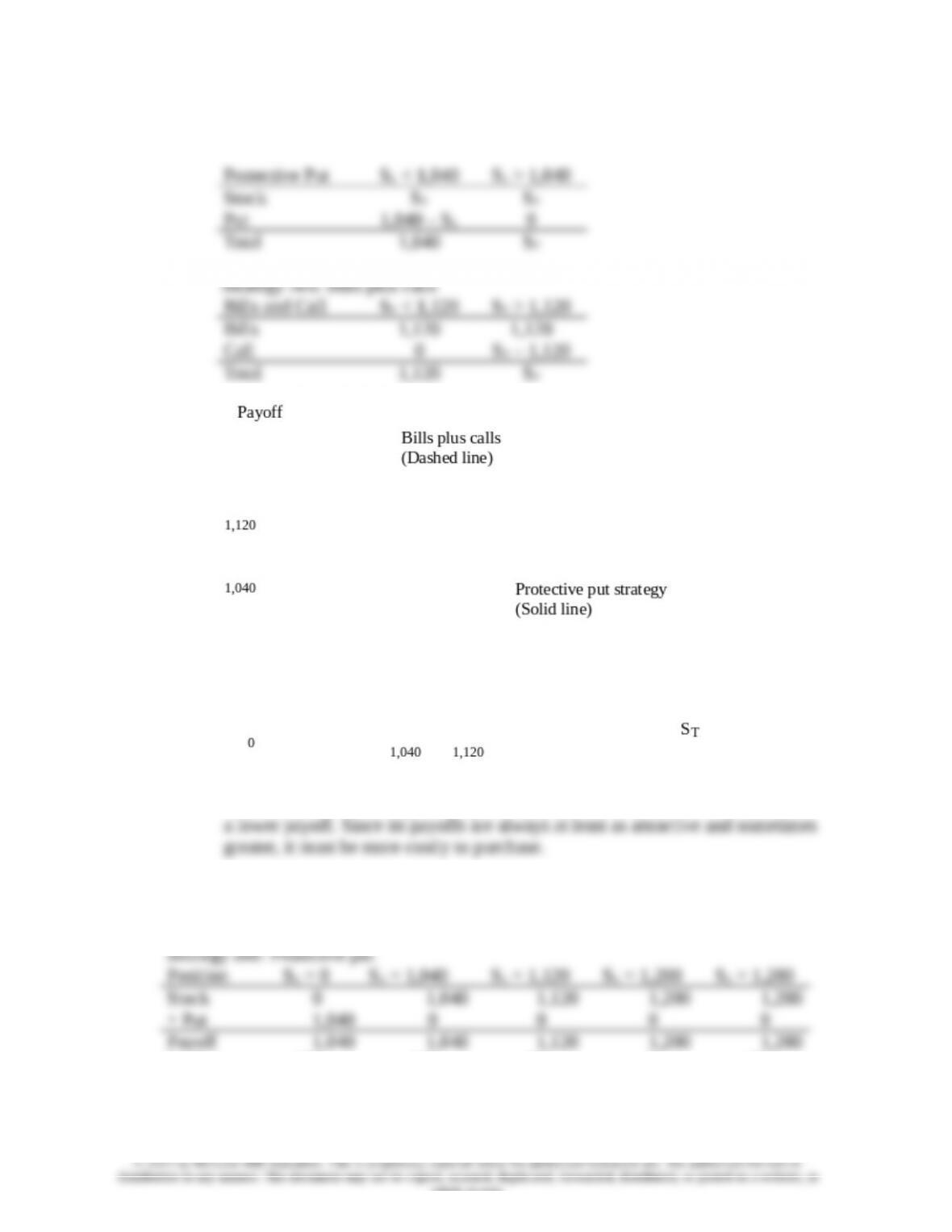

a. Strategy one: Protective put

b. The bills plus call strategy has a greater payoff for some values of ST and never

c. The initial cost of the stock plus put position is $1,208 and the cost of the bills

plus call position is $1,240.

Profit –168 –168 –88 –8 +72

*Profit = Payoff – Initial Outlay = Payoff – $1,208

15-1

whole or part.

Payoff 1,120 1,120 1,120 1,200 1,280

Profit –120 –120 –120 –40 +40

*Profit = Payoff – Initial Outlay = Payoff – $1,240

d. The stock and put strategy is riskier. It does worse when the market is down,

and better when the market is up. Therefore, its beta is higher.

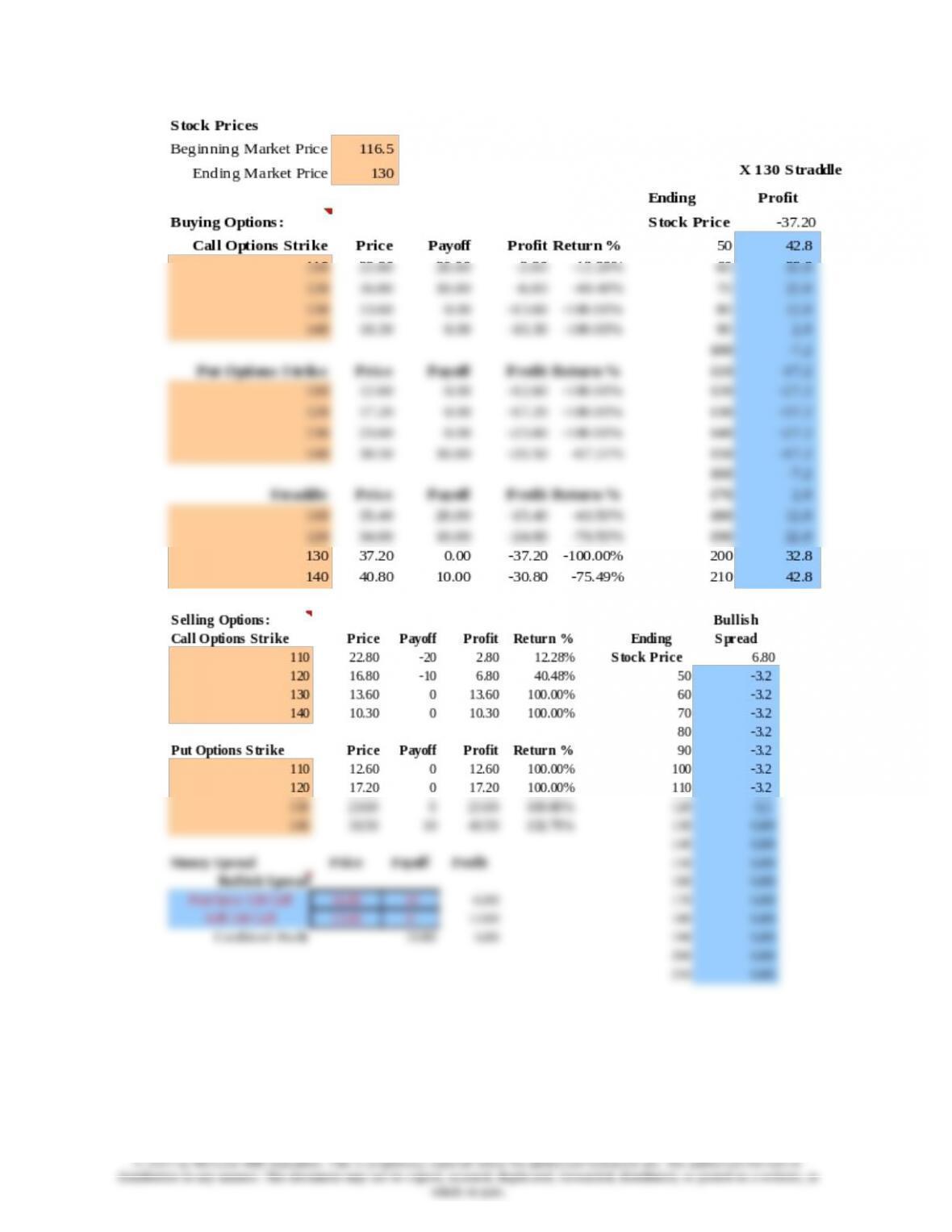

2. The Excel spreadsheet for both parts (a) and (b) is shown on the next page, and the

profit diagrams are on the following page.

a. & b.

15-2

Chapter 15 – Options Markets

15-3

15-4

Chapter 15 – Options Markets

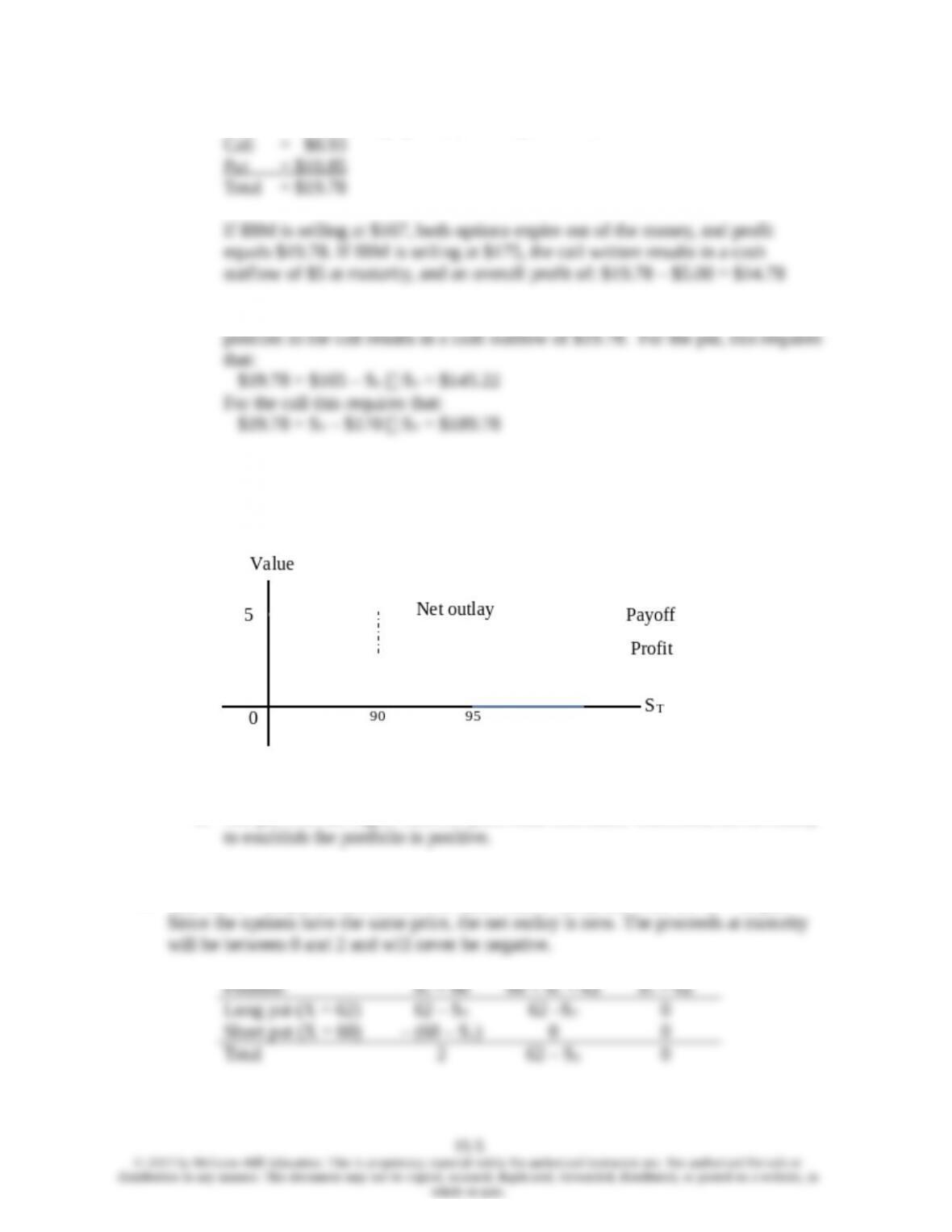

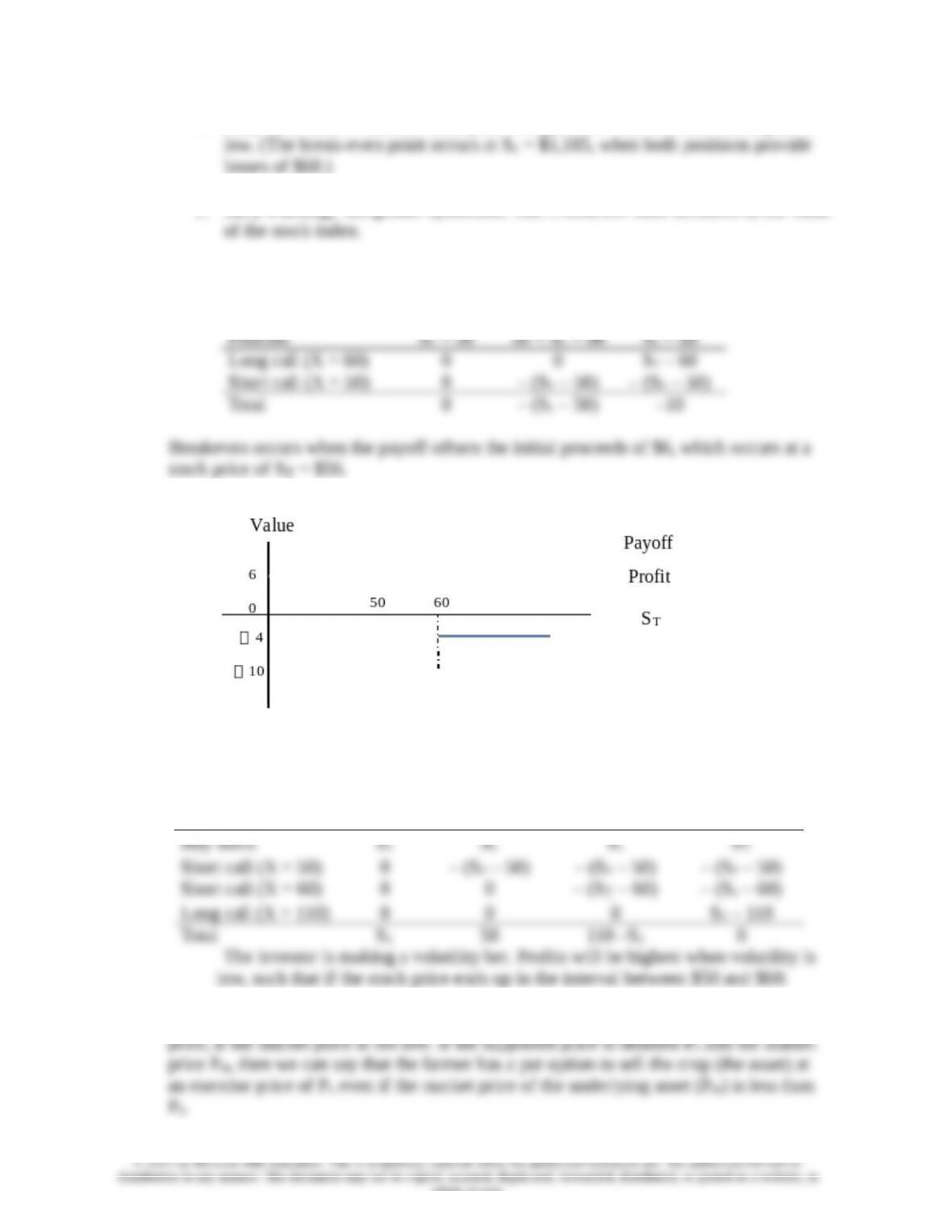

b. Proceeds from writing options (from Figure 15.1):

c. You will break even when either the short position in the put or the short

d. The investor is betting that the IBM stock price will have low volatility.

6.

a.

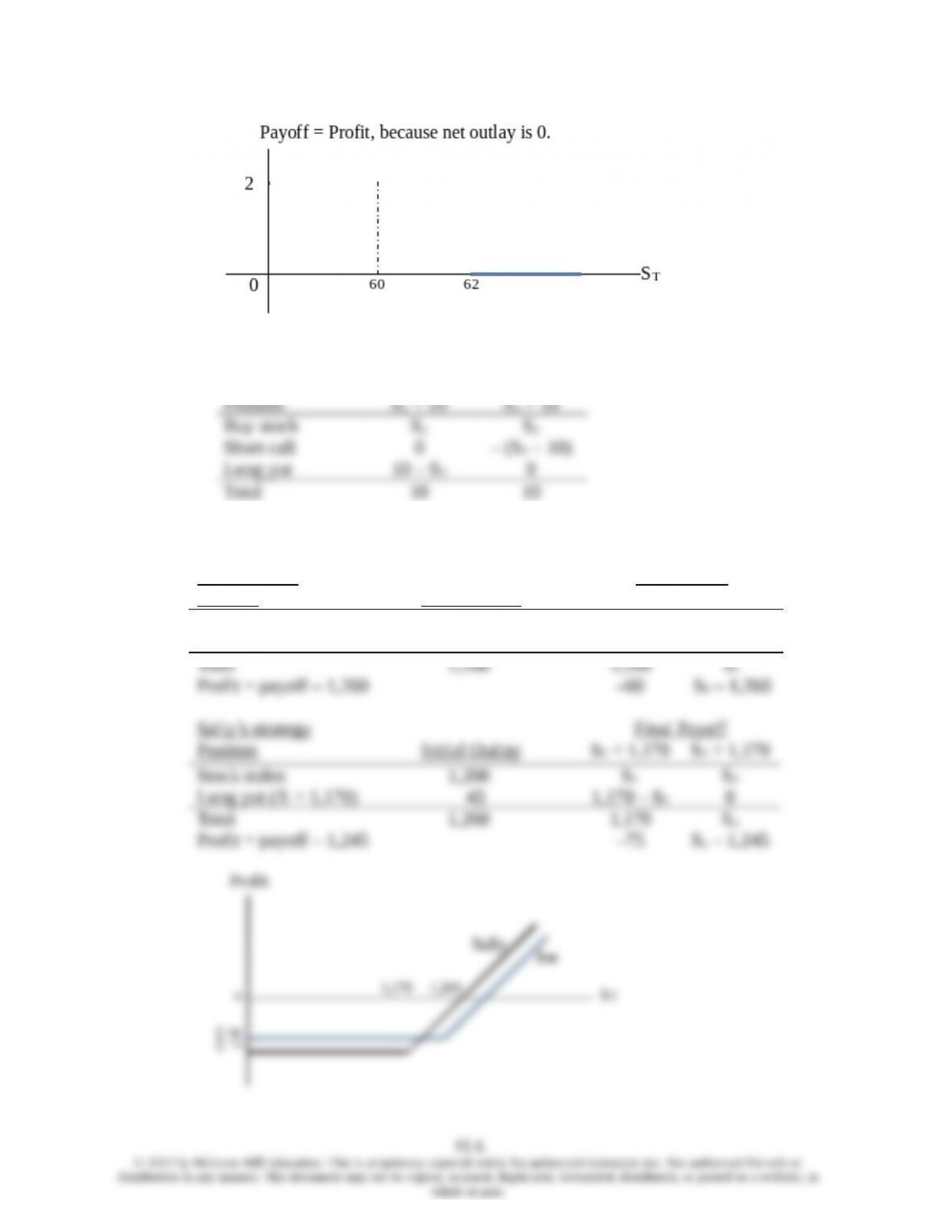

7. Buy the X = 62 put (which should cost more than it does) and write the X = 60 put.

Chapter 15 – Options Markets

8. The following payoff table shows that the portfolio is riskless with time-T value equal

to $10. Therefore, the risk-free rate is: ($10/$9.50) – 1 = .0526 = 5.26%

9.

a.

Joe’s strategy Final Payoff

Position Initial Outlay ST < 1200 ST > 1200

Stock index

1,200

ST

ST

Long put (X = 1,200) 60 1,200 – ST0

Total

1,260

1,200

ST

Stock index

1,200

ST

ST

Long put (X = 1,170) 45 1,170 – ST0

Total

1,260

1,170

ST

Profit = payoff – 1,245 –75 ST – 1,245

15-6

© 2013 by McGraw-Hill Education. This is proprietary material solely for authorized instructor use. Not authorized for sale or

distribution in any manner. This document may not be copied, scanned, duplicated, forwarded, distributed, or posted on a website, in

whole or part.

Chapter 15 – Options Markets

b. Sally does better when the stock price is high, but worse when the stock price is

10. This strategy is a bearish spread. The initial proceeds are: $9 – $3 = $6

The payoff is either negative or zero:

11. Buy a share of stock, write a call with X = 50, write a call with X = 60, and buy a call with

X = 110.

Position ST < 50 50 < ST < 60 60 < ST < 110 ST > 110

12. The farmer has the option to sell the crop to the government, for a guaranteed minimum

15-7

whole or part.

Chapter 15 – Options Markets

CFA 1

CFA 2

Answer:

a. Donie should choose the long strangle strategy. A long strangle option strategy

iii. The breakeven prices are $46.00 and $69.00. The put will just cover costs if

CFA 3

Answer:

a. If an investor buys a call option and writes a put option on a T-bond, then, at

b. Such a position would increase the portfolio duration, just as adding a T-bond

c. Futures can be bought and sold very cheaply and quickly. They give the manager

15-8

whole or part.

Chapter 15 – Options Markets

CFA 4

Answer:

a. Conversion value of a convertible bond is the value of the security if it is

CFA 5

Answer:

a. i. The current market conversion price is computed as follows:

ii. The expected one-year return for the Ytel convertible bond is:

iii. The expected one-year return for the Ytel common equity is:

b. The two components of a convertible bond’s value are:

i. In response to the increase in Ytel’s common equity price, the straight bond value

should stay the same and the option value should increase.

15-9

Chapter 15 – Options Markets

ii. In response to the increase in interest rates, the straight bond value should

15-10