Chapter 13 – Equity Valuation

CHAPTER 13

EQUITY VALUATION

1. Theoretically, dividend discount models can be used to value the stock of rapidly

growing companies that do not currently pay dividends; in this scenario, we would be

2. It is most important to use multi-stage dividend discount models when valuing

companies with temporarily high growth rates. These companies tend to be companies

3. The intrinsic value of a share of stock is the individual investor’s assessment of the true

worth of the stock. The market capitalization rate is the market consensus for the

4. Intrinsic value = V0 =

D1

1 + k

+

D2

(1 + k )2

+ … +

D H + P H

(1 + k )H

$1 × 1 .22 × 1.04

(0.0 85 - 0.0 4) × (1 + 0.0 85) 2

D 0× (1 + g )

k - g

D 0× (1 + g )

k - g

$1 × 1 .2

$1 × 1 .2 2

k - 0.0 5

7. Price = $41 =

E1

k

+ PVGO =

$3.64

0.0 9

+ PVGO PVGO = $0.56

8. Market value of the firm

= Market value of assets – Market value of debts

9. g = ROE b = 0.10 0.6 = 0.06 or 6%

1 - b

k - g

1 - 0.6

0.0 8 - 0.0 6

10. Market capitalization rate = k = rf + β [E(rM) – rf ]

D1

k - g

0. 10 - 0.0 4

11. Given EPS = $6, ROE = 15%, plowback ratio = 0.6, and k = 10%, we first calculate the

price with the constant dividend growth model:

D1

k - g

EPS × (1- b)

k - ROE × b

$ 6 × (1 - 0.6 )

0. 10 - 0.15 × 0.6

$ 2. 4

0. 10 - 0.0 9

= $240

Then, knowing that the price is equal to the price with no growth plus the present value

of the growth opportunity, we can solve the following equation:

k

0.10

E1

$6

12. FCFF = EBIT(1 – tc) + Depreciation – Capital expenditures – Increase in NWC

13. FCFE1 = FCFF – Interest expenses(1 – tc) + Increases in net debt

13-2

$1 × 1 .05

18. ROE = 20%, b = 0.3, EPS = $2, k = 12%

a. P/E Ratio

Chapter 13 – Equity Valuation

a. k = rf + β [E(rM) – rf ] = 0.06 + 1.25 (0.14 – 0.06) = 0.16 or 16%

k - g

0. 16 - 0.0 6

b. Leading P0/E1 = $10.60/$3.18 = 3.33

c. PVGO = P0 –

E1

k

= $10.60 –

$3.18

0. 16

= $9.28

d. Now, you revise the plowback ratio in the calculation so that b = 1/3:

D1

k - g

0. 16 - 0.03

V0 increases because the firm pays out more earnings instead of reinvesting

21. FI Corporation

D1

k - g

$8

0. 10 - 0.05

b. The dividend payout ratio is 8/12 = 2/3, so the plowback ratio is b = (1/3). The

implied value of ROE on future investments is found by solving as follows:

g = b ROE

0.05 = (1/3) ROE ROE = 15%

E1

k

$ 12

0. 10

22. Nogro Corporation

a. D1 = E1 (1 – b) = $2 0.5 = $1

13-5

D1

$1.06

23. Xyrong Corporation

a. k = rf + β [E(rM) – rf ] = 0.08 + 1.2 (0.15 – 0.08) = 0.164 or 16.4%

k - g

0. 164 - 0.12

b. P1 = V1 = V0 (1 + g) = $101.82 (1 + 0.12) = $114.04

D1 + P 1 - P 0

P 0

$4.48 + $114.04 - $100

$100

24.

Before-tax cash flow from operations $2,100,000

Depreciation 210,000

Taxable income 1,890,000

Taxes (@ 35%) 661,500

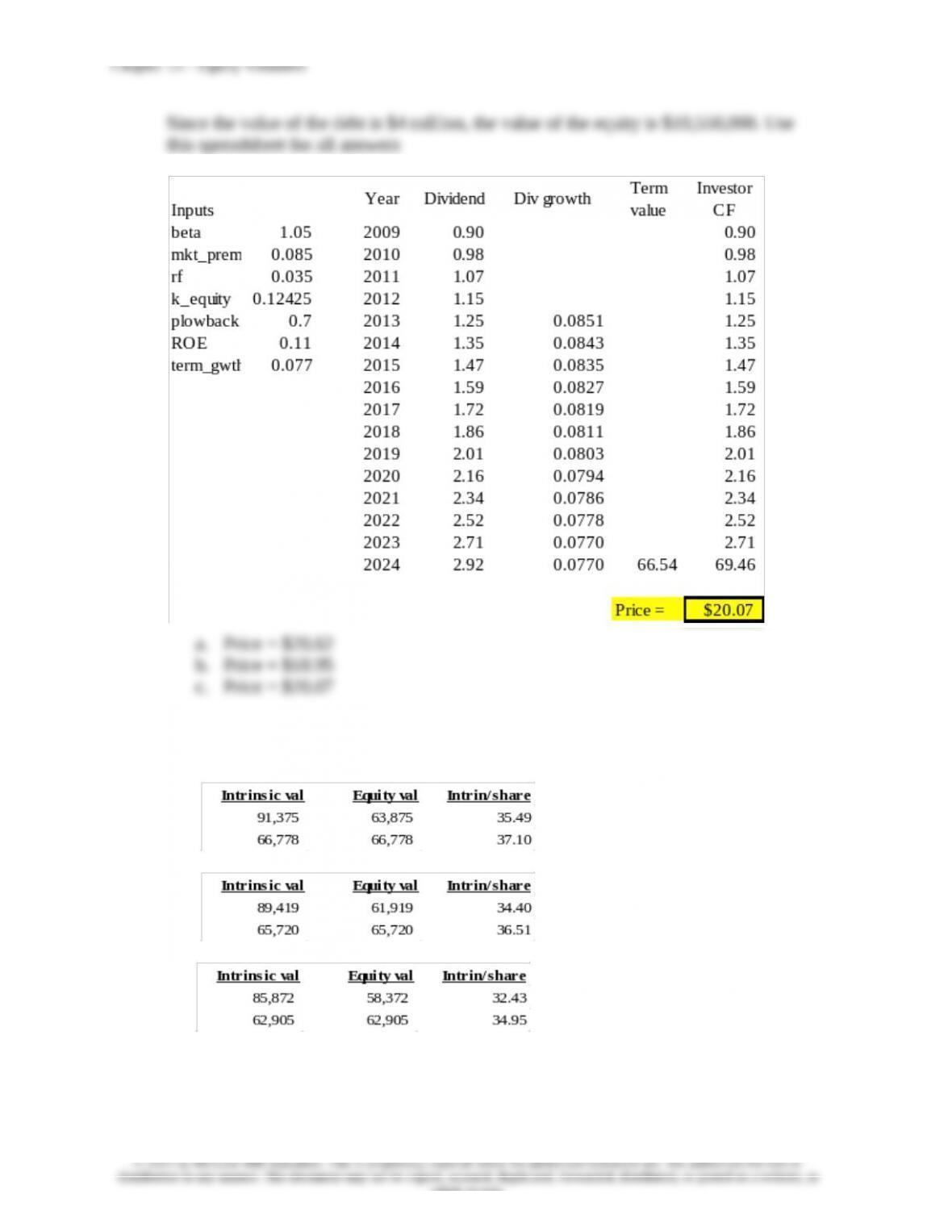

25. The solutions derived from Spreadsheet 13.2 are as follows:

a.

b.

c.

26.

a. g = ROE b = 0.20 0.5 = 0.10 or 10%

13-7

whole or part.

Chapter 13 – Equity Valuation

P0 =

D 0 × (1 + g)

k - g

=

$0.5 × (1 + 0.10)

0. 15 - 0.10

= $11

b.

Time EPS Dividend BVPS Comment

0

$1.0000

$0.5000

$5.5000

Book Value Per Share is $5.5.

1 $1.1000 $0.5500 $6.0500 g = 10%, plowback = 0.50

2 $1.2100 $0.7260 $6.5340

EPS has grown by 10% based on last year’s

earnings plowback and ROE; this year’s

earnings plowback ratio now falls to 0.40 and

payout ratio = 0.60

3 $0.9801 $0.5881 $6.9260

ROE has decrease to 15%, along with the

payout ratio of 0.6 gives the new growth rate of

15% (1 – 0.6) = 6% from next year.

c. P0 = $11 and P1 = P0 (1 + g) = $12.10

k - g

0. 15 - 0.06

k

k

Chapter 13 – Equity Valuation

a. This director is confused. In the context of the constant growth model, it is true

will not necessarily rise. In fact, if ROE > k, price will fall.

b. i. An increase in dividend payout reduces the sustainable growth rate as fewer

funds are reinvested in the firm.

CFA 2

Answer:

a. It is true that NewSoft sells at higher multiples of earnings and book value than

Capital. But this difference may be justified by NewSoft’s higher expected

b. The most important weakness of the constant-growth dividend discount model in

c. NewSoft should be valued using a multi-stage DDM, which allows for rapid

CFA 3

Answer:

a. The industry’s estimated P/E can be computed using the following model:

P0/E1 = payout ratio/(r g)

Therefore:

P0/E1 = 0.60/(0.12 0.10) = 30.0

13-9

whole or part.

Chapter 13 – Equity Valuation

b.

i. Forecast growth in real GDP would cause P/E ratios to be

generally higher for Country A. Higher expected growth in GDP implies

higher earnings growth and a higher P/E.

ii. Government bond yield would cause P/E ratios to be generally

higher for Country B. A lower government bond yield implies a lower risk-

free rate and therefore a higher P/E.

iii. Equity risk premium would cause P/E ratios to be generally

higher for Country B. A lower equity risk premium implies a lower

required return and a higher P/E.

CFA 4

Answer:

a. k = rf + β [E(rM) – rf ] = 0.045 + 1.15 (0.145 0.045) = 0.16 or 16%

b.

Present value of dividends paid in years 2011 to 2013:

c. The table presented in the problem indicates that QuickBrush is selling below

13-10

whole or part.

Chapter 13 – Equity Valuation

d. Strengths of two-stage DDM compared to constant growth DDM:

These inputs are difficult to measure.

13-11

whole or part.