Chapter 11 – Managing Bond Portfolios

1. Duration can be thought of as a weighted average of the ‘maturities’ of the cash flows

paid to holders of the perpetuity, where the weight for each cash flow is equal to the

3. An intermarket spread swap should work. The trade would be to long the corporate

4. Change in Price = – (Modified Duration Change in YTM) Price

=

−Macaulay’s Duration

1+ YTM

Change in YTM Price

1+ 0.0 6

5. d. None of the above.

6. The increase will be larger than the decrease in price.

7. While it is true that short-term rates are more volatile than long-term rates, the longer

duration of the longer-term bonds makes their rates of return more volatile. The higher

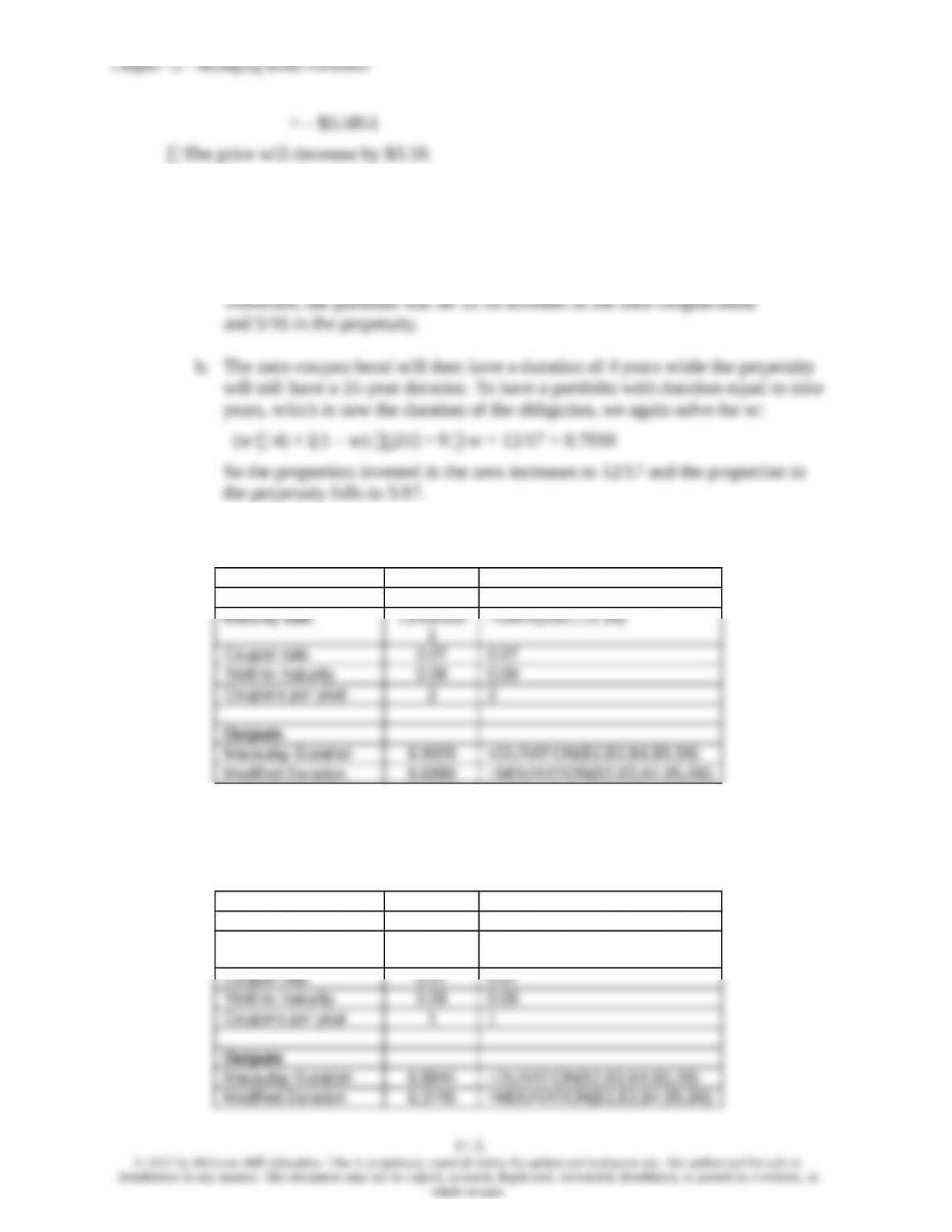

8. When YTM = 6%, the duration is 2.8334.

(1) (2) (3) (4) (5)

Time until

Payment

Payment

Payment

Discounted at

Weight

Column (1)

×

3 1060 796.39 0.8844 2.6531

Column Sum: 900.53 1.0000 2.8238

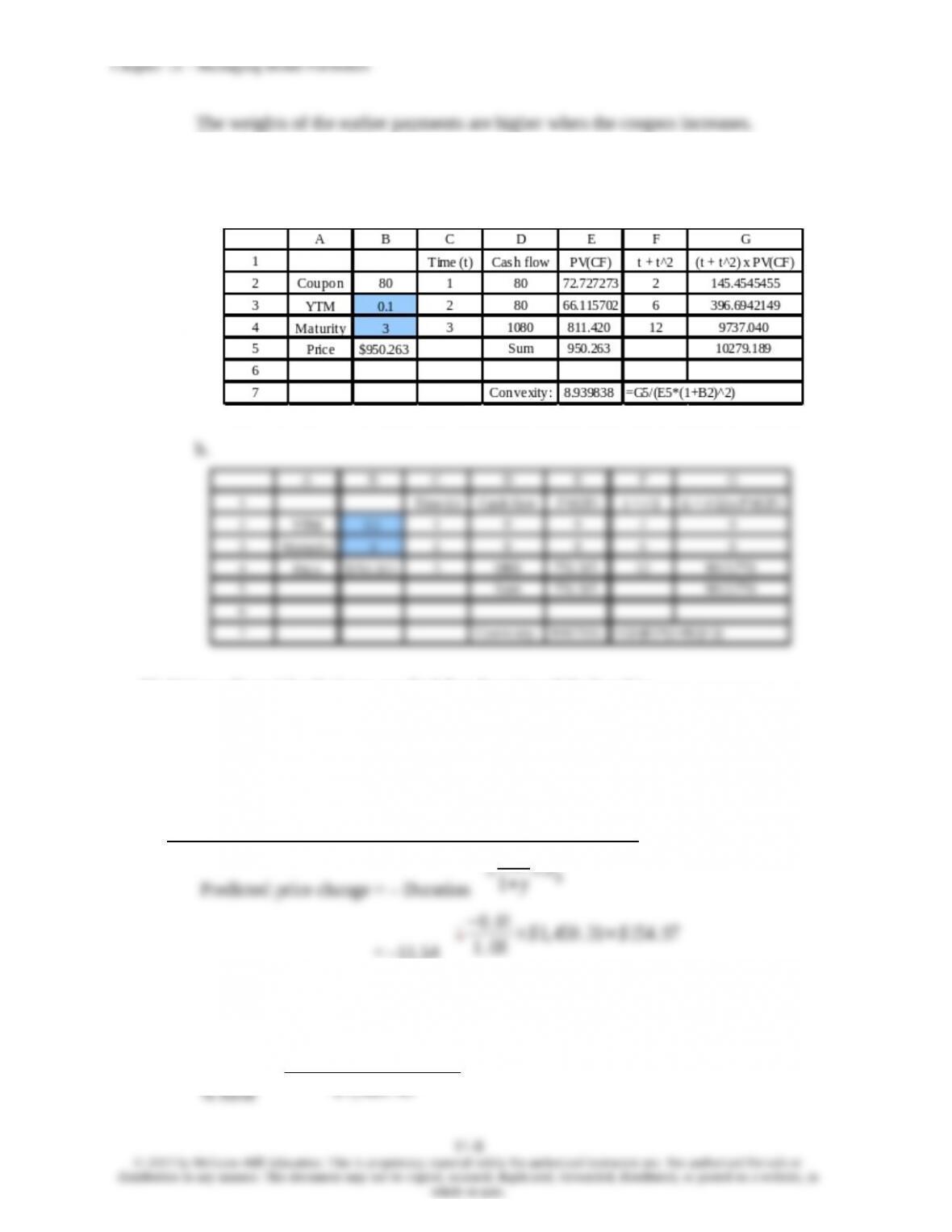

When the yield to maturity increases, the duration decreases.

9. Using Equation 11.2, the percentage change in the bond price is:

ΔP

P

= – Duration

Δy

1+y=−7 . 194×0 . 0050

1 .10 =−0 .0327

or a 3.27% decline

10. The computation of duration is as follows:

Interest Rate (YTM) is 10%.

(1) (2) (3) (4) (5)

11. The duration of the perpetuity is: (1 + y)/y = 1.10/0.10 = 11 years

Let w be the weight of the zero-coupon bond. Then we find w by solving:

12. Using Equation 11.2, the percentage change in the bond price will be:

11-2

13.

a. Bond B has a higher yield to maturity than bond A since its coupon payments and

maturity are equal to those of A, while its price is lower. (Perhaps the yield is higher

because of differences in credit risk.) Therefore, the duration of Bond B must be

14. Choose the longer-duration bond to benefit from a rate decrease.

a. The Aaa-rated bond has the lower yield to maturity and therefore the longer

15.

a. The present value of the obligation is $17,832.65 and the duration is 1.4808 years,

as shown in the following table:

Computation of duration, interest rate = 8%

(1) (2) (3) (4) (5)

Time until

Payment

Column (1)

11-3

Chapter 11 – Managing Bond Portfolios

$19 ,985 .26

(1. 09 )1. 4808 =$17 ,590 . 92

The present value of the tuition obligation would fall to $17,591.11, so that the net

position changes by $0.19.

If the interest rate falls to 7%, the zero-coupon bond would rise in value to:

$19 ,985 .26

(1. 07 )1. 4808 =$18 ,079 . 99

The present value of the tuition obligation would increase to $18,080.18, so that the

net position changes by $0.19.

The reason the net position changes at all is that, as the interest rate changes, so

does the duration of the stream of tuition payments.

16.

a. PV of obligation = $2 million/0.16 = $12.5 million

Duration of obligation = 1.16/0.16 = 7.25 years

0.5357 $12.5 = $6.7 million in the 5-year bond, and

0.4643 $12.5 = $5.8 million in the 20-year bond.

b. The price of the 20-year bond is:

[60 Annuity factor(16%, 20)] + [1000 PV factor(16%, 20)] = $407.1

17. a. Shorten his portfolio duration to decrease the sensitivity to the expected rate

increase.

18. Change in price = – (Modified duration Change in YTM) Price

= – 3.5851 0.01 $100

11-4

19.

a. The duration of the perpetuity is: 1.05/0.05 = 21 years

Let w be the weight of the zero-coupon bond, so that we find w by solving:

(w 5) + [(1 – w) 21] = 10 w = 11/16 = 0.6875

20. Macaulay Duration and Modified Duration are calculated using Excel as follows:

Inputs Formula in column B

Settlement date 5/27/2012 =DATE(2012,5,27)

21. Macaulay Duration and Modified Duration are calculated using Excel as follows:

Inputs Formula in column B

Settlement date 5/27/2012 =DATE(2012,5,27)

Maturity date 11/15/202

1

=DATE(2021,11,15)

first $70 is paid as follows: $35 on November 15, 2012 and $35 on May 15, 2013, so

the weighted average “maturity” of these payments is longer than the “maturity” of the

$70 payment on November 15, 2012 for the annual payment bond.

22.

a. The duration of the perpetuity is: 1.10/0.10 = 11 years

The present value of the payments is: $1 million/0.10 = $10 million

Let w be the weight of the five-year zero-coupon bond and therefore (1 – w) is

the weight of the twenty-year zero-coupon bond. Then we find w by solving:

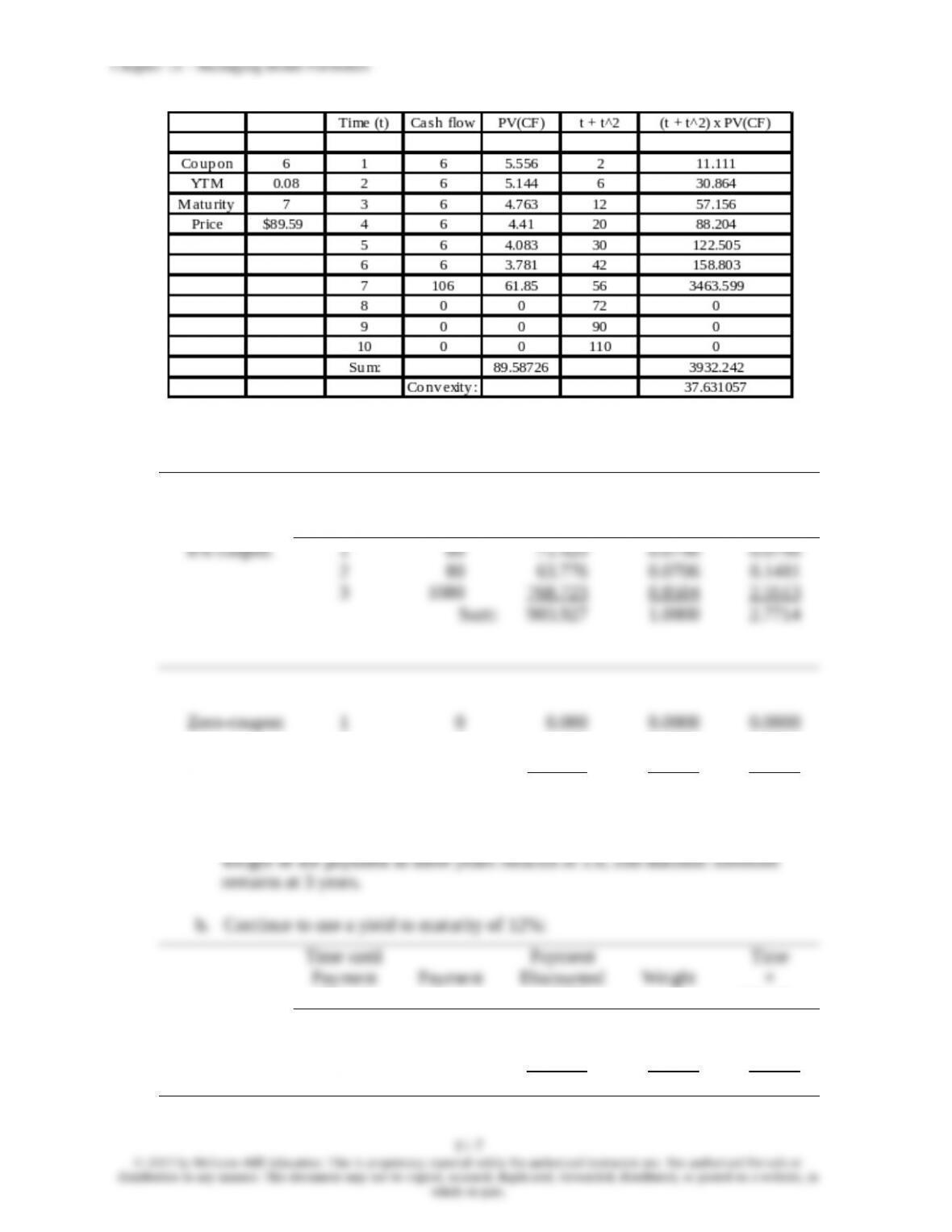

23. Convexity is calculated using the Excel spreadsheet below:

11-6

24.

a. Interest rate = 12%

Time until

Payment

(Years)

Payment

Payment

Discounted

at 12%

Weight

Time

×

Weight

2 0 0.000 0.0000 0.0000

3 1000 711.780 1.0000 3.0000

Sum: 711.780 1.0000 3.0000

At a higher discount rate, the weights of the later payments of the coupon bond

fall and those of the earlier payments rise. So duration falls. For the zero, the

(Years)

at 12%

Weight

12% coupon 1 120 107.143 0.1071 0.1071

2 120 95.663 0.0957 0.1913

3 1120 797.194 0.7972 2.3916

Sum: 1000.000 1.0000 2.6901

Therefore, duration falls.

25.

a.

26. Using a financial calculator, we find that the price of the bond is:

For yield to maturity of 7%: $1,620.45

For yield to maturity of 8%: $1,450.31

For yield to maturity of 9%: $1,308.21

Using the duration rule, assuming yield to maturity falls to 7%:

¿Δy

1+y×P0

Using the duration rule, assuming yield to maturity increases to 9%:

Predicted price change = – Duration

¿Δy

1+y×P0

¿+0 . 01

1 . 08 ×$1, 450. 31=−$154 . 97

Therefore: Predicted price = –$154.97 + $1,450.31 = $1,295.34

The actual price at a 9% yield to maturity is $1,308.21. Therefore:

% error

=$1,308 . 21−$1,295 . 34

$1, 308 .21 =0 . 0098=0. 98

Using the duration-with-convexity rule, assuming yield to maturity falls to 7%:

Predicted price change

[

(

1.08

)

]

= $168.92

Therefore: Predicted price = $168.92 + $1,450.31 = $1,619.23

The actual price at a 7% yield to maturity is $1,620.45. Therefore:

=$1,620 . 45−$1, 619 .23

$1, 620 . 45 =0. 00075=0 . 075

[

(

1.08

)

]

= –$141.02

Therefore: Predicted price = –$141.02 + $1,450.31 = $1,309.29

The actual price at a 9% yield to maturity is $1,308.21. Therefore:

11-9

27. You should buy the three-year bond because it will offer a 9% holding-period return

over the next year, which is greater than the return on either of the other bonds, as