Chapter 07: Current Asset Management

7-21

Then compute return on incremental investment.

$11,022 18.37%

$60,000 =

Yes, extend credit. 18.37% is greater than 10%.

21. Credit policy and return on investment (LO4) Global Services is considering a

promotional campaign that will increase annual credit sales by $400,000. The company

will require investments in accounts receivable, inventory, and plant and equipment. The

turnover for each is as follows:

Accounts receivable ……………………………..

4x

Inventory ……………………………………………

8x

Plant and equipment …………………………….

2x

All $400,000 of the sales will be collectible. However, collection costs will be 4 percent of

sales, and production and selling costs will be 76 percent of sales. The cost to carry

inventory will be 8 percent of inventory. Depreciation expense on plant and equipment will

be 5 percent of plant and equipment. The tax rate is 30 percent.

a. Compute the investments in accounts receivable, inventory, and plant and equipment

based on the turnover ratios. Add the three together.

b. Compute the accounts receivable collection costs and production and selling costs

and add the two figures together.

c. Compute the costs of carrying inventory.

d. Compute the depreciation expense on new plant and equipment.

e. Add together all the costs in parts b, c, and d.

f. Subtract the answer from part e from the sales figure of $400,000 to arrive at income

before taxes. Subtract taxes at a rate of 30 percent to arrive at income after taxes.

g. Divide the aftertax return figure in part f by the total investment figure in part a. If the

firm has a required return on investment of 12 percent, should it undertake the

promotional campaign described throughout this problem.

7-21. Solution:

Global Services

a. Accounts receivable = sales/accounts receivable turnover

Chapter 07: Current Asset Management

7-22

$100,000 $400,000/4=

Inventory = sales/inventory turnover

$50,000 $400,000/8=

Plant and equipment = sales/(plant and equipment turnover)

$200,000 400,000

$ / 2

=

$350,000 total investment

7-21. (Continued)

b. Collection cost = 4% × $400,000 $ 16,000

Production and selling costs = 76% × $400,000 = 304,000

Total costs related to accounts receivable $320,000

c. Cost of carrying inventory

Chapter 07: Current Asset Management

7-23

Taxes (30%) 19,800

Income after taxes $ 46,200

g.

Income after taxes $46,200 13.2%

Total investment 350,000

==

Yes, it should undertake the campaign.

The aftertax return of 13.2% exceeds the required rate of

return of 12%.

22. Continuation of Problem (LO4) In Problem 21, if inventory turnover had only been 4 times:

a. What would be the new value for inventory investment?

b. What would be the return on investment? You need to recompute the total investment

Should the campaign be undertaken?

7-22. Solution:

Global Services (Continued)

a. Inventory = sales/inventory turnover

$100,000 = $400,000/4

b. New Total Investment

Accounts receivable $100,000

Total Cost of the Campaign

Cost of carrying inventory

Chapter 07: Current Asset Management

New Income After Taxes

Sales $400,000

– total costs 342,000 ($334,000 + $8,000

(Problems 23-26 are a series and should be taken in order.)

23. Credit policy decision with changing variables (LO4) Dome Metals has credit sales of

$144,000 yearly with credit terms of net 30 days, which is also the average collection

period. Dome does not offer a discount for early payment, so its customers take the full 30

days to pay. What is the average receivables balance? Receivables turnover?

7-23. Solution:

Dome Metals

Sales/360 days = average daily sales

$144,000/360 = $400

Chapter 07: Current Asset Management

7-25

24. If Dome offered a 2 percent discount for payment in 10 days and every customer took

advantage of the new terms, what would the new average receivables balance be? Use the

full sales of $144,000 for your calculation of receivables.

7-24. Solution:

25. If Dome reduces its bank loans, which cost 10 percent, by the cash generated from its

reduced receivables, what will be the net gain or loss to the firm (don’t forget the 2

percent)? Should it offer the discount?

7-25. Solution:

Old receivables – new receivables = Funds freed by

with discount discount

$12,000 – $4,000 = $8,000 discount

26. Assume that the new trade terms of 2/10, net 30 will increase sales by 15 percent because

the discount makes the Dome’s price competitive. If Dome earns 20 percent on sales before

discounts, should it offer the discount? (Consider the same variables as you did for

problems 23 through 25 as will as increase sales.)

7-26. Solution:

Chapter 07: Current Asset Management

7-26

New sales = $144,000 × 1.15 = $165,000

Change in sales = $165,000 – $144,000 = $ 21,600

COMPREHENSIVE PROBLEM

Logan Distributing Company (receivables and inventory policy) (LO 04 & 05) Logan

Distributing Company of Atlanta sells fans and heaters to retail outlets through out the Southeast.

Joe Logan, the president of the company, is thinking about changing the firm’s credit policy to

attract customers away from competitors. The present policy calls for a 1/10, net 30 cash

discount. The new policy would call for a 3/10, net 50 cash discount. Currently, 30 percent of

Logan customers are taking the discount, and it is anticipated that this number would go up to 50

percent with the new discount policy. It is further anticipated that annual sales would increase

from a level of $400,000 to $600,000 as a result of the change in the cash discount policy.

The increased sales would also affect the inventory level. The average inventory carried by

Logan is based on a determination of an EOQ. Assume sales of fans and heaters increase from

15,000 to 22,500 units. The ordering cost for each order is $200 and the carrying cost per unit is

$1.50 (these values will not change with the discount). The average inventory is based on

EOQ/2. Each unit in inventory has an average cost of $12.

Cost of goods sold is equal to 65 percent of net sales; general and administrative expenses are

15 percent of net sales, and interest payments of 14 percent will only be necessary for the

increase in the accounts receivable and inventory balances. Taxes will be 40 percent of before–

tax income.

a. Compute the accounts receivable balance before and after the change in the cash

discount policy. Use the net sales (total sales minus cash discounts) to determine the

average daily sales.

b. Determine EOQ before and after the change in the cash discount policy. Translate this

into average inventory (in units and dollars) before and after the change in the cash

discount policy.

Chapter 07: Current Asset Management

7-27

c. Complete the following income statement.

Before Policy

Change

After Policy

Change

Net sales (Sales – Cash discounts) ……………

Cost of goods sold …………………………………

Gross profit ………………………………………….

General and administrative expense ………….

Operating profit …………………………..………..

Interest on increase in accounts

receivable and inventory (14%) …………….

Income before taxes……………………………….

Taxes…………………………………………………..

Income after taxes …………………………………

d. Should the new cash discount policy be utilized? Briefly comment.

CP 7-1. Solution:

Logan Distributing Company

a. Accounts receivable = average collection × average daily

period sales

Before

Average collection period

Chapter 07: Current Asset Management

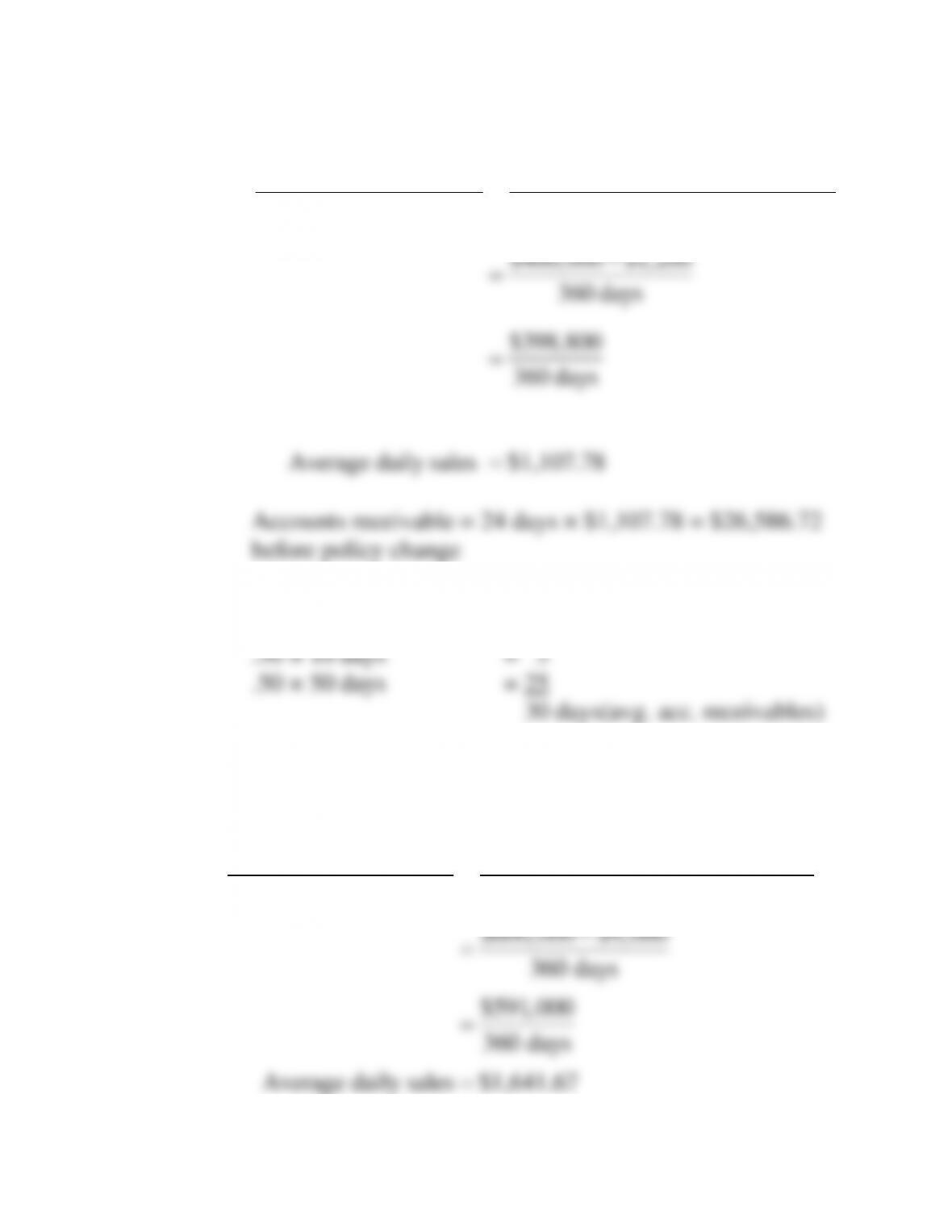

( )( )( )

$400,000 .01 .30 $400,000

Credit sales Discount

360 days 360 days

$400,000 $1,200

360 days

$398,800

360 days

Average daily sales $1,107.78

−

−=

−

=

=

=

Accounts receivable = 24 days × $1,107.78 = $26,586.72

before policy change

After

Average collection period

CP 7-1. (Continued)

Average daily sales

( )( )( )

$600,000 .03 .50 $600,000

Credit sales discount

360 days 360 days

$600,000 $9,000

360 days

$591,000

360 days

−

−=

−

=

=

Chapter 07: Current Asset Management

7-29

b. Before

2SO

EOQ C

=

2 15,000 $200 $6,000,000 4,000,000 2,000 units

$1.50 $1.50

= = =

After

2 22,000 $200 $9,000,000 6,000,000 2,449.49

$1.50 $1.50

= = =

Average inventory

Before

2,000 1,000 units 1,000 units $12 $12,000

2= =

Chapter 07: Current Asset Management

7-30

CP 7-1. (Continued)

After

2,449.49

2=

c.

Before

Policy

Change

After

Policy

Change

Net sales (sales – cash discount)

$398,800

$591, 000

Cost of goods sold (65%)

259,220

384,150

Gross Profit

139,580

206,850

General and admin. expense (15%)

59,820

88,650

Operating profit

79,760

118,200

*Interest on increase in accounts

receivable and inventory (14%)

3,550.45

Income before taxes

79,760

114,649.55

Taxes (40%)

31,904

45,859.82

Income after taxes

$ 47,856

$ 68,789.73

*14% AR

( )

14% $49,250.10 $26,586.72= −

14% $22,663.38=

$3,172.87=

14% INV

( )

=14% $14,697 $12,000−

14% $2.697=

$ 377.58=

$3,550.45

d. The new cash discount policy should be utilized. The interest

1,224.75 units 1,224.75 units ×$12 =

or 1,225 (rounded) $14,697 or $14,700

(rounded)