Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05: Operating and Financial Leverage

5-48

e. What would be the required new funds if the company brings its ratios into line with

the industry average during 2011? Specifically examine receivables turnover,

inventory turnover, and the profit margin. Use the new values to recompute the

factors in RNF (assume liabilities stay the same).

f. Do not calculate, only comment on these questions. How would required new funds

change if the company:

(1) Were at full capacity?

(2) Raised the dividend payout ratio?

(3) Suffered a decreased growth in sales?

(4) Faced an accelerated inflation rate?

CP 5-1. Solution:

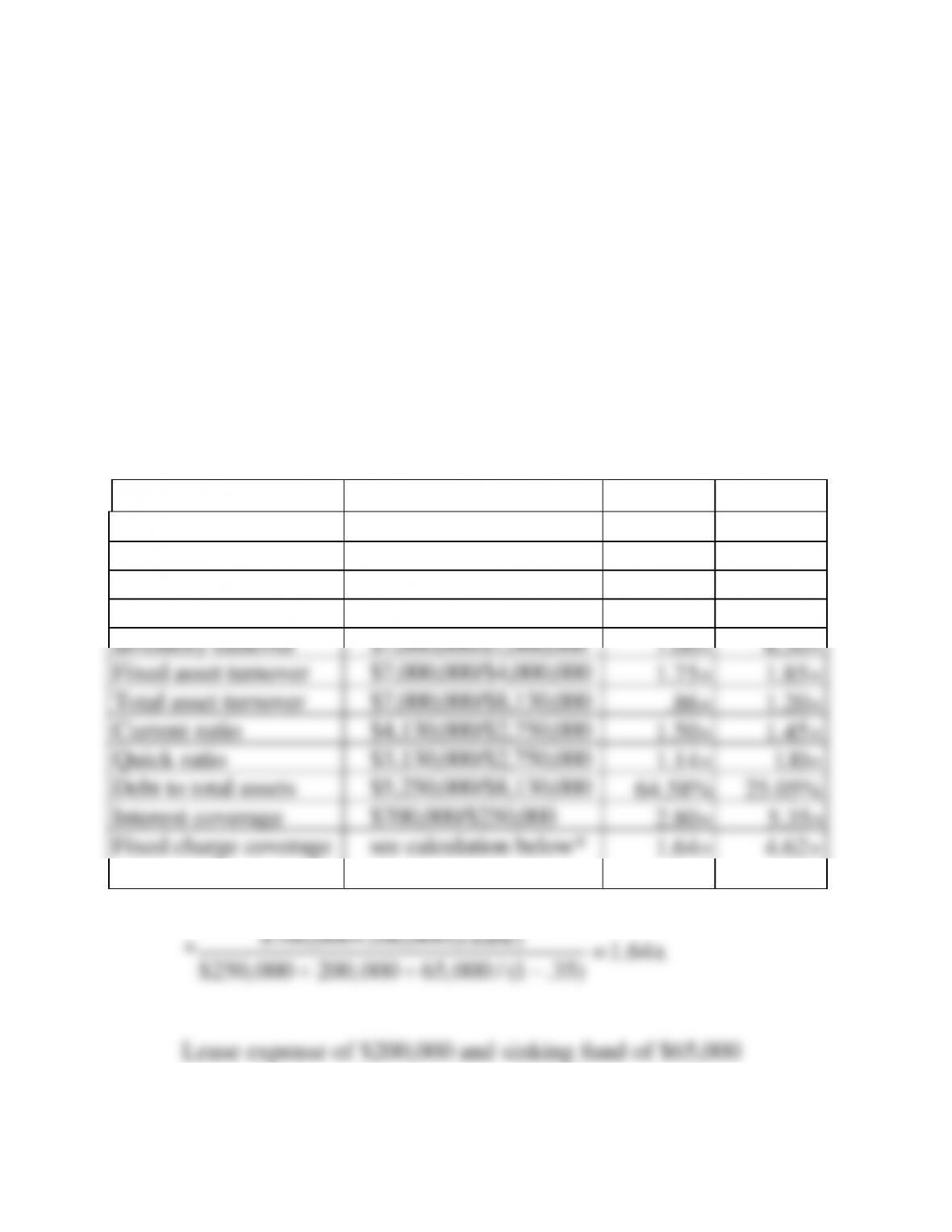

Ryan Boot Company

a. Ratio analysis

Ryan

Industry

Profit margin

$292,500/$7,000,000

4.18%

5.75%

Return on assets

$292,500/$8,130,000

3.60%

6.90%

Return on equity

$292,500/$2,880,000

10.16%

9.20%

Receivable turnover

$7,000,000/$3,000,000

2.33

4.35

Inventory turnover

$7,000,000/$1,000,000

7.00

6.50

Fixed asset turnover

$7,000,000/$4,000,000

1.75

1.85

Total asset turnover

$7,000,000/$8,130,000

.86

1.20

Current ratio

$4,130,000/$2,750,000

1.50

1.45

Quick ratio

$3,130,000/$2,750,000

1.14

l.l0

Debt to total assets

$5,250,000/$8,130,000

64.58

25.05

Interest coverage

$700,000/$250,000

2.80

5.35

Fixed charge coverage

see calculation below*

1.64

4.62

$700,000+200,000(Lease)

* 1.64x

$250,000 200,000 65,000 / (1 .35) =

+ + −

Lease expense of $200,000 and sinking fund of $65,000

Chapter 05: Operating and Financial Leverage

5-49

a. The company has a lower profit margin than the industry and

the problem is further compounded by the slow turnover of

assets (.86x versus an industry norm of 1.20x). This leads to

a much lower return on assets. The company has a higher

return on equity than the industry, but this is accomplished

through the firm's heavy debt ratio rather than through

superior profitability.

b. Break-even in sales

Sales Fixed Costs Variable costs=+

(variable costs are expressed as a percentage of sales)

BE

Sales $2,100,000 .60 Sales

.40 S $2,100,000

S $2,100,000 /.40

S $5,250,000

=+

=

=

=

Chapter 05: Operating and Financial Leverage

Cash break-even

Sales (Fixed costs Non cash expenses*) +Variable costs=−

BE

BE

Sales ($2,100,000 $500,000) + .60 Sales

Sales $1,600,000 .60 Sales

.40 S $1,600,000

S $1,600,000 /.40

S $4,000,000

=−

=+

=

=

=

*Depreciation

S TVC

DOL S TVC FC

$7,000,000 $4,200,000

$7,000,000 $4,200,000 $2,100,000

$2,800,000 4x

$700,000

−

=−−

−

=−−

==

EBIT $700,000

DFL EBIT I $700,000 $250,000

$700,000 1.56x

$450,000

==

−−

==

S TVC

DCL S TVC FC I

$7,000,000 $4,200,000

$7,000,000 $4,200,000 $2,100,000 $250,000

$2,800,000 6.22x

$450,000

−

=− − −

−

=− − −

==

Chapter 05: Operating and Financial Leverage

5-51

c. Ryan is operating at a sales volume that is $1,750,000 above

the traditional break-even point and $3,000,000 above the

cash break-even point. This can be viewed as somewhat

positive.

However, the firm has a high degree of leverage, which

indicates any reduction in sales volume could have a very

negative impact on profitability. The DOL of 4x is associated

with heavy fixed assets and relatively high fixed costs. The

so hopefully a large expansion would not take place here.

There appears to be a need to reduce accounts receivable

rather than increase the level.

One possible use of the funds might be to pay off part of the

improve its profitability.

Chapter 05: Operating and Financial Leverage

d.

( ) ( ) ( )

2

AL

Required new funds= S S PS 1 D

SS

− − −

( ) ( )

( )

Change in Sales = 20% x $7,000,000= $1,400,000

$4,130,000 $2,350,000

RNF $1,400,000 $1,400,000

$7,000,000 $7,000,000

4.18% $8,400,000 (1 .4)

=−

−−

( ) ( ) ( )

RNF = .590 $1,400,000 .336 $1,400,000 $351,120 .6

$826,000 $470,400 $210,672

$144,928

−−

= − −

=

e. Required funds if selected industry ratios were applied

Receivables = Sales/Receivable turnover

Chapter 05: Operating and Financial Leverage

5-53

( ) ( )

( )( )

$2,739,195 $2,350,000

RNF= $1,400,000 $1,400,000

$7,000,000 $7,000,000

5.75% $8,400,000 1 .4

−

−−

( ) ( ) ( )

RNF .391 $1,400,000 .336 $1,400,000 $483,000 .6

$547,400 $470,400 $289,800

$212,800

= − −

= − −

=−

higher profit margin.

f. (1) If Ryan Boots were at full capacity, more funds would be

needed to expand plant and equipment.

(2) More funds would be needed to offset the larger payout of

earnings to dividends.

growth.

(4) As inflation increased so would the cost of new assets,

Chapter 05: Operating and Financial Leverage

5-54

W E B E X E R C I S E

1. At the start of the chapter, we talked about how risky and volatile airlines' operations were.

Let's examine this further. Go to finance.yahoo.com.

Enter AMR for American Airlines in the "Get Quotes" box. Go to "Company Profile"

along the left-hand margin.

2. Click on profile in the left-hand column and write a one-paragraph description of the

company.

3 Scroll down and click on the "Income Statement." Describe the pattern of change for “Total

Revenue" and "Net Income from Continuing Operations" in one paragraph.

4. Next go to the "Balance Sheet." In one sentence, describe the pattern of change in

Stockholders' Equity and indicate whether this does or does not appear to be a matter of

concern.

5. Click on "Analyst Estimates." Do AMR's earnings estimates appear to be more or less

promising for the future?

6. Finally, click on "Competitors." How does AMR compare to the other airlines and the

industry in terms of Operating Margin?

Note: Occasionally a topic we have listed may have been deleted, updated, or moved into a different location on a

Web site. If you click on the site map or site index, you will be introduced to a table of contents which should aid

you in finding the topic you are looking for.