Chapter 05: Operating and Financial Leverage

5-41

5-26. (Continued)

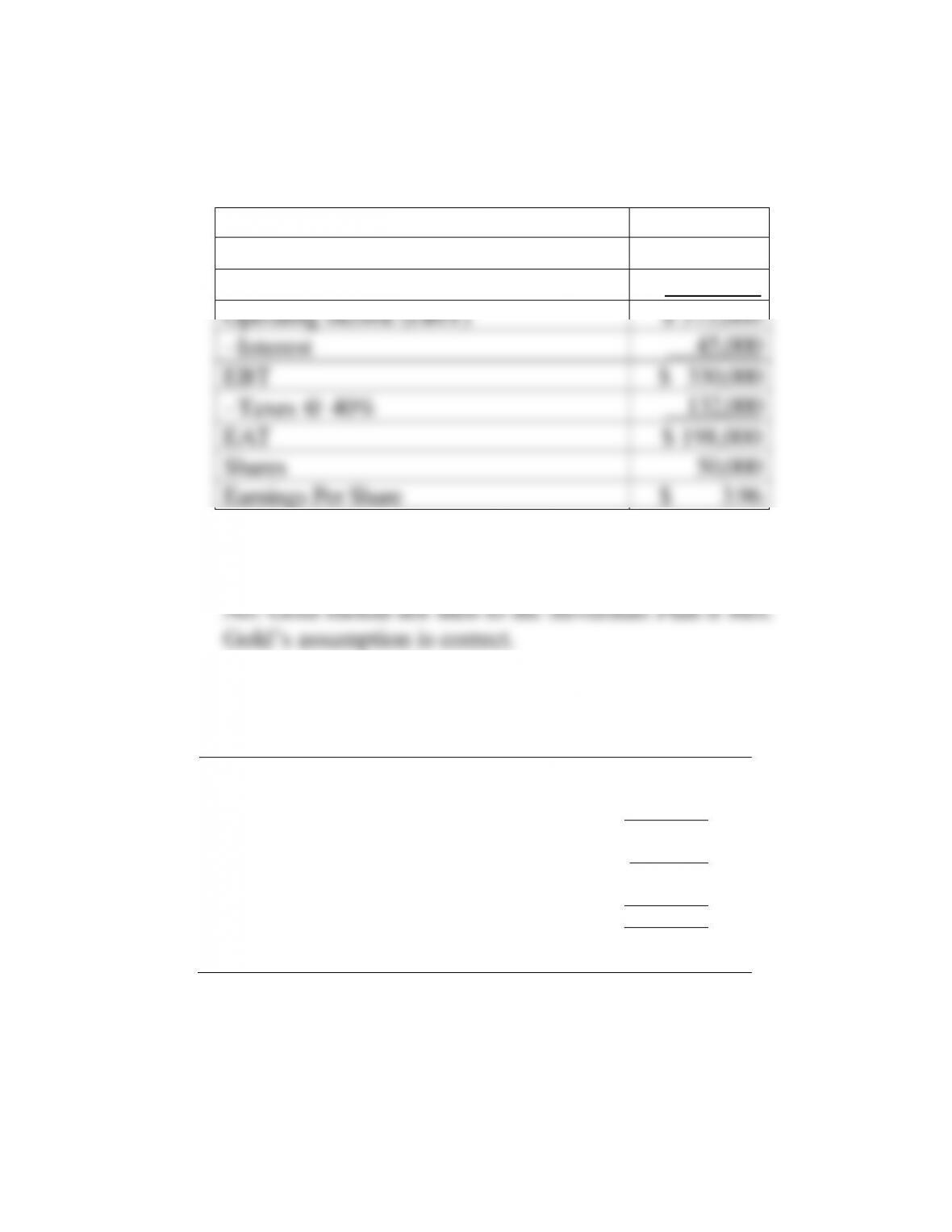

c. Silverman Plan (based on Mrs. Gold’s Assumption)

Sales ($1,400,000 units at $4.50)

$6,300,000

−Fixed costs ($1,500,000 1.15)

1,725,000

−Variable costs (1,400,000 units $3)

4,200,000

Operating income (EBIT)

$ 375,000

−Interest

45,000

EBT

$ 330,000

−Taxes @ 40%

132,000

EAT

$ 198,000

Shares

50,000

Earnings Per Share

$ 3.96

27. Expansion, break-even analysis, and leverage (LO2, 3 & 4) Delsing Canning Company

is considering an expansion of its facilities. Its current income statement is as follows:

Sales ………………………………………………………

$5,000,000

Less: Variable expense (50% of sales) ……….

2,500,000

Fixed expense ……………………………………..

1,800,000

Earnings before interest and taxes (EBIT) …….

700,000

Interest (10% cost) ……………………………………

200,000

Earnings before taxes (EBT)……………………….

500,000

Tax (30%) ……………………………………………….

150,000

Earnings after taxes (EAT) …………………………

$ 350,000

Shares of common stock—200,000 ……………..

Earnings per share …………………………………….

$1.75

The company is currently financed with 50 percent debt and 50 percent equity (common

stock, par value of $10). In order to expand the facilities, Mr. Delsing estimates a need for

$2 million in additional financing. His investment banker has laid out three plans for him

to consider:

1. Sell $2 million of debt at 13 percent.

Chapter 05: Operating and Financial Leverage

5-42

2. Sell $2 million of common stock at $20 per share.

3. Sell $1 million of debt at 12 percent and $1 million of common stock at $25 per

share.

Variable costs are expected to stay at 50 percent of sales, while fixed expenses will

increase to $2,300,000 per year. Delsing is not sure how much this expansion will add to

sales, but he estimates that sales will rise by $1 million per year for the next five years.

Delsing is interested in a thorough analysis of his expansion plans and methods of

financing. He would like you to analyze the following:

a. The break-even point for operating expenses before and after expansion (in sales

dollars).

b. The degree of operating leverage before and after expansion. Assume sales of $5

million before expansion and $6 million after expansion. Use the formula in footnote

2 of the chapter.

c. The degree of financial leverage before expansion and for all three methods of

financing after expansion. Assume sales of $6 million for this question.

d. Compute EPS under all three methods of financing the expansion at $6 million in

sales (first year) and $10 million in sales (last year).

e. What can we learn from the answer to part d about the advisability of the three

methods of financing the expansion?

5-27. Solution:

Delsing Canning Company

a. At break-even before expansion:

PQ FC VC

where PQ equals sales volume at break-even point

=+

Sales Fixed costs Variable costs

(Variable costs 50% of sales)

Sales $1,800,000 .50 Sales

.50 Sales $1,800,000

Sales $3,600,000

=+

=

=+

=

=

At break-even after expansion:

Chapter 05: Operating and Financial Leverage

Sales $2,300,000 .50 Sales

.50 Sales $2,300,000

Sales $4,600,000

=+

=

=

b. Degree of operating leverage, before expansion, at sales of

$5,000,000

( )

( )

Q P VC S TVC

DOL= Q P VC FC S TVC FC

$5,000,000 $2,500,000

$5,000,000 $2,500,000 $1,800,000

$2,500,000 3.57x

$700,000

−−

=

− − − −

−

=−−

==

5-27. (Continued)

Degree of operating leverage after expansion at sales of

$6,000,000

$6,000,000 $3,000,000

DOL= $6,000,000 $3,000,000 $2,300,000

$3,000,000 4.29x

$700,000

−

−−

==

This could also be computed for subsequent years.

c. DFL before expansion:

EBIT

DFL = EBIT 1−

Chapter 05: Operating and Financial Leverage

$700,000

$700,000 $200,000

$700,000 1.40x

$500,000

=−

==

DFL after expansion:

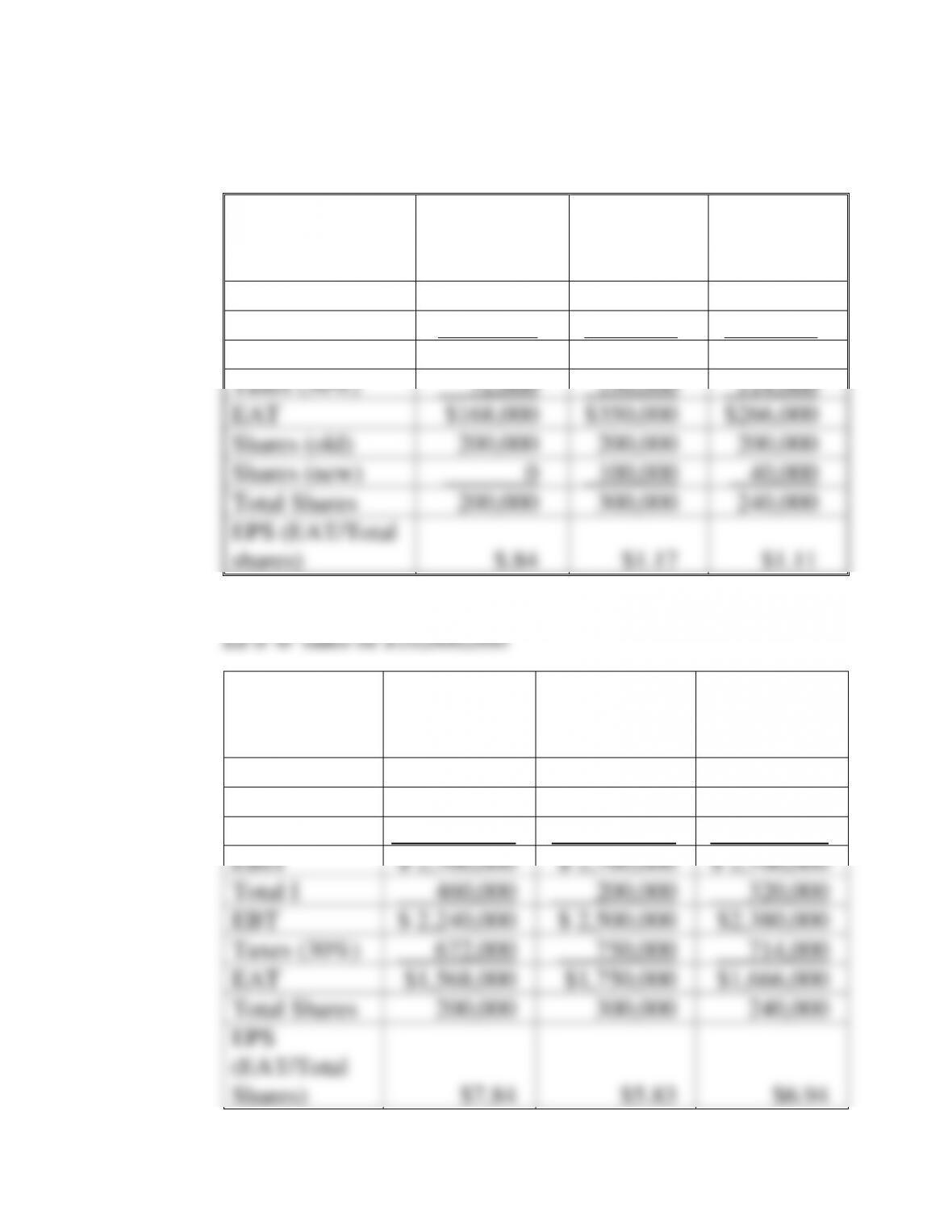

Compute EBIT and I for all three plans:

(100% Debt)

(1)

(100%

Equity) (2)

(50% Debt

and 50%

Equity) (3)

Sales

$6,000,000

$6,000,000

$6,000,000

–TVC (.50)

3,000,000

3,000,000

3,000,000

–FC

2,300,000

2,300,000

2,300,000

EBIT

$ 700,000

$ 700,000

$ 700,000

I – Old Debt

200,000

200,000

200,000

I – New Debt

260,000

0

120,000

Total Interest

$ 460,000

$ 200,000

$ 320,000

5-27. (Continued)

EBIT

DFL = EBIT I−

(1) (2) (3)

( ) ( ) ( )

$700,000 $700,000 $700,000

$700,000 $460,000 $700,000 $200,000 $700,000 $320,000−−−

DFL = 2.92x 1.40x 1.84x

Chapter 05: Operating and Financial Leverage

5-45

(refer back to part c to get the values for EBIT and Total I)

(100%

Debt) (1)

(100%

Equity) (2)

(50% Debt

and 50%

Equity) (3)

EBIT

$700,000

$700,000

$700,000

Total I

460,000

200,000

320,000

EBT

$240,000

$500,000

$380,000

Taxes (30%)

72,000

150,000

114,000

EAT

$168,000

$350,000

$266,000

Shares (old)

200,000

200,000

200,000

Shares (new)

0

100,000

40,000

Total Shares

200,000

300,000

240,000

EPS (EAT/Total

shares)

$.84

$1.17

$1.11

(100%

Debt) (1)

(100%

Equity) (2)

(50% Debt

and 50%

Equity) (3)

Sales

$10,000,000

$10,000,000

$10,000,000

–TVC

5,000,000

5,000,000

5,000,000

–FC

2,300,000

2,300,000

2,300,000

EBIT

$ 2,700,000

$ 2,700,000

$ 2,700,000

Total I

460,000

200,000

320,000

EBT

$ 2,240,000

$ 2,500,000

$2,380,000

Taxes (30%)

672,000

750,000

714,000

EAT

$1,568,000

$1,750,000

$1,666,000

Total Shares

200,000

300,000

240,000

EPS

(EAT/Total

Shares)

$7.84

$5.83

$6.94

Chapter 05: Operating and Financial Leverage

5-46

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Ryan Boot Company (review of Chapters 2 through 5) (multiple LO’s from Chapters 2

through 5)

RYAN BOOT COMPANY

Balance Sheet

December 31, 2010

Assets

Liabilities and Stockholders’ Equity

Cash …………………………………..

$ 50,000

Accounts payable ………………

$2,200,000

Marketable securities ……………

80,000

Accrued expenses ………………

150,000

Accounts receivable ……………..

3,000,000

Notes payable (current) ………

400,000

Inventory…………………………….

1,000,000

Bonds (10%) …………………….

2,500,000

Gross plant and equipment

Less…………………………………

6,000,00

Common stock (1.7 million

shares, par value $1) ………..

1,700,000

Accumulated depreciation ..

2,000,000

Retained earnings ………………

1,180,000

Total assets …………………………

$8,130,000

Total liabilities and

stockholders’ equity …………

$8,130,000

Income Statement—2010

Sates (credit) ………………………………………………………………

$7,000,000

Fixed costs* ……………………………………………………………….

2,100,000

Variable costs (0.60) ……………………………………………………

4,200,000

Earnings before interest and taxes ………………………………….

700,000

Less: Interest ……………………………………………………………

250,000

Earnings before taxes …………………………………………………..

450,000

Less: Taxes @ 35% …………………………………………………..

157,500

Earnings after taxes ……………………………………………………..

$ 292,500

Dividends (40% payout) …………………………………………….

117,000

Increased retained earnings …………………………………………..

$ 175,500

Chapter 05: Operating and Financial Leverage

5-47

*Fixed costs include (a) lease expense of $200,000 and (b) depreciation of

$500,000.

Note: Ryan Boots also has $65,000 per year in sinking fund obligations

associated with its bond issue. The sinking fund represents an annual repayment

of the principal amount of the bond. It is not tax-deductible.

Comprehensive Problem 1 (Continued)

Ratios

Ryan Boot

(to be filled in)

Industry

Profit margin …………………………….

_____________

5.75%

Return on assets ………………………..

_____________

6.90%

Return on equity ………………………..

_____________

9.20%

Receivables turnover ………………….

_____________

4.35X

Inventory turnover……………………..

_____________

6.50X

Fixed-asset turnover …………………..

_____________

1.85X

Total-asset turnover ……………………

_____________

1.20X

Current ratio ……………………………..

_____________

1.45X

Quick ratio ……………………………….

_____________

1.10X

Debt to total assets …………………….

_____________

25 05%

Interest coverage ……………………….

_____________

5.35X

Fixed charge coverage ………………..

_____________

4.62X

a. Analyze Ryan Boot Company, using ratio analysis. Compute the ratios on the prior

page for Ryan and compare them to the industry data that is given. Discuss the weak

points, strong points, and what you think should be done to improve the company’s

performance.

b. In your analysis, calculate the overall break-even point in sales dollars and the cash

break-even point. Also compute the degree of operating leverage, degree of financial

leverage, and degree of combined leverage. (Use footnote 2 for DOL and footnote 3

in the chapter for DCL.)

c. Use the information in parts a and b to discuss the risk associated with this company.

Given the risk, decide whether a bank should loan funds to Ryan Boot.

Ryan Boot Company is trying to plan the funds needed for 2011. The management

anticipates an increase in sales of 20 percent, which can be absorbed without increasing

fixed assets.

d. What would be Ryan’s needs for external funds based on the current balance sheet?

Compute RNF (required new funds). Notes payable (current) and bonds are not part

of the liability calculation.