Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05: Operating and Financial Leverage

5-31

5-21. (Continued)

d. The debt financing plan provides a greater earnings per share

in comparison to the equity plan. Conversely, with increasing

sales, the debt plan becomes more attractive. Based on

probably be favored.

22. Leverage analysis with actual companies (LO6) Using Standard & Poor's data or annual

reports, compare the financial and operating leverage of Chevron, Eastman Kodak, and

Delta Airlines for the most current year. Explain the relationship between operating and

financial leverage for each company and the resultant combined leverage. What accounts

for the differences in leverage of these companies?

5-22. Solution:

23. Leverage and sensitivity analysis (LO6) Dickinson Company has $12 million in assets.

Currently half of these assets are financed with long-term debt at 10 percent and half with

common stock having a par value of $8. Ms. Smith, vice-president of finance, wishes to

analyze two refinancing plans, one with more debt (D) and one with more equity (E). The

company earns a return on assets before interest and taxes of 10 percent. The tax rate is 45

percent.

Under Plan D, a $3 million long-term bond would be sold at an interest rate of 12 percent

and 375,000 shares of stock would be purchased in the market at $8 per share and retired.

Under Plan E, 375,000 shares of stock would be sold at $8 per share and the $3,000,000 in

proceeds would be used to reduce long-term debt.

a. How would each of these plans affect earnings per share? Consider the current plan

and the two new plans.

b. Which plan would be most favorable if return on assets fell to 5 percent? Increased to

15 percent? Consider the current plan and the two new plans.

c. If the market price for common stock rose to $12 before the restructuring, which plan

would then be most attractive? Continue to assume that $3 million in debt will be

used to retire stock in Plan D and $3 million of new equity will be sold to retire debt

in Plan E. Also assume for calculations in part c that return on assets is 10 percent.

Chapter 05: Operating and Financial Leverage

5-32

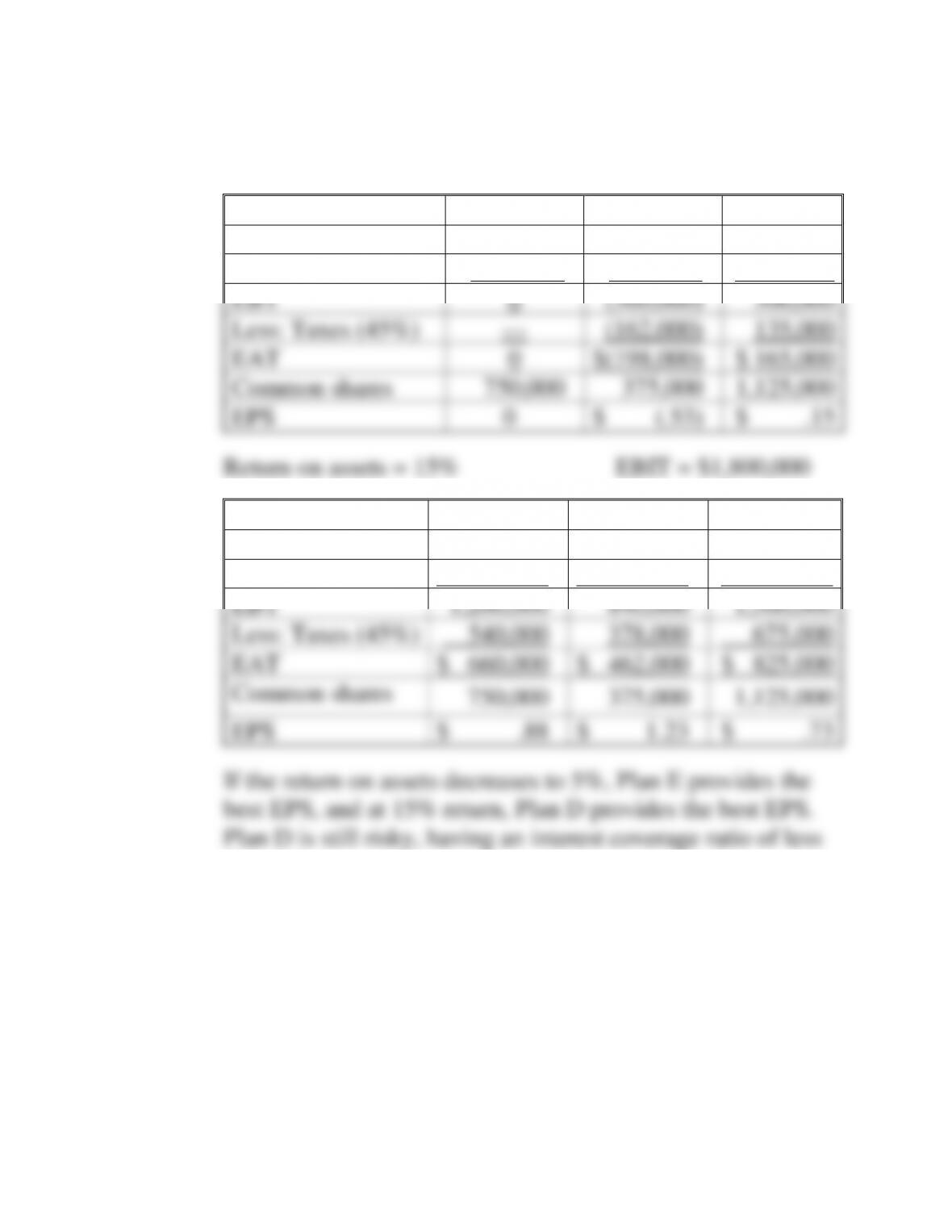

5-23. Solution:

Dickinson Company

Income Statements

a. Return on assets = 10% EBIT = $ 1,200,000

Current

Plan D

Plan E

EBIT

$1,200,000

$1,200,000

$1,200,000

Less: Interest

600,0001

960,0002

300,0003

EBT

600,000

240,000

900,000

Less: Taxes (45%)

270,000

108,000

405,000

EAT

330,000

132,000

495,000

Common shares

750,0004

375,000

1,125,000

EPS

$ .44

$ .35

$ .44

(1) $6,000,000 debt @ 10%

financial risk to Dickinson.

Chapter 05: Operating and Financial Leverage

5-33

5-23. (Continued)

b. Return on assets = 5% EBIT = $600,000

Current

Plan D

Plan E

EBIT

$600,000

$ 600,000

$ 600,000

Less: Interest

600,000

960,000

300,000

EBT

0

(360,000)

300,000

Less: Taxes (45%)

---

(162,000)

135,000

EAT

0

$(198,000)

$ 165,000

Common shares

750,000

375,000

1,125,000

EPS

0

$ (.53)

$ .15

Current

Plan D

Plan E

EBIT

$1,800,000

$1,800,000

$1,800,000

Less: Interest

600,000

960,000

300,000

EBT

1,200,000

840,000

1,500,000

Less: Taxes (45%)

540,000

378,000

675,000

EAT

$ 660,000

$ 462,000

$ 825,000

Common shares

750,000

375,000

1,125,000

EPS

$ .88

$ 1.23

$ .73

than 2.0.

Chapter 05: Operating and Financial Leverage

5-34

Current

Plan D

Plan E

EBIT

$1,200,000

$1,200,000

$1,200,000

EAT

330,000

132,000

495,000

Common shares

750,000

500,0001

1,000,0002

EPS

$. 44

$ .26

$ .50

under Plan E.

24. Leverage and sensitivity analysis (LO6) Edsel Research Labs has $24 million in assets.

Currently half of these assets are financed with long-term debt at 8 percent and half with

common stock having a par value of $10. Ms. Edsel, the vice-president of finance, wishes

to analyze two refinancing plans, one with more debt (D) and one with more equity (E).

The company earns a return on assets before interest and taxes of 8 percent. The tax rate is

40 percent.

Under Plan D, a $6 million long-term bond would be sold at an interest rate of 10 percent

and 600,000 shares of stock would be purchased in the market at $10 per share and retired.

Under Plan E, 600,000 shares of stock would be sold at $10 per share and the $6,000,000

in proceeds would be used to reduce long-term debt.

a. How would each of these plans affect earnings per share? Consider the current plan

and the two new plans. Which plan(s) would produce the highest EPS?

b. Which plan would be most favorable if return on assets increased to 12 percent?

Compare the current plan and the two new plans. What has caused the plans to give

different EPS numbers?

c. Assuming return on assets is back to the original 8 percent, but the interest rate on

new debt in Plan D is 6 percent, which of the three plans will produce the highest

EPS? Why?

Chapter 05: Operating and Financial Leverage

5-35

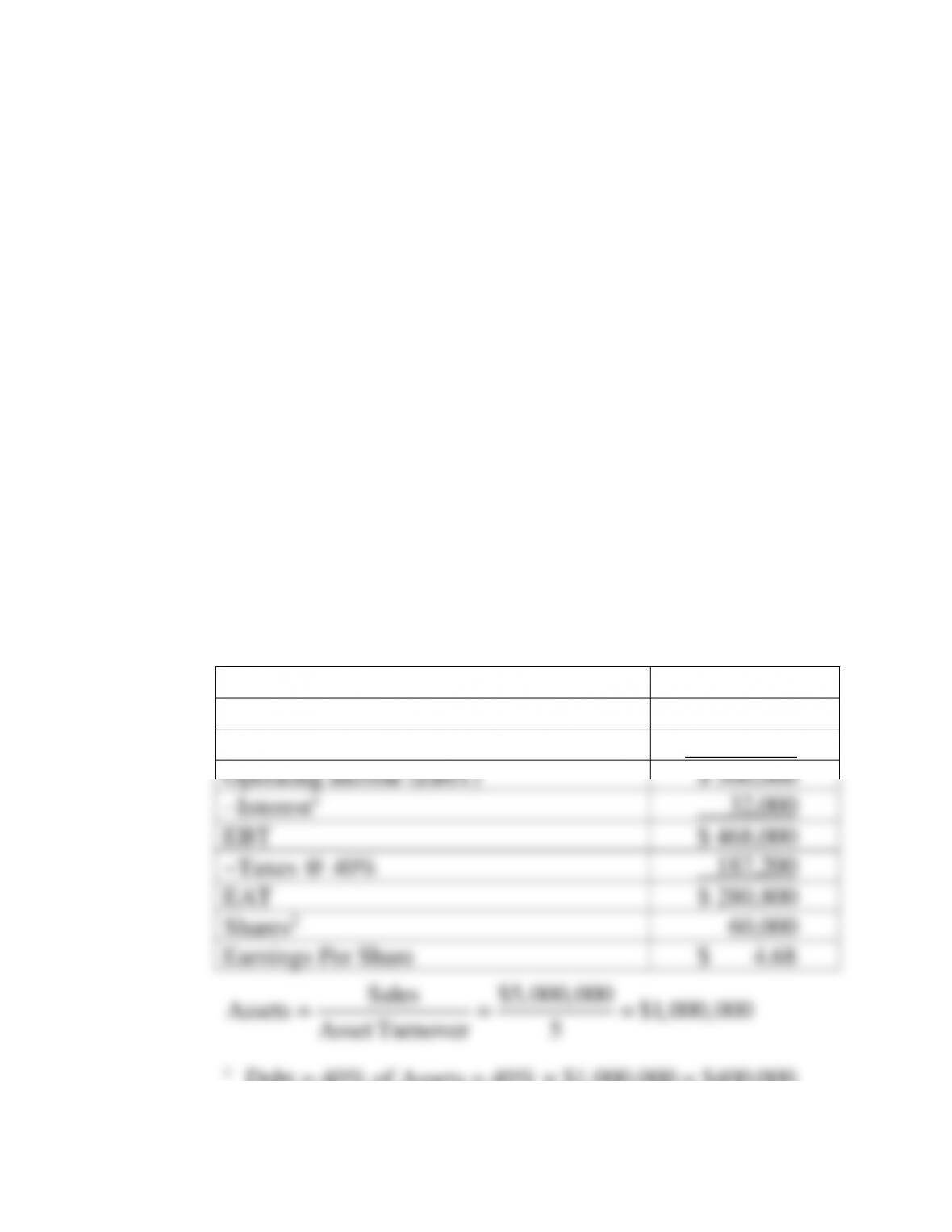

5-24. Solution:

Edsel Research Labs

Income Statement

a. Return on assets = 8% EBIT = $1,920,000

Current

Plan D

Plan E

EBIT

$1,920,000

$1,920,000

$1,920,000

Less: Interest

960,0001

1,560,0002

480,0003

EBT

960,000

360,000

1,440,000

Less: Taxes (40%)

384,000

144,000

576,000

EAT

576,000

216,000

864,000

Common shares

1,200,0004

600,0005

1,800,0006

EPS

$.48

$.36

$.48

1 $12,000,000 debt @ 8%

2 $960,000 interest + ($6,000,000 new debt @ 10%)

3 ($12,000,000 − $6,000,000 debt retired) 8%

4 ($12,000,000 common equity / $10 par value) = 1,200,000

shares

5 ($6,000,000 common equity / $10 par value) = 600,000

shares

6 ($18,000,000 common equity / $10 par value) = 1,800,000

shares

Chapter 05: Operating and Financial Leverage

5-36

5-25. (Continued)

b. Return on assets = 12% EBIT = $2,880,000

Current

Plan D

Plan E

EBIT

$2,880,000

$2,880,000

$2,880,000

Less: Interest

960,000

1,560,000

480,000

EBT

1,920,000

1,320,000

2,400,000

Less: taxes (40%)

768,000

528,000

960,000

EAT

1,152,000

792,000

1,440,000

Common shares

1,200,000

600,000

1,800,000

EPS

$.96

$1.32

$.80

Pan D provides the highest return. The % EBIT (12%) is

higher than the interest rate (8% and 10%). The more

debt the better.

c. Return on assets = 8% EBIT = $1,920,000

Current

Plan D

Plan E

EBIT

$1,920,000

$1,920,000

$1,920,000

Less: Interest

960,000

1,320,0001

480,000

EBT

960,000

600,000

1,440,000

Less: taxes (40%)

384,000

240,000

576,000

EAT

576,000

360,000

864,000

Common shares

1,200,000

600,000

1,800,000

EPS

$.48

$.60

$.48

1 $960,000 + (6,000,000 6%)

Chapter 05: Operating and Financial Leverage

5-37

25. Leverage and sensitivity analysis The Lopez-Portillo Company has $10 million in assets,

80 percent financed by debt and 20 percent financed by common stock. The interest rate on

the debt is 15 percent and the par value of the stock is $10 per share. President Lopez-

Portillo is considering two financing plans for an expansion to $15 million in assets.

Under Plan A, the debt-to-total-assets ratio will be maintained, but new debt will cost a

whopping 18 percent! Under Plan B, only new common stock at $10 per share will be

issued. The tax rate is 40 percent.

a. If EBIT is 15 percent on total assets, compute earnings per share (EPS) before the

expansion and under the two alternatives.

b. What is the degree of financial leverage under each of the three plans?

c. If stock could be sold at $20 per share due to increased expectations for the firm's

sales and earnings, what impact would this have on earnings per share for the two

expansion alternatives? Compute earnings per share for each.

d. Explain why corporate financial officers are concerned about their stock values.

5-25. Solution:

Lopez-Portillo Company

a. Return on Assets = 12%

Current

Plan A

Plan B

EBIT

$1,500,000

$2,250,000

$2,250,000

Less: Interest

1,200,000(a)

1,920,000(c)

1,200,000(e)

EBT

300,000

330,000

1,050,000

Less: Taxes (40%)

120,000

132,000

420,000

EAT

$ 180,000

$ 198,000

$ 630,000

Common shares

200,000(b)

300,000(d)

700,000(f)

EPS

$.90

$.66

$.90

(a) (80% $10,000,000) 15% = $8,000,000 15% =

$1,200,000

(b) (20% $10,000,000)/$10 = $2,000,000/$10 = 200,000 shares

Chapter 05: Operating and Financial Leverage

5-25. (Continued)

b.

EBIT

DFL EBIT I

=

−

$1,500,000

DFL (Current) 5.00x

$1,500,000 $1,200,000

$2,250,000

DFL (Plan A) 6.82x

$2,250,000 $1,920,000

$2,250,000

DFL (Plan B) 2.14x

$2,250,000 $1,200,000

==

−

==

−

==

−

c.

Plan A

Plan B

EAT

$198,000

$630,000

Common Shares

250,0001

450,0002

EPS

$. 79

$ 1.40

1 200,000 shares (current) + (20% $5,000,000)/$20

than that indicated in part (a).

d. Not only does the price of the common stock create wealth to

the shareholder, which is the major objective of the financial

Chapter 05: Operating and Financial Leverage

5-39

26. Operating leverage and ratios (LO6) Mr. Gold is in the widget business. He currently

sells 1 million widgets a year at $5 each. His variable cost to produce the widgets is $3 per

unit, and he has $1,500,000 in fixed costs. His sales-to-assets ratio is five times, and 40

percent of his assets are financed with 8 percent debt, with the balance financed by

common stock at $10 par value per share. The tax rate is 40 percent.

His brother-in-law, Mr. Silverman, says he is doing it all wrong. By reducing his price

to $4.50 a widget, he could increase his volume of units sold by 40 percent. Fixed costs

would remain constant, and variable costs would remain $3 per unit. His sales-to-assets

ratio would be 6.3 times. Furthermore, he could increase his debt-to-assets ratio to 50

percent, with the balance in common stock. It is assumed that the interest rate would go up

by 1 percent and the price of stock would remain constant.

a. Compute earnings per share under the Gold plan.

b. Compute earnings per share under the Silverman plan.

c. Mr. Gold's wife, the chief financial officer, does not think that fixed costs would

remain constant under the Silverman plan but that they would go up by 15 percent.

If this is the case, should Mr. Gold shift to the Silverman plan, based on earnings per

share?

5-26. Solution:

Gold-Silverman

a. Gold Plan

Sales ($1,000,000 units $5)

$5,000,000

−Fixed costs

−1,500,000

−Variable costs

−3,000,000

Operating income (EBIT)

$ 500,000

−Interest1

32,000

EBT

$ 468,000

−Taxes @ 40%

187,200

EAT

$ 280,800

Shares2

60,000

Earnings Per Share

$ 4.68

Sales $5,000,000

Assets $1,000,000

AssetTurnover 5

= = =

1 Debt = 40% of Assets = 40% × $1,000,000 = $400,000

Chapter 05: Operating and Financial Leverage

5-40

5-26. (Continued)

b. Silverman Plan

Sales ($1,400,000 units at $4.50)

$6,300,000

−Fixed costs

1,500,000

−Variable costs (1,400,000 units $3)

4,200,000

Operating income (EBIT)

$ 600,000

−Interest3

45,000

EBT

$ 555,000

−Taxes @ 40%

222,000

EAT

$ 333,000

Shares4

50,000

Earnings Per Share

$ 6.66

Sales $6,300,000

Assets $1,000,000

AssetTurnover 6.3

= = =

3 Debt = 50% of Assets = 50% × $1,000,000 = $500,000

Interest = 9% × $500,000 = $45,000

4 Stock = 50% of $1,000,000 = $500,000

Shares = $500,000/$10 = 50,000 shares