Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 05: Operating and Financial Leverage

5-21

5-16. Solution:

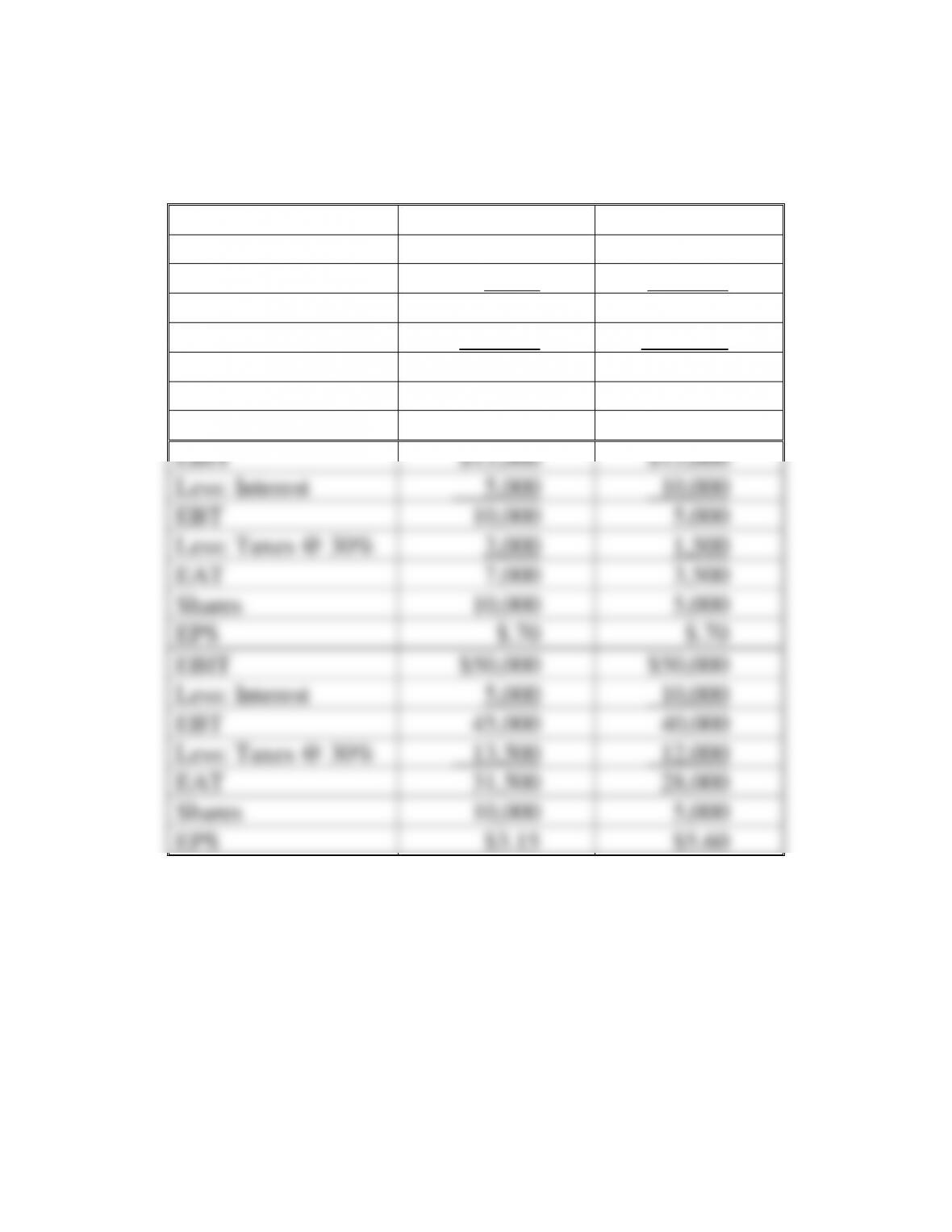

a. Cain Auto Supplies and Able Auto Parts

Cain

Able

EBIT

$10,000

$10,000

Less: Interest

5,000

10,000

EBT

5,000

0

Less: Taxes @ 30%

1,500

0

EAT

3,500

0

Shares

10,000

5,000

EPS

$.35

0

EBIT

$15,000

$15,000

Less: Interest

5,000

10,000

EBT

10,000

5,000

Less: Taxes @ 30%

3,000

1,500

EAT

7,000

3,500

Shares

10,000

5,000

EPS

$.70

$.70

EBIT

$50,000

$50,000

Less: Interest

5,000

10,000

EBT

45,000

40,000

Less: Taxes @ 30%

13,500

12,000

EAT

31,500

28,000

Shares

10,000

5,000

EPS

$3.15

$5.60

Chapter 05: Operating and Financial Leverage

5-22

5-16. (Continued)

b. Before-tax return on assets = 6.67%, 10% and 33% at the

respective levels of EBIT. When the before-tax return on

assets (EBIT/Total Assets) is less than the cost of debt

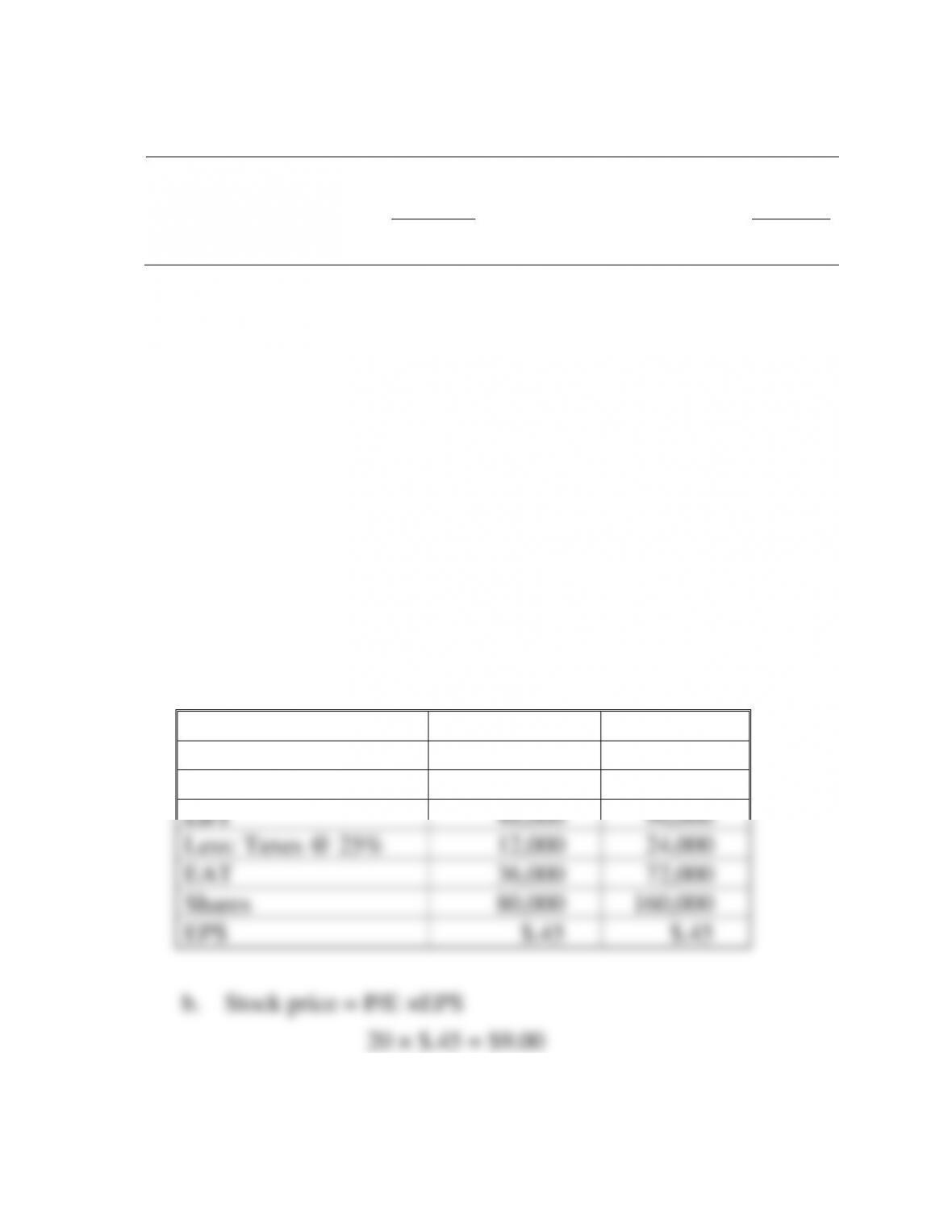

17. P/E Ratio (LO6) In Problem 16, compute the stock price for Cain if it sells at 18 times

earnings per share and EBIT is $40,000.

5-17. Solution:

Cain Supplies and Able Auto Parts (Continued)

Cain

EBIT

$40,000

Less: Interest

5,000

EBT

$35,000

Less: Taxes @ 30%

10,500

EAT

$24,500

Shares

10,000

EPS

$2.45

P/E

18x

Stock Price

$ 44.10

18. Leverage and stockholder wealth (LO4) Sterling Optical and Royal Optical both make

glass frames and each is able to generate earnings before interest and taxes of $120,000.

The separate capital structures for Sterling and Royal are shown below:

Chapter 05: Operating and Financial Leverage

5-23

Sterling

Royal

Debt @ 12%………………

$ 600,000

Debt @ 12%……………

$ 200,000

Common stock, $5 par……

400,000

Common stock, $5 par

800,000

Total………………………

$1,000,000

Total……………………

$1,000,000

Common shares…………..

80,000

Common shares………...

160,000

a. Compute earnings per share for both firms. Assume a 25 percent tax rate.

b. In part a, you should have gotten the same answer for both companies' earnings per

share. Assuming a P/E ratio of 20 for each company, what would its stock price be?

c. Now as part of your analysis, assume the P/E ratio would be 16 for the riskier

company in terms of heavy debt utilization in the capital structure and 25 for the less

risky company. What would the stock prices for the two firms be under these

assumptions? (Note: Although interest rates also would likely be different based on

risk, we will hold them constant for ease of analysis.)

d. Based on the evidence in part c, should management only be concerned about the

impact of financing plans on earnings per share or should stockholders' wealth

maximization (stock price) be considered as well?

5-18. Solution:

Sterling Optical and Royal Optical

a.

Sterling

Royal

EBIT

$120,000

$120,000

Less: Interest

72,000

24,000

EBT

48,000

96,000

Less: Taxes @ 25%

12,000

24,000

EAT

36,000

72,000

Shares

80,000

160,000

EPS

$.45

$.45

b. Stock price = P/E ×EPS

20 × $.45 = $9.00

Chapter 05: Operating and Financial Leverage

c. Sterling Royal

16 × $.45 = $7.20 25 × $.45 = $11.25

19. Japanese firm and combined leverage (LO5) Firms in Japan often employ both high

operating and financial leverage because of the use of modern technology and close

borrower-lender relationships. Assume the Mitaka Company has a sales volume of 125,000

units at a price of $25 per unit; variable costs are $5 per unit and fixed costs are

$1,800,000. Interest expense is $400,000. What is the degree of combined leverage for this

Japanese firm?

5-19. Solution:

Mitaka Company

Q(P VC)

DCL Q(P VC) FC I

125,000 ($25 $5)

125,000 ($25 $5) $1,800,000 $400,000

125,000 ($20)

125,000 ($20) $2,200,000

$2,500,000

−

=

− − −

−

=

− − −

=

−

Chapter 05: Operating and Financial Leverage

5-25

20. Combining operating and financial leverage (LO5) Sinclair Manufacturing and Boswell

Brothers Inc. are both involved in the production of brick for the homebuilding industry.

Their financial information is as follows:

Capital Structure

Sinclair

Boswell

Debt @ 12%............................................................

$ 600,000

0

Common stock, $10 per share................................

400,000

$ 1,000,000

Total.....................................................................

$ 1,000,000

$ 1,000,000

Common shares.......................................................

40,000

100,000

Operating Plan

Sales (50,000 units at $20 each)..............................

$ 1,000,000

$ 1,000,000

Less: Variable costs.............................................

800,000

500,000

..................................................................................

($16 per unit)

($10 per unit)

Fixed costs.......

0

300,000

Earnings before interest and taxes (EBIT)...............

$ 200,000

$ 200,000

a. If you combine Sinclair's capital structure with Boswell's operating plan, what is the

degree of combined leverage? (Round to two places to the light of the decimal point.)

b. If you combine Boswell's capital structure with Sinclair's operating plan, what is the

degree of combined leverage?

c. Explain why you got the results you did in part b.

d. In part b, if sales double, by what percentage will EPS increase?

5-20. Solution:

Sinclair Manufacturing and Boswell Brothers

Chapter 05: Operating and Financial Leverage

a.

Q(P VC)

DCL Q(P VC) FC I

50,000 ($20 $10)

50,000 ($20 $10) $300,000 $72,000

500,000

500,000 $300,000 $72,000

$500,000

$128,000

3.91x

−

=

− − −

−

=

− − −

=

−−

=

=

b.

Q(P VC)

DCL Q(P VC) FC I

50,000($20 $16)

50,000($20 $16) 0 0

50,000($4)

50,000($4)

−

=

− − −

−

=

− − −

=

Chapter 05: Operating and Financial Leverage

5-27

5-20. (Continued)

21. Expansion and leverage (LO5) The Norman Automatic Mailer Machine Company is

planning to expand production because of the increased volume of mailouts. The increased

mailout capacity will cost $2,000,000. The expansion can be financed either by bonds at an

interest rate of 12 percent or by selling 40,000 shares of common stock at $50 per share.

The current income statement (before expansion) is as follows:

NORMAN AUTOMATIC MAILER

Income Statement

201X

Sales.

$3,000,000

Less: Variable costs (40%). .........................

$1,200,000

Fixed costs................................................

800,000

Earnings before interest and taxes ...................

1,000,000

Less: Interest expense ..................................

400,000

Earnings before taxes .....................................

600,000

Less: Taxes (@ 35%) ..................................

210,000

Earnings after taxes ........................................

$ 390,000

Shares ............................................................

100,000

Earnings per share ..........................................

$ 3.90

Assume that after expansion, sales are expected to increase by $1,500,000. Variable costs

will remain at 40 percent of sales, and fixed costs will increase by $550,000. The tax rate is

35 percent.

a. Calculate the degree of operating leverage, the degree of financial leverage, and the

degree of combined leverage before expansion. (For the degree of operating leverage,

use the formula developed in footnote 2 of this chapter; for the degree of combined

leverage, use the formula developed in footnote 3. These instructions apply

throughout this problem.)

b. Construct the income statement for the two financial plans.

c. Calculate the degree of operating leverage, the degree of financial leverage, and the

degree of combined leverage, after expansion, for the two financing plans.

d. Explain which financing plan you favor and the risks involved.

Chapter 05: Operating and Financial Leverage

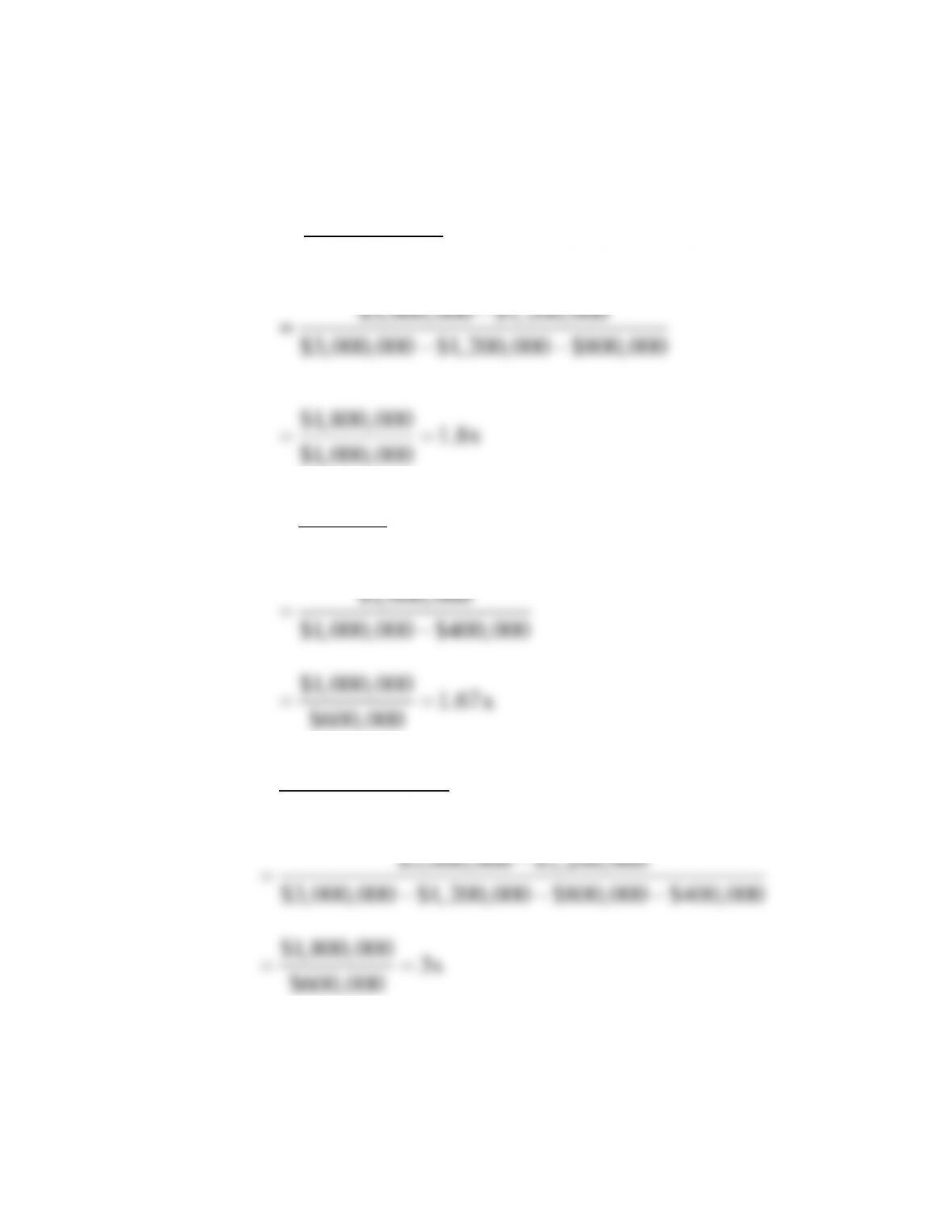

5-21. Solution:

Norman Automatic Mailer Machine

a.

S TVC

DOL S TVC FC

−

=

−−

$3,000,000 $1,200,000

$3,000,000 $1,200,000 $800,000

$1,800,000 1.8x

$1,000,000

EBIT

DFL EBIT I

$1,000,000

$1,000,000 $400,000

$1,000,000 1.67x

$600,000

−

=

−−

==

=

−

=

−

==

S TVC

DCL S TVC FC I

$600,000

−

=

==

Chapter 05: Operating and Financial Leverage

5-29

5-21. (Continued)

b. Income Statement After Expansion

Debt

Equity

Sales

$4,500,000

$4,500,000

Less: Variable Costs (40%)

1,800,000

1,800,000

Fixed Costs

1,350,000

1,350,000

EBIT

1,350,000

1,350,000

Less: Interest

640,0001

400,000

EBT

710,000

950,000

Less: Taxes @ 35%

248,500

332,500

EAT (Net Income)

461,500

617,500

Common Shares

100,000

140,0002

EPS

$ 4.62

$ 4.41

(1) New interest expense level if expansion is financed

with debt.

(2) Number of common shares outstanding if expansion is

financed with equity.

Chapter 05: Operating and Financial Leverage

5-21. (Continued)

c.

S TVC

DOL (Sameundereitherplan)

S TVC FC

−

=

−−

$4,500,000 $1,800,000

DOL (Debt/Equity) $4,500,000 $1,800,000 $1,350,000

$2,700,000 2x

$1,350,000

−

=

−−

==

EBIT

DFL EBIT I

$1,350,000 $1,350,000

DFL (Debt) 1.90x

$1,350,000-$640,000 $710,000

$1,350,000 $1,350,000

DFL (Equity) 1.42x

$1,350,000-$400,000 $950,000

$4,500,000 $1,800,000

DCL (Debt) $4,500,000 $1,800,000

=

−

= = =

= = =

−

=

−−

$1,350,000 $640,000

$2,700,000 3.80x

$710,000

−

==

$4,500,000 $1,800,000

DCL (Equity) $4,500,000 $1,800,000 $1,350,000 $400,000

$2,700,000 2.84x

−

=

− − −