Chapter 04: Financial Forecasting

4-41

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Mansfield Corporation (external funds requirement) (LO4) Mansfield Corporation had 2010

sales of $100 million. The balance sheet items that vary directly with sales and the profit margin

are as follows:

Percent

Cash ……………………………………………………..

5%

Accounts receivable ………………………………..………..

15

Inventory ……………………………………………………….

20

Net fixed assets ………………………………………………..

40

Accounts payable……………………………………………..

15

Accruals ……………………………………………….………

10

Profit margin after taxes…………………………..………..

10%

The dividend payout rate is 50 percent of earnings, and the balance in retained earnings

at the end of 2010 was $33 million. Notes payable are currently $7 million. Long-term

bonds and common stock are constant at $5 million and $10 million, respectively.

a. How much additional external capital will be required for next year if sales increase

15 percent? (Assume that the company is already operating at full capacity.)

b. What will happen to external fund requirements if Mansfield Corporation reduces the

payout ratio, grows at a slower rate, or suffers a decline in its profit margin? Discuss

each of these separately.

c. Prepare a pro forma balance sheet for 2011 assuming that any external funds being

acquired will be in the form of notes payable. Disregard the information in part b in

answering this question (that is, use the original information and part a in constructing

your pro forma balance sheet).

Chapter 04: Financial Forecasting

4-42

CP 4-1. Solution:

Mansfield Corporation

Sales .15 $100 million =15 million

Spontaneous assets 5% 15% 20% 40% 80%

Spontaneous liabilities 15% 10% 25%

=

= + + + =

= + =

a.

( ) ( ) ( )

( ) ( ) ( )( )

2

AL

RNF= S S PS 1 D

SS

.8 $15million .25 $15 million .10 $115 1 .5

$12million $3.75million $5.75million

= $2.5 million

− − −

= − − −

= − −

more external funds.

c. Balance Sheet—December 31, 2011

(Dollars in Millions)

Cash ………………………..

$ 5.75

Accounts Payable ……..

$ 17.25

Accounts Receivable ….

17.25

Accruals ………………….

11.50

Inventory ………………….

23.00

Notes Payable …………..

17.501

Net Fixed Assets ……….

46.00

Long-Term Bonds …….

5.00

Common Stock …………

10.00

_____

Retained Earnings …….

38.752

$92.00

$92.00

1 Original notes payable plus required new funds. This is the plug figure.

2 2011 retained earnings (end of 2010) + PS2 (1–D)

Chapter 04: Financial Forecasting

4-43

Comprehensive Problem 2

Marsh Corporation (financial forecasting with seasonal production) (LO5) The difficult part

of solving a problem of this nature is to know what to do with the information contained within a

story problem. Therefore, this problem will be easier to complete if you rely on Chapter 4 for the

format of all required schedules.

The Marsh Corporation makes standard-size 2-inch fasteners, which it sells for $155 per

thousand. Mr. Marsh is the majority owner and manages the inventory and finances of the

company. He estimates sales for the following months to be:

January ……………

$263,500 (1,700,000 fasteners)

February ………….

$186,000 (1,200,000 fasteners)

March……………..

$217,000 (1,400,000 fasteners)

April ………………

$310,000 (2,000,000 fasteners)

May ……………….

$387,500 (2,500,000 fasteners)

Last year Marsh Corporation’s sales were $175,000 in November and $232,500 in

December (1,500,000 fasteners).

Mr. Marsh is preparing for a meeting with his banker to arrange the financing for the

first quarter. Based on his sales forecast and the following information he has provided,

your job as his new financial analyst is to prepare a monthly cash budget, monthly and

quarterly pro forma income statements, a pro forma quarterly balance sheet, and all

necessary supporting schedules for the first quarter.

Past history shows that Marsh Corporation collects 50 percent of its accounts receivable

in the normal 30-day credit period (the month after the sale) and the other 50 percent in 60

days (two months after the sale). It pays for its materials 30 days after receipt. In general,

Mr. Marsh likes to keep a two-month supply of inventory in anticipation of sales. Inventory

at the beginning of December was 2,600,000 units. (This was not equal to his desired two–

month supply.)

The major cost of production is the purchase of raw materials in the form of steel rods,

which are cut, threaded, and finished. Last year raw material costs were $52 per 1,000

fasteners, but Mr. Marsh has just been notified that material costs have risen, effective

January 1, to $60 per 1,000 fasteners. The Marsh Corporation uses FIFO inventory

accounting. Labor costs are relatively constant at $20 per thousand fasteners, since workers

are paid on a piecework basis. Overhead is allocated at $10 per thousand units, and selling

and administrative expense is 20 percent of sales. Labor expense and overhead are direct

cash outflows paid in the month incurred, while interest and taxes are paid quarterly.

The corporation usually maintains a minimum cash balance of $25,000, and it puts its

excess cash into marketable securities. The average tax rate is 40 percent, and Mr. Marsh

usually pays out 50 percent of net income in dividends to stockholders. Marketable

securities are sold before funds are borrowed when a cash shortage is faced. Ignore the

interest on any short-term borrowings. Interest on the long-term debt is paid in March, as

are taxes and dividends.

Chapter 04: Financial Forecasting

4-44

As of year-end, the Marsh Corporation balance sheet was as follows:

MARSH CORPORATION

Balance Sheet

December 31, 201X

Assets

Current assets:

Cash ……………………………………………………

$ 30,000

Accounts receivable ………………………………

320,000

Inventory ……………………………………………..

237,800

Total current assets ……………………………..

$ 587,800

Fixed assets:

Plant and equipment ………………………………

1,000,000

Less: Accumulated depreciation ……………

200,000

800,000

Total assets ……………………………………………

$1,387,800

Liabilities and Stockholders’ Equity

Accounts payable ……………………………………

$ 93,600

Notes payable…………………………………………

0

Long-term debt, 8 percent ………………………..

400,000

Common stock ……………………………………….

504,200

Retained earnings ……………………………………

390,000

Total liabilities and stockholders’ equity …….

$1,387,800

Chapter 04: Financial Forecasting

CP 4-2. Solution:

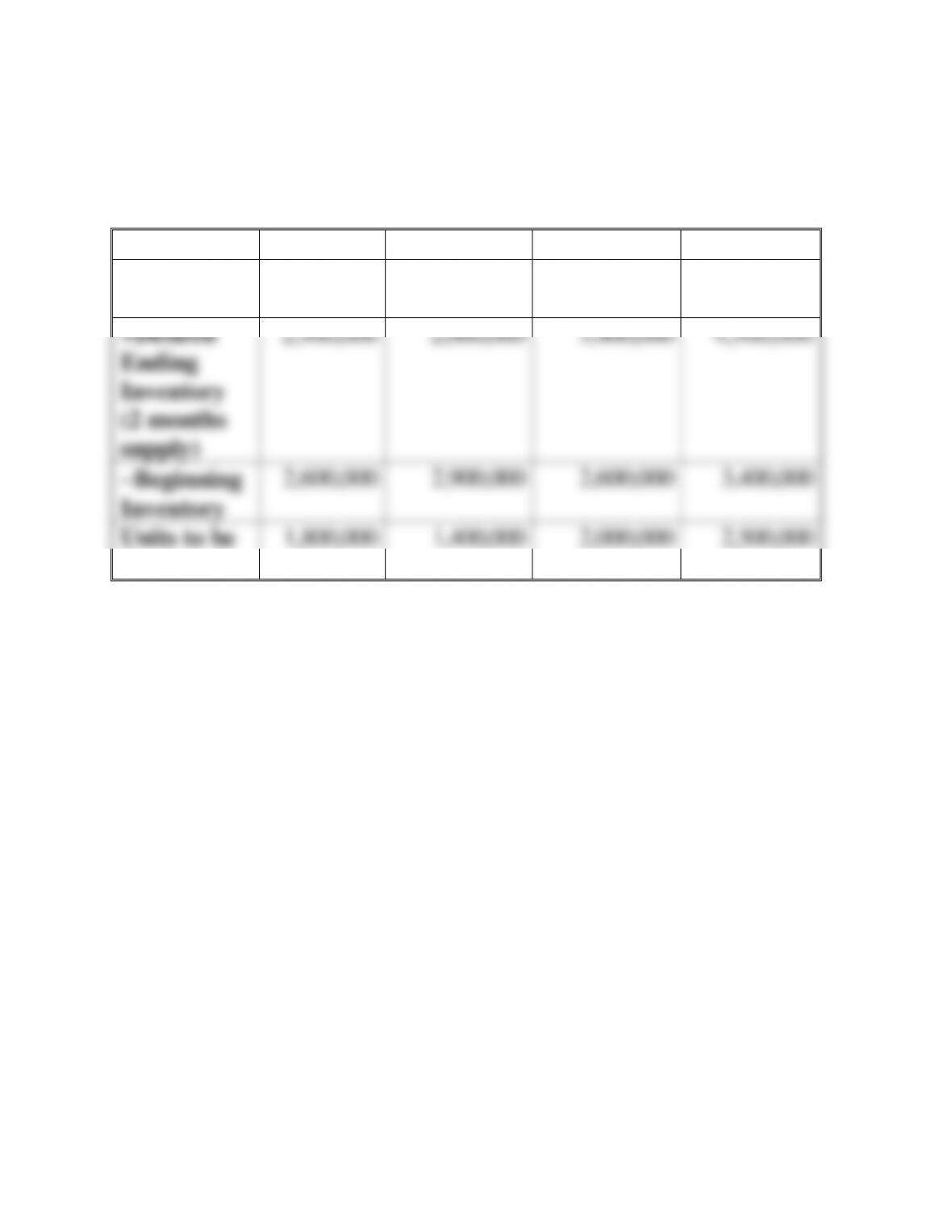

Marsh Corporation

Forecasting with Seasonal Production

Dec.

Jan.

Feb.

Mar.

Projected

Unit Sales

1,500,000

1,700,000

1,200,000

1,400,000

+Desired

Ending

Inventory

(2 months

supply)

2,900,000

2,600,000

3,400,000

4,500,000

−Beginning

Inventory

2,600,000

2,900,000

2,600,000

3,400,000

Units to be

Produced

1,800,000

1,400,000

2,000,000

2,500,000

Chapter 04: Financial Forecasting

CP 4-2. (Continued)

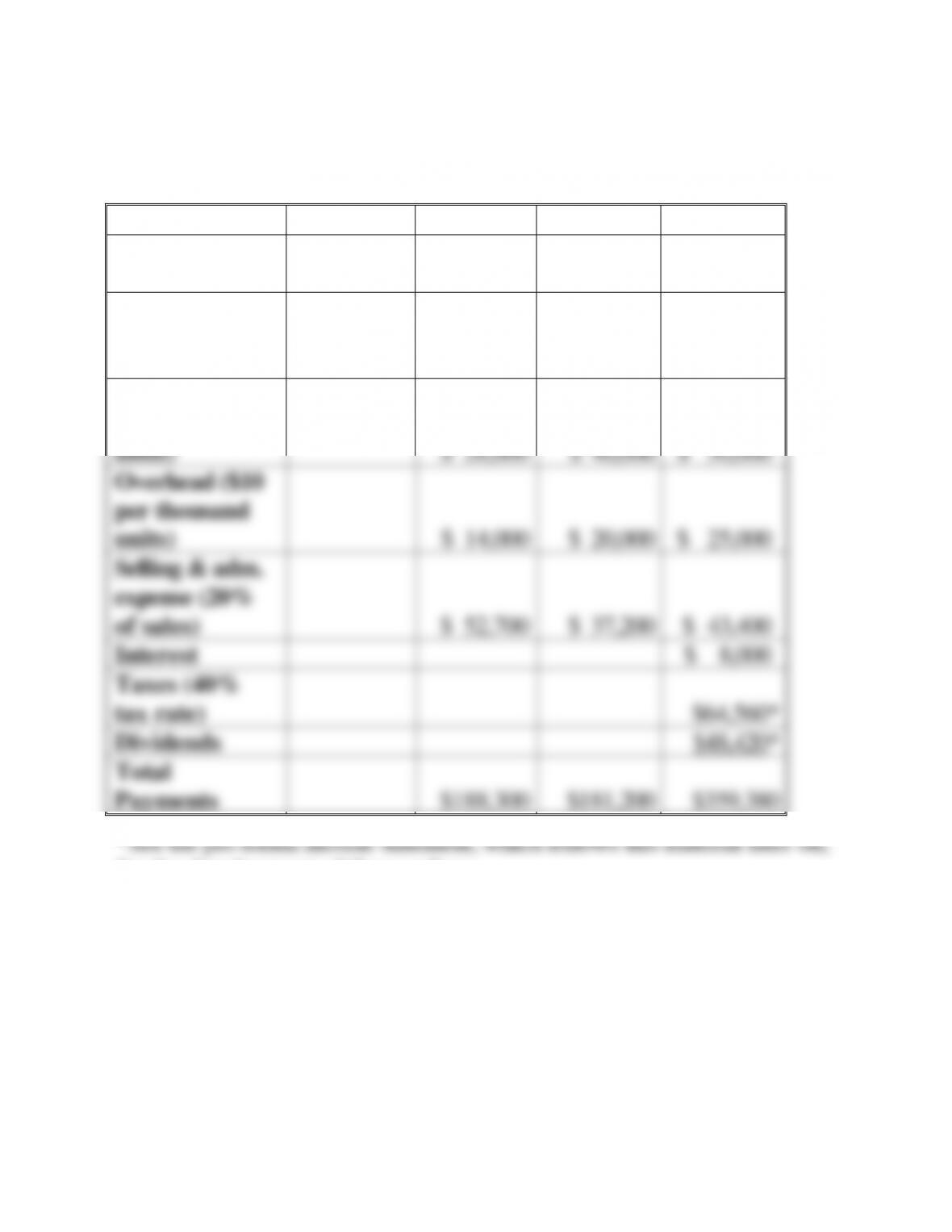

Monthly Cash Payments

Dec.

Jan.

Feb.

Mar.

Units to be

produced

1,800,000

1,400,000

2,000,000

2,500,000

Materials

(from previous

month)

$ 93,600

$ 84,000

$ 120,000

Labor ($20 per

thousand

units)

$ 28,000

$ 40,000

$ 50,000

Overhead ($10

per thousand

units)

$ 14,000

$ 20,000

$ 25,000

Selling & adm.

expense (20%

of sales)

$ 52,700

$ 37,200

$ 43,400

Interest

$ 8,000

Taxes (40%

tax rate)

$64,560*

Dividends

$48,420*

Total

Payments

$188,300

$181,200

$359,380

for the development of these values.

Chapter 04: Financial Forecasting

CP 4-2. (Continued)

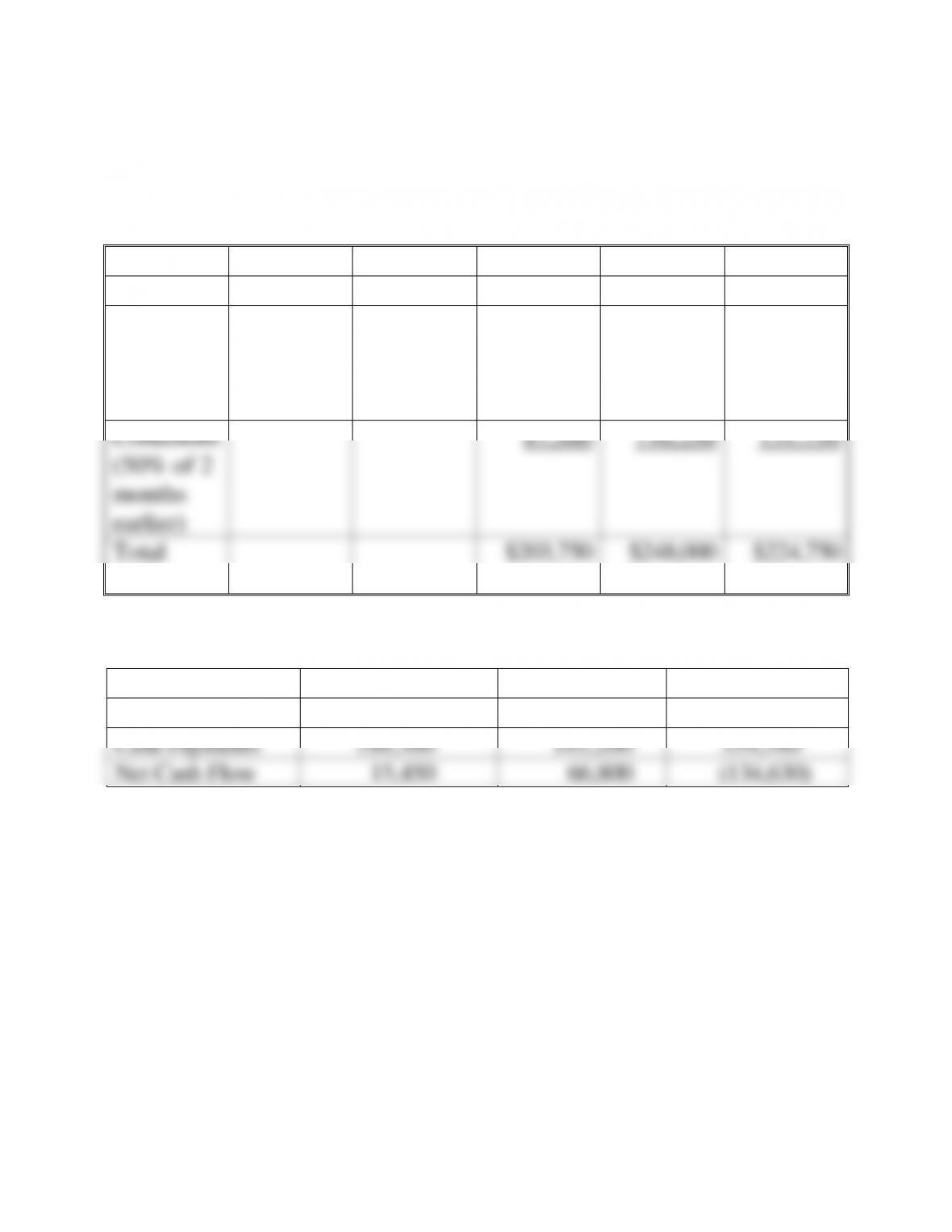

Marsh Corporation

Monthly Cash Receipts

Nov.

Dec.

Jan.

Feb.

Mar.

Sales

$175,000

$232,500

$263,500

$186,000

$217,000

Collections

(50% of

Previous

month)

87,500

116,250

131,750

93,000

Collections

(50% of 2

months

earlier)

87,500

116,250

131,750

Total

Collections

$203,750

$248,000

$224,750

Monthly Cash Flow

January

February

March

Cash Receipts

$203,750

$248,000

$224,750

Cash Payments

188,300

181,200

359,380

Net Cash Flow

15,450

66,800

(134,630)

Chapter 04: Financial Forecasting

4-48

CP 4-2. (Continued)

Marsh Corporation

Cash Budget

January

February

March

Net Cash Flow

$15,450

$66,800

$(134,630)

Beginning Cash Balance

30,000

25,000

25,000

Cumulative Cash Balance

$45,450

$91,800

($109,630)

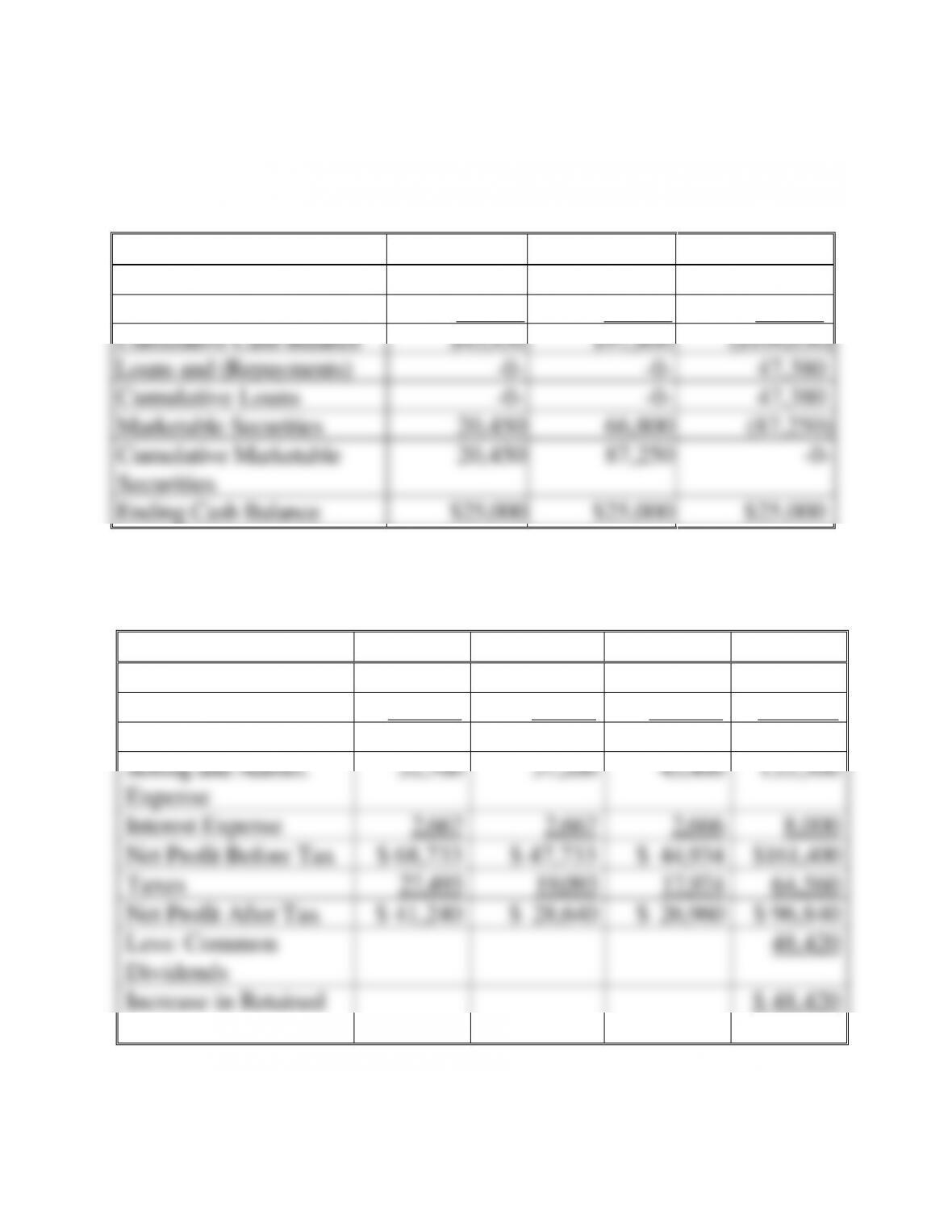

Loans and (Repayments)

-0-

-0-

47,380

Cumulative Loans

-0-

-0-

47,380

Marketable Securities

20,450

66,800

(87,250)

Cumulative Marketable

Securities

20,450

87,250

-0-

Ending Cash Balance

$25,000

$25,000

$25,000

Marsh Corporation

Pro Forma Income Statement

Jan.

Feb.

Mar.

Total

Sales

$263,500

$186,000

$217,000

$666,500

Cost of Goods Sold

139,400

98,400

126,000

363,800

Gross Profit

124,100

87,600

91,000

302,700

Selling and Admin.

Expense

52,700

37,200

43,400

133,300

Interest Expense

2,667

2,667

2,666

8,000

Net Profit Before Tax

$ 68,733

$ 47,733

$ 44,934

$161,400

Taxes

27,493

19,093

17,974

64,560

Net Profit After Tax

$ 41,240

$ 28,640

$ 26,960

$ 96,840

Less: Common

Dividends

48,420

Increase in Retained

Earnings

$ 48,420

Chapter 04: Financial Forecasting

4-49

CP 4-2. (Continued)

Marsh Corporation

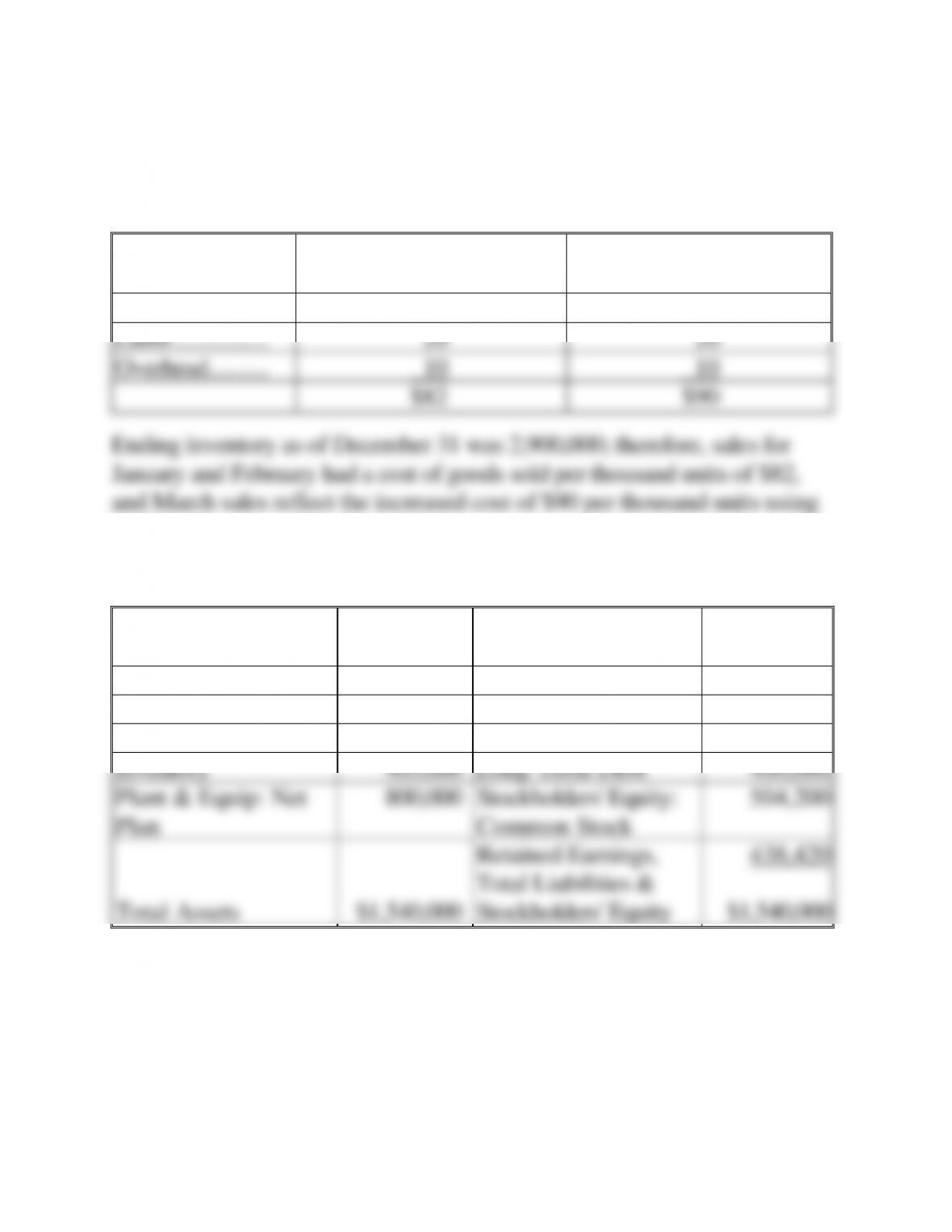

Cost of Goods Sold

Unit Cost per thousand

before January 1st

Unit cost per thousand

after January 1st

Material …………

$52

$60

Labor ……………..

20

20

Overhead ……….

10

10

$82

$90

Ending inventory as of December 31 was 2,900,000; therefore, sales for

January and February had a cost of goods sold per thousand units of $82,

and March sales reflect the increased cost of $90 per thousand units using

FIFO inventory methods.

Pro Forma Balance Sheet (March)

Assets

Liabilities &

Stockholders‘ Equity

Current Assets:

Current Liabilities:

Cash

$ 25,000

Accounts Payable

$ 150,000

Accounts Receivable

310,000

Notes Payable

47,380

Inventory

405,000

Long-Term Debt

400,000

Plant & Equip: Net

Plan

800,000

Stockholders‘ Equity:

Common Stock

504,200

Total Assets

$1,540,000

Retained Earnings,

Total Liabilities &

Stockholders‘ Equity

438,420

$1,540,000

Chapter 04: Financial Forecasting

4-50

CP 4-2. (Continued)

Explanation of Changes in the Balance Sheet:

Cash = ending cash balance from cash budget in March

Accounts receivable =

all of March sales

plus 50% of Feb.

sales

$217,000

93,000

$310,000

Inventory = ending inventory in March of 4,500,000 units at $90 per

thousand

Plant and equipment did not change since we did not include depreciation.

( )

( )

RE Old RE NI dividends

$390,000 $96,840 $48,240 $438,420

= + −

= + − =