Chapter 04: Financial Forecasting

4-21

21. Schedule of cash payments (LO2) The Denver Corporation has forecast the following

sales for the first seven months of the year:

January……… ……. $10,000 May……… $10,000

February……… ….. 12,000 June……… 16,000

March……… ……… 14,000 July…….. 18,000

April……… ……….. 20,000

Monthly material purchases are set equal to 30 percent of forecasted sales for the next

month. Of the total material costs, 40 percent are paid in the month of purchase and 60

percent in the following month. Labor costs will run $4,000 per month, and fixed overhead

is $2,000 per month. Interest payments on the debt will be $3,000 for both March and June.

Finally, the Denever salesforce will receive a 1.5 percent commission on total sales for the

first six months of the year, to be paid on June 30.

Prepare a monthly summary of cash payments for the six-month period from January

through June. (Note: Compute prior December purchases to help get total material

payments for January.)

Chapter 04: Financial Forecasting

4-22

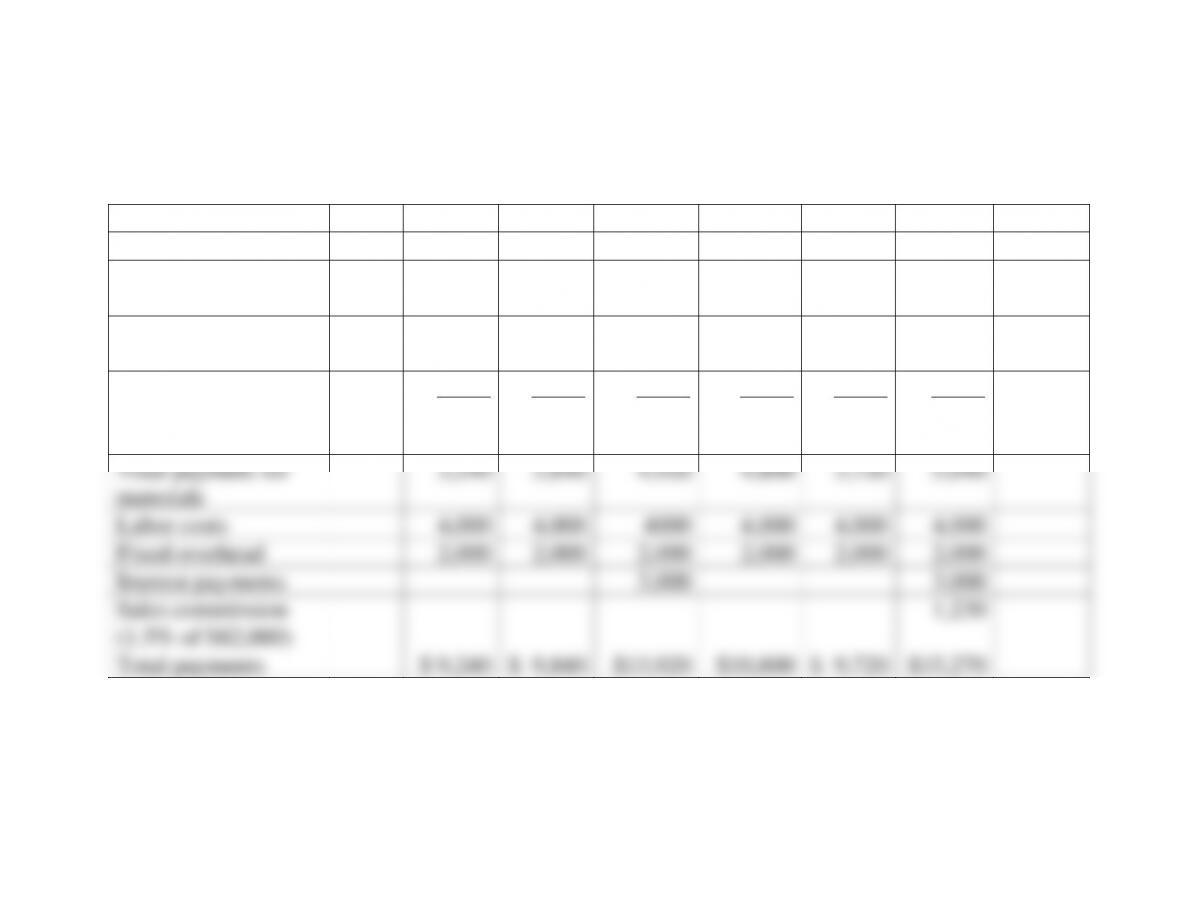

4-21. Solution:

Denver Corporation

Cash Payments Schedule

Dec.

Jan.

Feb.

March

April

May

June

July

Sales

$10,000

$12,000

$14,000

$20,000

$10,000

$16,000

$18,000

Purchases (30% of

next month’s sales)

3,000

3,600

4,200

6,000

3,000

4,800

5,400

Payment (40% of

current purchases)

1,440

1,680

2,400

1,200

1,920

2,160

Material payment

(60% of previous

month’s purchases)

1,800

2,160

2,520

3,600

1,800

2,880

Total payment for

materials

3,240

3,840

4,920

4,800

3,720

5,040

Labor costs

4,000

4,000

4000

4,000

4,000

4,000

Fixed overhead

2,000

2,000

2,000

2,000

2,000

2,000

Interest payments

3,000

3,000

Sales commission

(1.5% of $82,000)

1,230

Total payments

$ 9,240

$ 9,840

$13,920

$10,800

$ 9,720

$15,270

Chapter 04: Financial Forecasting

4-23

22. Schedule of cash payments (LO2) The Boswell Corporation forecasts its sales in units for

the next four months as follows:

March……….. ……. 6,000

April………… ……. 8,000

May…………. ……. 5,500

June…………. ……. 4,000

Boswell maintains an ending inventory for each month in the amount of one and one-half

times the expected sales in the following month. The ending inventory for February

(March’s beginning inventory) reflects this policy. Materials cost $5 per unit and are paid

for in the month after production. Labor cost is $10 per unit and is paid for in the month

incurred. Fixed overhead is $12,000 per month. Dividends of $20,000 are to be paid in

May. Five thousand units were produced in February.

Complete a production schedule and a summary of cash payments for March, April,

and May. Remember that production in any one month is equal to sales plus desired ending

inventory minus beginning inventory.

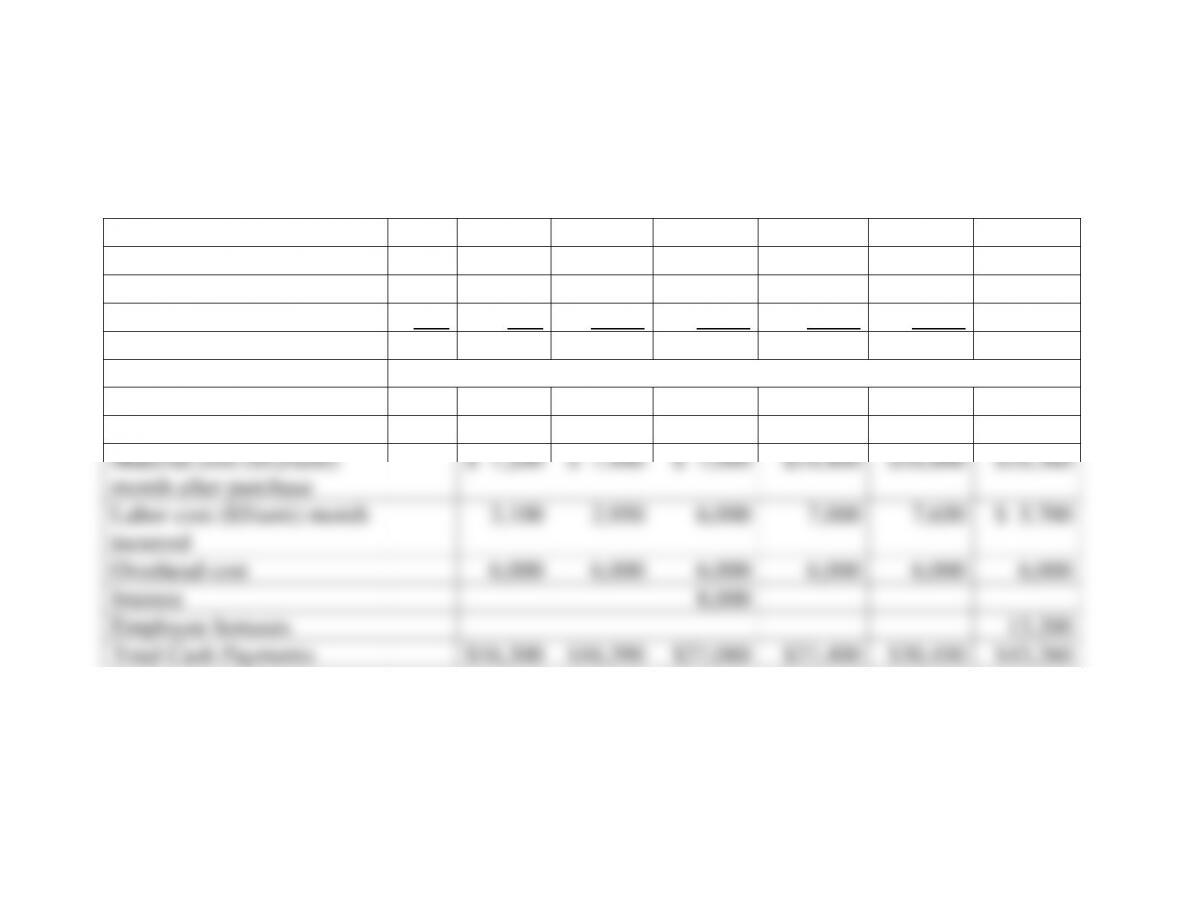

4-22. Solution:

Boswell Corporation

Production Schedule

March

April

May

June

Forecasted unit sales

6,000

8,000

5,500

4,000

+Desired ending

inventory

12,000

8,250

6,000

–Beginning inventory

9,000

12,000

8,250

Units to be produced

9,000

4,250

3,250

Cash Payments

Feb

March

April

May

Units produced

5,000

9,000

4,250

3,250

Materials ($5/unit)

month after production

$25,000

$45,000

$21,250

Labor ($10/unit)

month of production

90,000

42,500

32,500

Fixed overhead

12,000

12,000

12,000

Dividends

20,000

Total Cash Payments

$127,000

$99,500

$85,750

Chapter 04: Financial Forecasting

4-24

23. Schedule of cash payments (LO2) The Volt Battery Company has forecast its sales in

units as follows:

January……… ……. 800 May……… 1,350

February……… ….. 650 June……… 1,500

March……… ……… 600 July……… 1,200

April……… ……….. 1,100

Volt Battery always keeps an ending inventory equal to 120 percent of the next month’s

expected sales. The ending inventory for December (January’s beginning inventory) is 960

units, which is consistent with this policy.

Materials cost $12 per unit and are paid for in the month after purchase. Labor cost is $5

per unit and is paid in the month the cost is incurred. Overhead costs are $6,000 per month.

Interest of $8,000 is scheduled to be paid in March, and employee bonuses of $13,200 will

be paid in June.

Prepare a monthly production schedule and a monthly summary of cash payments for

January through June. Volt produced 600 units in December.

Chapter 04: Financial Forecasting

4-25

4-23. Solution:

Volt Battery Company

Production Schedule

Jan.

Feb.

March

April

May

June

July

Forecasted unit sales

800

650

600

1,100

1,350

1,500

1,200

+ Desired ending inventory

780

720

1,320

1,620

1,800

1,440

– Beginning inventory

960

780

720

1,320

1,620

1,800

= Units to be produced

620

590

1,200

1,400

1,530

1,140

Summary of Cash Payments

Dec.

Jan.

Feb.

March

April

May

June

Units produced

600

620

590

1,200

1,400

1,530

1,140

Material cost ($12/unit)

month after purchase

$ 7,200

$ 7,440

$ 7,080

$14,400

$16,800

$18,360

Labor cost ($5/unit) month

incurred

3,100

2,950

6,000

7,000

7,650

$ 5,700

Overhead cost

6,000

6,000

6,000

6,000

6,000

6,000

Interest

8,000

Employee bonuses

13,200

Total Cash Payments

$16,300

$16,390

$27,080

$27,400

$30,450

$43,260

Chapter 04: Financial Forecasting

4-26

24. Cash Budget (LO2) Lansing Auto Parts, Inc., has projected sales of $25,000 in October,

$35,000 in November, and $30,000 in December. Of the company’s sales, 20 percent are

paid for by cash and 80 percent are sold on credit. The credit sales are collected one month

after sale. Determine collections for November and December.

Also assume that the company’s cash payments for November and December are

$30,400 and $29,800, respectively. The beginning cash balance in November is $6,000,

which is the desired minimum balance.

Prepare a cash budget with borrowing needed or repayments for November and

December. (You will need to prepare a cash receipts schedule first.)

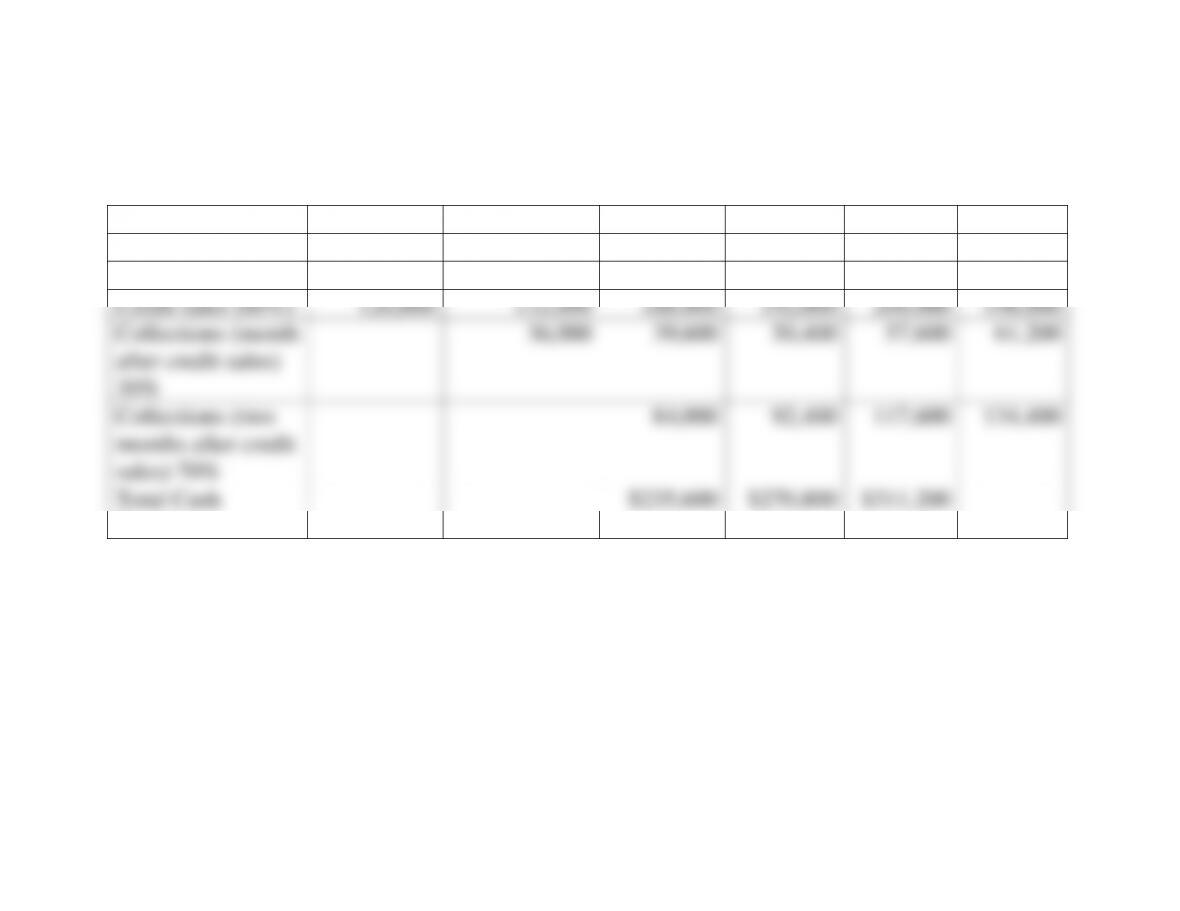

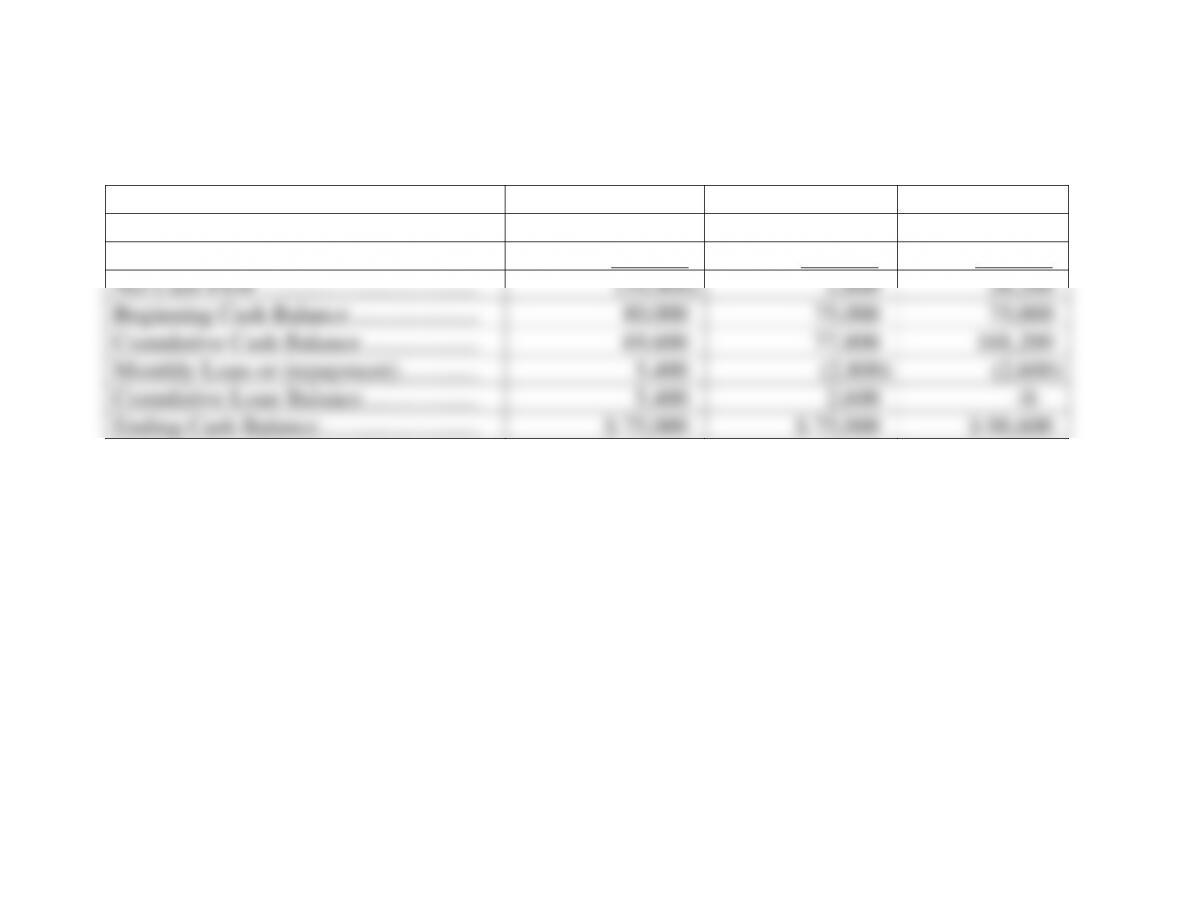

4-24. Solution:

Lansing Auto Parts, Inc.

Cash Receipts Schedule

October

November

December

Sales

$25,000

$35,000

$30,000

Cash sales (20%)

7,000

6,000

Collections (80% of

previous month’s

sales)

20,000

28,000

Total cash receipts

$27,000

$34,000

Lansing Auto Parts, Inc.

Cash Budget

November

July

Cash Receipts

$27,000

$34,000

Cash Payments

30,400

29,800

Net Cash Flow

(3,400)

4,200

Beginning Cash Balance

6,000

6,000

Cumulative Cash Balance

2,600

10,200

Monthly Loan or (Repayment)

3,400

(3,400)

Cumulative Loan Balance

3,400

-0-

Ending Cash Balance

$ 6,000

$ 6,800

Chapter 04: Financial Forecasting

4-27

25. Complete cash budget (LO2) Harry’s Carryout Stores has eight locations. The firm wishes

to expand by two more stores and needs a bank loan to do this. Mr. Wilson, the banker, will

finance construction if the firm can present an acceptable three-month financial plan for

January through March. The following are actual and forecasted sales figures:

Actual Forecast Additional Information

November ……….. $200,000 January ………. $280,000 April forecast ….. $330,000

December ……….. 220,000 February …….. 320,000

March……… . 340,000

Of the firm’s sales, 40 percent are for cash and the remaining 60 percent are on credit. Of

credit sales, 30 percent are paid in the month after sale and 70 percent are paid in the

second month after the sale. Materials cost 30 percent of sales and are purchased and

received each month in an amount sufficient to cover the following month’s expected sales.

Materials are paid for in the month after they are received. Labor expense is 40 percent of

sales and is paid for in the month of sales. Selling and administrative expense is 5 percent

of sales and is also paid in the month of sales. Overhead expense is $28,000 in cash per

month.

Depreciation expense is $10,000 per month. Taxes of $8,000 will be paid in January,

and dividends of $2,000 will be paid in March. Cash at the beginning of January is

$80,000, and the minimum desired cash balance is $75,000.

For January, February, and March, prepare a schedule of monthly cash receipts, monthly

cash payments, and a complete monthly cash budget with borrowings and repayments.

Chapter 04: Financial Forecasting

4-25. Solution:

Harry’s Carry-Out Stores

Cash Receipts Schedule

November

December

January

February

March

April

Sales

$200,000

$220,000

$ 280,000

$320,000

$340,000

$330,000

Cash sales (40%)

80,000

88,000

112,000

128,000

136,000

132,000

Credit sales (60%)

120,000

132,000

168,000

192,000

204,000

198,000

Collections (month

after credit sales)

30%

36,000

39,600

50,400

57,600

61,200

Collections (two

months after credit

sales) 70%

84,000

92,400

117,600

134,400

Total Cash

Receipts

$235,600

$270,800

$311,200

Chapter 04: Financial Forecasting

4-29

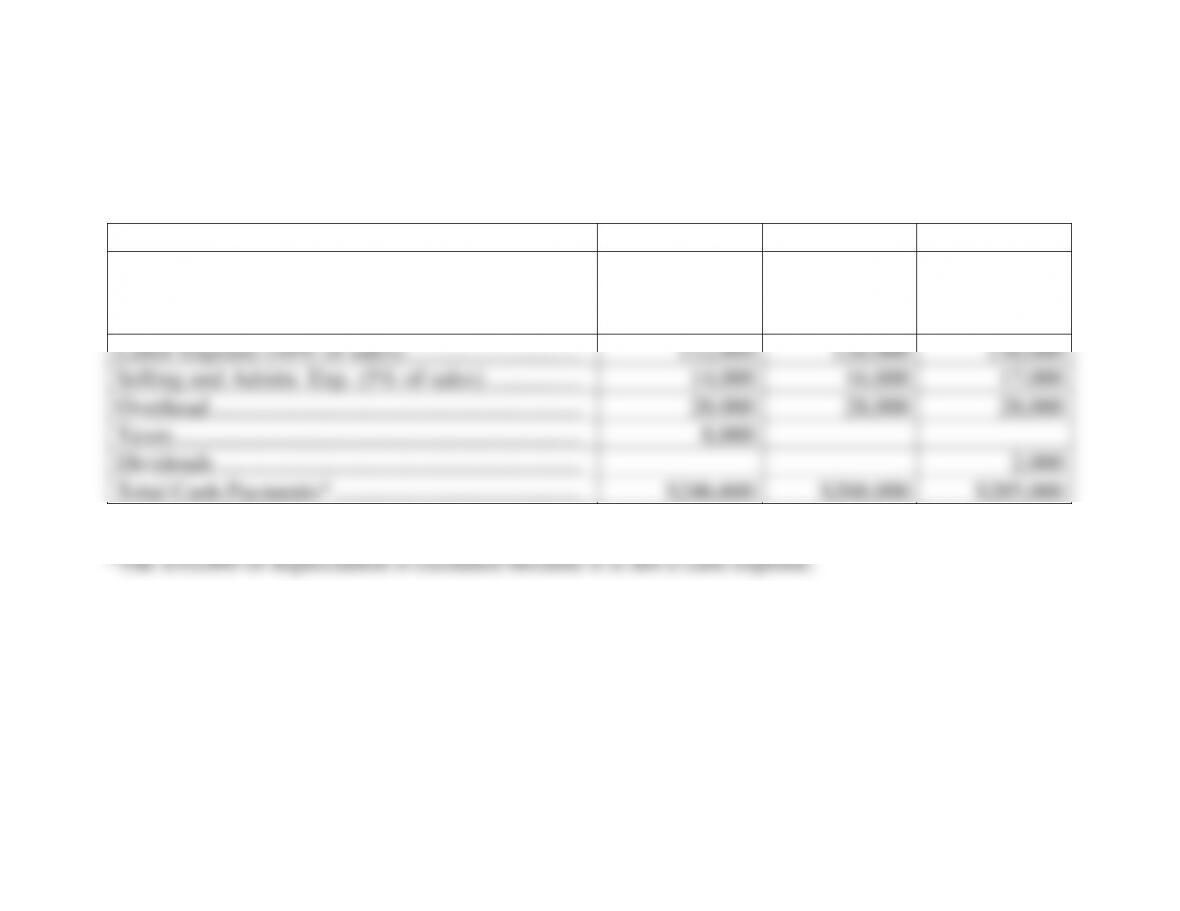

4-25. (Continued) Harry’s Carry-Out Stores

Cash Payments Schedule

January

February

March

Payments for Purchases (30% of next month’s

sales paid in month after purchases—equivalent

to 30% of current sales) …………………………………

$ 84,000

$ 96,000

$102,000

Labor Expense (40% of sales) ………………………..

112,000

128,000

136,000

Selling and Admin. Exp. (5% of sales) …………….

14,000

16,000

17,000

Overhead …………………………………………………….

28,000

28,000

28,000

Taxes ………………………………………………………….

8,000

Dividends ……………………………………………………

2,000

Total Cash Payments* …………………………..………

$246,600

$268,000

$285,000

Chapter 04: Financial Forecasting

4-30

4-25. (Continued)

Harry’s Carry-Out Stores

Cash Budget

January

February

March

Total Cash Receipts ……………………….

$235,600

$270,800

$311,200

Total Cash Payments ……………………..

246,000

268,000

285,000

Net Cash Flow ………………………………

(10,400)

2,800

26,200

Beginning Cash Balance …………………

80,000

75,000

75,000

Cumulative Cash Balance ……………….

69,600

77,800

101,200

Monthly Loan or (repayment) ………….

5,400

(2,800)

(2,600)

Cumulative Loan Balance ……………….

5,400

2,600

-0-

Ending Cash Balance ……………………..

$ 75,000

$ 75,000

$ 98,600