Chapter 04: Financial Forecasting

4-11

Beginning inventory at these costs on July 1 was 3,000 units. From July 1 to December

1, 2011, Bradley produced 12,000 units. These units had a material cost of $3, labor of $5,

and overhead of $3 per unit. Bradley uses FIFO inventory accounting.

Assuming that Bradley sold 13,000 units during the last six months of the year at $16

each, what is its gross profit? What is the value of ending inventory?

4-14. Solution:

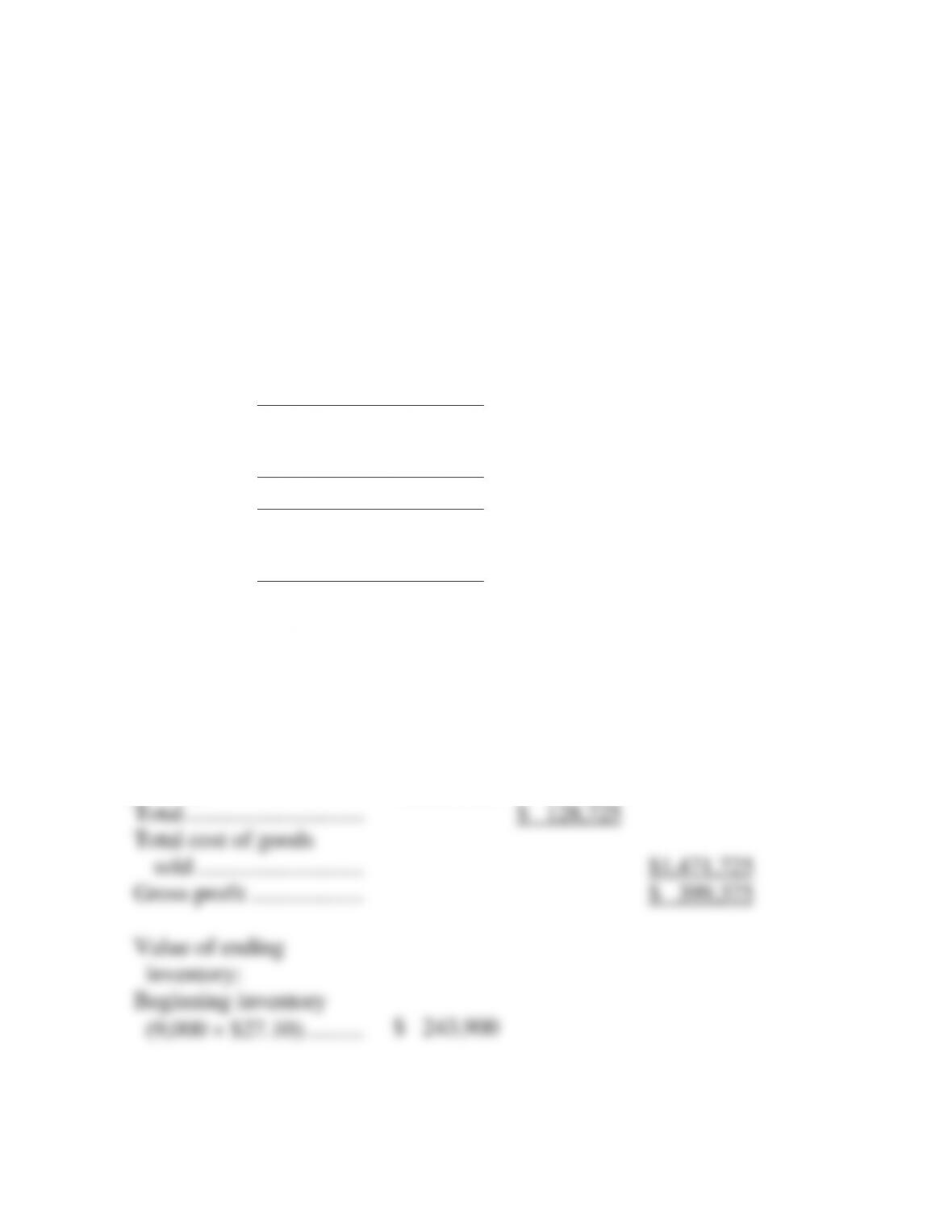

Bradley Corporation

Sales (13,000 @ $16)

$208,000

Cost of goods sold:

Old inventory:

Quantity (units) ………..

3,000

Cost per unit …………….

$ 8

Total …………………………

$ 24,000

New inventory:

Quantity (units) ………..

10,000

Cost per unit …………….

$ 11

Total …………………………

$ 110,000

Total cost of goods

sold ……………………….

$134,000

Gross profit ……………….

$ 74,000

Value of ending

inventory:

Beginning inventory

(3,000 $8) ……………..

$ 24,000

+ Total production

(12,000 $11) ………….

$132,000

Total inventory

available for sale ………

$156,000

– Cost of good sold ……

$134,000

Ending inventory ………..

$ 22,000

Or

2,000 units $11 = $22,000

Chapter 04: Financial Forecasting

4-12

15. Gross profit and ending inventory (LO2) Assume in Problem 14 that the Bradley

Corporation used LIFO accounting instead of FIFO; what would its gross profit be? What

would be the value of ending inventory?

4-15. Solution:

Bradley Corporation(Continued)

Sales (13,000 @ $16)

$208,000

Cost of goods sold:

New inventory:

Quantity (units) ………..

12,000

Cost per unit …………….

$ 11

Total …………………………

$132,000

Old inventory:

Quantity (units) ………..

1,000

Cost per unit …………….

$ 8

Total …………………………

$ 8,000

Total cost of goods

sold ……………………….

$140,000

Gross profit ……………….

$ 68,000

Value of ending

inventory:

Beginning inventory

(3,000 $8) ……………..

$ 24,000

+ Total production

(12,000 $11) ………….

$132,000

Total inventory

available for sale ………

$156,000

– Cost of good sold ……

$140,000

Ending inventory ………..

$ 16,000

Or

2,000 units $8 = $16,000

Chapter 04: Financial Forecasting

4-13

16. Gross profit and ending inventory (LO2) Sprint Shoes, Inc., had a beginning inventory

of 9,000 units on January 1, 2010. The costs associated with the inventory were:

Material ……………. $13.00 per unit

Labor ……………….. 8.00 per unit

Overhead ………….. 6.10 per unit

During 2010, the firm produced 42,500 units with the following costs:

Material ……………. $15.50 per unit

Labor ……………….. 7.80 per unit

Overhead ………….. 8.30 per unit

Sales for the year were 47,250 units at $39.60 each. Sprint Shoes uses LIFO accounting.

What was the gross profit? What was the value of ending inventory?

4-16. Solution:

Sprint Shoes, Inc.

Sales (47,250 @ $39.60)

$1,871,100

Cost of goods sold:

New inventory:

Quantity (units) ………..

42,500

Cost per unit …………….

$ 31.60

Total …………………………

$1,343,000

Old inventory:

Quantity (units) ………..

4,750

Cost per unit …………….

$ 27.10

Total …………………………

$ 128,725

Total cost of goods

sold ……………………….

$1,471,725

Gross profit ……………….

$ 399,375

Value of ending

inventory:

Beginning inventory

(9,000 $27.10) ……….

$ 243,900

Chapter 04: Financial Forecasting

+ Total production

(42,500 $31.60) ……..

$1,343,000

Total inventory

available for sale ………

$1,586,900

– Cost of good sold ……

$1,471,725

Ending inventory ………..

$ 115,175

Or

42,500 units $27.10 = $115,175

17. Schedule of cash receipts (LO2) Victoria’s Apparel has forecast credit sales for the fourth

quarter of the year as:

September (actual) ……… $50,000

Fourth Quarter

October …………………….. $40,000

November …………………. 35,000

December………………….. 60,000

Experience has shown that 20 percent of sales receipts are collected in the month of sale,

70 percent in the following month, and 10 percent are never collected.

Prepare a schedule of cash receipts for Victoria’s Apparel covering the fourth quarter

(October through December).

4-17. Solution:

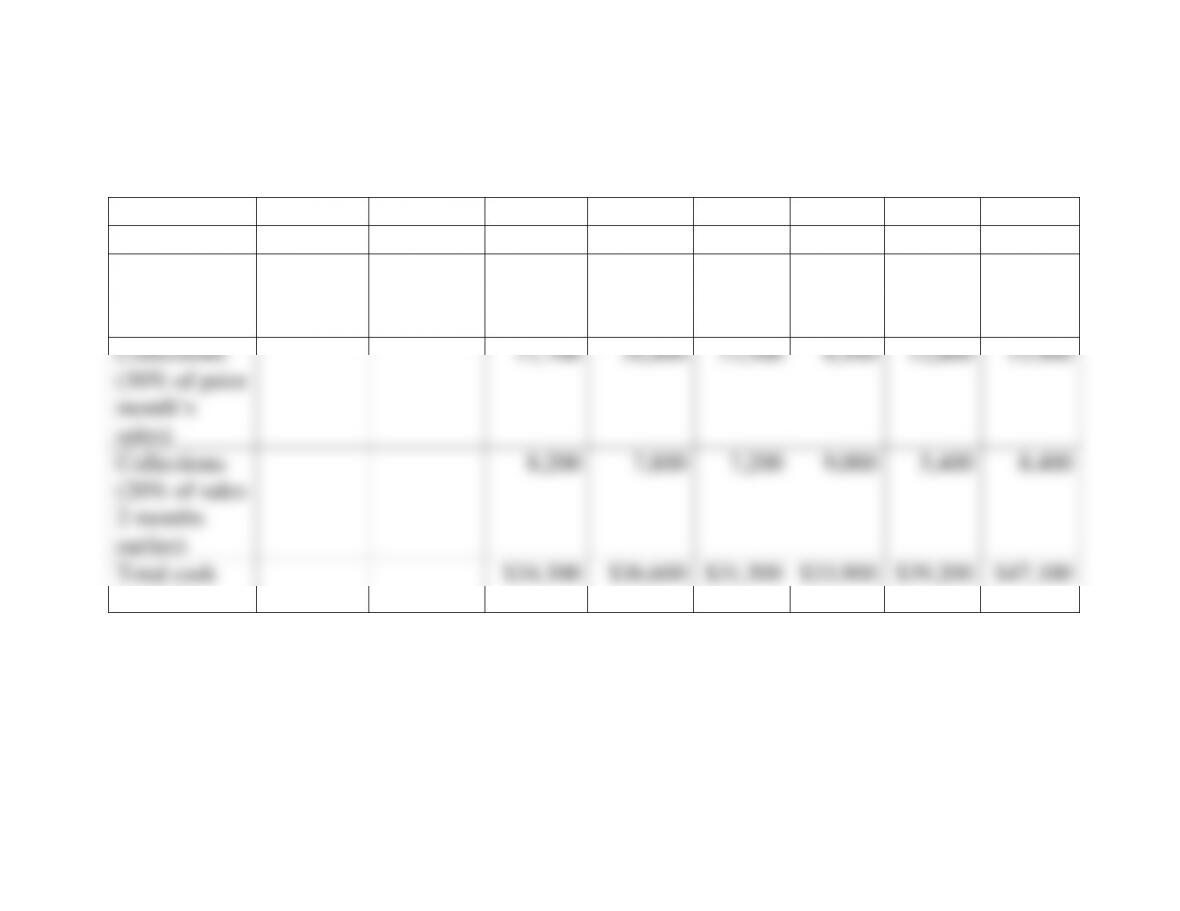

Victoria’s Apparel

September

October

November

December

Credit sales

$50,000

$40,000

$35,000

$60,000

20% Collected

in month of

sales

8,000

7,000

12,000

70%

Collected in

month after

sales

35,000

28,000

24,500

Total cash

receipts

$43,000

$35,000

$36,500

Chapter 04: Financial Forecasting

4-15

18. Schedule of cash receipts (LO2) Simpson Glove Company has made the following sales

projections for the next six months. All sales are credit sales.

March ………………………. $36,000

April ………………………… 45,000

May …………………………. 27,000

June …………………………. 42,000

July ………………………….. 53,000

August ……………………… 57,000

Sales in January and February were $41,000 and $39,000 respectively. Experience has

shown that of total sales receipts 10 percent are uncollectible, 40 percent are collected in

the month of sale, 30 percent are collected in the following month, and 20 percent are

collected two months after sale.

Prepare a monthly cash receipts schedule for the firm for March through August.

Chapter 04: Financial Forecasting

4-18. Solution:

Simpson Glove Company

Cash Receipts Schedule

January

February

March

April

May

June

July

August

Sales

$41,000

$39,000

$36,000

$45,000

$27,000

$42,000

$53,000

$57,000

Collections

(40% of

current sales)

14,400

18,000

10,800

16,800

21,200

22,800

Collections

(30% of prior

month’s

sales)

11,700

10,800

13,500

8,100

12,600

15,900

Collections

(20% of sales

2 months

earlier)

8,200

7,800

7,200

9,000

5,400

8,400

Total cash

receipts

$34,300

$36,600

$31,500

$33,900

$39,200

$47,100

Chapter 04: Financial Forecasting

4-17

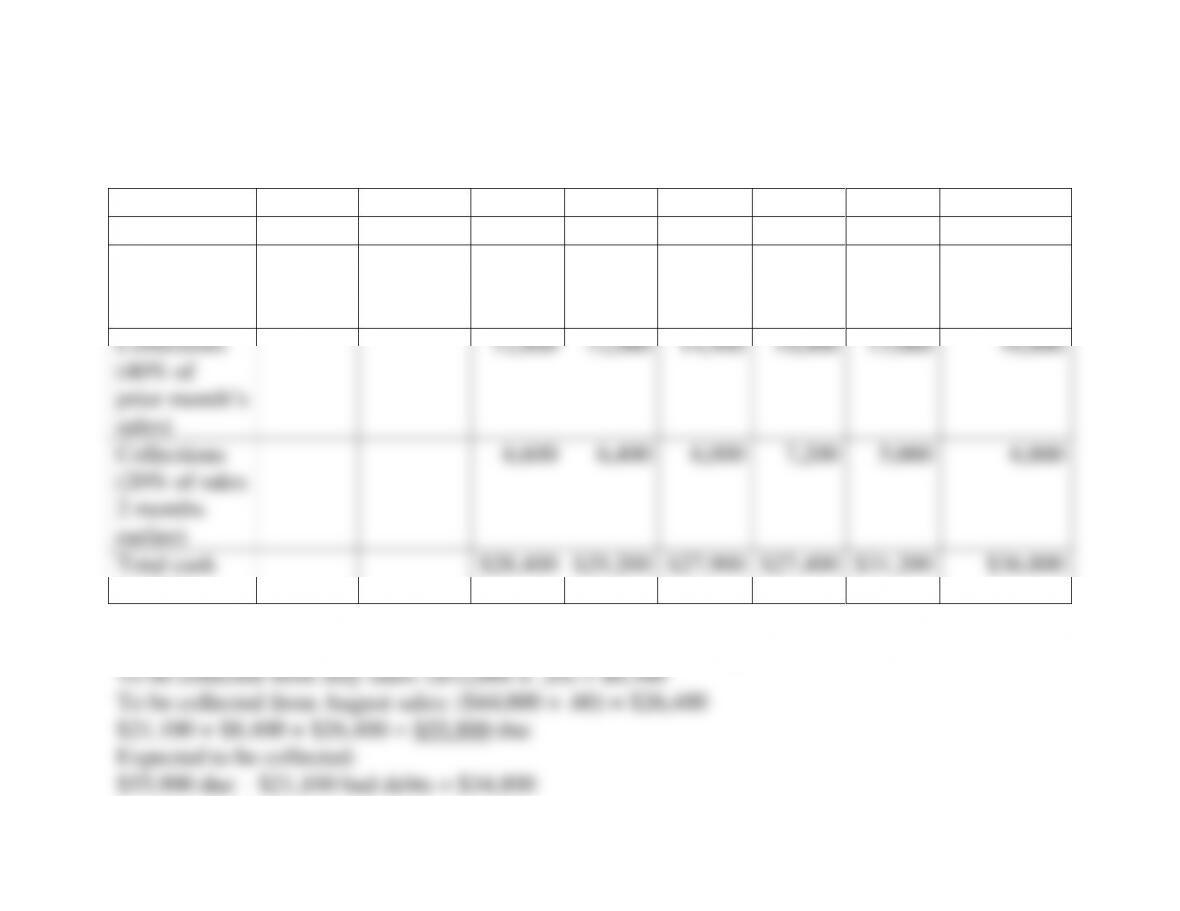

19. Schedule of cash receipts (LO2) Watt’s Lighting Stores made the following sales

projection for the next six months. All sales are credit sales.

March ………………………. $30,000

April ………………………… 36,000

May …………………………. 25,000

June …………………………. 34,000

July ………………………….. 42,000

August ……………………… 44,000

Sales in January and February were $33,000 and $32,000, respectively.

Experience has shown that of total sales, 10 percent are uncollectible, 30 percent are

collected in the month of sale, 40 percent are collected in the following month, and 20

percent are collected two months after sale.

Prepare a monthly cash receipts schedule for the firm for March through August.

Of the sales expected to be made during the six months from March through August,

how much will still be uncollected at the end of August? How much of this is expected to

be collected later?

Chapter 04: Financial Forecasting

4-19. Solution:

Watt’s Lighting Stores

Cash Receipts Schedule

January

February

March

April

May

June

July

August

Sales

$33,000

$32,000

$30,000

$36,000

$25,000

$34,000

$42,000

$44,000

Collections

(30% of

current sales)

9,000

10,800

7,500

10,200

12,600

13,200

Collections

(40% of

prior month’s

sales)

12,800

12,000

14,400

10,000

13,600

16,800

Collections

(20% of sales

2 months

earlier)

6,600

6,400

6,000

7,200

5,000

6,800

Total cash

receipts

$28,400

$29,200

$27,900

$27,400

$31,200

$36,800

Still due (uncollected) in August:

Bad debts: ($30,000 + 36,000 + 25,000 + 34,000 + 42,000 + 44,000) × .1 = (211,000) × .1 = $21,100

Chapter 04: Financial Forecasting

4-19

20. Schedule of cash payments (LO2) Ultravision, Inc., anticipates sales of $240,000 from

January through April. Materials will represent 50 percent of sales and because of level

production, material purchases will be equal for each month during the four months of

January, February, March, and April.

Materials are paid for one month after the month purchased. Materials purchased in

December of last year were $20,000 (half of $40,000 in sales). Labor costs for each of the

four months are slightly different due to a provision in the labor contract in which bonuses

are paid in February and April. The labor figures are:

January …………………….. $10,000

February …………………… 13,000

March ………………………. 10,000

April ………………………… 15,000

Fixed overhead is $6,000 per month. Prepare a schedule of cash payments for January through

April.

Chapter 04: Financial Forecasting

4-20

4-20. Solution:

Ultravision, Inc.

Cash Payment Schedule

Dec.

Jan.

Feb.

March

April

* Purchases

$20,000

$30,000

$30,000

$30,000

$30,000

** Payment to material purchases

20,000

30,000

30,000

30,000

Labor

10,000

13,000

10,000

15,000

Fixed overhead

6,000

6,000

6,000

6,000

Total Cash Payments

$36,000

$49,000

$46,000

$51,000

For January through April