Chapter 03: Financial Analysis

3-51

Bonds payable ………………………………. 150,000

Total liabilities ……………………………… $320,000

Stockholders’ equity

Preferred stock, $50 per value …………. 100,000

Common stock, $1 par value …………… 80,000

Capital paid in excess of par ……………. 190,000

Retained earnings ………………………….. 210,000

Total stockholders’ equity ……………. 580,000

Total liabilities and stockholders’ equity $900,000

SNIDER CORPORATION

Income statement

For the Year Ending December 31, 2010

Sales (on credit) …………………………………………………………………..

$1,980,000

Less: Cost of goods sold …………………………………………………...

1,280,000

Gross profit ………………………………………………………………………...

700,000

Less: Selling and administrative expenses …………………………….

475,000*

Operating profit (EBIT) ………………………………………………………..

225,000

Less: Interest expense ……………………………………………………….

25,000

Earnings before taxes (EBT) ………………………………………………….

200,000

Less: Taxes ……………………………………………………………………..

80,000

Earnings after taxes (EAT) …………………………………………………….

$ 120,000

*Includes $35,000 in lease payments.

3-36. Solution:

Snider Corporation

Profitability ratios

Profit margin = $120,000/$1,980,000 = 6.06%

Assets utilization ratios

Chapter 03: Financial Analysis

3-52

Receivable turnover = $1,980,000/$160,000 = 12.38x

Average collection period = $160,000/$5,500 = 29.09 days

Liquidity ratio

Debt utilization ratios

Debt to total assets = $320,000/$900,000 = 35.56%

37. Ratio computation and analysis (LO2) Given the financial statements for Jones

Corporation and Smith Corporation shown here:

a. To which one would you, as credit manager for a supplier, approve the extension of

(short-term) trade credit? Why? Compute all ratios before answering.

b. In which one would you buy stock? Why?

JONES CORPORATION

Current Assets

Liabilities

Cash ……………………………………..

$ 20,000

Accounts payable ………………

$100,000

Accounts receivable ………………..

80,000

Bonds payable (long-term) ….

80,000

Inventory……………………………….

50,000

Long-Term Assets

Stockholders’ Equity

Fixed assets …………………………...

$500,000

Common stock ………………….

$150,000

Less: Accumulated depreciation

(150,000)

Paid-in capital …………………..

70,000

Net fixed assets* …………………….

350,000

Retained earnings………………

100,000

Total assets…………………………

$500,000

Total liab. and equity……..

$500,000

Sales (on credit) ………………………………………………………………………..

$1,250,000

Cost of goods sold ……………………………………………………….

750,000

Gross profit ……………………………………………………………….……………..

500,000

Selling and administrative expense† …………………………….……………..

257,000

Less: Depreciation expense ………………………………………..……………..

50,000

Operating profit ……………………………………………………….………………..

193,000

Interest expense ……………………………………………………….………………..

8,000

Earnings before taxes ………………………………………………….……

185,000

Chapter 03: Financial Analysis

3-53

Tax expense ……………………………………………………………………………..

92,500

Net income ………………………………………………………………..……………..

$ 92,500

*Use net fixed assets in computing fixed asset turnover.

†Includes $7,000 in lease payments.

SMITH CORPORATION

Current Assets

Liabilities

Cash ………………………….

$ 35,000

Accounts payable ………………

$ 75,000

Marketable securities …..

7,500

Bonds payable (long-term) ….

210,000

Accounts receivable …….

70,000

Inventory …………………..

75,000

Long-Term Assets

Stockholders’ Equity

Fixed assets ………………..

$500,000

Common stock ………………….

$ 75,000

Less: Accum. dep. …….

(250,000)

Paid-in capital …………………..

30,000

Net fixed assets* …………

250,000

Retained earnings ……………..

47,500

Total assets ……………

$437,500

Total liab. and equity ……….

$437,500

*Use net fixed assets in computing fixed asset turnover.

SMITH CORPORATION

Sales (on credit) …………………………………………………………..……………

$1,000,000

Cost of goods sold ………………………………………………………..……………

600,000

Gross profit ………………………………………………………………………………

400,000

Selling and administrative expense† ……………………………………………

224,000

Less: Depreciation expense ………………………………………………………

50,000

Operating profit…………………………………………………………………………

126,000

Interest expense…………………………………………………………………………

21,000

Earnings before taxes …………………………..……………………….….

105,000

Tax expense ……………………………………………………….……….……………

52,500

Net income………………………………………………………………….……………

$ 52,500

†Includes $7,000 in lease payments.

3-37. Solution:

Jones and Smith Comparison

One way of analyzing the situation for each company is to

compare the respective ratios for each. Examining those ratios

which would be most important to a supplier or short-term lender

and a stockholder.

Chapter 03: Financial Analysis

3-54

JONES CORPORATION

Profit margin = $92,500/$1,250,000 = 7.40%

Return on assets (investment) = $92,500/$500,000 = 18.50%

Return on equity = $92,500/$320,000 = 28.91%

SMITH CORPORATION

Profit margin = $52,500/$1,000,000 = 5.25%

Return on assets (investment) = $52,500/$437,500 = 12.0%

Return on equity = $52,500/$152,500 = 34.43%

3-37. (Continued)

a. Since suppliers and short-term lenders are most concerned with

liquidity ratios, Smith Corporation would get the nod as having

Chapter 03: Financial Analysis

3-55

the best ratios in this category. One could argue, however, that

Smith had benefited from having its debt primarily long term

rather than short term. Nevertheless, it appears to have better

liquidity ratios.

b. Stockholders are most concerned with profitability. In this

category, Jones has much better ratios than Smith. Smith does

Smith and its lower liquidity ratios could reflect better short-term

asset management, and that point was covered in part a.

Note: Remember that to make actual financial decisions more than

one year’s comparative data is usually required. Industry

comparisons should also be made.

SMITH CORPORATION

Sales (on credit) …………………………………..

$1,000,000

Cost of goods sold ………………………………..

600,000

Gross profit………………………………………….

400,000

Selling and administrative expense ………

224,000

Less: Depreciation expense ………………….

50,000

Operating profit ……………………………………

126,000

Interest expense ……………………………………

21,000

Earnings before taxes …………………………...

105,000

Tax expense …………………………………………

52,500

Net income ………………………………………….

$ 52,500

Includes $7,000 in lease payments.

Chapter 03: Financial Analysis

3-56

COMPREHENSIVE PROBLEM

Comprehensive Problem 1.

Lamar Swimwear (trend analysis and industry comparisons)(LO3) Bob Adkins has recently

been approached by his first cousin, Ed Lamar, with a proposal to buy a 15 percent interest in

Lamar Swimwear. The firm manufactures stylish bathing suits and sunscreen products.

Mr. Lamar is quick to point out the increase in sales that has taken place over the last three years

as indicated in the income statement, Exhibit 1. The annual growth rate is 25 percent. A balance

sheet for a similar time period is shown in Exhibit 2, and selected industry ratios are presented in

Exhibit 3. Note the industry growth rate in sales is only 10 to 12 percent per year.

There was a steady real growth of 3 to 4 percent in gross domestic product during the period

under study.

Comprehensive Problem 1 (Continued)

Exhibit 1

LAMAR SWIMWEAR

Income Sheet

201X

201Y

201Z

Sales (all on credit) …………………………………….

$1,200,000

$1,500,000

$1,875,000

Cost of goods sold ………………………………………

800,000

1,040,000

1,310,000

Gross profit ……………………………………………….

$ 400,000

$ 460,000

$ 565,000

Selling and administrative expense* ………………

239,900

274,000

304,700

Operating profit (EBIT)……………………………….

$ 160,100

$ 186,000

$ 260,300

Interest expense ………………………………………….

35,000

45,000

85,000

Net income before taxes ………………………………

$ 125,100

$ 141,000

$ 175,300

Taxes ……………………………………………………….

36,900

49,200

55,600

Net income ………………………………………………..

$ 88,200

$ 91,800

$ 119,700

Shares ………………………………………………………

30,000

30,000

38,000

Earnings per share ………………………………………

$ 2.94

$ 3.06

$ 3.15

*Includes $15,000 in lease payments for each year.

Exhibit 2

LAMAR SWIMWEAR

Balance Sheet

Assets

201X

201Y

201Z

Cash …………………………………………………………

$ 30,000

$ 40,000

$ 30,000

Marketable securities ………………………………….

20,000

25,000

30,000

Accounts receivable ……………………………………

170,000

259,000

360,000

Inventory…………………………………………………..

230,000

261,000

290,000

Total current assets …………………………..……..

$ 450,000

$ 585,000

$ 710,000

Chapter 03: Financial Analysis

3-57

Net plant and equipment………………………………

650,000

765,000

1,390,000

Total assets ……………………………………………….

$1,100,000

$1,350,000

$ 2,100,000

Liabilities and Stockholders’ Equity

Accounts payable ……………………………………….

$ 200,000

$ 310,000

$ 505,000

Accrued expenses ……………………………………….

20,400

30,000

35,000

Total current liabilities …………………………….

$ 220,400

$ 340,000

$ 540,000

Long-term liabilities …………………………..……….

325,000

363,600

703,900

Total liabilities ……………………………………….

$ 545,400

$ 703,600

$ 1,243,900

Common stock ($2 par) …………………………..…..

60,000

60,000

76,000

Capital paid in excess of par …………………………

190,000

190,000

264,000

Retained earnings ……………………………………….

304,600

396,400

516,100

Total stockholders’ equity ………………………..

$ 554,600

$ 646,400

$ 856,100

Total liabilities and stockholders’ equity ………..

$1,100,000

$1,350,000

$2, 100,000

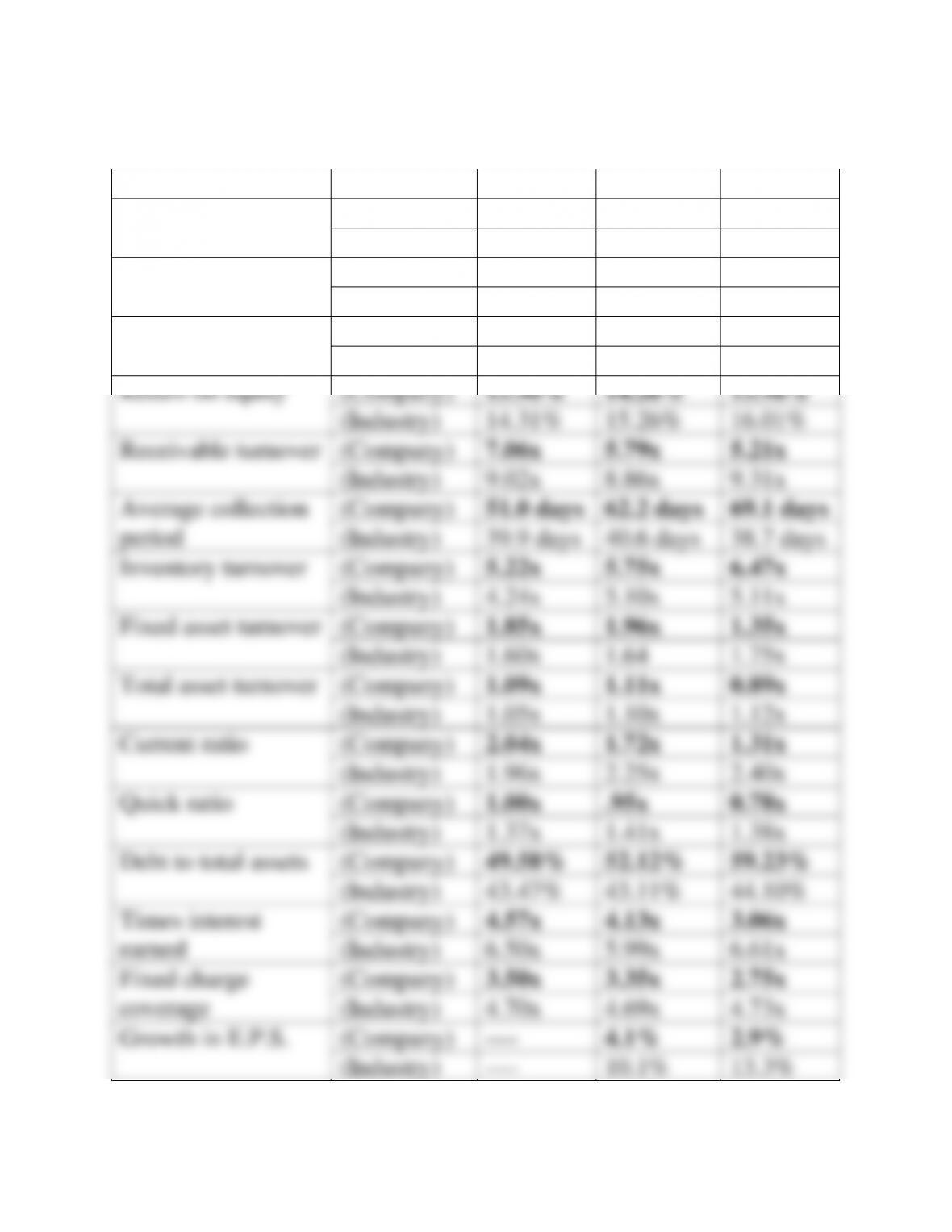

Exhibit 3

Selected Industry Ratios

201X

201Y

201Z

Growth in sales …………………………...

—

10.00%

12.00%

Profit margin ……………………………….

7.71%

7.82%

7.96%

Return on assets (investment) …………

7.94%

8.86%

8.95%

Return on equity …………………………..

14.31%

15.26%

16.01%

Receivable turnover ……………………..

9.02X

8.86X

9.31X

Average collection period………………

39.9 days

40.6 days

38.7 days

Inventory turnover………………………..

4.24X

5.10X

5.11X

Fixed asset turnover ……………………..

1.60X

1.64X

1.75X

Total asset turnover ………………………

1.05X

1.10X

1.12X

Current ratio ………………………………..

1.96X

2.25X

2.40X

Quick ratio ………………………………….

1.37X

1.41X

1.38X

Debt to total assets ……………………….

43.47%

43.11%

44.10%

Times interest earned ……………………

6.50X

5.99X

6.61X

Fixed charge coverage …………………..

4.70X

4.69X

4.73X

Growth in EPS …………………………….

—

10.10%

13.30%

The stock in the corporation has become available due to the ill health of a current stockholder,

who is in need of cash. The issue here is not to determine the exact price for the stock, but rather

whether Lamar Swimwear represents an attractive investment situation. Although Mr. Adkins

has a primary interest in the profitability ratios, he will take a close look at all the ratios. He has

no fast and firm rules about required return on investment, but rather wishes to analyze the

overall condition of the firm. The firm does not currently pay a cash dividend, and return to the

investor must come from selling the stock in the future. After doing a thorough analysis

(including ratios for each year and comparisons to the industry), what comments and

recommendations do you offer to Mr. Adkins?

Chapter 03: Financial Analysis

3-58

CP 3–1. Solution: Lamar Swimwear

201X

201Y

201Z

Growth in sales

(Company)

25%

25%

(Industry)

10%

12%

Profit margin

(Company)

7.35%

6.12%

6.38%

(Industry)

7.71%

7.82%

7.96%

Return on assets

(Company)

8.02%

6.80%

5.70%

(Industry)

7.94%

8.68%

8.95%

Return on equity

(Company)

15.90%

14.20%

13.98%

(Industry)

14.31%

15.26%

16.01%

Receivable turnover

(Company)

7.06x

5.79x

5.21x

(Industry)

9.02x

8.86x

9.31x

Average collection

period

(Company)

51.0 days

62.2 days

69.1 days

(Industry)

39.9 days

40.6 days

38.7 days

Inventory turnover

(Company)

5.22x

5.75x

6.47x

(Industry)

4.24x

5.10x

5.11x

Fixed asset turnover

(Company)

1.85x

1.96x

1.35x

(Industry)

1.60x

1.64

1.75x

Total asset turnover

(Company)

1.09x

1.11x

0.89x

(Industry)

1.05x

1.10x

1.12x

Current ratio

(Company)

2.04x

1.72x

1.31x

(Industry)

1.96x

2.25x

2.40x

Quick ratio

(Company)

1.00x

.95x

0.78x

(Industry)

1.37x

1.41x

1.38x

Debt to total assets

(Company)

49.58%

52.12%

59.23%

(Industry)

43.47%

43.11%

44.10%

Times interest

earned

(Company)

4.57x

4.13x

3.06x

(Industry)

6.50x

5.99x

6.61x

Fixed charge

coverage

(Company)

3.50x

3.35x

2.75x

(Industry)

4.70x

4.69x

4.73x

Growth in E.P.S.

(Company)

—-

4.1%

2.9%

(Industry)

—-

10.1%

13.3%

Chapter 03: Financial Analysis

3-59

CP 3-1. (Continued)

Discussion of Ratios

(25 percent per year). There obviously are no economies of scale for this

firm. Higher costs of goods sold and interest expense appear to be

causing the problem. The return–on-asset ratio starts out in 201X above

the industry average (8.02 percent versus 7.94 percent) and ends up well

of the progressively larger debt that the firm is using. High debt

utilization tends to contribute to high return on equity, but not in this

case. There is simply too much deterioration in return on assets

translating into low return on equity.

asset turnover. A decline from 1.85x to 1.35x was caused by an increase

in 113.8 percent in fixed assets (representing $740,000).

We can summarize the discussion of the turnover ratios by saying that

despite a 56.25 percent increase in sales, assets grew even more rapidly