Chapter 20 – External Growth through Mergers

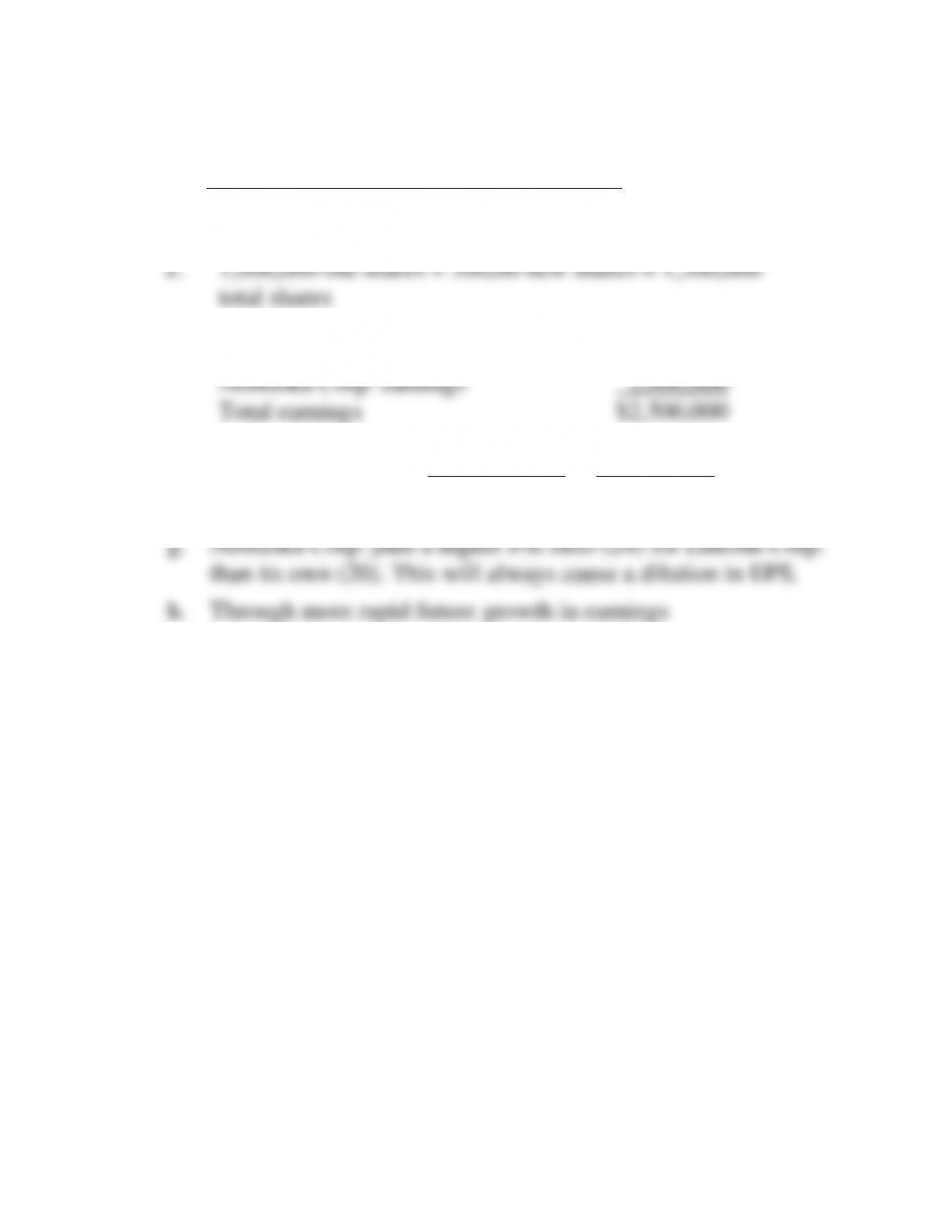

a. Total earnings Noble $ 1,200,000

+ Barnes $ 3,600,000

Combined earnings $ 4,800,000

Chapter 20 – External Growth through Mergers

20-12

Lincoln

Corp.

Nebraska

Corp.

Total earnings ……………………………………….

$500,000

$2,000,000

Number of shares of stock outstanding ………

200,000

1,000,000

Earnings per share ………………………………….

$2.50

$2.00

Price-earnings ratio (P/E) ………………………..

16

20

Market price per share …………………………….

$40

$40

a. The Nebraska Corp. is going to give Lincoln Corp. a 50 percent premium over Lincoln

Corp.’s current market value. What price will it pay?

b. At the price computed in part a, what is the total market value of Lincoln Corp.? (Use

the number of Lincoln Corp. shares times price.)

c. At the price computed in part a, what is the P/E ratio Nebraska Corp. is assigning

Lincoln Corp.?

d. How many shares must Nebraska Corp. issue to buy the Lincoln Corp. at the total value

computed in part b? (Keep in mind Nebraska Corp.’s price per share is $40.)

e. Given the answer to part d, how many shares will Nebraska Corp. have after the

merger?

f. Add together the total earnings of both corporations and divide by the total shares

computed in part e. What are the new postmerger earnings per share?

g. Why has Nebraska Corp.’s earnings per share gone down?

h. How can Nebraska Corp. hope to overcome this dilution?

20–7 Solution:

Nebraska Corp. and Lincoln Corp.

a.

$40

current price

×1.50

50% premium

$60

price paid

b.

$60

price paid

×200,000

shares

$12,000,000

total market value

c.

Price $60 24 P/E ratio

EPS $2.50

==

Chapter 20 – External Growth through Mergers

20-13

20–7. (Continued)

d.

$12,000,000 total market value of Lincoln Corp. 300,000 new shares

$40 Nebraska Corp.’s share price =

e.

1,000,000 old shares + 300,00 new shares = 1,300,000

total shares

f.

Lincoln Corp. earnings

$500,000

Nebraska Corp. earnings

2,000,000

Total earnings

$2,500,000

New postmerger

EPS =

total earnings $2,500,000

= $1.92

total shares 1,300,000

==

8. Two-step buyout (LO2) The Hollings Corporation is considering a two-step buyout of the

Norton Corporation. The latter firm has 2 million shares outstanding and its stock price is

currently $40 per share. In the two-step buyout, Hollings will offer to buy 51 percent of

Norton’s shares outstanding for $68 per share in cash and the balance in a second offer of

980,000 convertible preferred stock shares. Each share of preferred stock would be valued

at 45 percent over the current value of Norton’s common stock. Mr. Green, a newcomer to

the management team at Hollings, suggests that only one offer for all Norton’s shares be

made at $65.25 per share. Compare the total costs of the two alternatives. Which is better

in terms of minimizing costs?

20–8. Solution:

Chapter 20 – External Growth through Mergers

20-14

Hollings Corporation

Two Step Offer

1. 51% × 2,000,000 shares = $1,020,000 shares

1,020,000 shares × $68 cash = $69,360,000

2. 980,000 shares of convertible preferred stock ×

9. Future tax obligation to selling stockholder (LO1) Al Simpson helped start Excel

Systems in 2005. At the time, he purchased 100,000 shares of stock at $1 per share. In

2010 he has the opportunity to sell his interest in the company to Folsom Corp. for $50 a

share in cash. His capital gains tax rate would be 15 percent.

a. If he sells his interest, what will be the value for before-tax profit, taxes, and aftertax

profit?

b. Assume, instead of cash, he accepts Folsom Corp. stock valued at $50 per share. He

pays no tax at that time. He holds the stock for five years and then sells it for $88.50

(the stock pays no cash dividends). What will be the value for before-tax profit, taxes,

and aftertax profit in 2015? His capital gains tax is once again 15 percent.

c. Using an 9 percent discount rate, compare the aftertax profit figure in part b to that in

part a (that is, discount back the answer in part b for five years and compare it to the

answer in part a.

20–9 Solution:

Chapter 20 – External Growth through Mergers

20-15

Excel Systems

a. Sales amount 100,000 Shares. × $50 $5,000,000

Purchase amount 100,000 Shares. × $1 100,000

b. Sales amount 100,000 Shares. × $88.50 $8,850,000

Purchase amount 100,000 Shares. × $1 100,000

c. Discount back $7,437,500 for 5 years at 9 %

desirable alternative.

10. Premium offers and stock price movement (LO1) Chicago Savings Corp. is planning to

make an offer for Ernie’s Bank & Trust. The stock of Ernie’s Bank & Trust is currently

selling for $40 a share.

a. If the tender offer is planned at a premium of 60 percent over market price, what will be

the value offered per share for Ernie’s Bank & Trust?

b. Suppose before the offer is actually announced, the stock price of Ernie’s Bank & Trust

goes to $56 because of strong merger rumors. If you buy the stock at that price and the

merger goes through (at the price computed in part a), what will be your percentage gain?

c. Because there is always the possibility that the merger could be called off after it is

announced, you also want to consider your percentage loss if that happens. Assume you

buy the stock at $56 and it falls back to its original value after the merger cancellation,

what will be your percentage loss?

d. If there is a 80 percent probability that the merger will go through when you buy the

stock at $56 and only a 20 percent chance that it will be called off, does this appear to

be a good investment? Compute the expected value of the return on the investment.

Chapter 20 – External Growth through Mergers

20–10. Solution: Chicago Savings Corp.

a. Market price of Ernie’s Bank & Trust $40

+ Premium of 60% 24

Value offered per share $64

Chapter 20 – External Growth through Mergers

20-17

20–11. Solution:

Shelton Corporation

a. Premerger Postmerger

Standard deviation $1.89 $1.20

V = .63 .40

Mean or expected value $3.00 $3.00

= = =

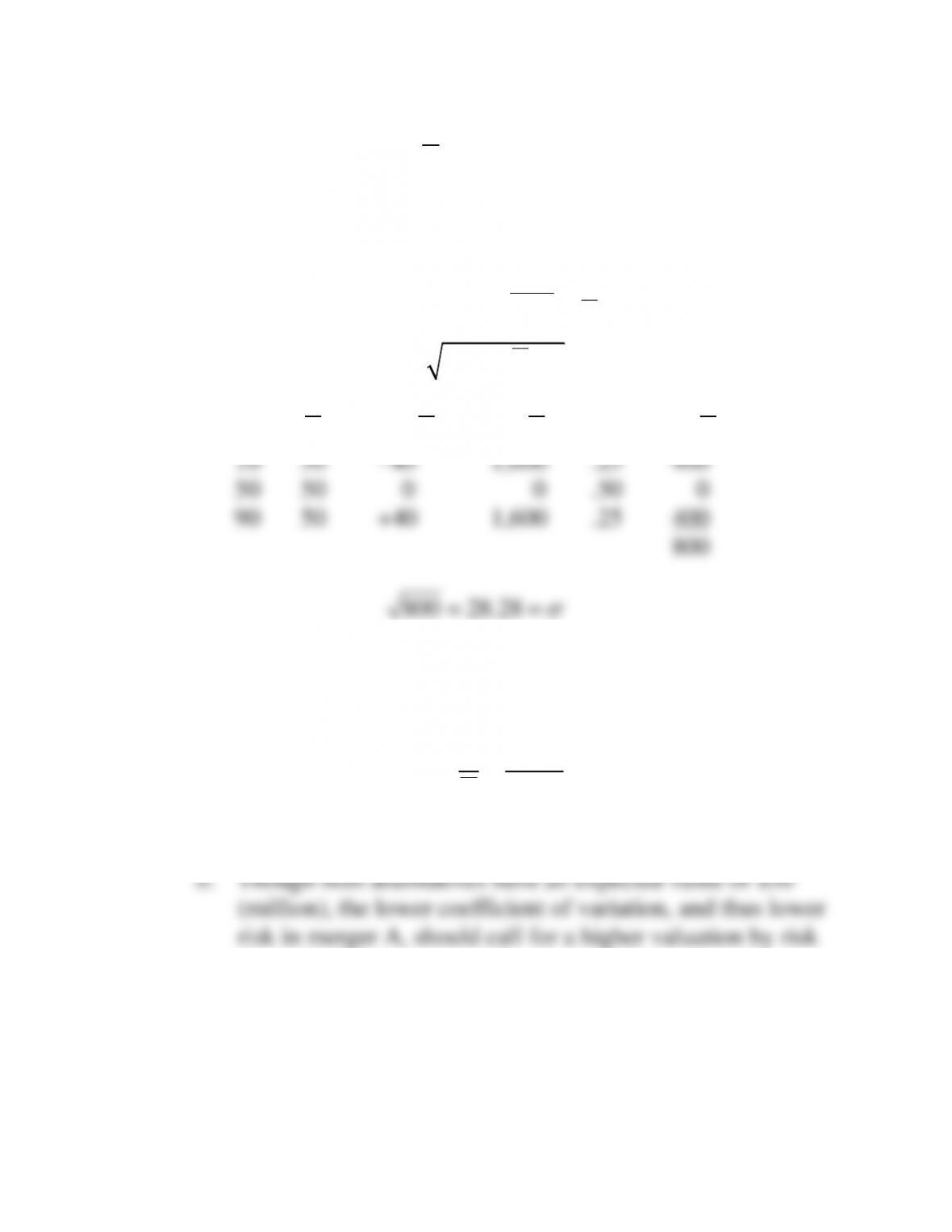

12. Portfolio consideration and risk aversion (LO4) General Meters is considering two

mergers. The first is with Firm A in its own volatile industry, the auto speedometer

industry, whereas the second is a merger with Firm B in an industry that moves in the

opposite direction (and will tend to level out performance due to negative correlation).

a Compute the mean, standard deviation, and coefficient of variation for both investments

(refer to Chapter 13 if necessary).

General Meters Merger General Meters Merger

with Firm A with Firm B

Possible Possible

Earnings Earnings

($ in millions) Probability ($ millions) Probability

$40 ………………….. .30 $10 ……………. . .25

50 …………………. .40 50 ……………. . .50

60 …………………. . .30 90 ……………. . .25

b. Assuming investors are risk-averse, which alternative can be expected to bring the

higher valuation?

20–12. Solution:

Chapter 20 – External Growth through Mergers

General Meters

a. Merger with A (answer in millions of dollars)

D DP=

D P DP

40 .30 12.0

50 .40 20.0

Chapter 20 – External Growth through Mergers

D DP=

D P DP

10 .25 2.5

50 .50 25.0

90 .25 22.5

50.0 =

D

2

(D D) P

= −

D

D

(D –

D

) (D –

D

)2 P (D –

D

)2P