Chapter 02: Review of Accounting

2-11

2-10. Solution:

Precision Systems

Sales…………………………………………………….. $800,000

11. Depreciation and earnings (LO1) Stein Books, Inc. sold 1,400 finance textbooks for $195

each to High Tuition University in 2010. These books cost $150 to produce. Stein Books

spent $12,000 (selling expense) to convince the university to buy its books.

Depreciation expense for the year was $15,000. In addition, Stein Books borrowed

$100,000 on January 1, 2010, on which the company paid 10 percent interest. Both the

interest and principal of the loan were paid on December 31, 2010. The publishing firm’s

tax rate is 30 percent.

Did Stein Books make a profit in 2010? Please verify with an income statement

presented in good form.

2-11. Solution:

Stein Books, Inc.

Income Statement

For the Year Ending December 31, 2010

Sales (1,400 books at $195 each) …………………………... $273,000

Chapter 02: Review of Accounting

2-12

12. Determination of profitability (LO1) Lemon Auto Wholesalers had sales of $700,000 in

2010 and cost of goods sold represented 70 percent of sales. Selling and administrative

expenses were 12 percent of sales. Depreciation expense was $10,000 and interest expense

for the year was $8,000. The firm’s tax rate is 30 percent.

a. Compute earnings after taxes.

b. Assume the firm hires Ms. Carr, an efficiency expert, as a consultant. She suggests

that by increasing selling and administrative expenses to 14 percent of sales, sales can

be increased to $750,000. The extra sales effort will also reduce cost of goods sold to

66 percent of sales (There will be a larger markup in prices as a result of more

aggressive selling). Depreciation expense will remain at $10,000. However, more

automobiles will have to be carried in inventory to satisfy customers, and interest

expense will go up to $15,000. The firm’s tax rate will remain at 30 percent. Compute

revised earnings after taxes based on Ms. Carr’s suggestions for Lemon Auto

Wholesalers. Will her ideas increase or decrease profitability?

2-12. Solution:

Lemon Auto Wholesalers

Income Statement

a. Sales ………………………………………………………… $700,000

Cost of goods sold (70% of sales) ………………… $490,000

Chapter 02: Review of Accounting

2-13

2-12. (Continued)

b. Sales ………………………………………………………… $750,000

Cost of goods sold (66% of sales) ……………….. $495,000

Gross profit …………………………………………… $255,000

13. Balance sheet (LO3) Classify the following balance sheet items as current or

noncurrent:

Retained earnings Bonds payable

Accounts payable Accrued wages payable

Prepaid expenses Accounts receivable

Plant and equipment Capital in excess of par

Inventory Preferred stock

Common stock Marketable securities

2-13. Solution:

Retained earnings – noncurrent

Accounts payable – current

Chapter 02: Review of Accounting

2-14

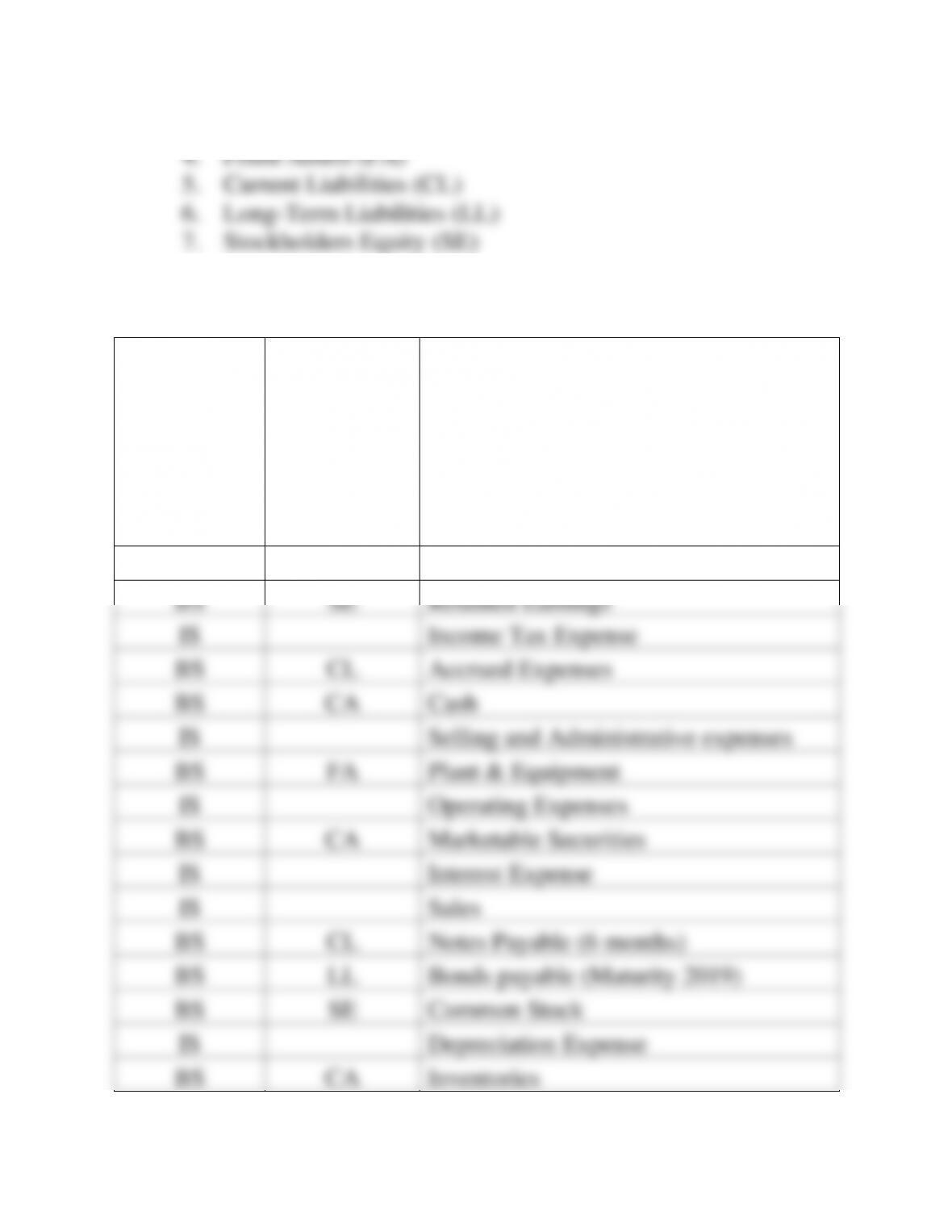

14. Balance sheet and income statement classification (LO1 & 3) Fill in the blank spaces

with categories 1 through 7:

1. Balance sheet (BS) 5. Current liabilities (CL)

2. Income statement (IS) 6. Long-term liabilities (LL)

3. Current assets (CA) 7. Stockholders’ equity (SE)

4. Fixed assets (FA)

Indicate Whether

Item Is on Balance

Sheet (BS) or

Income

Statement (IS)

If on Balance

Sheet, Designate

Which

Category

Item

_____

_____

Accounts receivable

_____

_____

Retained earnings

_____

_____

Income tax expense

_____

_____

Accrued expenses

_____

_____

Cash

_____

_____

Selling and administrative expenses

_____

_____

Plant and equipment

_____

_____

Operating expenses

_____

_____

Marketable securities

_____

_____

Interest expense

_____

_____

Sales

_____

_____

Notes payable (6 months)

_____

_____

Bonds payable, maturity 2019

_____

_____

Common stock

_____

_____

Depreciation expense

_____

_____

Inventories

_____

_____

Capital in excess of par value

_____

_____

Net income (earnings after taxes)

_____

_____

Income tax payable

2-14. Solution:

Chapter 02: Review of Accounting

2-15

2-14. (Continued)

Indicate

Whether the

item is on

Income

Statement or

Balance

Sheet

If the Item

is on

Balance

Sheet,

Designate

Which

Category

Item

BS

CA

Accounts Receivable

BS

SE

Retained Earnings

IS

Income Tax Expense

BS

CL

Accrued Expenses

BS

CA

Cash

IS

Selling and Administrative expenses

BS

FA

Plant & Equipment

IS

Operating Expenses

BS

CA

Marketable Securities

IS

Interest Expense

IS

Sales

BS

CL

Notes Payable (6 months)

BS

LL

Bonds payable (Maturity 2019)

BS

SE

Common Stock

IS

Depreciation Expense

BS

CA

Inventories

Chapter 02: Review of Accounting

2-16

BS

SE

Capital in excess of par value

IS

Net Income (Earnings after Taxes)

BS

CL

Income tax payable

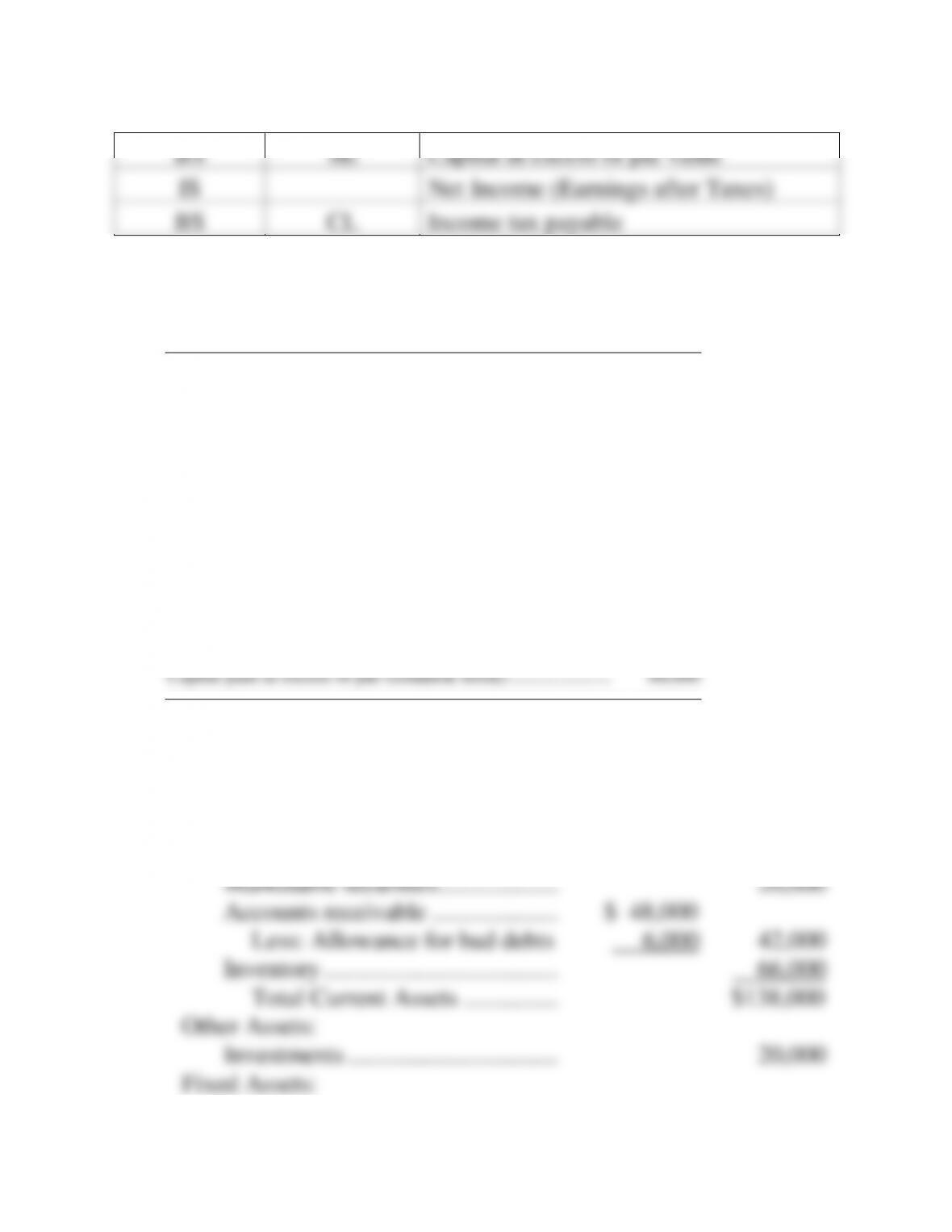

15. Development of balance sheet (LO3) Arrange the following items in proper balance sheet

presentation:

Accumulated depreciation………………………..………………….. $300,000

Retained earnings………………………….….. ……………………….. 96,000

Cash………………………………….……… ……………………………… 10,000

Bonds payable…………………………………. ………………………… 136,000

Accounts receivable……………………………. ……………………… 48,000

Plant and equipment—original cost……………….. …………….. 680,000

Accounts payable………………………………. ………………………. 35,000

Allowance for bad debts..……………..……….. …………………… 6,000

Common stock, $1 par, 100,000 shares outstanding….. ……. 100,000

Inventory…………………………………….. ……………………………. 66,000

Preferred stock, $50 par, 1,000 shares outstanding… ……….. 50,000

Marketable securities………………………….. ……………………… 20,000

Investments…………………………………… ………………………….. 20,000

Notes payable…………………………………. …………………………. 33,000

2-15. Solution:

Assets

Current Assets:

Cash ……………………………………. $ 10,000

Chapter 02: Review of Accounting

2-15. (Continued)

Liabilities and Stockholders’ Equity

Current Liabilities:

Accounts payable ……………………………………………..

Notes payable ………………………………………………….

Total current liabilities ……………………………………

Long-term Liabilities ………………………………………….

Bonds payable …………………………………………………

Total Liabilities …………………………..………………..

Stockholders’ Equity:

Preferred stock, $50 par, 1,000 shares outstanding ..

Common stock, $1 par, 100,000 shares outstanding

Capital paid in excess of par (common stock)……….

Retained earnings …………………………………………….

Total Stockholders’ Equity ……………………………..

Total Liabilities and Stockholders’ Equity ……..

$ 35,000

33,000

$ 68,000

136,000

$204,000

50,000

100,000

88,000

96,000

$334,000

$538,000

16. Earnings per share and retained earnings (LO1 & 3) Okra Snack Delights, Inc., has an

operating profit of $210,000. Interest expense for the year was $30,000; preferred

dividends paid were $24,700; and common dividends paid were $36,000. The tax was

Chapter 02: Review of Accounting

2-18

Okra Snack Delights, Inc.

a. Operating profit (EBIT) ………………………………….. $210,000

Interest expense ………………………………………… 30,000

Earnings Available to

Common Stockholders

Earnings per Share = Number of Shares of

Com. Stock Outstanding

$96,000/16,000 shares

$6.00 per share

=

=

Dividends per Share = $36,000/16,000 shares

= $2.25 per share

b. Increase in retained earnings = $60,000

Chapter 02: Review of Accounting

17. Earnings per share and retained earnings (LO1 & 3) Quantum Technology had

$640,000 of retained earnings on December 31, 2010. The company paid common

dividends of $30,000 in 2010 and had retained earnings of $500,000 on December 31,

2009. How much did Quantum Technology earn during 2010, and what would earnings per

share be if 40,000 shares of common stock were outstanding?

2-17. Solution:

Quantum Technology

Retained earnings, December 31, 2010 …………………… $640,000

Chapter 02: Review of Accounting

2-20

$40.00

19. Price/earning ratio (LO2) Assume for Botox Facial Care discussed in Problem 18 that in

2011, earnings after taxes declined to $140,000 with the same 200,000 shares outstanding.

The stock price declined to $24.50.

a. Compute earnings per share and the P/E ratio for 2011.

b. Give a general explanation of why the P/E changed. You might want to consult the

textbook to explain this surprising result.

2-19. Solution:

Botox Facial Care (continued)

a. EPS (2011)

$140,000 $.70

200,000

==

P/E ratio (2011) = Price/EPS =

$24.50 35

$.70 x=

20. Cash flow (LO4) Identify whether each of the following items increases or decreases

cash flow:

Increase in accounts receivable Decrease in prepaid expenses

Increase in notes payable Increase in inventory

Depreciation expense Dividend payment

Increase in investments Increase in accrued expenses

Decrease in accounts payable

2-20. Solution: