Chapter 18: Dividend Policy and Retained Earnings

Chapter 18

Dividend Policy and Retained Earnings

Discussion Questions

18-1.

How does the marginal principle of retained earnings relate to the returns that a

stockholder may make in other investments?

The marginal principle of retained earnings suggests that the corporation must do

an analysis of whether the corporation or the stockholders can earn the most on

funds associated with retained earnings. Thus, we must consider what the

stockholders can earn on other investments.

18-2.

Discuss the difference between a passive and an active dividend policy.

A passive dividend policy suggests that dividends should be paid out if the

corporation cannot make better use of the funds. We are looking more at

alternate investment opportunities than at preferences for dividends.

If dividends are considered as an active decision variable, stockholder preference

for cash dividends is considered very early in the decision process.

18-3.

How does the stockholder, in general, feel about the relevance of dividends?

The stockholder would appear to consider dividends as relevant. Dividends do

resolve uncertainty in the minds of investors and provide information content. Some

stockholders may say that the dividends are relevant, but in a different sense. Perhaps

they prefer to receive little or no dividends because of the immediate income tax.

18-4.

Explain the relationship between a company’s growth possibilities and its

dividend policy.

The greater a company’s growth possibilities, the more funds that can be justified for

profitable internal reinvestment. This is very well illustrated in Table 18-1 in which

we show four-year growth rates for selected U.S. corporations and their associated

dividend payout percentages. This is also discussed in the life cycle of the firm.

Chapter 18: Dividend Policy and Retained Earnings

18-5.

Since initial contributed capital theoretically belongs to the stockholders, why are

there legal restrictions on paying out the funds to the stockholders?

Creditors have extended credit on the assumption that a given capital base would

remain intact throughout the life of a loan. While they may not object to the

payment of dividends from past and current earnings, they must have the

protection of keeping contributed capital in place.

18-6.

Discuss how desire for control may influence a firm’s willingness to pay

dividends.

Management’s desire for control could imply that a closely held firm should

avoid dividends to minimize the need for outside financing. For a larger firm,

management may have to pay dividends in order to maintain their current

position through keeping stockholders happy.

18-7.

If you buy stock on the ex-dividend date, will you receive the upcoming quarterly

dividend?

No, the old stockholder receives the upcoming quarterly dividend. Of course,

if you continue to hold the stock, you will receive the next dividend.

18-8.

How is a stock split (versus a stock dividend) treated on the financial

statements of a corporation?

For a stock split, there is no transfer of funds, but merely a –reduction in

par value and a –proportionate increase in the number of shares outstanding.

Impact of a Stock Split

Before After

Common stock (1,000,000 shares at $10 par) (2,000,000 shares at $5 par)

Chapter 18: Dividend Policy and Retained Earnings

18-9.

Why might a stock dividend or a stock split be of limited value to an investor?

The asset base remains the same and the stockholders’ proportionate interest is

unchanged (everyone got the same new share). Earnings per share will go down

by the exact proportion that the number of shares increases. If the P/E ratio

remains constant, the total value of each shareholder’s portfolio will not

increase.

The only circumstances in which a stock dividend may be of some usefulness

and perhaps increase value is when dividends per share remain constant and total

dividends go up, or where substantial information is provided about the growth

of the company. A stock split may have some functionality in placing the

company into a lower “stock price” trading range.

18-10.

Does it make sense for a corporation to repurchase its own stock? Explain.

A corporation can make a rational case for purchasing its own stock as an

alternate to a cash dividend policy. Earnings per share will go up as the shares

decline and if the price-earnings ratio remains the same, the stockholder will

receive the same dollar benefit as if a cash dividend was paid. Because the

benefits are in the format of capital gains the tax may be deferred until the stock

is sold.

A corporation also may justify the repurchase of its own stock because it is at a

very low price, or to maintain constant demand for the shares. Reacquired shares

may be used for employee options or as a part of a tender offer in a merger or

acquisition. Firms may also reacquire part of their stock as protection against a

hostile takeover.

18-11.

What advantages to the corporation and the stockholder do dividend

reinvestment plans offer?

Dividend reinvestment plans allow corporations to raise funds continually from

Chapter 18: Dividend Policy and Retained Earnings

18-4

Chapter 18

Problems

1. Payout ratio (LO1) Neil Diamond Brokers, Inc., reported earnings per share of $4.00 and

paid $.90 in dividends. What is the payout ratio?

18–1. Solution:

Neil Diamond Brokers, Inc.

Payout ratio = dividends per share/earnings per share

2. Payout ratio (LO1) Sewell Enterprises earned $160 million last year and retained $100

million. What is the payout ratio?

18–2. Solution:

Sewell Enterprises

Dividends = (earnings – retained funds)

Payout ratio = dividends/earnings

3. Payout ratio (LO1) Biogen, Inc., earned $850 million last year and had a 30 percent

payout ratio. How much did the firm add to its retained earnings?

18–3. Solution:

Biogen, Inc.

Addition to retained earnings = Earnings – Dividends

Chapter 18: Dividend Policy and Retained Earnings

18-5

4. Dividends, retained earnings, and yield (LO1) Polycom Systems earned $480 million

last year and paid out 20 percent of earnings in dividends.

a. By how much did the company’s retained earnings increase?

b. With 100 million shares outstanding and stock price of $80, what was the dividend

yield? (Hint: First compute dividends per share.)

18–4. Solution:

Polycom Systems

a. Addition to retained earnings = Earnings – Dividends

5. Growth and dividend policy (LO2) The following companies have different financial

statistics. What dividend policies would you recommend for them? Explain your reasons.

Turtle Co. Hare Corp.

Growth rate in sales and earnings ……….. 5% 20%

Cash as a percentage of total assets …….. 15 2

18–5. Solution:

assets. For this reason, Hare should have a low dividend payout.

Chapter 18: Dividend Policy and Retained Earnings

18-6

6. Limits on dividends (LO3) Carnegie Mellon and Produce Co. has $120,000,000 in

stockholders’ equity. Forty million dollars is listed as common stock and the balance is in

retained earnings. The firm has $250,000,000 in total assets and 3 percent of this value is in

cash. Earnings for the year are $20,000,000 and are included in retained earnings.

a. What is the legal limit on current dividends?

b. What is the practical limit based on liquidity?

c. If the company pays out the amount in part b, what is the dividend payout ratio?

(Compute this based on total dollars rather than on a per share basis because the

number of shares is not given.)

Payout ratio = Dividends/Earnings

18–6. Solution:

Carnegie Mellon and Produce Company

a. The legal limit is equal to retained earnings

Retained earnings = stockholder’s equity–common stock

b. The practical limit based on liquidity is equal to the cash

balance

Cash = Cash percentage × total assets

c. Payout ratio = Dividends / Earnings

7. Life cycle growth and dividends (LO2) A financial analyst is attempting to assess the future

dividend policy of Environmental Systems by examining its life cycle. She anticipates no

payout of earnings in the form of cash dividends during the development stage (I). During the

growth stage (II), she anticipates 10 percent of earnings will be distributed as dividends. As

the firm progresses to the expansion stage (III), the payout ratio will go up to 30 percent, and

eventually reach 50 percent during the maturity stage (IV).

a. Assuming earnings per share will be as follows during each of the four stages, indicate

the cash dividend per share (if any) during each stage.

Chapter 18: Dividend Policy and Retained Earnings

18-7

Stage I………………… $ .15

Stage II ………………. 1.80

Stage III ……………… 2.60

Stage IV ……………… 3.10

b. Assume in Stage IV that an investor owns 275 shares and is in a 31 percent tax bracket;

what will be the investor’s aftertax income from the cash dividend?

c. In what two stages is the firm most likely to utilize stock dividends or stock splits?

18–7. Solution:

Environmental Systems

a.

Earnings

Payout Ratio

Dividends

Stage I

$ .15

0

0

Stage II

1.80

10%

$ .18

Stage III

2.60

30%

$. 78

Stage IV

3.10

50%

$1.55

b. Total Dividends = Shares × dividends per share

Aftertax income = total dividends × (1 – T)

8. Stock split and stock dividend (LO4) Austin Power Company has the following balance

sheet:

Chapter 18: Dividend Policy and Retained Earnings

18-8

Assets

Cash ……………………………………………………. $ 50,000

Accounts receivable ………………………………. 250,000

Fixed assets ………………………………………….. 700,000

Total assets …………………………………… $1,000,000

Liabilities

Accounts payable …………………… $ 250,000

Notes payable ……………………….. 50,000

Common stock

100,000 shares @ $2 par ……… 200,000

Capital in excess of par …………… 100,000

Retained earnings ………………….. 400,000

$1,000,000

The firm’s has a market price of $11 a share.

a. Show the effect on the capital account(s) of a two-for-one stock split.

b. Show the effect on the capital accounts of a 10 percent stock dividend. Part b is

separate from part a. In part b do not assume the stock split has taken place.

c. Based on the balance in retained earnings, which of the two dividend plans is more

restrictive on future cash dividends?

18–8. Solution:

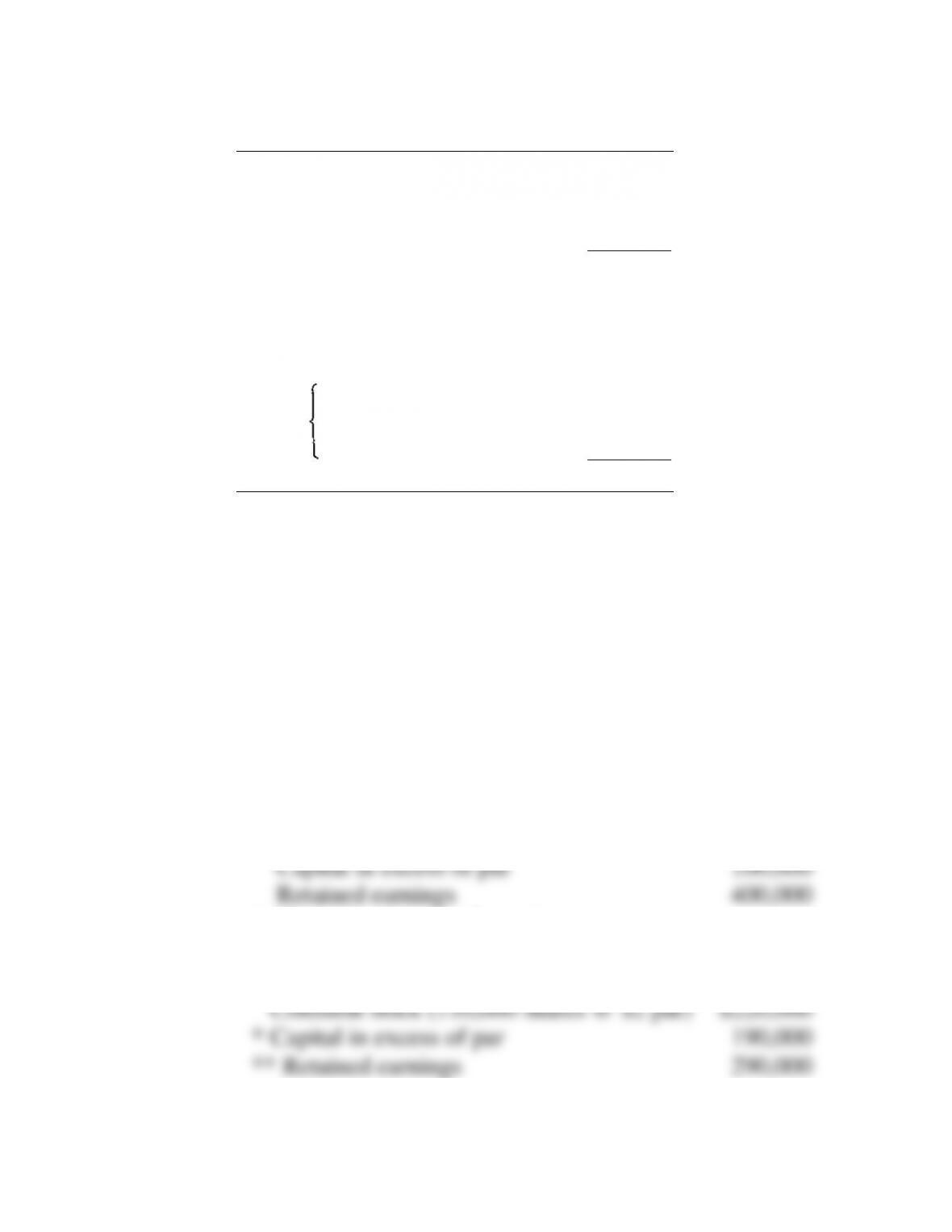

Austin Power Company

a. 2 for 1 stock split

* Common stock (200,000 shares @ $1 par) $200,000

* The only account affected

b. 10% stock dividend

Capital

accounts

Chapter 18: Dividend Policy and Retained Earnings

18-9

18–8. (Continued)

9. Policy on payout ratio (LO1) In doing a five-year analysis of future dividends, the

Dawson Corporation is considering the following two plans. The values represent

dividends per share.

Year Plan A Plan B

1 …………….. $1.50 $ .50

2 …………….. 1.50 2.00

3 …………….. 1.50 .20

4 …………….. 1.60 4.00

5 …………….. 1.60 1.70

a. How much in total dividends per share will be paid under each plan over the five years?

b. Mr. Bright, the vice-president of finance, suggests that stockholders often prefer a

stable dividend policy to a highly variable one. He will assume that stockholders apply

a lower discount rate to dividends that are stable. The discount rate to be used for Plan

A is 10 percent; the discount rate for Plan B is 12 percent. Which plan will provide the

higher present value for the future dividends? (Round to two places to the right of the

decimal point.)

18–9. Solution:

Dawson Corporation

Chapter 18: Dividend Policy and Retained Earnings

18-10

b. Plan A

Dividend

Per Share

×

PVIF (10%)

PV

1

$1.50

.909

$1.36

2

1.50

.826

1.24

3

1.50

.751

1.13

4

1.60

.683

1.09

5

1.60

.621

.99

Present Value of future dividends

$5.81

18–9. (Continued)

Plan B

Dividend

Per Share

×

PVIF (12%)

PV

1

$ .50

.893

$ .45

2

2.00

.797

1.59

3

.20

.712

.14

4

4.00

.636

2.54

5

1.70

.567

.96

Present Value of future dividends

$5.68

Plan A will provide the higher present value of future