Chapter 16: Long-Term Debt and Lease Financing

Present value of principal payment at maturity

PV = FV × PVIF (n = 20*, i = 6%)

Total present value

Present value of interest payments $401.45

b. Purchase price $1,000.00

Chapter 16: Long-Term Debt and Lease Financing

16-22

17. Advanced Refunding decision (LO3) The Bowman Corporation has a $20 million bond

obligation outstanding, which it is considering refunding. Though the bonds were initially

issued at 12 percent, the interest rates on similar issues have declined to 10.5 percent. The

bonds were originally issued for 20 years and have 15 years remaining. The new issue

would be for 15 years. There is an 8 percent call premium on the old issue. The

underwriting cost on the new $20,000,000 issue is $570,000, and the underwriting cost on

the old issue was $400,000. The company is in a 35 percent tax bracket, and it will use a

7 percent discount rate (rounded after-tax cost of debt) to analyze the refunding decision.

Should the old issue be refunded with new debt?

16–17. Solution:

Bowman Corporation

Outflows

1. Payment of call premium

2. Underwriting cost on new issue

Amortization of costs ($570,000/15) (.35)

Actual expenditure $570,000

Inflows

3. Cost savings in lower interest rates

Chapter 16: Long-Term Debt and Lease Financing

16-23

16–17. (Continued)

$ 195,000

× 9.108 PVIFA (n = 15, i = 7%) Appendix D

$1,776,060

4. Underwriting cost on old issue

Original amount $400,000

Amount written off over 5 years

at $20,000 per year 100,000

Summary

Outflows

Inflows

1.

$1,040,000

3.

$1,776,060

2.

448,864

4.

41,244

$1,488,864

$1,817,304

PV of inflows

$1,817,304

PV of outflows

1,448,864

Net present value

$ 328,440

Refund the old issue (particularly if it is perceived that

interest rates will not go down even more).

Chapter 16: Long-Term Debt and Lease Financing

16-24

18. Refunding decision (LO3) The Robinson Corporation has $50 million of bonds

outstanding that were issued at a coupon rate of 11¾ percent seven years ago. Interest rates

have fallen to 10¾ percent. Mr. Brooks, the vice-president of finance, does not expect rates

to fall any further. The bonds have 18 years left to maturity, and Mr. Brooks would like to

refund the bonds with a new issue of equal amount also having 18 years to maturity. The

Robinson Corporation has a tax rate of 35 percent. The underwriting cost on the old issue

was 2.5 percent of the total bond value. The underwriting cost on the new issue will be 1.8

percent of the total bond value. The original bond indenture contained a five-year

protection against a call, with a 9.5 percent call premium starting in the sixth year and

scheduled to decline by one-half percent each year thereafter. (Consider the bond to be

seven years old for purposes of computing the premium). Assume the discount rate is equal

to the aftertax cost of new debt rounded up to the nearest whole number. Should the

Robinson Corporation refund the old issue?

16–18. Solution:

Robinson Corporation

First compute the discount rate

Outflows

1. Payment on call provision (7th year = 9% call premium)

2. Underwriting cost on new issue

Actual expenditure $900,000

Chapter 16: Long-Term Debt and Lease Financing

16-25

16–18. (Continued)

Inflows

3. Cost savings in lower interest rates

Savings per year $500,000 × (1 – .35) = $325,000 Aftertax

4. Underwriting cost on old issue

Original amount (2.5% × $50,000,000) $1,250,000

Amount written off over last 7 years at

Present value of deferred future write off:

$50,000 × 10.059 502,950

16–18. (Continued)

Chapter 16: Long-Term Debt and Lease Financing

16-26

Summary

Outflows

Inflows

1.

$2,925,000

3.

$3,269,175

2.

723,967

4.

138,968

$3,648,967

$3,408,143

PV of inflows

$3,408,143

PV of outflows

3,648,967

Net present value

$ (240,824)

Based on the negative net present value, the Robinson

Corporation should not refund the issue. As time passes the

call premium will decline and if interest rates stay down or

decline further, the refunding decision could have a positive

net present value in the future.

19. Call premium (LO3) In problem 18, what would be the aftertax cost of the call premium

at the end of year 13 (in dollar value)?

16–19. Solution:

The Robinson Corporation (Continued)

Call premium (aftertax cost)

Year 1-5 not callable

Year 6……. 9.5% Year 10 ……. 7.5%

Chapter 16: Long-Term Debt and Lease Financing

16-27

OR

7 years of ½% deductions (7th through 13th year) = 3 ½%

9 ½% Call premiums

–3 1/2%

20. Capital lease or operating lease (LO4) The Deluxe Corporation has just signed a

120-month lease on an asset with a 15-year life. The minimum lease payments are $2,000

per month ($24,000 per year) and are to be discounted back to the present at a 7 percent

annual discount rate. The estimated fair value of the property is $175,000.

Should the lease be recorded as a capital lease or an operating lease?

Use criteria 3 and 4 on page 511 for a capital lease.

16–20. Solution:

The Deluxe Corporation

The lease is less than 75% of the estimated life of the leased

property.

However, the present value of the lease payments is greater than

90% of the fair value of the property.

Chapter 16: Long-Term Debt and Lease Financing

16-28

capital lease.

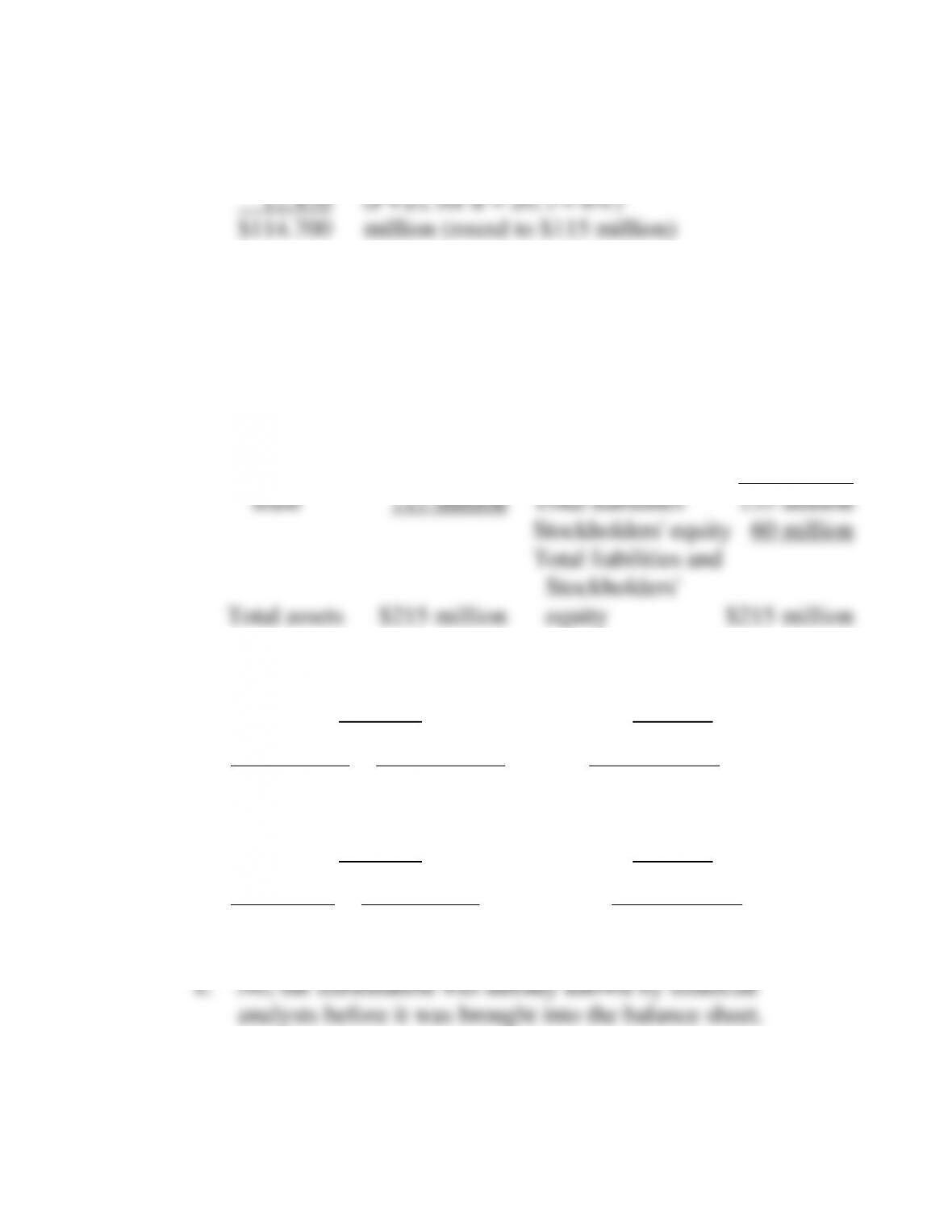

21. Balance sheet effect of leases (LO4) The Ellis Corporation has heavy lease commitments.

Prior to SFAS No. 13, it merely footnoted lease obligations in the balance sheet, which

appeared as follows:

In $ millions In $ millions

Current asserts ………………..…………

$ 50

Current liabilities …………………………

$ 10

Fixed asserts …………………..………

50

Long-term liabilities ……………….……

30

Total liabilities …………………………

$ 40

Stockholders’ equity ……………….……

60

Total assets …………………….…….

$100

Total liabilities and

stockholders’ equity …………………

$100

The footnotes stated that the company had $10 million in annual capital lease obligations

for the next 20 years.

a. Discount these annual lease obligations back to the present at a 6 percent discount rate

(round to the nearest million dollars).

b. Construct a revised balance sheet that includes lease obligations, as in Table 16–8

page 511.

c. Compute total debt to total assets on the original and revised balance sheets.

d. Compute total debt to equity on the original and revised balance sheets.

e. In an efficient capital market environment, should the consequences of SFAS No. 13,

as viewed in the answers to parts c and d, change stock prices and credit ratings?

f. Comment on management’s perception of market efficiency (the viewpoint of the

financial officer).

16–21. Solution:

The Ellis Corporation

Chapter 16: Long-Term Debt and Lease Financing

a. $10 million annual lease payments

16–21. (Continued)

b.

Current assets $50 million

Current liabilities $ 10 million

Fixed assets 50 million

Long-term liabilities 30 million

Leased property

under capital

lease 115 million

Total assets $215 million

Obligations under

capital lease 115 million

Total liabilities 155 million

Stockholders‘ equity 60 million

Total liabilities and

Stockholders’

equity $215 million

c.

Original Revised

Total debt $40 million $155 million

40% 72.1%

Total assets $100 million $215 million

= = =

d.

Original Revised

Total debt $40 million $155 million

66.7% 258.3%

Equity $60 million $60 million

= = =

Chapter 16: Long-Term Debt and Lease Financing

16-30

f. Management is concerned about whether the market is as

questionable.

22. Determining size of lease payment (LO4) The Hardaway Corporation plans to lease a

$900,000 asset to the O’Neil Corporation. The lease will be for 10 years.

a. If the Hardaway Corporation desires a 12 percent return on its investment, how much

should the lease payments be?

b. If the Hardaway Corporation is able to take a 10 percent deduction from the purchase

price of $900,000 and will pass the benefits along to the O’Neil Corporation in the

form of lower lease payments, (related to the Hardaway Corporation in the form of

lower initial net cost), how much should the revised lease payments be? Continue to

assume the Hardaway Corporation desires a 12 percent return on the 10-year lease.

16–22. Solution:

Hardaway Corporation

a. Determine 10–year annuity that will yield 12%.

A IFA

A = PV / PV (i = 12%, n = 10) Appendix D

$900,000

= $159,292

5.650 =