Chapter 16: Long-Term Debt and Lease Financing

16-1

Chapter 16

Long-Term Debt and Lease Financing

Discussion Questions

16-1.

Corporate debt has been expanding very dramatically in the last three decades.

What has been the impact on interest coverage, particularly since 1977?

In 1977, the average U.S. manufacturing corporation had its interest covered

almost eight times. By the 2000’s, the ratio had been cut to less than half.

16-2.

What are some specific features of bond agreements?

The bond agreement specifies such basic items as the par value, the coupon

rate, and the maturity date.

16-3.

What is the difference between a bond agreement and a bond indenture?

The bond agreement covers a limited number of items, whereas the bond

indenture is a supplement that often contains over 100 pages of complicated

legal wording and specifies every minute detail concerning the bond issue. The

bond indenture covers such topics as pledged collateral, methods of repayment,

restrictions on the corporation, and procedures for initiating claims against the

corporation.

16-4.

Discuss the relationship between the coupon rate (original interest rate at time

of issue) on a bond and its security provisions.

The greater the security provisions afforded to a given class of bondholders, the

lower the coupon rate.

Chapter 16: Long-Term Debt and Lease Financing

16-5.

Take the following list of securities and arrange them in order of their priority

of claims:

Preferred stock Senior debenture

Subordinated debenture Senior secured debt

Common stock Junior secured debt

The priority of claims can be determined from Figure 16-2:

senior secured debt,

junior secured debt,

senior debenture,

subordinated debenture,

preferred stock,

common stock.

16-6.

What method of “bond repayment” reduces debt and increases the amount of

common stock outstanding?

Conversion of bonds to common stock through either a convertible bond or an

exchange offer.

16-7.

What is the purpose of serial repayments and sinking funds?

The purpose of serial and sinking fund payments is to provide an orderly

procedure for the retirement of a debt obligation. To the extend bonds are paid

off over their life, there is less risk to the security holder.

16-8.

Under what circumstances would a call on a bond be exercised by a

corporation? What is the purpose of a deferred call?

A call provision may be exercised when interest rates on new securities are

considerably lower than those on previously issued debt. The purpose of a

deferred call is to insure that the bondholder will not have to surrender the

security due to a call for at least the first five or ten years.

Chapter 16: Long-Term Debt and Lease Financing

16-9.

Discuss the relationship between bond prices and interest rates. What

impact do changing interest rates have on the price of long-term bonds

versus short-term bonds?

Bond prices on outstanding issues and market interest rates move in

opposite directions. If interest rates go up, bond prices will go down and

vice versa. Long-term bonds are particularly sensitive to interest rate

changes because the bondholder is locked into the interest rate for an

extended period of time.

16-10.

What is the difference between the following yields: coupon rate, current yield,

yield to maturity?

The different bond yield terms may be defined as follows:

Coupon rate – stated interest rate divided by par value.

Current yield – stated interest rate divided by the current price of the bond.

Yield to maturity – the interest rate that will equate future interest payments

and payment at maturity to a current market price.

16-11.

How does the bond rating affect the interest rate paid by a corporation on

its bonds?

The higher the rating on a bond, the lower the interest payment that will be

required to satisfy the bondholder.

16-12.

Bonds of different risk classes will have a spread between their interest

rates. Is this spread always the same? Why?

The spread in the yield between bonds in different risk classes is not

always the same. The yield spread changes with the economy. If investors

are pessimistic about the economy, they will accept as much as 3% less

return to go into very high-quality securities-whereas, in more normal

times the spread may only be 1 ½%.

16-13.

Explain how the bond refunding problem is similar to a capital budgeting

decision.

The bond refunding problem is similar to a capital budgeting problem in

that an initial investment must be made in the form of redemption and

reissuing costs, and cash inflows will take place in the form of interest

savings. We take the present value of the inflows to determine if they

equal or exceed the outflow.

Chapter 16: Long-Term Debt and Lease Financing

16-14.

What cost of capital is generally used in evaluating a bond refunding

decision? Why?

We use the aftertax cost of new debt as the discount rate rather than the

more generalized cost of capital. Because the net cash benefits are known

with certainty, the refunding decision represents a riskless investment. For

this reason, we use a lower discount rate.

16-15.

Explain how the zero-coupon rate bond provides return to the investor.

What are the advantages to the corporation?

The zero-coupon-rate bond is initially sold at a deep discount from par

value. The return to the investor is the difference between the investor’s

cost and the face value received at the end of the life of the bond. The

advantages to the corporation are that there is immediate cash inflow to the

corporation, without any outflow until the bond matures. Furthermore, the

difference between the initial bond price and the maturity value may be

amortized for tax purposes over the life of the bond by the corporation.

16-16.

Explain how floating rate bonds can save the investor from potential

embarrassments in portfolio valuations.

Interest payments change with changing interest rates rather than with the

market value of the bond. This means that the market value of a floating

rate bond is almost fixed. The one exception is when interest rates dictated

by the floating rate formula approach (or exceed) broadly defined limits.

16-17.

Discuss the advantages and disadvantages of debt.

The primary advantages of debt are:

a. Interest payments are tax deductible.

b. The financial obligation is clearly specified and of a fixed nature.

c. In an inflationary economy, debt may be paid back with cheaper

dollars (the dollars have less purchasing power than when received).

d. The use of debt, up to a prudent point, may lower the cost of capital to

the firm.

Chapter 16: Long-Term Debt and Lease Financing

16-18.

What is a Eurobond?

A Eurobond is a bond payable in the borrower’s currency but sold outside

the borrower’s country. It is usually sold by an international syndicate.

16-19.

What do we mean by capitalizing lease payments?

Capitalizing lease payments means computing the present value of future

lease payments and showing them as an asset and liability on the balance

sheet.

16-20.

Explain the close parallel between a capital lease and the borrow-purchase

decision from the viewpoint of both the balance sheet and the income

statement.

In both cases we create an asset and liability on the balance sheet.

Furthermore in both cases, for income statement purposes, we amortize the

asset and write off interest (implied or actual) on the debt.

Appendix

16A-1.

What is the difference between technical insolvency and bankruptcy?

Technical insolvency refers to the circumstances where a firm is unable to pay its bills

as they come due. A firm may be technically insolvent even though it has a positive net

worth. Bankruptcy, on the other hand, indicates that the market value of a firm’s assets

is less than its liabilities and the firm has a negative net worth. Under the law, either

technical insolvency or bankruptcy may be adjudged as a financial failure of the

business firm.

Chapter 16: Long-Term Debt and Lease Financing

16A-2.

What are the four types of out-of-court settlements? Briefly describe each.

Extension – Creditors agree to allow the firm more time to meet its

financial obligations.

Composition – Creditors agree to accept a fractional settlement on their

original claims.

Creditor committee – A creditor committee is set up to run the business because it is

believed that management can no longer conduct the affairs of

the firm.

Assignment – Liquidation of assets takes place without going through formal

court action.

16A-3.

What is the difference between an internal reorganization and an external

reorganization under formal bankruptcy procedures?

An internal reorganization calls for an evaluation and restricting of the current affairs

of the firm. Current management may be replaced and a redesign of the capital

structure may be necessary. An external reorganization means that an actual merger

partner will be found for the firm.

16A-4.

What are the first three priority items under liquidation in bankruptcy?

(1) Cost of administering the bankruptcy procedures.

(2) Wages due workers if earned within three months of filing the bankruptcy

petition. The maximum amount is $600 per worker.

(3) Tax due at the federal, state or local level.

Chapter 16: Long-Term Debt and Lease Financing

Chapter 16

Problems

(Assume the par value of the bonds in the following problems is $1,000 unless otherwise

specified.)

1. Bond yields (LO2) Garland Corporation has a bond outstanding with a $90 annual interest

payment, a market price of $820, and a maturity date in five years. Find the following:

a. The coupon rate.

b. The current rate.

c. The approximate yield to maturity.

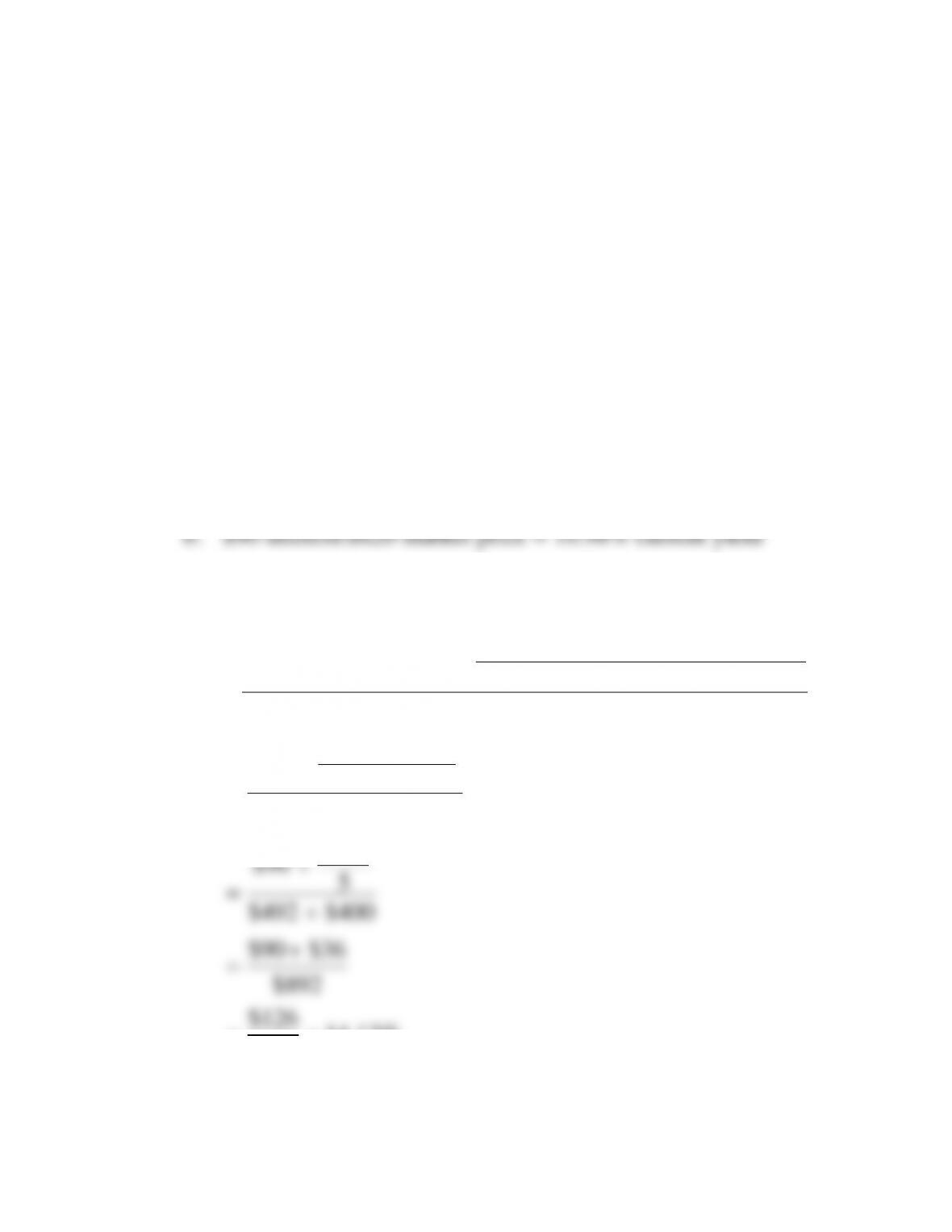

16–1. Solution:

Garland Corporation

a. $90 interest/$1,000 par = 9% coupon rate

c. Approximate yield to maturity = (Y’)

payment) (Principal .4bond) theof (Price .6

maturity toyears ofNumber

bond theof Pricepayment Principal

paymentinterest Annual

)Y’(+

−

+

=

$1,000 $820

$90 5

.6($820) .4($1,000)

$180

$90 5

$492 $400

$90 $36

$892

$126 14.13%

−

+

=

+

+

=

+

+

=

Chapter 16: Long-Term Debt and Lease Financing

2. Bond yields (LO2) Preston Corporation has a bond outstanding with a $110 annual interest

payment, a market price of $1,200, and a maturity date in 10 years.

Find the following:

a. The coupon rate.

b. The current rate.

c. The approximate yield to maturity.

16–2. Solution:

Preston Corporation

a. $110 interest/$1,000 par = 11% coupon rate

b. $110 interest/$1,200 market price = 9.17% current yield

c. Approximate yield to maturity = (Y’)

payment) (Principal .4bond) theof (Price .6

maturity toyears ofNumber

bond theof Pricepayment Principal

paymentinterest Annual

)Y’(+

−

+

=

$1,000 $1,200

$110 10

.6($1,200) .4($1,000)

$200

$110 10

$720 $400

$110 $20

−

+

=

+

−

+

=

+

−

=

Chapter 16: Long-Term Debt and Lease Financing

16-9

3. Bond yields (LO2) An investor must choose between two bonds:

Bond A pays $80 annual interest and has a market value of $800. It has 10 years to

maturity.

Bond B pays $85 annual interest and has a market value of $900. It has two years to

maturity.

a. Compute the current yield on both bonds.

b. Which bond should he select based on your answer to part a?

c. A drawback of current yield is that it does not consider the total life of the bond. For

example, the approximate yield to maturity on Bond A is 11.36 percent. What is the

approximate yield to maturity on Bond B?

d. Has your answer changed between parts b and c of this question in terms of which

bond to select?

16–3. Solution:

a. Bond A

$80 interest/$800 market price = 10% current yield

Bond B

$85 interest/$900 market price = 9.44% current yield

payment) (Principal .4bond) theof (Price .6

maturity toyears ofNumber

bond theof Pricepayment Principal

paymentinterest Annual

)Y’(+

−

+

=

Chapter 16: Long-Term Debt and Lease Financing

16–3. (Continued)

$1,000 $900

$85 2

.6($900) .4($1,000)

$100

$85 2

($540 $400)

$85 $50

$940

$135 14.36%

$940

−

+

=

+

+

=

+

+

=

==

recovery period.

4. Bond yields (LO2) An investor must choose between two bonds:

Bond A pays $92 annual interest and has a market value of $875. It has 10 years to

maturity. Bond B pays $82 annual interest and has a market value of $900. It has two years

to maturity.

a. Compute the current yield on both bonds.

b. Which bond should she select based on your answer to part a?

c. A drawback of current yield is that it does not consider the total life of the bond. For