Chapter 13: Risk and Capital Budgeting

13-41

COMPREHENSIVE PROBLEMS

Comprehensive Problem 1.

Gibson Appliance Co. (portfolio effect of a merger) (LO5) Gibson Appliance Co. is a very

stable billion-dollar company with a sales growth of about 7 percent per year in good or bad

economic conditions. Because of this stability (a coefficient of correlation with the economy

of +.4, and a standard deviation of sales of about 5 percent from the mean), Mr. Hoover, the

vice-president of finance, thinks the company could absorb a small risky company that could

add quite a bit of return without increasing the company’s risk very much. He is trying to decide

which of the two companies he will buy, using the figures below. Gibson’s cost of capital is

12 percent.

Genetic Technology Co.

(cost $80 million)

Silicon Microchip Co.

(cost $80 million)

Cash Flow

for 10 Years

($ millions)

Probability

Cash Flow

for 10 Years

($ millions)

Probability

$ 2

.2

$ 5

.2

8

.3

7

.2

16

.2

18

.3

25

.2

24

.3

40

.1

a. What is the expected cash flow from both companies?

b. Which company has the lower coefficient of variation?

c. Compute the net present value of each company.

d. Which company would you pick, based on the net present values?

e. Would you change your mind if you added the risk dimensions to the problem? Explain.

f. What if Genetic Technology Co. had a coefficient of correlation with the economy

of –.2 and Silicon Microchip Co. had one of +.5? Which of these companies would

give you the best portfolio effects for risk reduction?

g. What might be the effect of the acquisitions on the market value of Gibson Appliance

Co.’s stock?

Chapter 13: Risk and Capital Budgeting

13-42

CP 13-1 Solution:

Portfolio Effect of a Merger

Gibson Appliance Co.

a. Genetic Technology Co. Silicon Microchip Co.

D

P

DP

D

P

DP

$ 2

.2

.4

$ 5

.2

1.0

8

.3

2.4

7

.2

1.4

16

.2

3.2

18

.3

5.4

25

.2

5.0

24

.3

7.2

40

.1

4.0

Expected Value

of Cash Flows

$15.0

(million)

Expected Value

of Cash Flows

$15.0

(million)

b. Coefficient of variation for Genetic Technology Co.

D

D

(D D)−

2

(D D)−

P

2

(D D)−

P

$ 2

$15

$–13

$169

.2

$33.8

8

15

–7

49

.3

14.7

16

15

+1

1

.2

.2

25

15

+10

100

.2

20.0

40

15

+25

625

.1

62.5

$131.2

131.2 $11.45 (million)

==

Chapter 13: Risk and Capital Budgeting

CP 13-1. (Continued)

Coefficient of variation for Silicon Microchip Co.

D

D

(D D)−

2

(D D)−

P

2

(D D)−

P

$ 5

$15

$–103

$100

.2

$20.0

7

15

–8

64

.2

12.8

18

15

+3

9

.3

2.7

24

15

+9

81

.3

24.3

$59.8

Chapter 13: Risk and Capital Budgeting

13-44

the economy is –.2.

g. Because Gibson Appliance Co. is a stable billion–dollar company,

this investment of $80 million would probably not have a great

impact on the stock price in the short run. There could be some

discuss risk-return trade-offs and market reactions.

Comprehensive Problem 2.

Kennedy Trucking Company (investment decision based on probability analysis) (LO1)

Five years ago, Kennedy Trucking Company was considering the purchase of 60 new diesel

trucks that were 15 percent more fuel-efficient than the ones the firm is now using. Mr. Hoffman,

the president, had found that the company uses an average of 10 million gallons of diesel fuel per

year at a price of $1.25 per gallon. If he can cut fuel consumption by 15 percent, he will save

$1,875,000 per year (1,500,000 gallons times $1.25).

Mr. Hoffman assumed that the price of diesel fuel is an external market force that he cannot

control and that any increased costs of fuel will be passed on to the shipper through higher rates

endorsed by the Interstate Commerce Commission. If this is true, then fuel efficiency would save

more money as the price of diesel fuel rises (at $1.35 per gallon, he would save $2,025,000 in

total if he buys the new trucks). Mr. Hoffman has come up with two possible forecasts shown

below—each of which he feels has about a 50 percent chance of coming true. Under assumption

number 1, diesel prices will stay relatively low; under assumption number 2, diesel prices will

rise considerably. Sixty new trucks will cost Kennedy Trucking $5 million. Under a special

provision from the Interstate Commerce Commission, the allowable depreciation will be

25 percent in year 1, 38 percent in year 2, and 37 percent in year 3. The firm has a tax rate of

40 percent and a cost of capital of 10 percent.

a. First compute the yearly expected price of diesel fuel for both assumption 1 (relatively

low prices) and assumption 2 (high prices) from the forecasts below.

Forecast for assumption 1 (low fuel prices):

Chapter 13: Risk and Capital Budgeting

13-45

Probability

(same for each year)

Price of Diesel Fuel per Gallon

Year 1

Year 2

Year 3

.1

$ .80

$ .90

$1.00

.2

1.00

1.10

1.10

.3

1.10

1.20

1.30

.2

1.30

1.45

1.45

.2

1.40

1.55

1.60

Forecast for assumption 2 (high fuel prices):

Probability

(same For each year)

Price of Diesel Fuel per Gallon

Year 1

Year 2

Year 3

.1

$1.20

$1.50

$1.70

.3

1.30

1.70

2.00

.4

1.80

2.30

2.50

.2

2.20

2.50

2.80

b. What will be the dollar savings in diesel expenses each year for assumption 1 and for

assumption 2?

c. Find the increased cash flow after taxes for both forecasts.

d. Compute the net present value of the truck purchases for each fuel forecast

assumption and the combined net present value (that is, weigh the NPV by .5).

e. If you were Mr. Hoffman, would you go ahead with this capital investment?

f. How sensitive to fuel prices is this capital investment?

CP 13-2 Solution:

Investment Decision Based on Probability Analysis

Kennedy Trucking Company

a. Assumption One:

Chapter 13: Risk and Capital Budgeting

13-46

Yr.1

Yr.2

Yr.3

Probability

D

DP

D

DP

D

DP

.1

$0.80

.08

$0.90

.09

$1.00

.10

.2

1.00

.20

1.10

.22

1.10

.22

.3

1.10

.33

1.20

.36

1.30

.39

.2

1.30

.26

1.45

.29

1.45

.29

.2

1.40

.28

1.55

.31

1.60

.32

Expected value

$1.15/gallon

$1.27/gallon

$1.32/gallon

Assumption Two:

Yr.1

Yr.2

Yr.3

Probability

D

DP

D

DP

D

DP

.1

$1.20

.12

$1.50

.15

$1.70

.17

.3

1.30

.39

1.70

.51

2.00

.60

.4

1.80

.72

2.30

.92

2.50

1.00

.2

2.20

.44

2.50

.50

2.80

.56

Expected value

$1.67/gallon

$2.08/gallon

$2.33/gallon

13-CP 2. (Continued)

b. Assumption One:

Yr.

Expected

Cost/gal.

#of Gals.

Without

Efficiency=

Cost

% Savings

with

Efficiency

Total

$ Saved

1

$1.15

10 million

$11,500,000

15%

$1,725,000

2

1.27

12,700,000

1,905,000

3

1.32

13,200,000

1,980,000

Assumption Two:

Chapter 13: Risk and Capital Budgeting

13-47

Yr.

Expected

Cost/gal.

#of Gals.

without

Efficiency=

Cost

% Savings

with

Efficiency

Total

$ Saved

1

$1.67

10 million

$16,700,000

15%

$2,505,000

2

2.08

20,800,000

3,120,000

3

2.33

23,300,000

3,495,000

c. First compute annual depreciation: Then proceed to the analysis.

Year 1

25% × $5 mil. = 1.25 mil.

Year 2

38% × $5 mil. = 1.90 mil.

Year 3

37% × $5 mil. = 1.85 mil.

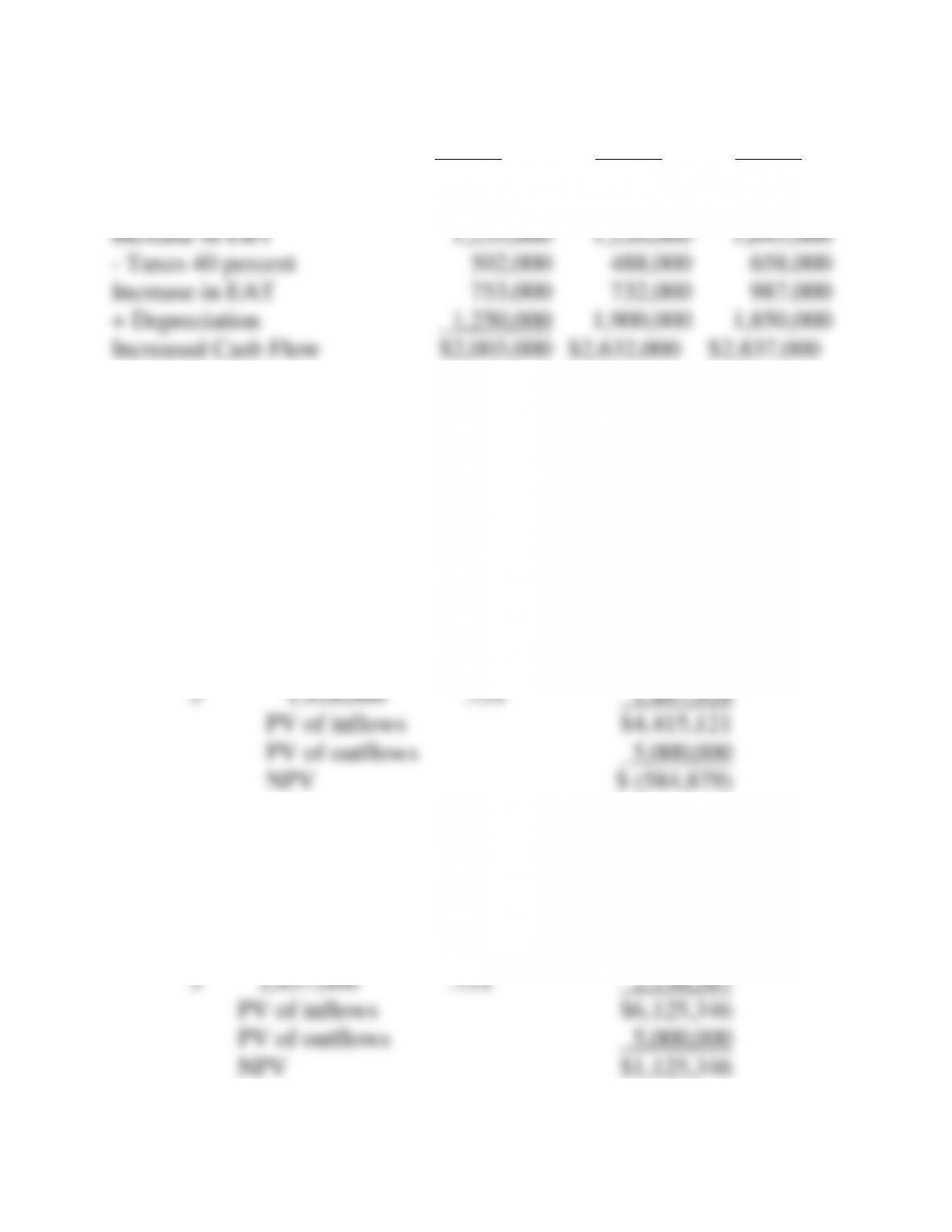

13-CP 2. (Continued)

Assumption One:

Year 1

Year 2

Year 3

Increase in EBDT

$1,725,000

$1,905,000

$1,980,000

– Depreciation

1,250,000

1,900,000

1,850,000

Increase in EBT

475,000

5,000

130,000

– Taxes 40 percent

190,000

2,000

52,000

Increase in EAT

285,000

3,000

78,000

+ Depreciation

1,250,000

1,900,000

1,850,000

Increased Cash Flow

$1,535,000

$1,903,000

$1,928,000

Assumption Two:

Chapter 13: Risk and Capital Budgeting

13-48

Year 1

Year 2

Year 3

Increase in EBDT

$2,505,000

$3,120,000

$3,495,000

– Depreciation

1,250,000

1,900,000

1,850,000

Increase in EBT

1,255,000

1,220,000

1,645,000

– Taxes 40 percent

502,000

488,000

658,000

Increase in EAT

753,000

732,000

987,000

+ Depreciation

1,250,000

1,900,000

1,850,000

Increased Cash Flow

$2,003,000

$2,632,000

$2,837,000

13-CP 2. (Continued)

d. Present Value

Assumption One:

Year

Cash Flow

PVIF @ 10%

Present Value

1

$1,535,000

.909

$1,395,315

2

1,903,000

.826

1,571,878

3

1,928,000

.751

1,447,928

PV of inflows

$4,415,121

PV of outflows

5,000,000

NPV

$ (584,879)

Assumption Two:

Year

Cash Flow

PVIF @ 10%

Present Value

1

$2,003,000

.909

$1,820,727

2

2,632,000

.826

2,174,032

3

2,837,000

.751

2,130,587

PV of inflows

$6,125,346

PV of outflows

5,000,000

NPV

$1,125,346

Chapter 13: Risk and Capital Budgeting

13-49

Combined NPV:

Outcome

NPV

Probability

Assumption One

–584,879

.5

–292,440

Assumption Two

1,125,346

.5

562.673

Expected Outcome

$270,233

e. Yes—The combined expected value of the outcomes is positive.