Unlock document.

This document is partially blurred.

Unlock all pages and 1 million more documents.

Get Access

Chapter 13: Risk and Capital Budgeting

13-23. (Continued)

Standard deviation—year 10

D

D

(D D)−

2

(D D)−

P

2

(D D)−

P

40

80

–40

1,600

.30

480

80

80

0

0

.40

0

120

80

+40

1,600

.30

480

960

Chapter 13: Risk and Capital Budgeting

13-32

13-23. (Continued)

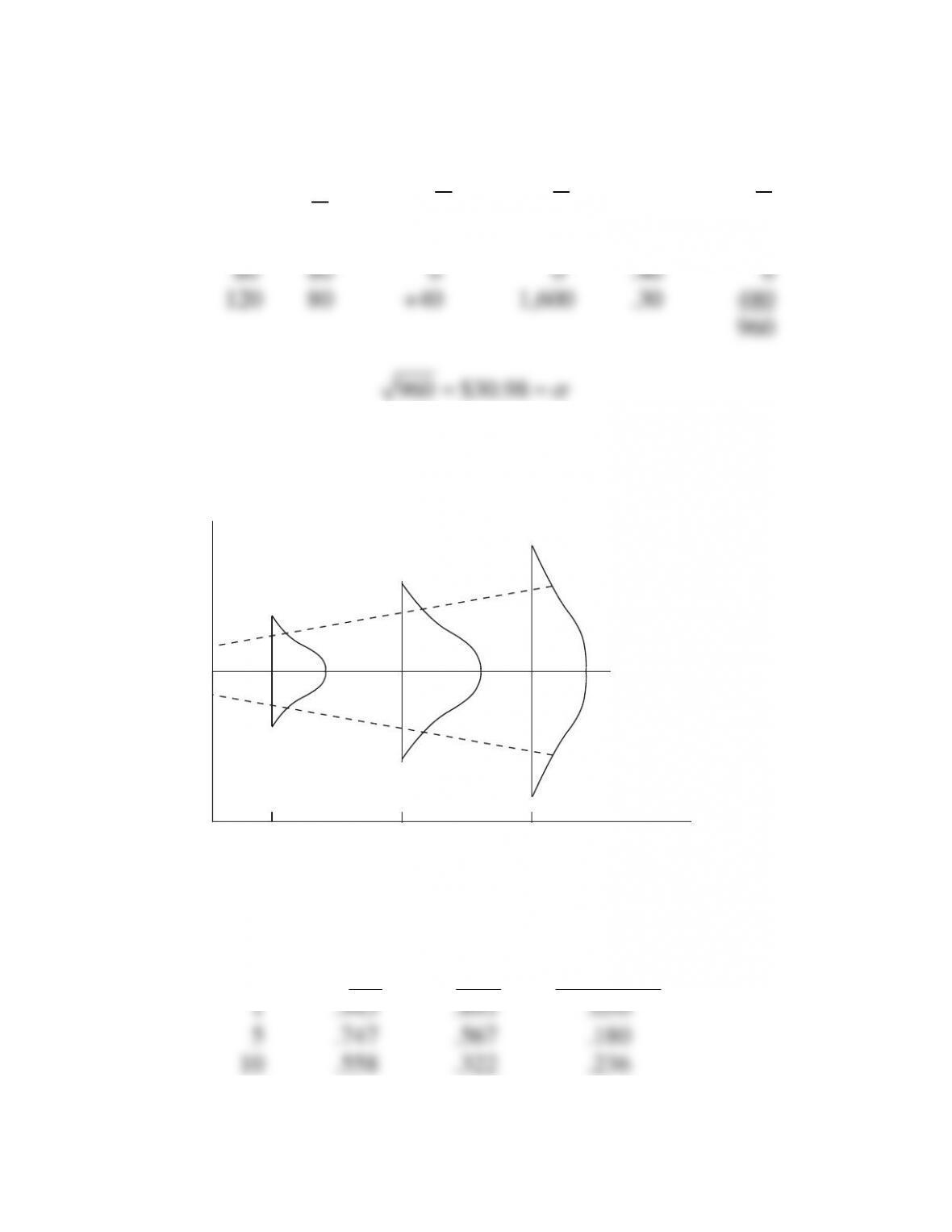

d. Yes. The larger risk over time is consistent with the larger

differences in the present value interest factors (IFPV) over

Year

Inflow

PVIF (12%)

PV

1

$80

.893

$ 71.4

5

80

.567

$ 45.4

10

80

.322

$ 25.8

PV of inflows

$142.6

Investment

$135.0

NPV

$ 7.6

e. Accept the investment.

Chapter 13: Risk and Capital Budgeting

13-33

24. Portfolio effect of a merger (LO5) Treynor Pie Co. is a food company specializing in

high-calorie snack foods. It is seeking to diversify its food business and lower its risks. It is

examining three companies—a gourmet restaurant chain, a baby food company and a

nutritional products firm. Each of these companies can be bought at the same multiple of

earnings. The following represents information about all the companies.

Company

Correlation

with Treynor

Pie Company

Sales

($ millions)

Expected

Earnings

($ millions)

Standard

Deviation

in Earnings

($ millions)

Treynor Pie Company ............

+ 1.0

$100

$8

$2.0

Gourmet restaurant ................

+ .6

60

6

1.2

Baby food company ...............

+ .2

50

4

1.8

Nutritional products

company ................................

− .7

70

5

3.4

a. Using the last two columns, compute the coefficient of variation for each of the four

companies. Which company is the least risky? Which company is the most risky?

b. Discuss which of the acquisition candidates is most likely to reduce Treynor Pie

Company’s risk? Explain why.

13-24. Solution:

Treynor Pie Co.

a.

standard deviation

Coefficient of variation (V) expected value

=

(millions)

Treynor Pie Co. $2/$8 = .25

The Gourmet Restaurant chain is the least risky with

Chapter 13: Risk and Capital Budgeting

13-34

13-24. (Continued)

b. Because the nutritional products firm is highly negatively

correlated (–.7) with Treynor Pie Co., it is most likely to

Thus, Treynor Pie Co. would reduce its risk to the largest

extent by acquiring the company with the highest

25. Portfolio effect of a merger (LO5) Transoceanic Airlines is examining a resort motel

chain to add to its operation. Prior to the acquisition, the normal expected outcomes for the

firm are as follows:

Outcomes

($ millions)

Probability

Recession ...........................

$30

.30

Normal economy ................

50

.40

Strong economy .................

70

.30

After the acquisition, the expected outcomes for the firm would be:

Outcomes

($ millions)

Probability

Recession ...........................

$ 10

.30

Normal economy ................

50

.40

Strong economy .................

100

.30

Chapter 13: Risk and Capital Budgeting

a. Compute the expected value, standard deviation, and coefficient of variation before

the acquisition.

After the acquisition, these values are as follows:

Expected value ......................................

53.0 ($ millions)

Standard deviation .................................

34.9 ($ millions)

Coefficient of variation..........................

.658

b. Comment on whether this acquisition appears desirable to you.

c. Do you think the firm’s stock price is likely to go up as a result of this acquisition?

d. If the firm were interested in reducing its risk exposure, which of the following three

industries would you advise it to consider for an acquisition? Briefly comment on

your answer.

(1) Major travel agency

(2) Oil company

(3) Gambling casino

13-25. Solution:

Transoceanic Airlines

D DP=

D P PD

$30 .30 9

Chapter 13: Risk and Capital Budgeting

13-36

13-25. (Continued)

D

D

(D D)−

2

(D D)−

P

2

(D D)−

P

$30

50

–20

400

.30

120

50

50

0

0

.40

0

70

50

+20

400

.30

120

240

240 $15.5 ($million)=

V = $15.5/$50 = .310

c. Probably not. There may be a higher discount rate applied

to the firm’s earnings to compensate for the additional risk.

The stock price may actually go down.

way of risk reduction benefits. They are both closely

associated with entertainment and travel.

Chapter 13: Risk and Capital Budgeting

13-37

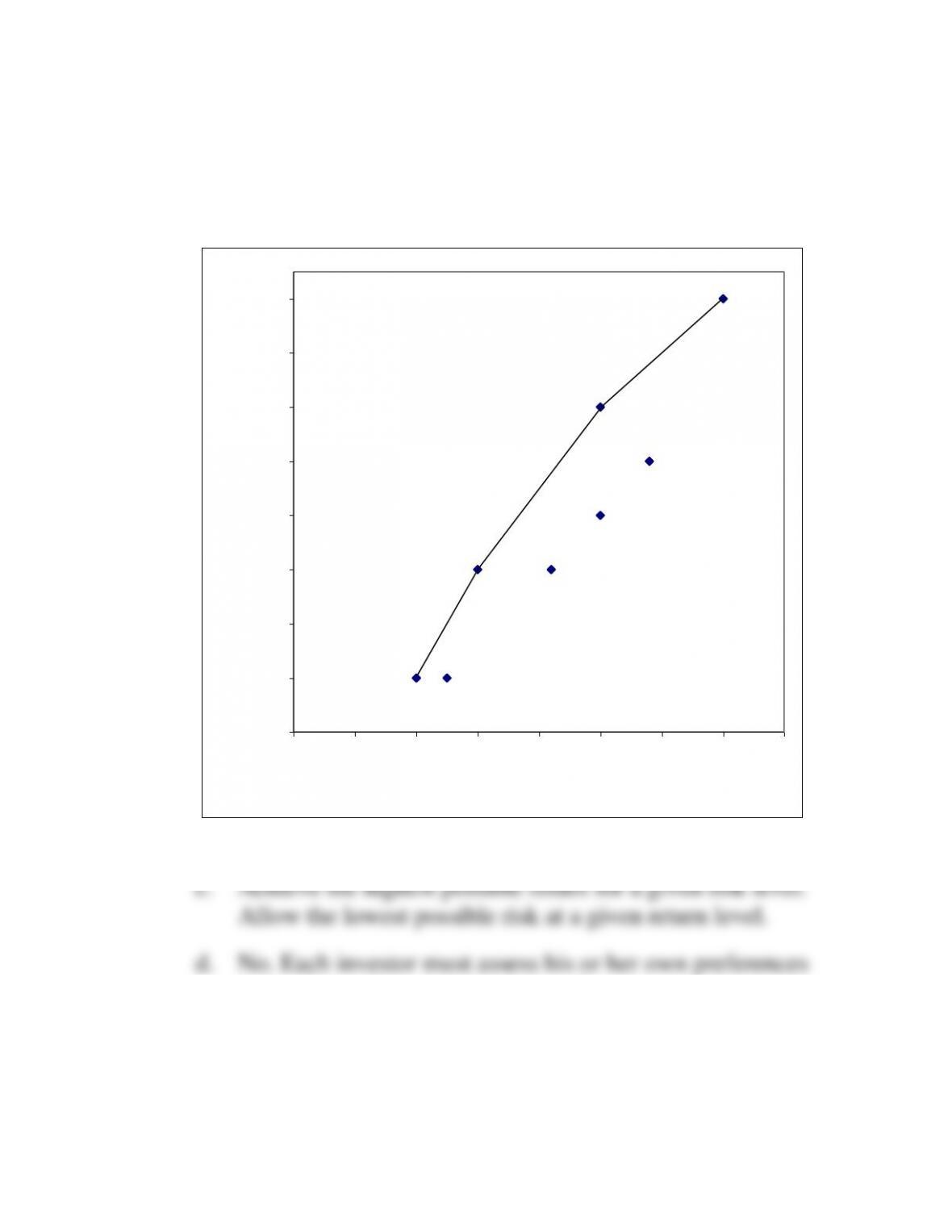

26. Efficient frontier (LO5) Ms. Sharp is looking at a number of different types of

investments for her portfolio. She identifies eight possible investments.

Return

Risk

Return

Risk

(a) .................

11%

2%

(e).................

14%

5.0%

(b) .................

11

2.5

(f) .................

16

5.0

(c) .................

13

3.0

(g) ................

15

5.8

(d) .................

13

4.2

(h) ................

18

7.0

a. Graph the data in a manner similar to Figure 13–11. Use the axes below for your data.

b. Draw a curved line representing the efficient frontier.

c. What two objectives do points on the efficient frontier satisfy?

d. Is there one point on the efficient frontier that is best for all investors?

Chapter 13: Risk and Capital Budgeting

13-38

13-26. Solution: Ms. Sharp

a., b.

10

11

12

13

14

15

16

17

18

0 1 2 3 4 5 6 7 8

Risk (percent)

Return

about their risk and return trade-off.

Chapter 13: Risk and Capital Budgeting

13-39

27. Certainty equivalent approach (LO1) Sheila Goodman recently received her MBA from

the Harvard Business School. She has joined the family business, Goodman Software

Products, Inc., as vice-president of finance.

She believes in adjusting projects for risk. Her father is somewhat skeptical but agrees

to go along with her. Her approach is somewhat different than the risk-adjusted discount

rate approach, but achieves the same objective.

She suggests that the inflows for each year of a project be adjusted downward for lack

of certainty and then be discounted back at a risk-free rate. The theory is that the

adjustment penalty makes the inflows the equivalent of risk-less inflows, and therefore a

risk-free rate is justified.

A table showing the possible coefficient of variation for an inflow and the associated

adjustment factor is shown below:

Coefficient

of Variation

Adjustment

Factor

0 –.25 .................

.90

.26 –.50 .................

.80

.51 –.75 .................

.70

.76 –1.00 ...............

.60

1.01–1.25 ...............

.50

Assume a $150,000 project provides the following inflows with the associated coefficients

of variation for each year.

Year

Inflow

Coefficient of Variation

1 ........................

$30,000

.12

2 ........................

50,000

.22

3 ........................

70,000

.46

4 ........................

55,000

.78

5 ........................

60,000

1.06

a. Fill in the table below:

Year

Inflow

Coefficient of

Variation

Adjustment

Factor

Adjusted

Inflow

1 ...................

$30,000

.12

____________

____________

2 ...................

50,000

.22

____________

____________

3 ...................

70,000

.46

____________

____________

4 ...................

55,000

.78

____________

____________

5 ...................

60,000

1.06

____________

____________

b. If the risk-free rate is 5 percent, should this $150,000 project be accepted? Compute

the net present value of the adjusted inflows.

Chapter 13: Risk and Capital Budgeting

13-40

13-27. Solution: Goodman Software Products

a. Adjusted Inflows

Year

Inflow

Coefficient

of Variation

Adjustment

Factor

Adjusted

Inflow

1

$30,000

.12

.90

$27,000

2

50,000

.22

.90

45,000

3

70,000

.46

.80

56,000

4

55,000

.78

.60

33,000

5

60,000

1.06

.50

30,000

b. Net Present Value

Year

Adjusted

Inflow

PVIF

at 5%

Present

Value

1

$27,000

.952

$ 25,704

2

45,000

.907

40,815

3

56,000

.864

43,384

4

33,000

.823

27,154

5

30,000

.784

23,520

Present value of adjusted inflows $165,577

Present value of outflows 150,000

Net present value $ 15,577

Based on the positive net present value of $15,577, the project

should be accepted.