Chapter 12: The Capital Budgeting Decision

12-41

29. MACRS depreciation and net present value (LO4) Universal Electronics is considering the

purchase of manufacturing equipment with a 10–year midpoint in its asset depreciation range

(ADR). Carefully refer to Table 12–8 to determine in what depreciation category the asset falls.

(Hint: It is not 10 years.) The asset will cost $90,000, and it will produce earnings before

depreciation and taxes of $32,000 per year for three years, and then $12,000 a year for seven

more years. The firm has a tax rate of 34 percent. With a cost of capital of 11 percent, should it

purchase the asset? Use the net present value method. In doing your analysis, if you have years

in which there is no depreciation, merely enter a zero for depreciation.

12–29. Solution:

Universal Electronics

Because the manufacturing equipment has a 10-year midpoint

of its asset depreciation range (ADR), it falls into the seven–

year MACRS category as indicated in Table 12–8.

We first determine the annual depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $90,000 .143 $12,870

2 90,000 .245 22,050

Chapter 12: The Capital Budgeting Decision

12-42

12-29. (Continued)

Annual Cash Flow

1

2

3

4

5

6

7

8

9

10

EBDT

$32,000

$32,000

$32,000

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

$12,000

– D

12,870

22,050

15,750

11,250

8,010

8,010

8,010

4,050

0

0

EBT

$19,130

$ 9,950

$16,250

$ 750

$ 3,990

$ 3,990

$ 3,990

$ 7,950

$12,000

$12,000

T (34%)

6,504

3,383

5,525

255

1,357

1,375

1,375

2,703

4,080

4,080

EAT

$12,626

$ 6,567

$10,725

$ 495

$ 2,633

$ 2,633

$ 2,633

$ 5,247

$ 7,920

$ 7,920

+ D

12,870

22,050

15,750

11,250

8,010

8,010

8,010

4,050

0

0

Cash Flow

$25,496

$28,617

$26,475

$11,745

$10,643

$10,643

$10,643

$ 9,297

$ 7,920

$ 7,920

Chapter 12: The Capital Budgeting Decision

12-43

12-29. (Continued)

Next determine the net present value.

Cash Flow Present

Year (inflows) PVIF at 11% Value

1 $25,496 .901 $ 22,972

2 28,617 .812 23,237

3 26,475 .731 19,353

Chapter 12: The Capital Budgeting Decision

12-44

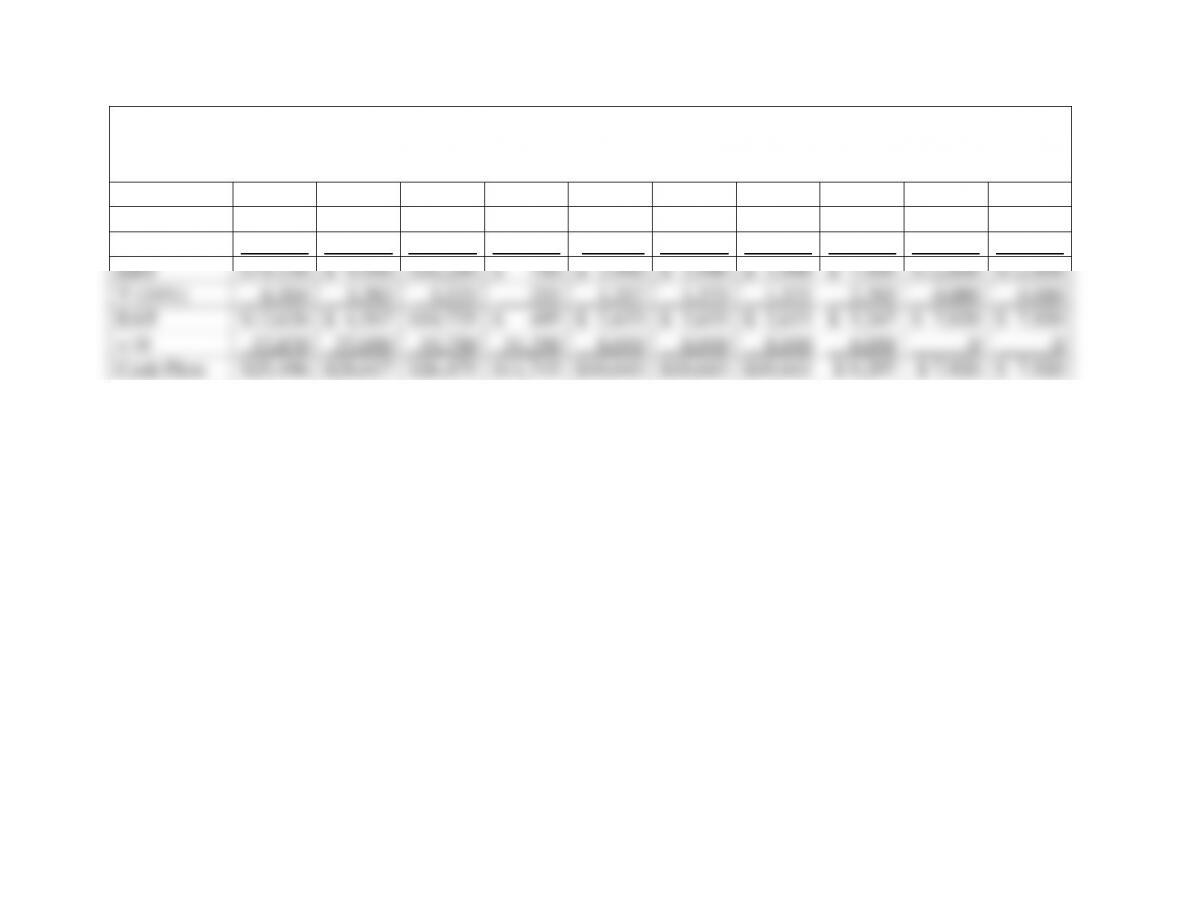

30. Working capital requirements in capital budgeting (LO4) The Bagwell Company has a

proposed contract with the First Military Base Facility of Texas. The initial investment in land

and equipment will be $90,000. Of this amount, $60,000 is subject to five–year MACRS

depreciation. The balance is in nondepreciable property (land). The contract covers six year

period. At the end of six years the nondepreciable assets will be sold for $30,000. The

depreciated assets will have zero resale value.

The contract will require an additional investment of $40,000 in working capital at the

beginning of the first year and, of this amount, $20,000 will be returned to the Bagwell

Company after six years.

The investment will produce $32,000 in income before depreciation and taxes for each of

the six years. The corporation is in a 35 percent tax bracket and has a 10 percent cost of capital.

Should the investment be undertaken? Use the net present value method.

12–30. Solution:

Bagwell Ball Bearing Company

Although there are some complicating features in the problem,

we are still comparing the present value of cash flows to the

total initial investment.

The initial investment is:

Non Depreciable Land …… $ 30,000

Chapter 12: The Capital Budgeting Decision

12-45

12-30. (Continued)

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $60,000 .200 $12,000

2 60,000 .320 19,200

We then determine the annual cash flow. In addition to normal

cash flow from operations; we also consider the funds

Annual Cash Flow

1 2 3 4 5 6

EBDT $32,000 $32,000 $32,000 $32,000 $32,000 $32,000

– D 12,000 19,200 11,520 6,900 6,900 3,480

Chapter 12: The Capital Budgeting Decision

12-46

12-30. (Continued)

We then determine the net present value.

Cash Flow Present

Year (inflows) PVIF at 10% Value

1 $ 25,000 .909 $ 22,725

2 27,520 .826 22,732

3 24,832 .751 18,649

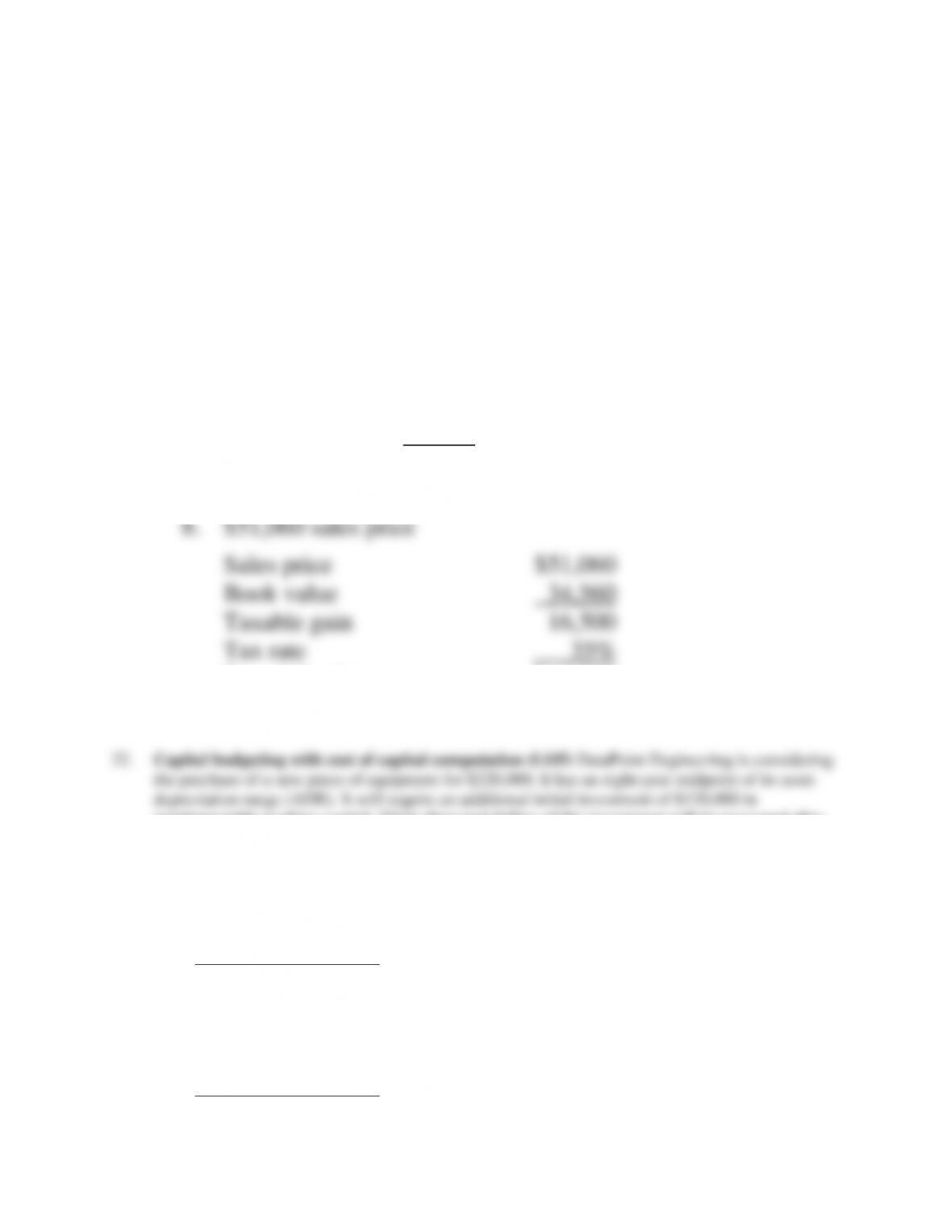

31. Tax losses and gains in capital budgeting (LO2) An asset was purchased three years ago

for $120,000. It falls into the five-year category for MACRS depreciation. The firm is in a

35 percent tax bracket. Compute the following:

a. Tax loss on the sale and the related tax benefit if the asset is sold now for $12,560.

b. Gain and related tax on the sale if the asset is sold now for $51,060. (Refer to footnote 4 in

the chapter.)

12–31. Solution:

First determine the book value of the asset.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $120,000 .200 $24,000

Chapter 12: The Capital Budgeting Decision

12-47

Purchase price $120,000

– Total depreciation to date 85,440

Book value $ 34,560

a. $12,560 sales price

b. $51,060 sales price

Sales price $51,060

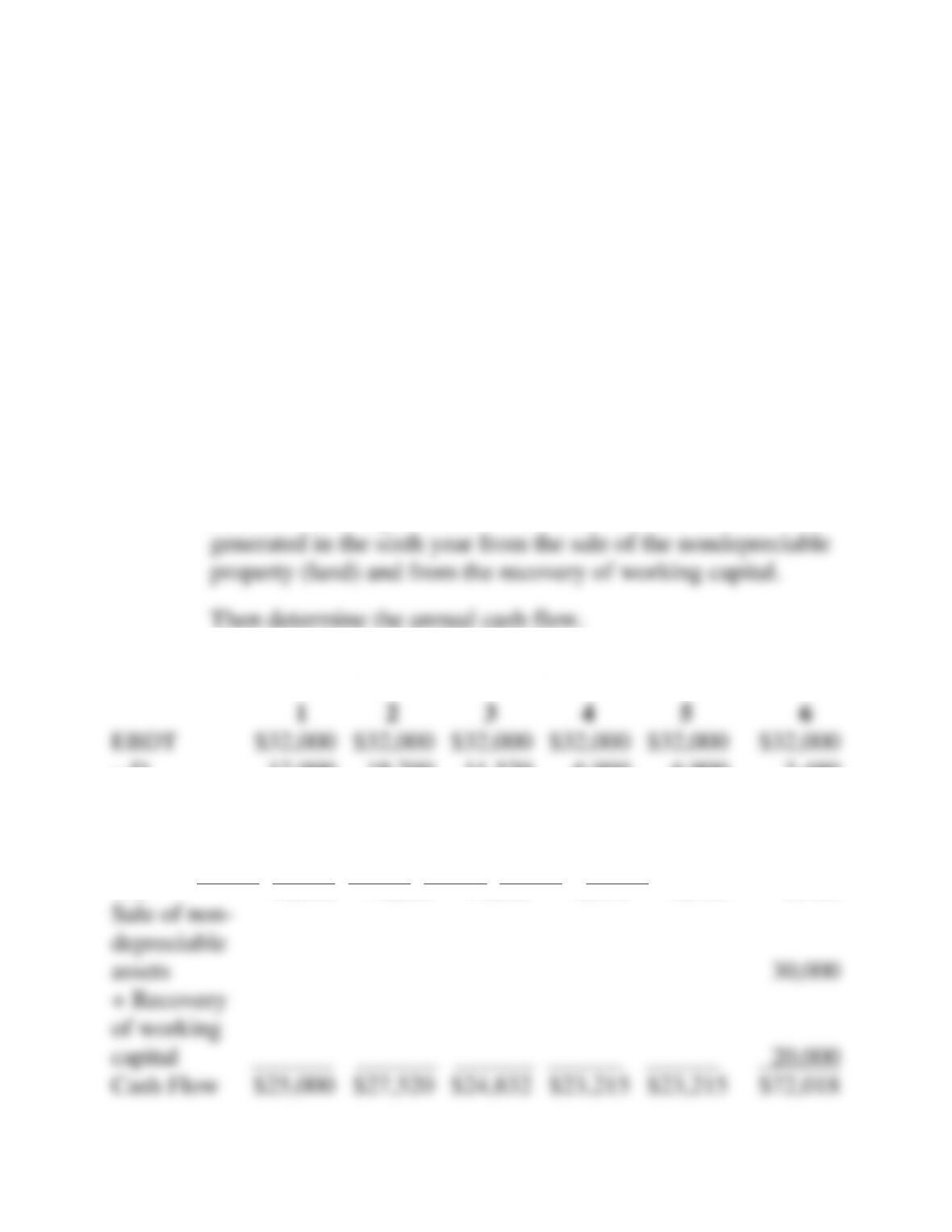

32. Capital budgeting with cost of capital computation (LO5) DataPoint Engineering is considering

the purchase of a new piece of equipment for $220,000. It has an eight-year midpoint of its asset

depreciation range (ADR). It will require an additional initial investment of $120,000 in

nondepreciable working capital. Thirty thousand dollars of this investment will be recovered after

the sixth year and will provide additional cash flow for that year. Income before depreciation and

taxes for the next six years will be:

Year Amount

1 ……………….. $170,000

2 ……………….. 150,000

3 ……………….. 120,000

4 ……………….. 105,000

5 ……………….. 90,000

6 ……………….. 80,000

Chapter 12: The Capital Budgeting Decision

12-48

The tax rate is 30 percent. The cost of capital must be computed based on

the following (round the final value to the nearest whole number):

Cost (aftertax)

Weights

Debt ………………………………………………….

Kd

6.5%

30%

Preferred stock ……………………………………

Kp

10.2

10

Common equity (retained earnings). ………

Ke

15.0

60

a. Determine the annual depreciation schedule.

b. Determine annual cash flow. Include recovered working capital in the sixth year.

c. Determine the weighted average cost of capital.

d. Determine the net present value. Should DataPoint purchase the new equipment?

12–32. Solution:

DataPoint Engineering

a. An 8-year midpoint of the ADR leads to 5–year MACRS

depreciation.

Percentage

Depreciation Depreciation Annual

Year Base (Table 12-9) Depreciation

1 $ 220,000 .200 $ 44,000

2 220,000 .320 70,400

Chapter 12: The Capital Budgeting Decision

12-49

b. Annual Cash Flow

1

2

3

4

5

6

EBDT

$170,000

$150,000

$120,000

$105,000

$90,000

$80,000

– D

44,000

70,400

42,240

25,300

25,300

12,760

EBT

$126,000

$ 79,600

$ 77,760

79,700

$64,700

67,240

T (30%)

37,800

23,880

23,328

23,910

19,410

20,172

EAT

88,000

55,720

54,432

55,790

45,290

47,068

+ D

44,000

70,400

42,240

25,300

25,300

12,760

+ Recov-

ery of

working

capital

30,000

Cash

Flow

$132,200

$126,120

$ 96,672

$ 81,090

$70,590

$89,828

12-31. (Continued)

c. Weighted Average Cost of Capital

Cost

(after tax)

Weights

Weighted

Debt

kd

6.5%

30%

1.95%

Preferred stock

kp

10.2%

10%

1.02%

Common equity

(retained earnings)

ke

15.0%

60%

9.00%

Weighted average

cost of Capital

11.97%