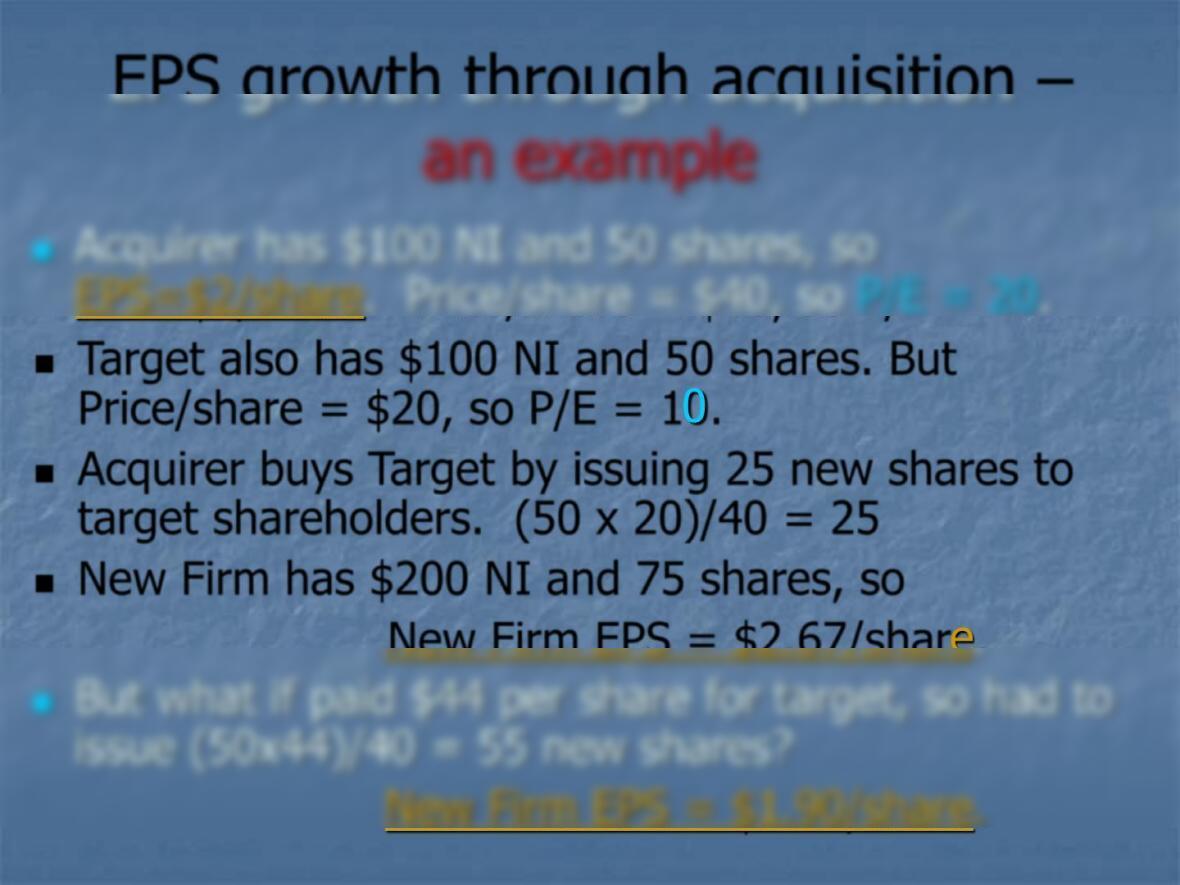

EPS growth through acquisition

◼A stock acquisition generally improves EPS

if the P/E of acquirer is greater than the

P/E of target.

◼Target also has $100 NI and 50 shares. But

Price/share = $20, so P/E = 10.

◼Acquirer buys Target by issuing 25 new shares to

target shareholders. (50 x 20)/40 = 25

◼New Firm has $200 NI and 75 shares, so

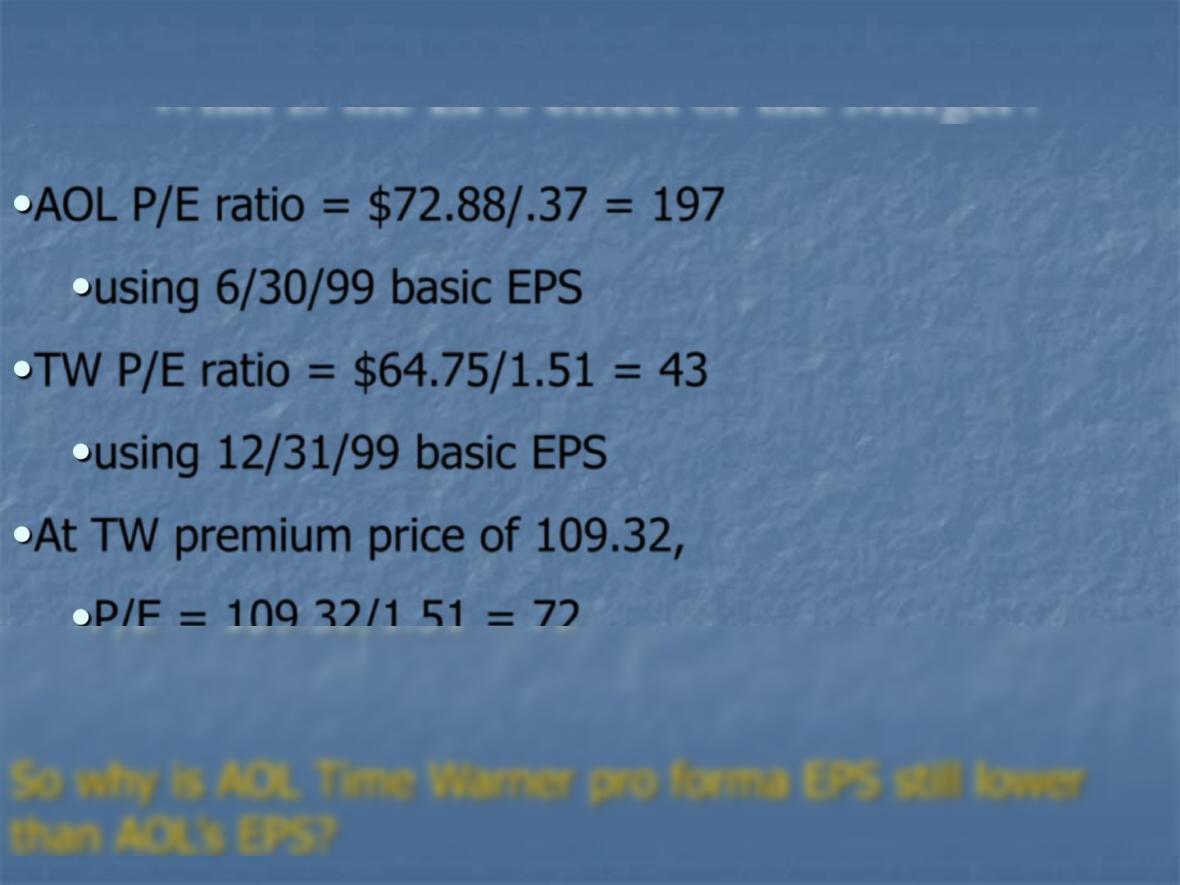

•AOL P/E ratio = $72.88/.37 = 197

•using 6/30/99 basic EPS

•TW P/E ratio = $64.75/1.51 = 43

•using 12/31/99 basic EPS

•At TW premium price of 109.32,

•P/E = 109.32/1.51 = 72

So why is AOL Time Warner pro forma EPS still lower

than AOL’s EPS?

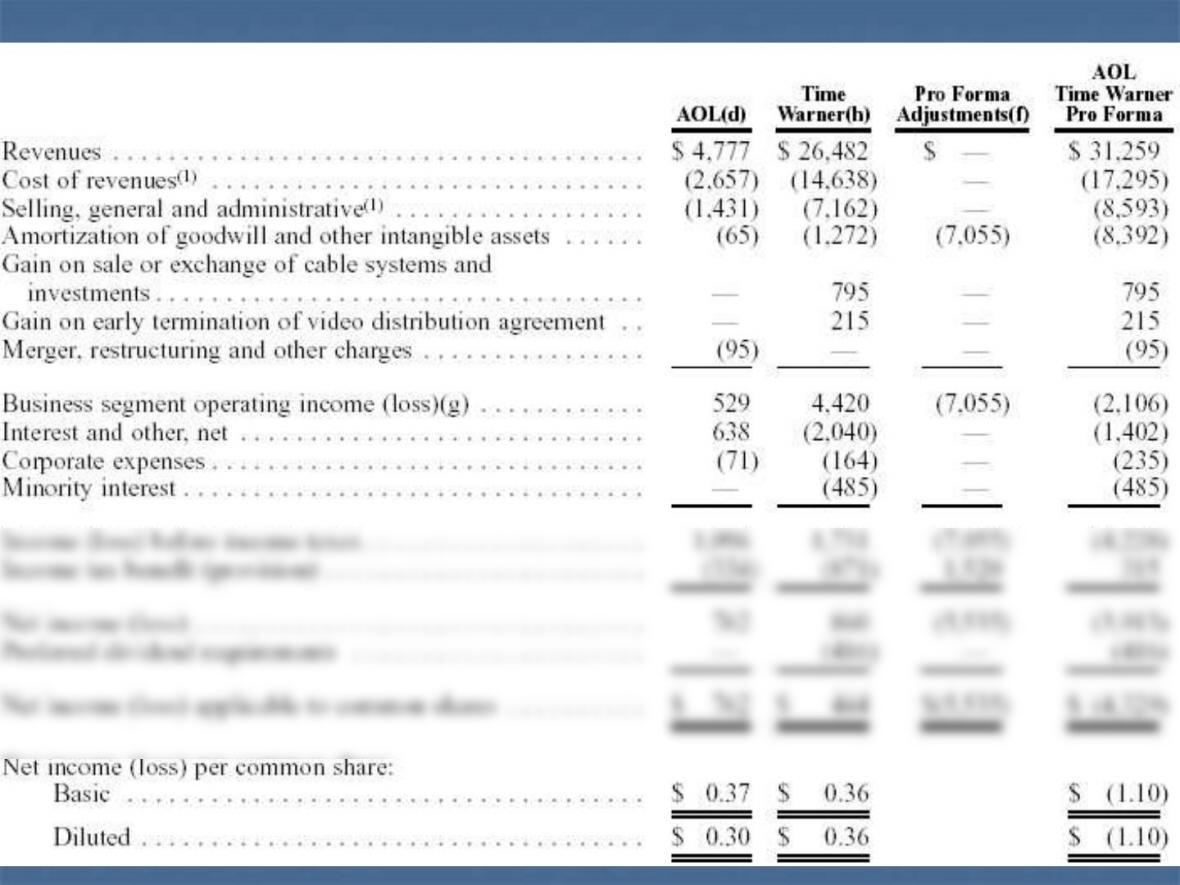

What is the EPS effect of the Merger?

Pro Forma AOL- Time Warner Income Statement 6/30/99

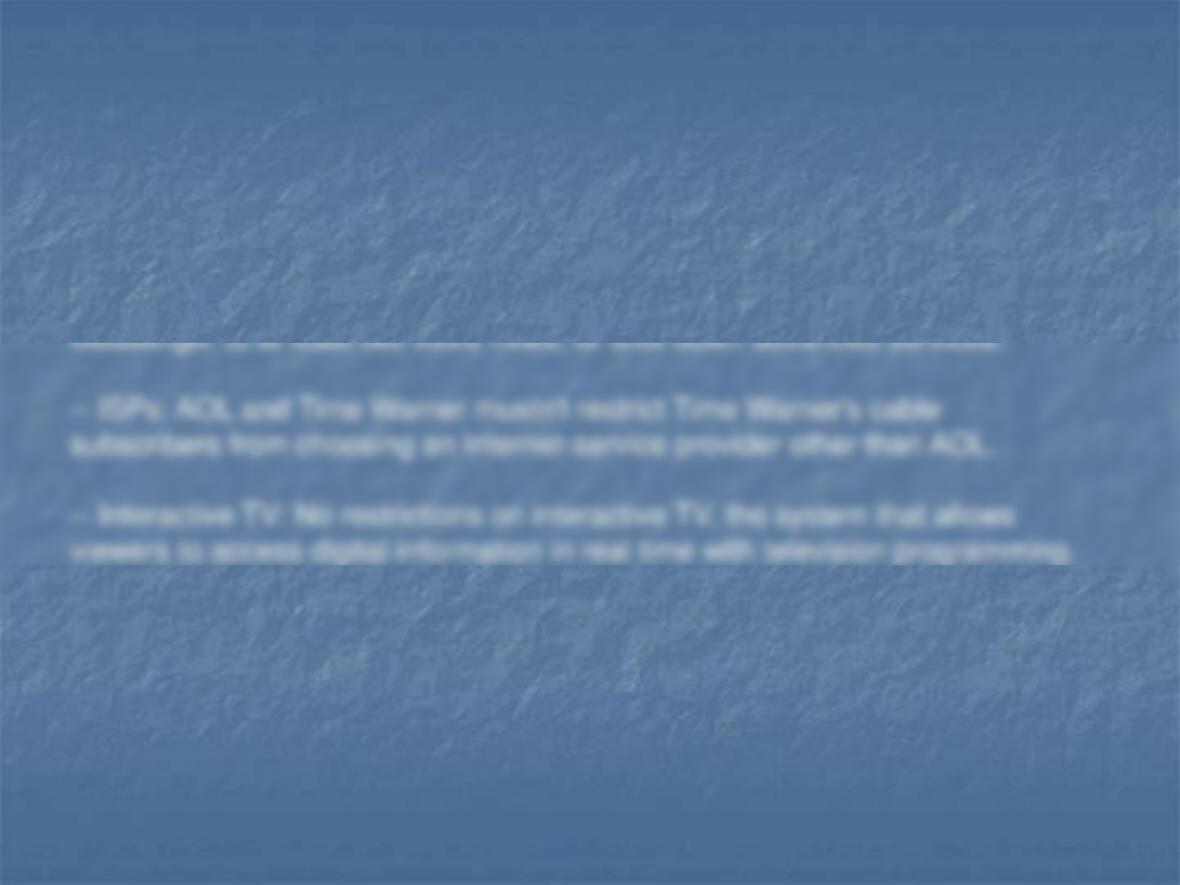

— Instant Messaging:

Option 1: AOL can’t offer advanced services, such as video streaming and

voice communications, over its Instant Messenger until it grants access to at

least one IM rival. Within six months, AOL would have to open up Instant

But the FCC said it would begin an inquiry into ways to ensure competition.

— AT&T: AOL-Time Warner and AT&T can’t enter into exclusive agreements

with each other that will affect rival ISPs’ access and terms of access to AOL–

Time Warner and AT&T‘s cable systems.

Source: FCC

Regulatory Constraints on Deal

Deal finally closed on

Jan. 11, 2001. Value

went from $162B to

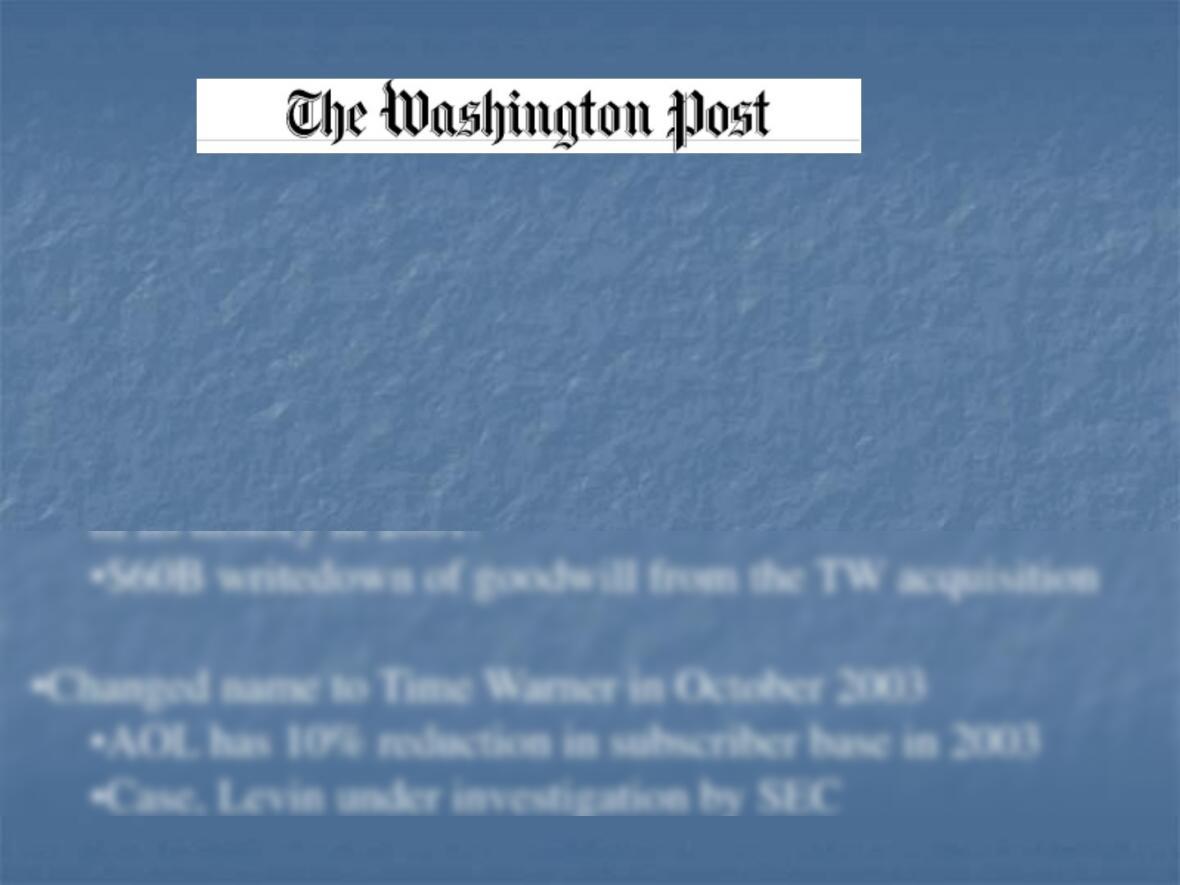

AOL Time Warner Lost $1.82 Billion; Dismal 4th-Quarter Result,

While Expected, Sends Stock to 3-Year Low

The Washington Post; Washington, D.C.; Jan 31, 2002; Alec Klein;

•2001 EPS = $-1.11

•Revenue per subscriber at AOL declined for the first time