Chestnuts (American Lorain) and

Chinese reverse mergers

The Chestnut – she’s a fickled beast

China’s

a’

world’

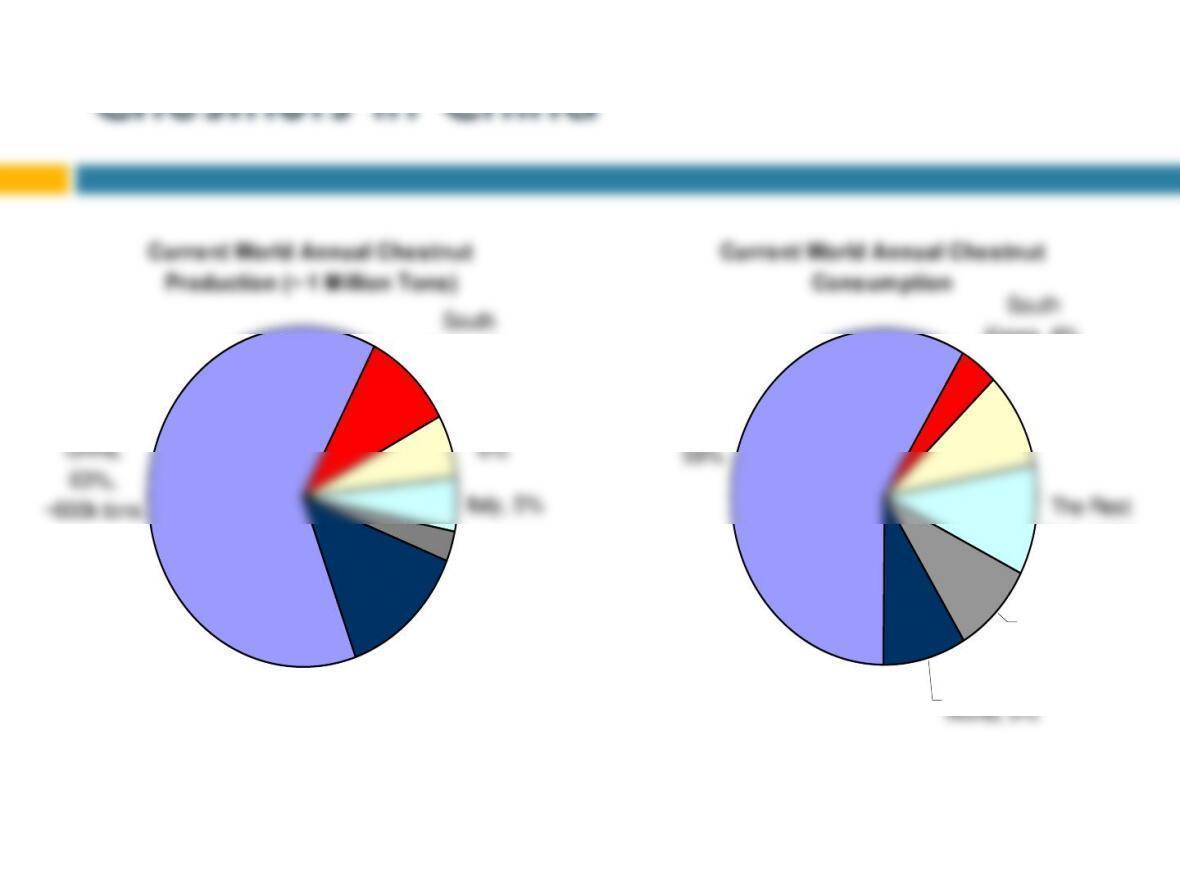

Current World Annual Chestnut

Production (~ 1 Million Tons)

South

Korea, 9%

Italy, 5%

Japan, 3%

13%

63%,

~600k tons

Current World Annual Chestnut

Cons um ption

South

Korea, 4%

The Rest

Asia, 11%

The Rest

World, 9%

China’s

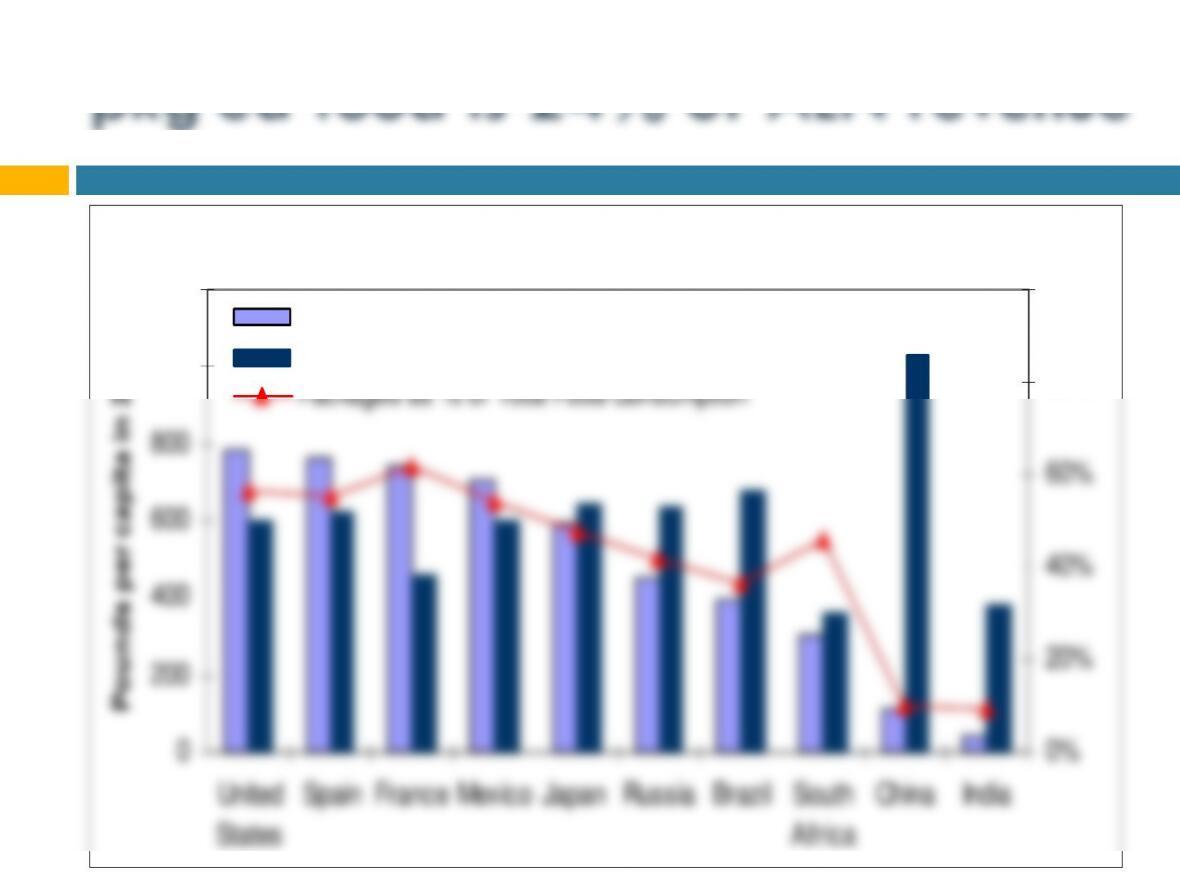

Chinese Citizens Consum e Less Packaged Food

1000

1200

States

Africa

80%

100%

Packaged Food Consumption

Fresh Food Consumption

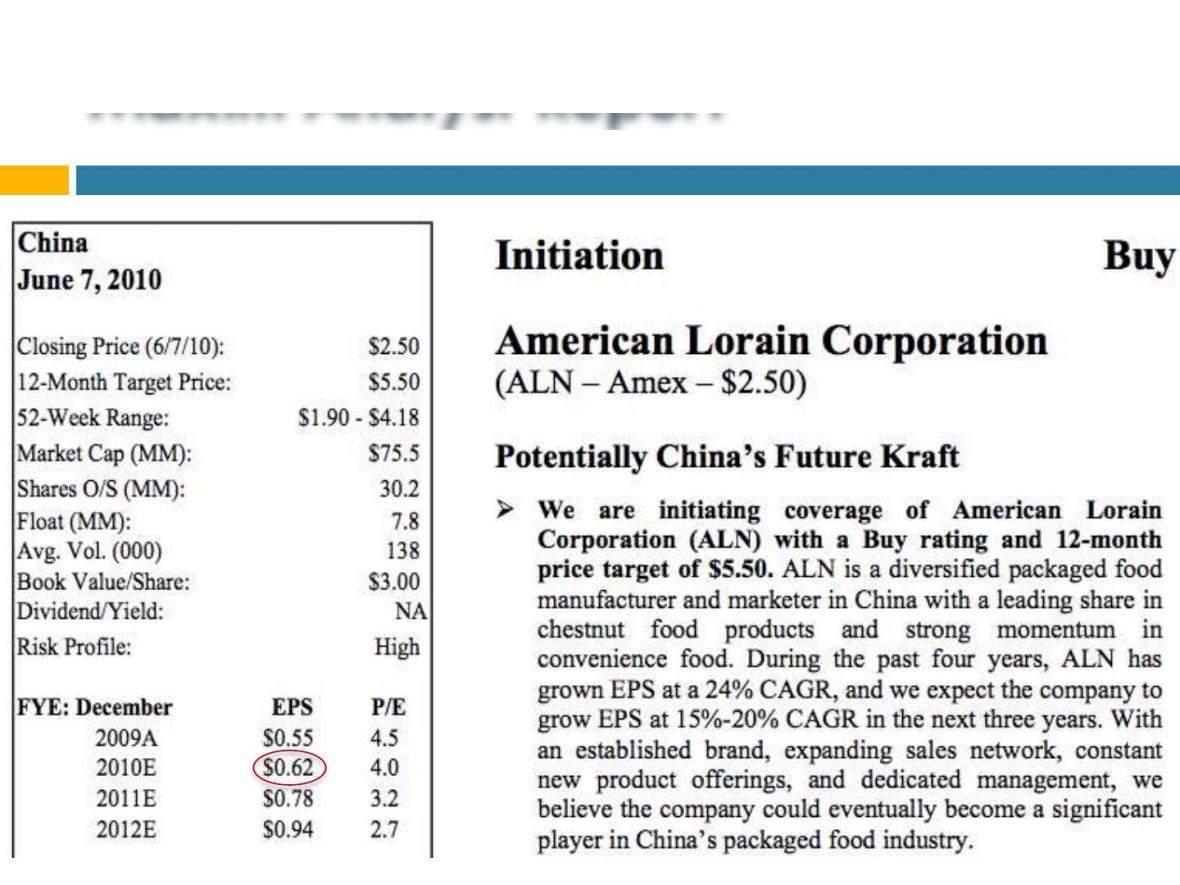

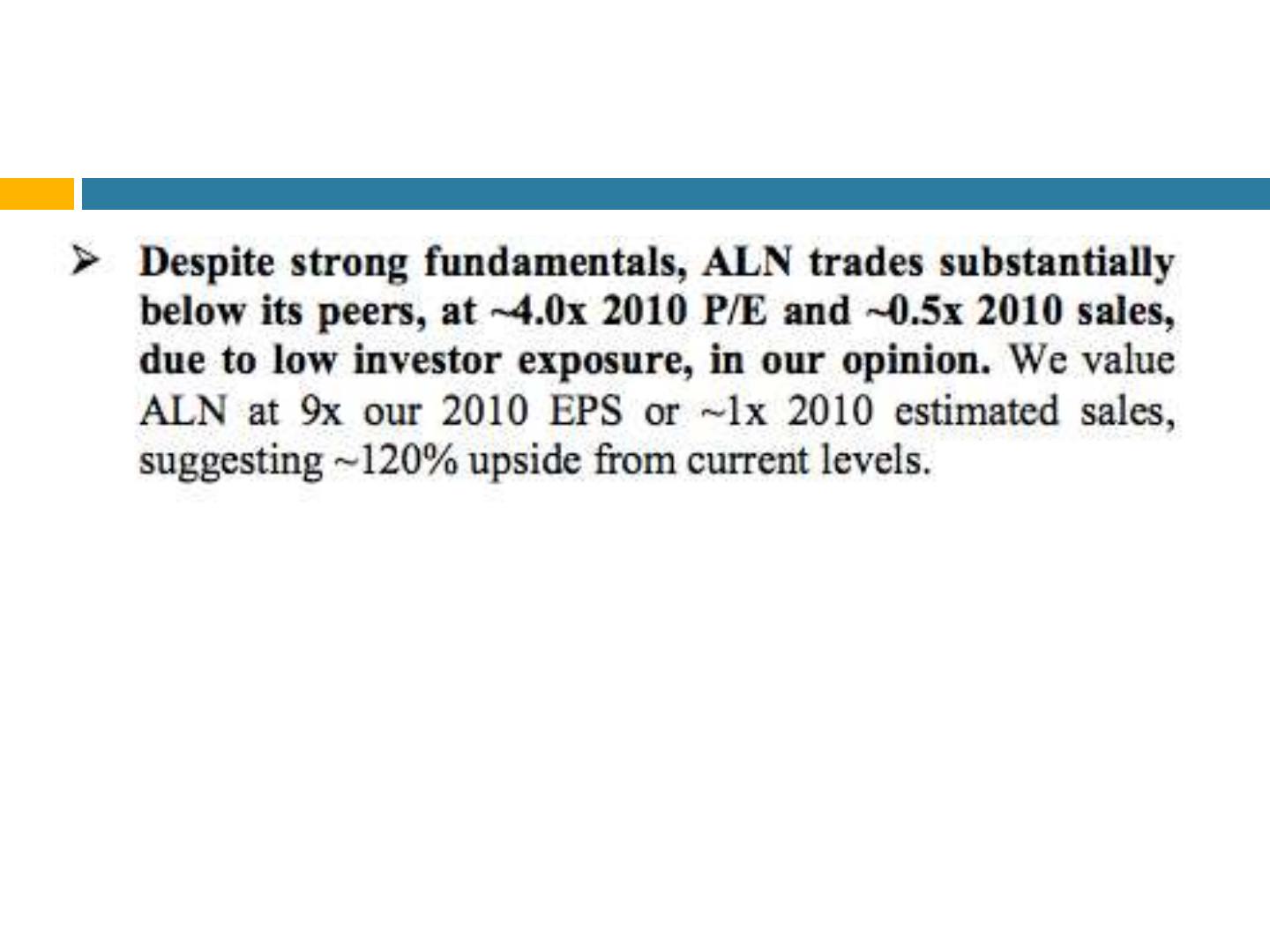

valuation based on P/E

Under what circumstances is this a good valuation

model? (assume the EPS of 62 cents/shr)

when is P/E = 9 the right answer?

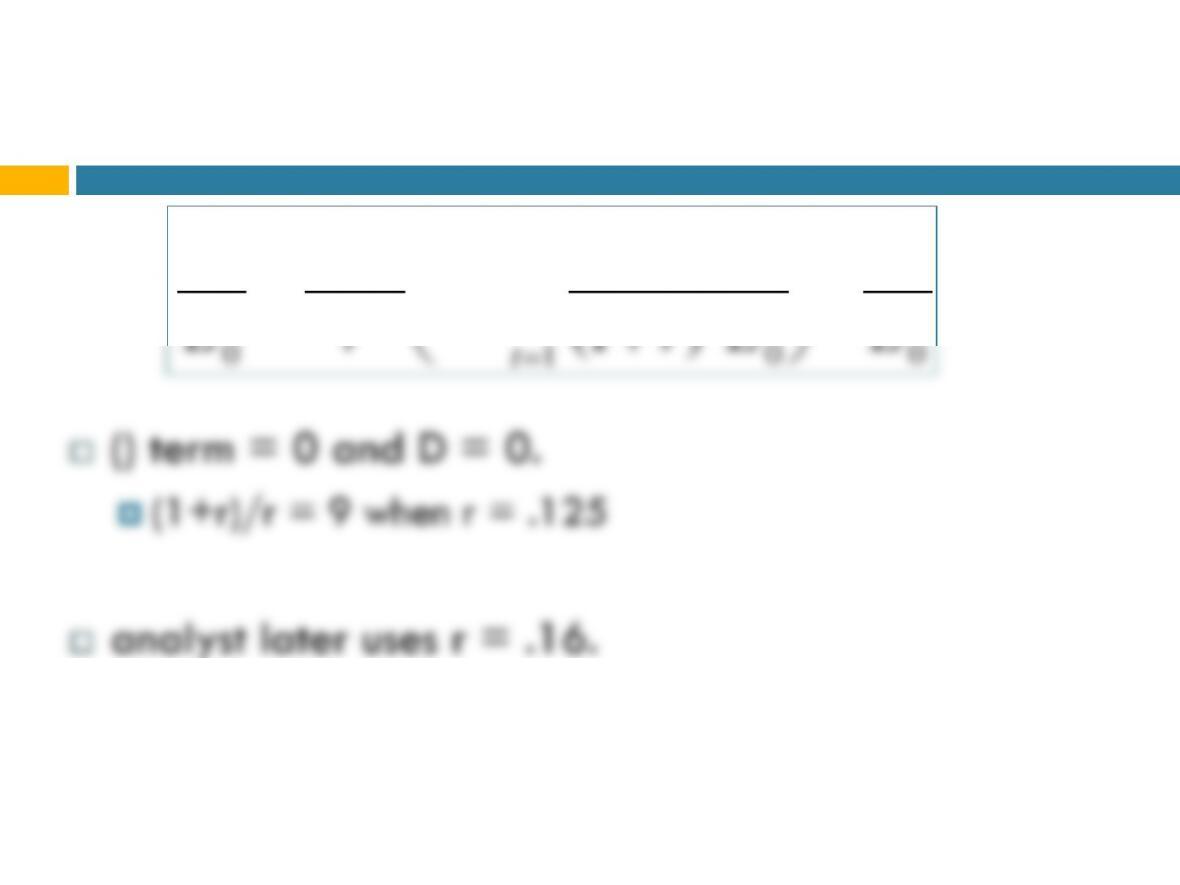

(1+.16)/.16 = 7.25.

need more growth in RI (need summation = .24)

did analyst forecast such growth from 2010 to 2011?

P0

E0

=1+r

r1+DRIt

(1+r)tE0

t=1

¥

å

æ

è

ç ö

ø

÷ –D0

E0

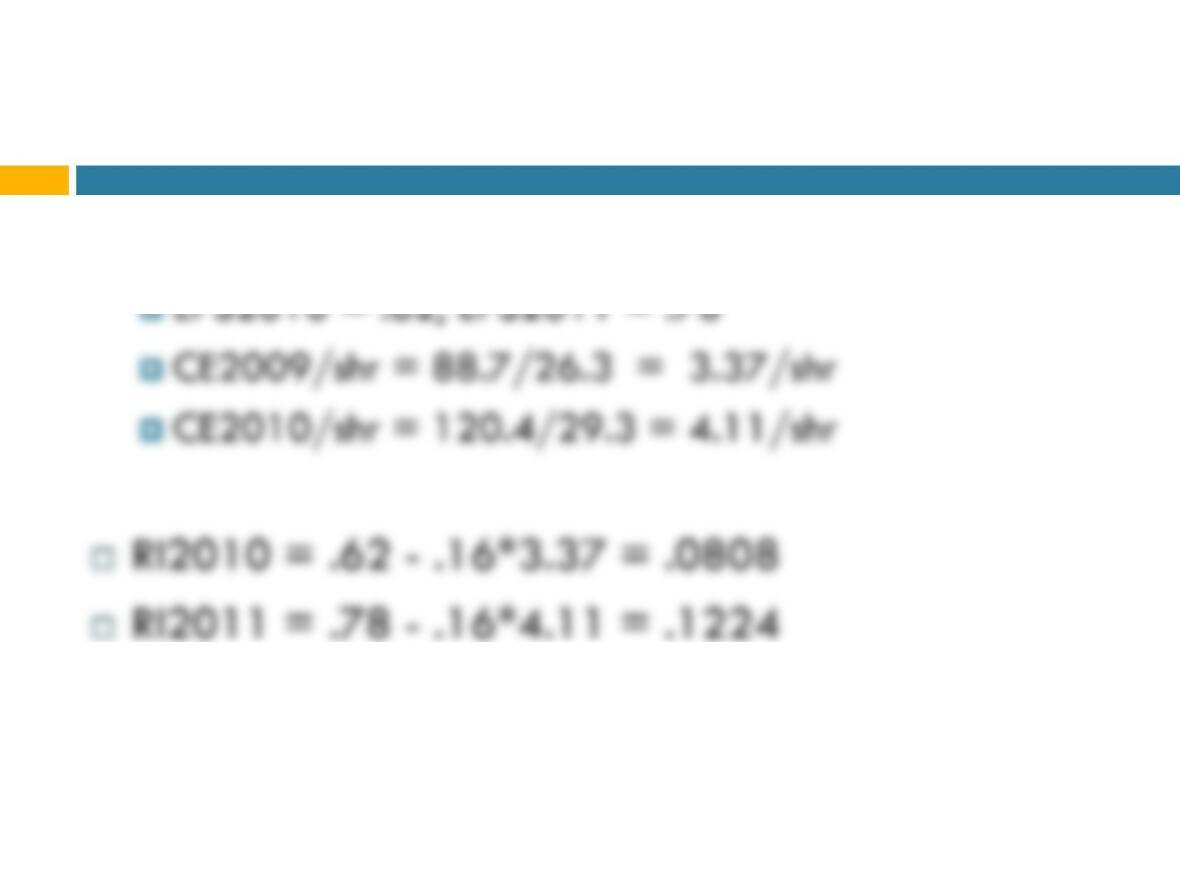

implied assumptions about RI growth

from analyst report

ΔRI = .1224 – .0808 = .0416.

ΔRI/E2009 = .0416/.55 = .0756

ΔRI/E in perpetuity = .0756/.16 = .47.

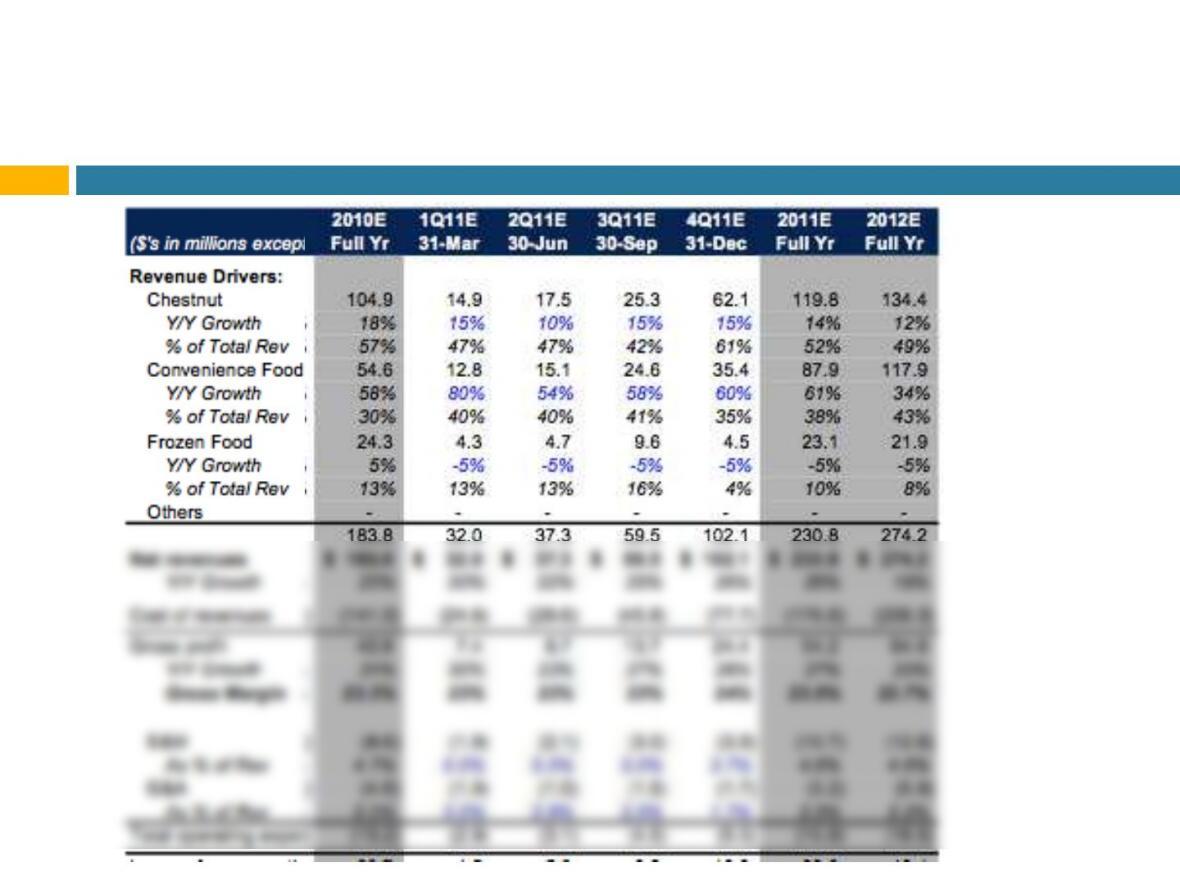

reserve-engineering the margins

reverse engineering the interest,