Turnaround at Bally Total Fitness

Case Overview

⚫A second revenue recognition case to compare and

contrast with the Boston Chicken Case.

⚫New management promotes installment membership

–Significant provision for loan losses on receivables

–Revenues are deferred and recognized ratably over the life of

membership contracts

Overview of Business

⚫The largest and only nationwide operator of fitness

⚫Initial membership fee can be financed for up to 36

months, and new management are heavily promoting

this option (aiming for 90% in 1999)

⚫Large losses in 1996 and 1997 turned to healthy profits

in 1998.

membership programs

⚫Strategic clustering in major metropolitan areas increases

access to target customers and facilitates sale of all-club

memberships

⚫Brand identity associated with ‘Bally’ service mark

–Localized competitors can better serve needs of local

community

⚫Fitness craze is a fad

⚫High operating leverage due to fixed costs associated with

fitness centers

⚫High interest rates

⚫Low cost of default (suspend membership)

⚫Very pro-active in limiting defaults

–Electronic payments

–“Aggressive” collection efforts

–Check the web page below for examples (warning: may

contain some unsavory language)

http://www.mwns.com/btf/

⚫Regulatory and legal risks

Bally’s Accounting for Financed

memberships

⚫Costs associated with membership origination are also

capitalized and deferred

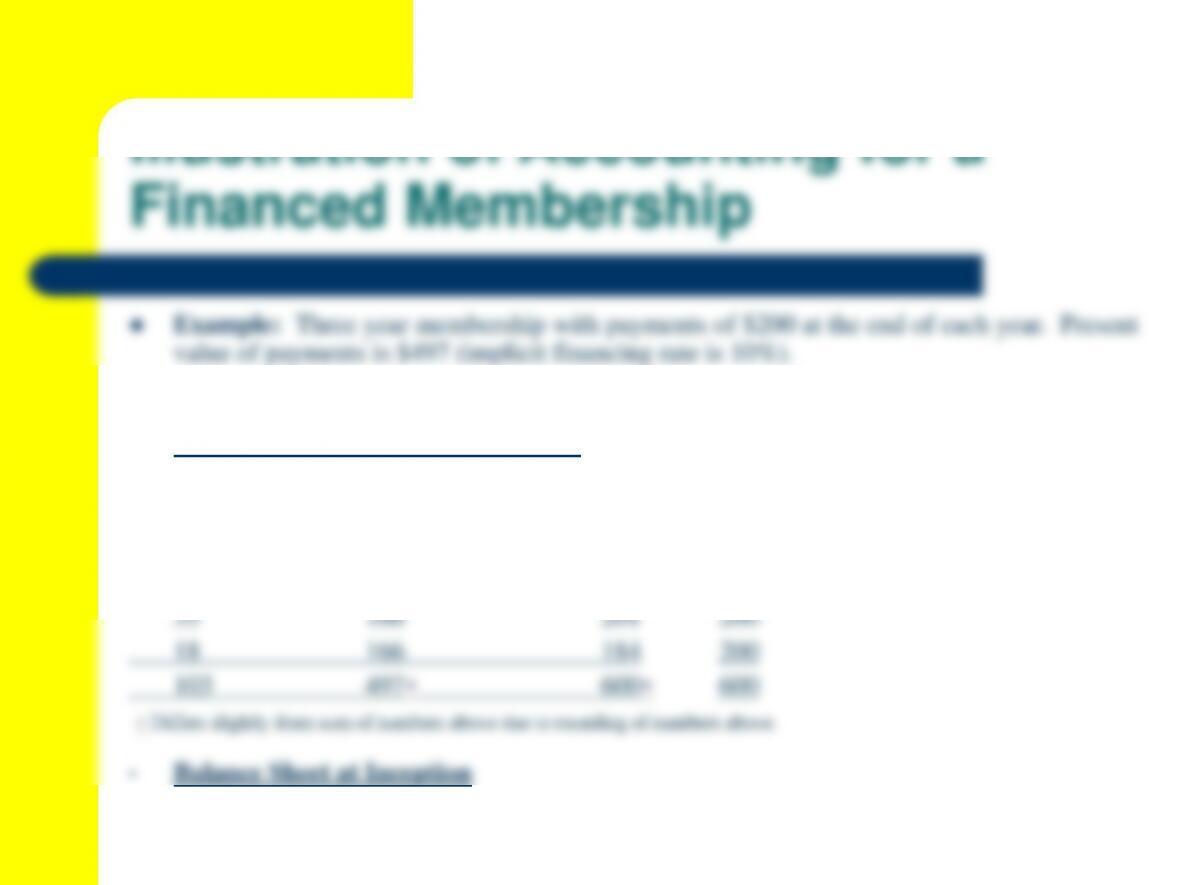

⚫Finance charges are accrued as earned using the

sum-of-the-months digits method, which approximates

BFT Deferral Basis Cash Basis

•Revenue Recognition Over Contract

Interest Membership Total Membership

Income Revenue Revenue

50 166 216 200

Accounts Receivable = 497 [no entry required]

Deferred Revenue = 497

GAAP Revenue Recognition Criteria

⚫Revenue cannot be recognized until:

⚫An exchange transaction has taken place

consistent with GAAP (assuming that they are

being correctly applied)