Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

12

FW3 = 3000(F/P,15%,2) + 15,000(F/P,15%,1)

= 3000(1.3225) + 15,000(1.1500)

= $21,218

Find i′ at which PW0 is equivalent to FW3

–10,757(F/P,i′,3) = 21,218

i’ = (21,218/10,757)1/3 -1

= 0.254 (25.4% per year)

(b) By MIRR with ib = 10% and ii = 30%

i’ = 31.7% per year

7.42 PW0 = -50,000 – 8000(P/F,12%,7)

7.43 (a) Descartes’ rule of signs: 2 sign changes; up to two i* values

(b) 0 = –65 + 30(P/F,i*,1) + 84(P/F,i*,2) – 10(P/F,i*,3) – 12(P/F,i*,4)

(c) Apply net-investment procedure steps because the investment rate ii = 15% is not

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

13

equal to i* rate of 28.6% per year.

Hand solution:

Step 1: F0 = -65 F0 < 0; use i″

Step 2: Set F4 = 0 and solve for i″ by trial and error.

Solve by quadratic equation, trial and error, or spreadsheet

Spreadsheet solution: Using the format and functions of Figure 7-13, i″ = 26.62%.

Before Goal Seek After Goal Seek Goal Seek template

Bonds

7.45 75 = 5000(b)/4

7.47 0 = –9250 + 50,000(P/F,i*,18)

7.48 (a) Dividend = 1000(0.05)/2 = $25 per 6 months

7.50 0 = –60,000 + 50,000(0.14)(P/A,i*,5) + 50,000(P/F,i*,5)

7.51 I = 10,000(0.08)/4 = $200 per quarter

7.52 I = 10,000(0.08)/4 = $200 per quarter

(a) 0 = –6000 + 200(P/A,i*,12) + 11,500(P/F,i*,12)

(b) Nominal i*/year = 8.13(4) = 32.5% per year

7.53 The utility would pay a penalty of $2,000,000 in return for saving 4% per year, payable

Spreadsheet Exercises

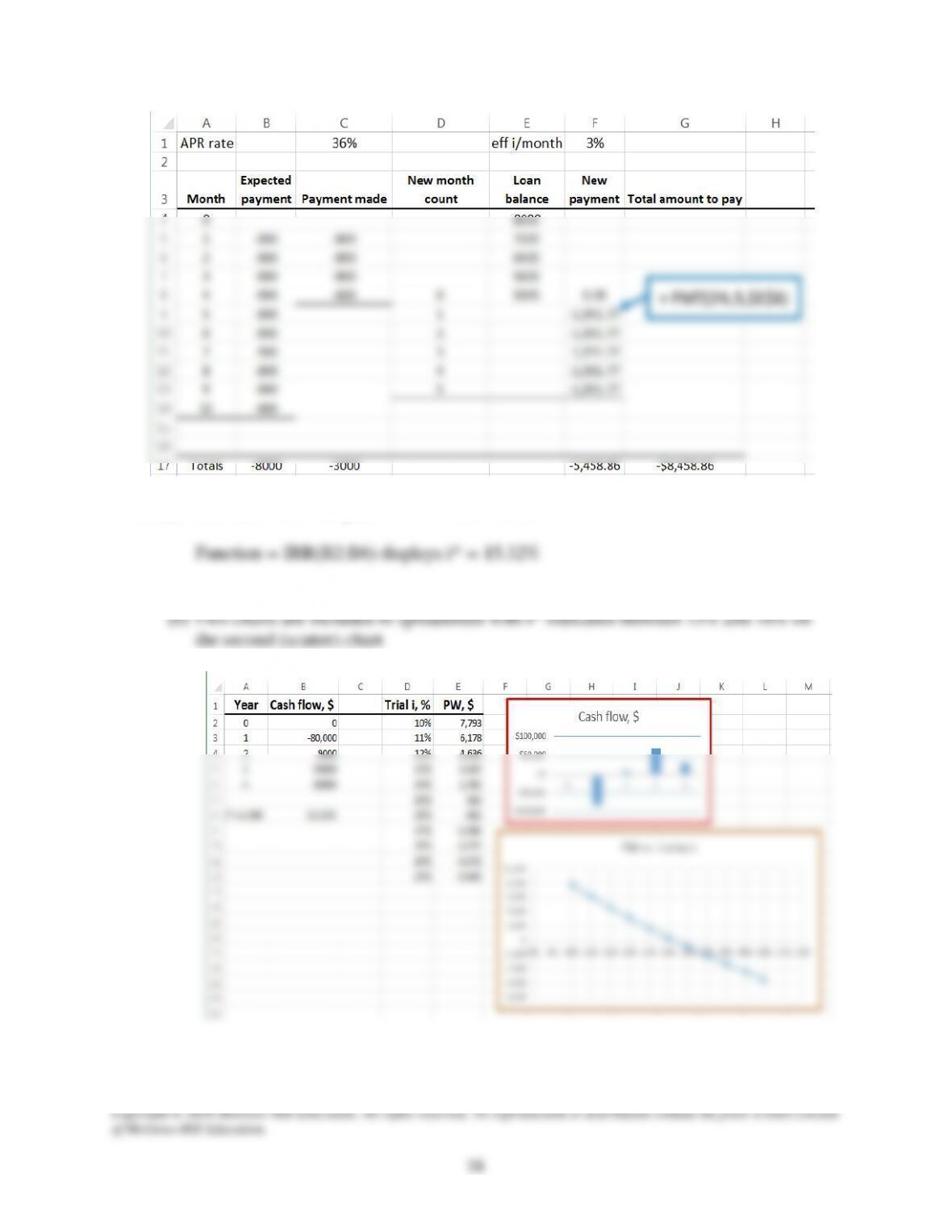

7.54 (a) Balance on loan after payment 4 = $5000

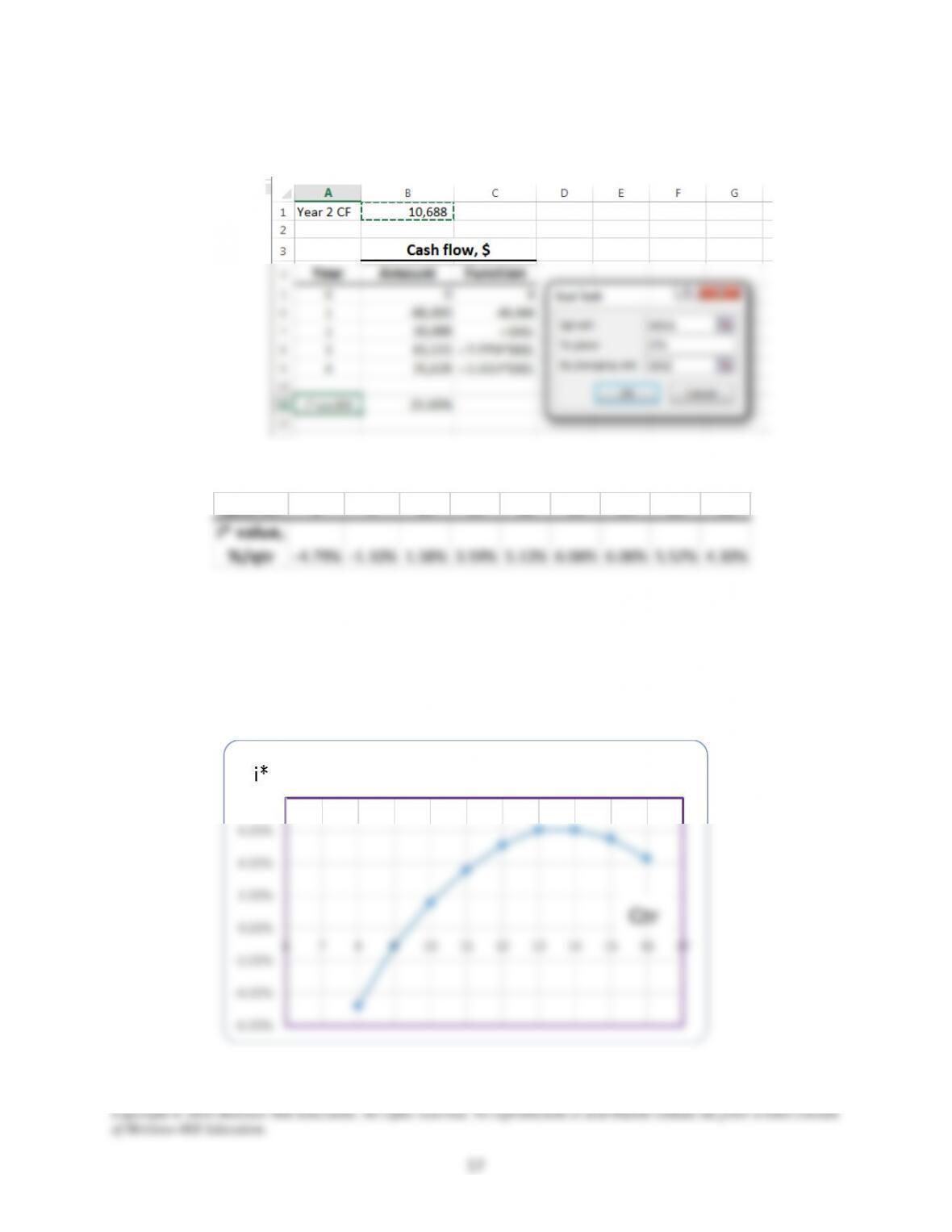

7.55 (a) Enter cash flows for years 0 to 4 in cells B2:B6

(c) Use Goal Seek tool to change $9000 estimate in year 1 to $10,688 with multiples shown

for years 3 and 4 estimates. Amounts needed are in cells B7 to B9.

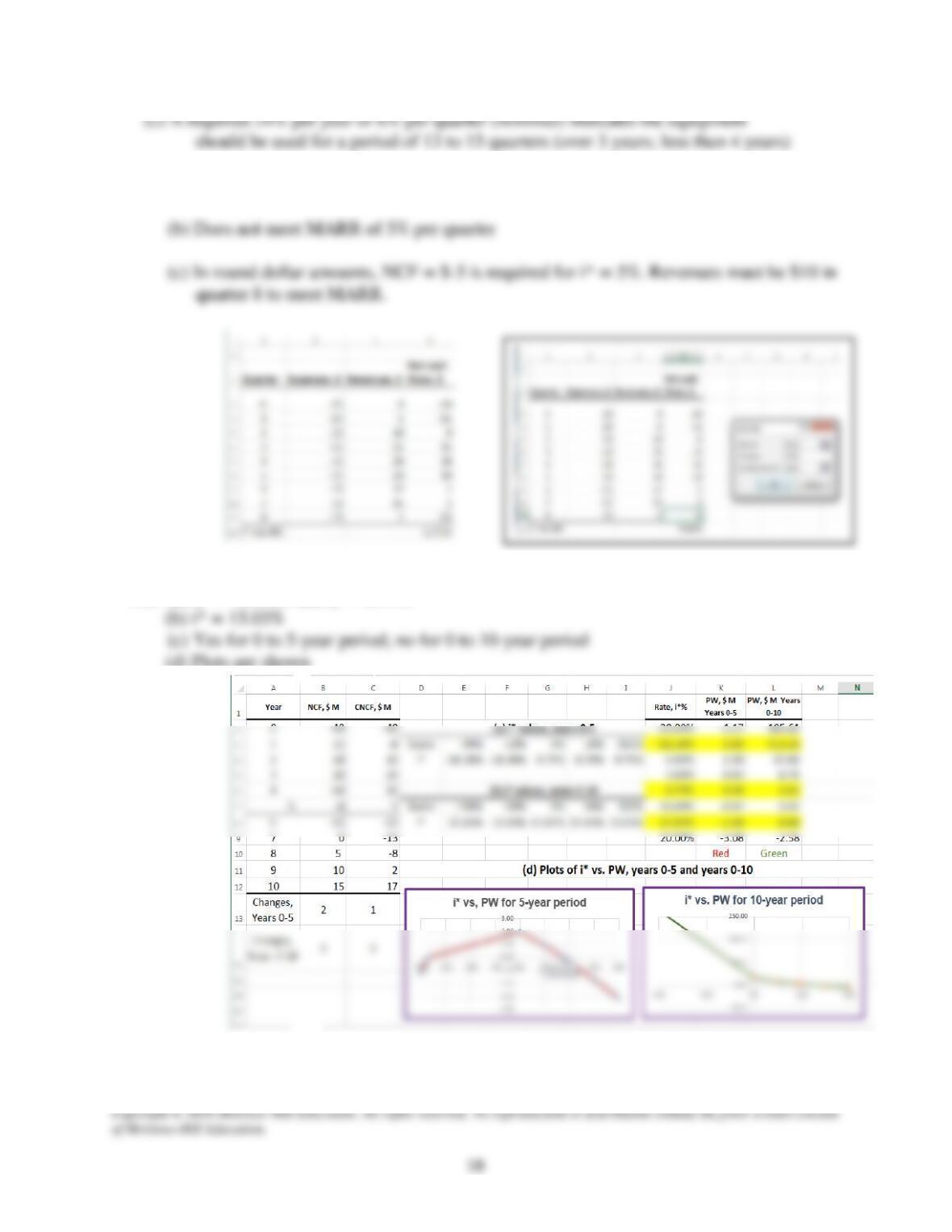

7.56 (a) Spreadsheet table not shown intentionally; i* per quarter series is:

(b) Plot of i* per quarter vs. quarters 8 through 16

Quarter 8 9 10 11 12 13 14 15 16

i* value,

%/qtr

–4.79% –1.10% 1.58% 3.59% 5.13% 6.06% 6.06% 5.52% 4.30%

-6.00%

-4.00%

-2.00%

0.00%

2.00%

4.00%

6.00%

8.00%

i*, % per quarter

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

18

(c) A required 24% per year or 6% per quarter (nominal) indicates the equipment

should be used for a period of 13 to 15 quarters (over 3 years; less than 4 years)

7.57 (a) i* = -2.71% per quarter (see spreadsheet)

7.58 (a) i1

* = -18.38% and i2

* = 8.79%

(d) Plots are shown

7.59 ROIC analysis results in i” = 11.26%, same as the IRR result. The MARR of 10% is being met

and the company is effectively using the funds invested in it.

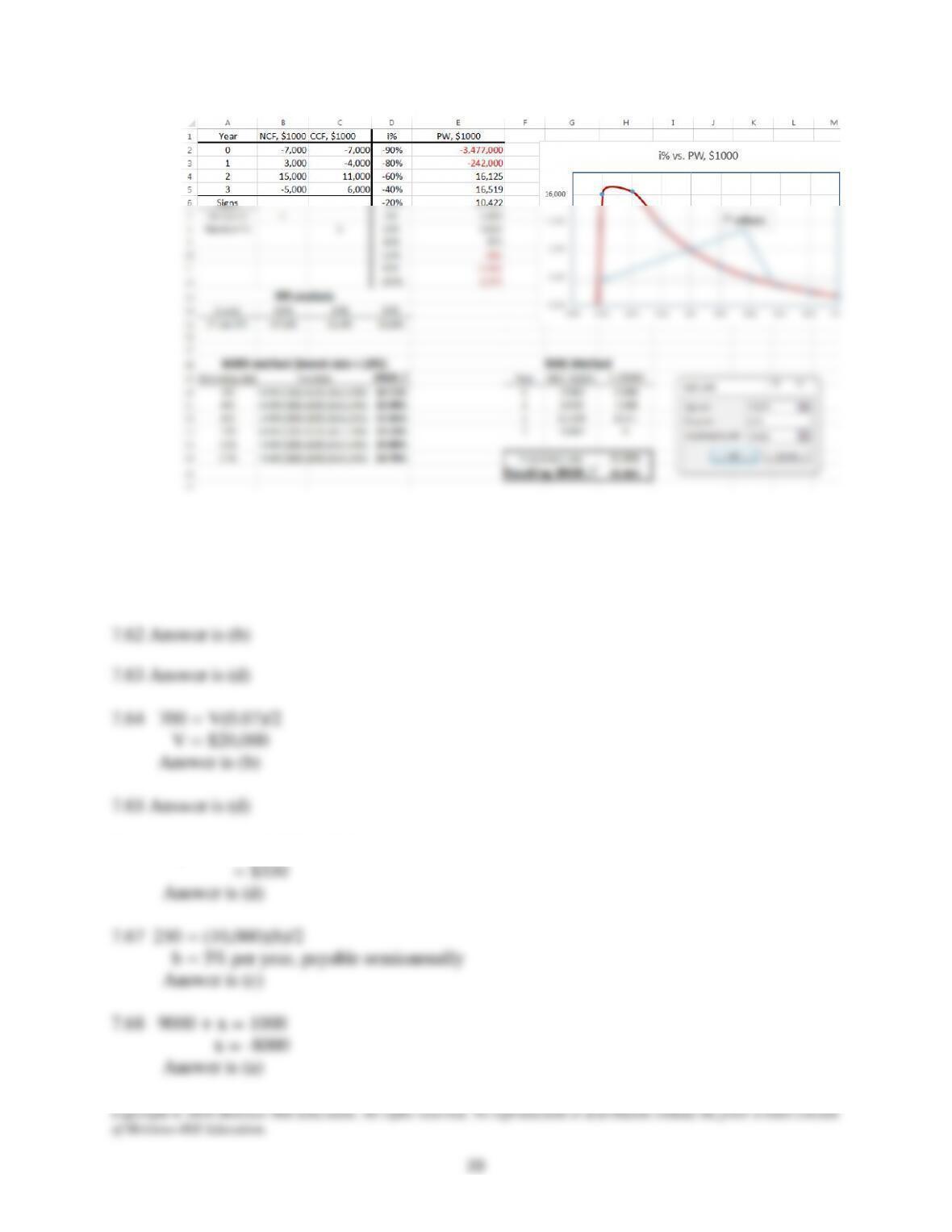

7.60 (a) Sign changes: Descartes: 2; up to two i* values

Norstrom’s: 1; one positive i*

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

20

Additional Problems and FE Exam Review Problems

7.61 Answer is (c)

7.66 I/quarter = 20,000(0.07)/4

7.69 0 = 1,000,000 – 20,000(P/A,i*,24) – 1,000,000(P/F,i*,24)

7.70 0 = –60,000 + 10,000(P/A,i*,10)

7.72 i* = 4500/50,000 = 0.09 (9% per year)

7.74 PW0 = -40,000 – 29,000(P/F,8%,2)

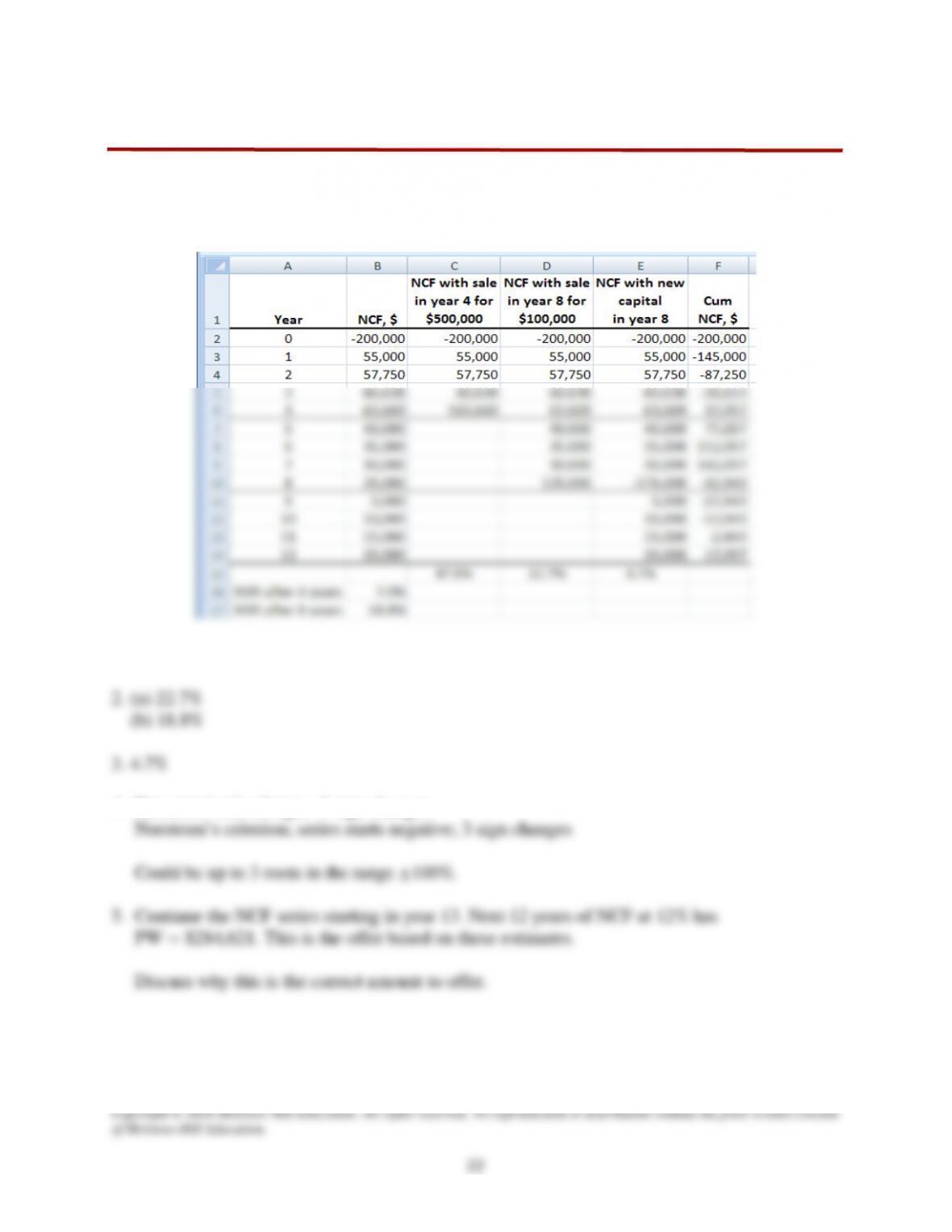

Solution to Case Study, Chapter 7

There is not always a definitive answer to case study exercises. Here are example responses

DEVELOPING AND SELLING AN INNOVATIVE IDEA

1. (a) 47.9%; (b) 7.0%

4. Descartes’ rule of signs: 3 sign changes