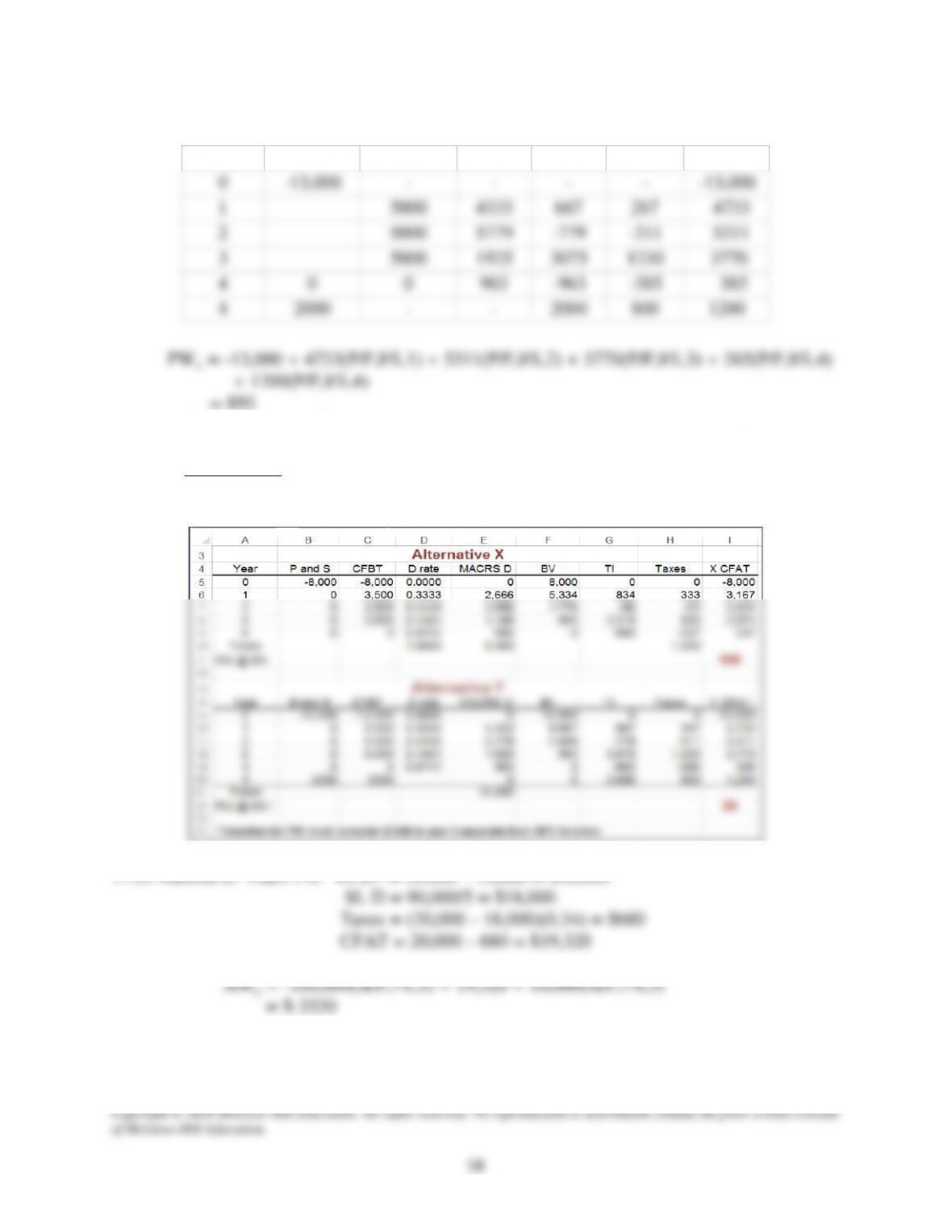

Alternative Y

-13,000

4733

1230

. Select alternative X

(b) Spreadsheet: Select X with the larger PW value. Note handling of $2000 salvage for Y

in year 4

Year

P and S

GI – OE

D

TI

Taxes

CFAT

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

19

Method H: Years 1-5: CFBT = 45,000 – 6,000 = $39,000

SL D = 130,000/5 = $26,000

Taxes = (39,000 – 26,000)(0.34) = $4420

CFAT = 39,000 – 4420 = $34,580

AWH = -150,000(A/P,7%,5) + 34,580 + 20,000(A/F,7%,5)

= $1474

Method H is selected; the same as with MACRS.

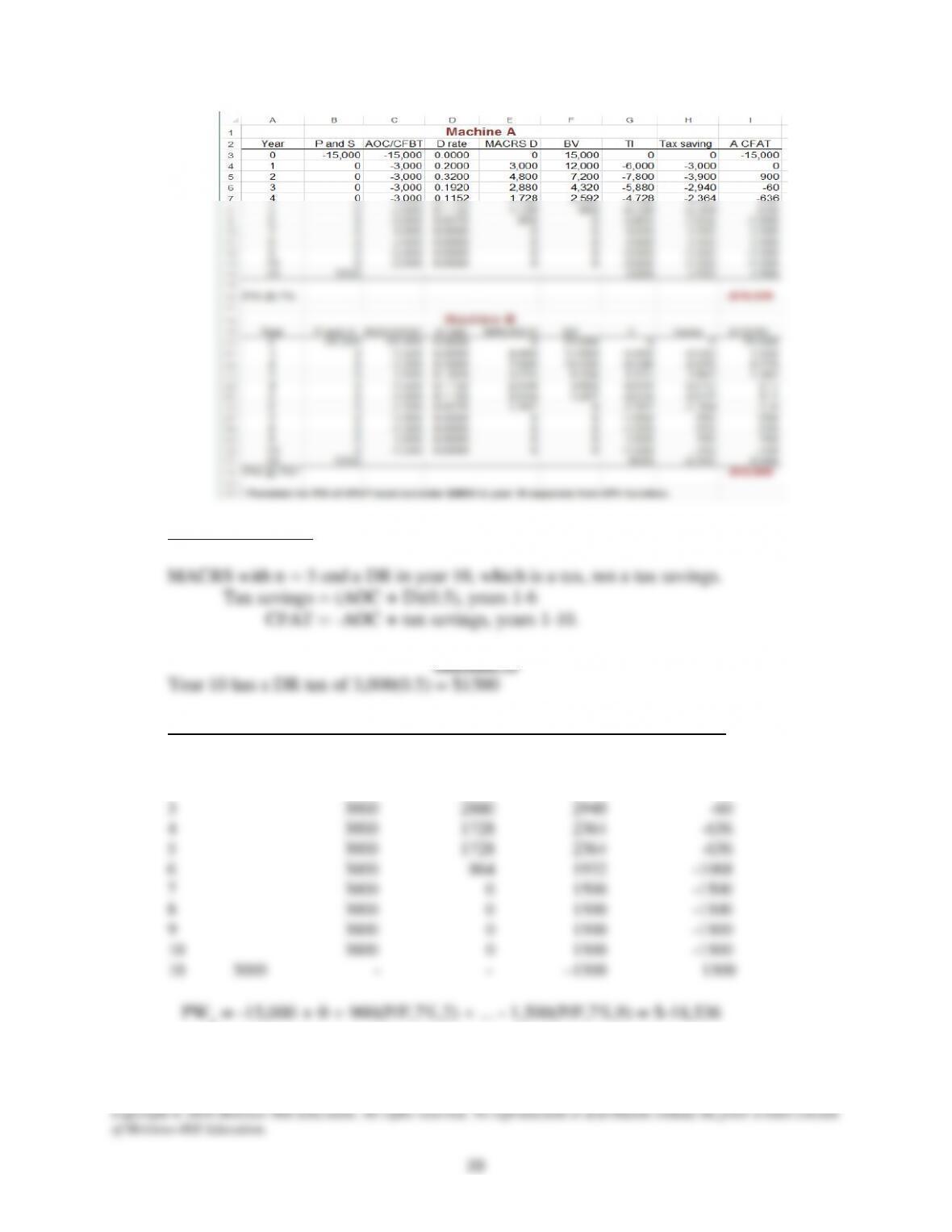

17.53 (a) Function for PWA: = -PV(14%,10,-3000,3000) – 15000 displays PWA = $-29,839

(b) All AOC estimates generate tax savings; GI estimates are equal.

Machine A

Machine B

(c) Again, select machine B. All methods give the same conclusion

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

20

By hand, if needed:

Machine A

Year P or S AOC Depr. Tax savings CFAT

0 $-15,000 – – – $-15,000

1 $3000 $3000 $3000 0

2 3000 4800 3900 900

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

21

Machine B

Year 10 has a DR tax of 5,000(0.5) = $2,500

Year P or S AOC Depr Tax savings CFAT

0 $–22,000 – – – $–22,000

1 $1500 $4400 $2950 1450

2 1500 7040 4270 2770

3 1500 4224 2862 1362

After–Tax Replacement

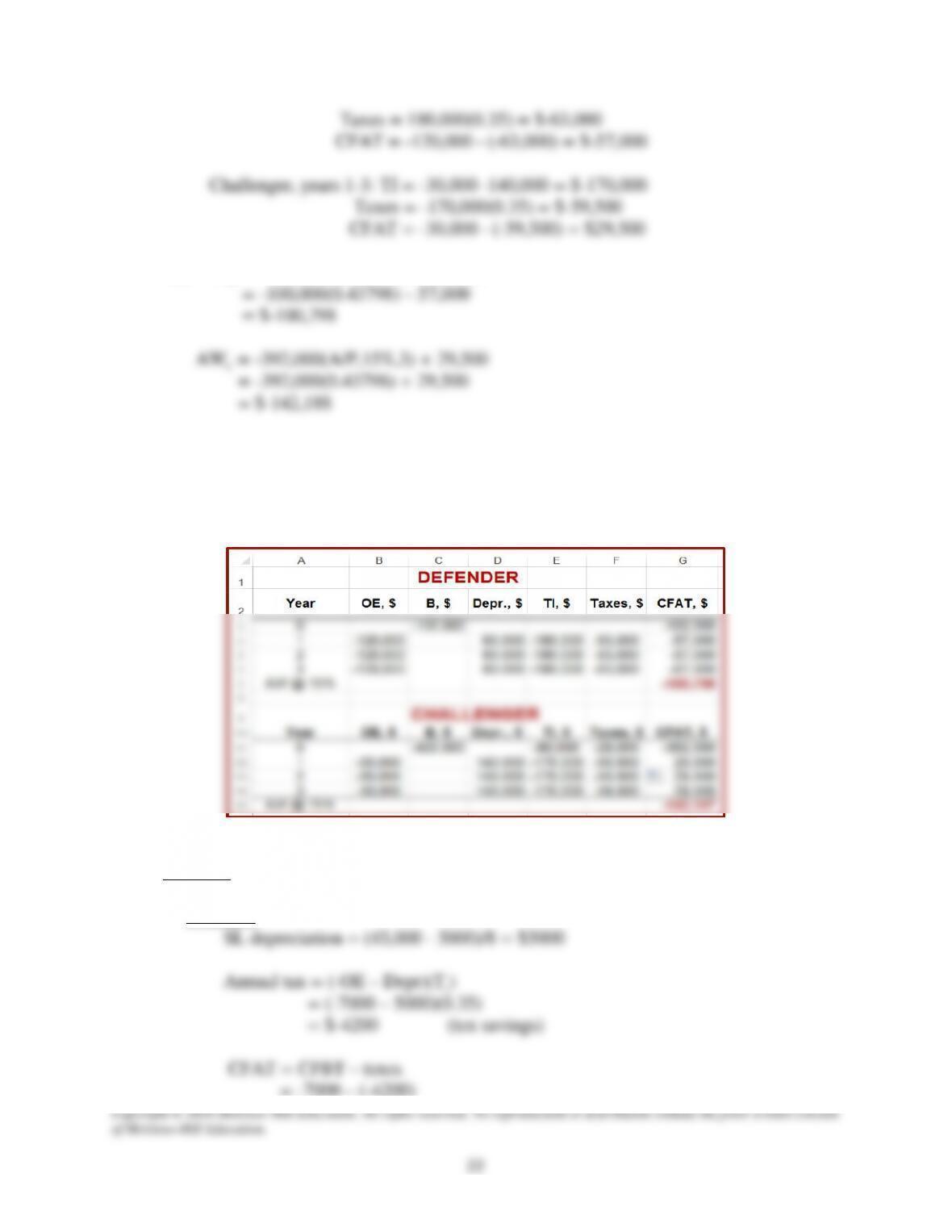

17.54 (a) For a capital loss, it is the difference between sales price and the asset’s book value.

(b) The AW of the challenger is affected in year 0 by the capital gains tax. If it is a capital

17.56 (a) Defender: CL = BV2 – sales price = [300,000 – 2(60,000)] – 100,000

This represents a tax savings for the challenger in year 0.

(b) Defender, years 1-3: TI = -120,000 – 60,000 = $-180,000

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

22

Taxes = 180,000(0.35) = $-63,000

CFAT = -120,000 – (-63,000) = $-57,000

Challenger, years 1-3: TI = -30,000 –140,000 = $-170,000

Taxes = -170,000(0.35) = $-59,500

CFAT = -30,000 – (-59,500) = $29,500

(c) AWD = -100,000(A/P,15%,3) – 57,000

Conclusion: Keep the defender

(d) Spreadsheet shows CFAT and AW values; keep the defender.

17.57 Find after-tax PW of costs over 4-year study period. DR is involved on the defender trade.

By hand:

Defender:

= -7000 – (-4200)

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

23

= $-2800

PWD = -35,000 + 5000(P/F,12%,4) – 2800(P/A,12%,4)

= –35,000 + 5000(0.6355) – 2800(3.0373)

= $-40,327

Challenger:

0

-25,750

-25,750

1

-8000

0.3333

8,000

-16,000

-2,400

2

-8000

0.4445

-6,534

3

-8000

0.1481

3,554

-11,554

-4,044

-3,956

Conclusion: Select the challenger with a lower PW of cost

Spreadsheet: Same decision; select the challenger

Year

OE

P and S

Rate

Depr.

TI

Taxes

CFAT

4

-8000

0

0.0741

1,778

-9,778

-3,422

-4,578

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

24

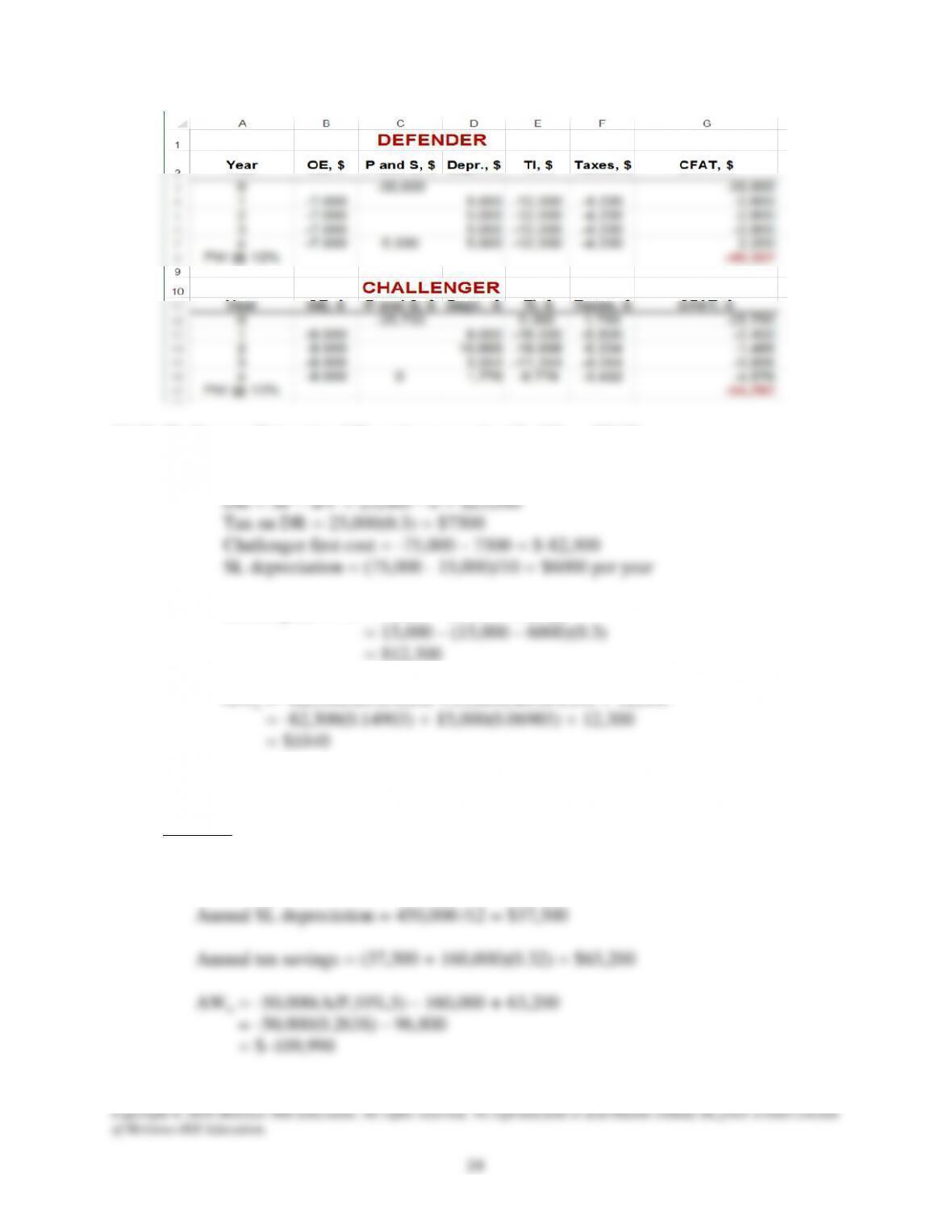

17.58 Challenger: Determine AWC and compare it with AWD = $2100.

Defender has DR on trade since BV = 0 now.

CFAT, years 1-10 = CFBT – (CFBT – D)( Te )

AWC = -82,500(A/P,8%,10) +15,000(A/F,8%,10) + 12,300

Retain the defender; it has a larger AW value.

17.59 Defender

Original life estimate was 12 years.

Challenger

CL from sale of D = BV7 – Market value

Tax savings from CL, year 0 = 137,500(0.32)

Challenger DR when sold in year 8 = $0

Select the defender. Decision was incorrect since D has a lower AW value of costs.

17.60 (a) By hand: Lives are set at 5 (remaining) for the defender and 8 years for the challenger.

Defender

Challenger

DR from sale of D = Market value – BV5

Challenger annual depreciation = 15,000 – 3000 = $1500

8

AWC = –15,000(A/P,6%,8) + 3000(A/F,6%,8) – 1500 + 180

Select the challenger

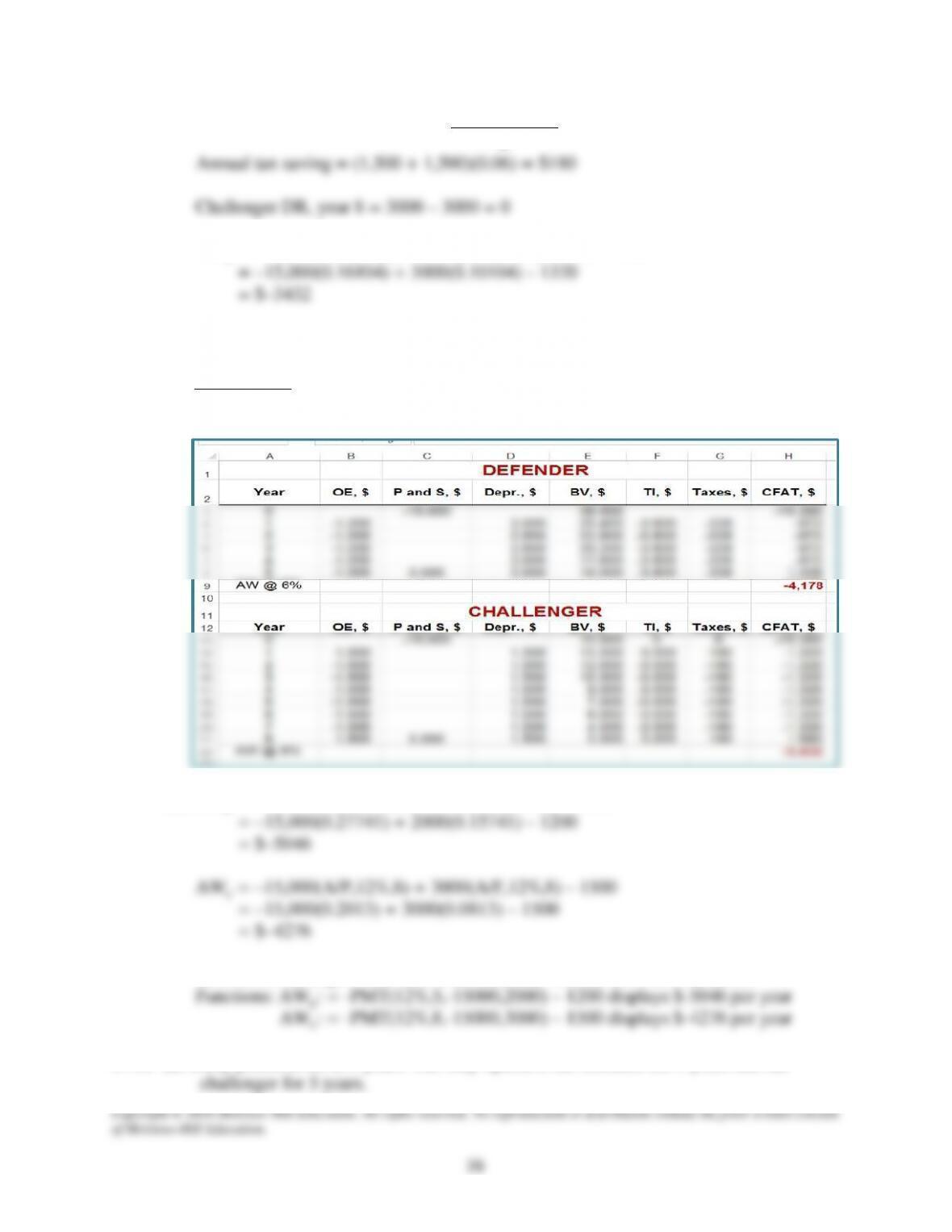

(b) Spreadsheet: With n = 5, AWD = $-4178; with n = 8, AWC = $-3432.

Select the challenger

(c) AWD = –15,000(A/P,12%,5) + 2000(A/F,12%,5) – 1200

Select the challenger. The before–tax and after-tax decisions are the same.

17.61 (a) Study period is set at 5 years. The only option is the defender for 5 years and the

Defender

Upgrade SL depreciation = $3000 year (years 1–3 only)

Actual cost, years 4-5: = 6000 – 2400 = $3600

AWD = -24,000(A/P,12%,5) – 2400 – 1200(F/A,12%,2)(A/F,12%,5)

Challenger

DR on defender = $15,000

Retain the defender since the AW of cost is smaller.

(b) AWC will become less costly, but the revenue from the challenger’s sale between

$2000 to $4000 will be reduced by the 40% tax on DR in year 5.

Economic Value Added

17.62 (a) The EVA shows the monetary worth added to a corporation by an alternative.

17.63 BV1 = 300,000 – 300,000(0.20) = $240,000

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

28

EVA = NOPAT – MARR(BV1)

= 70,000 – (0.15)(240,000)

= $34,000

17.64 Find BVt-1 and solve for NOPAT and TI, year 2, and solve for OE

Year 2 results:

EVA = 28,000 = NOPAT – (0.14)(366,685)

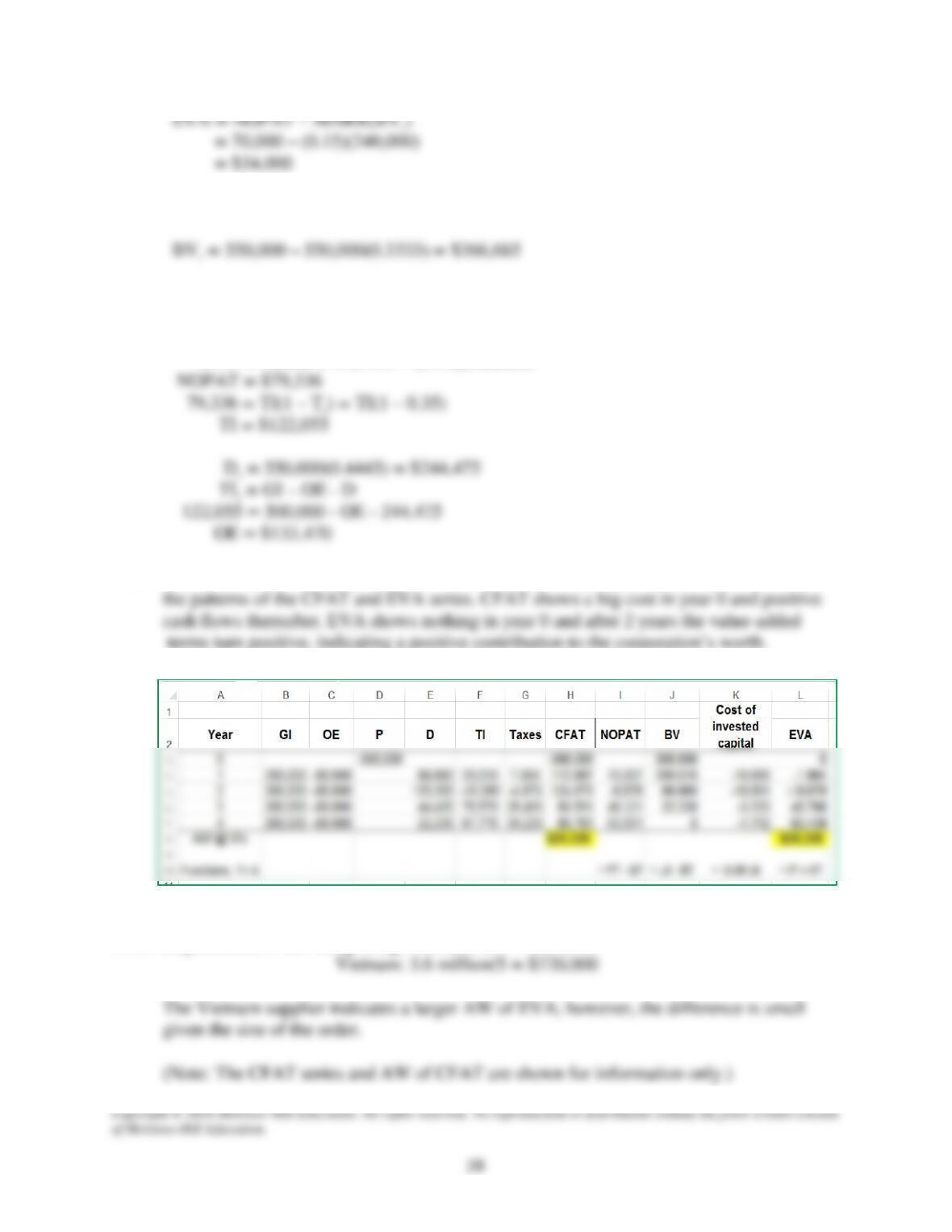

17.65 The spreadsheet verifies that the AW values are the same. Note the difference in

terms turn positive, indicating a positive contribution to the corporation’s worth.

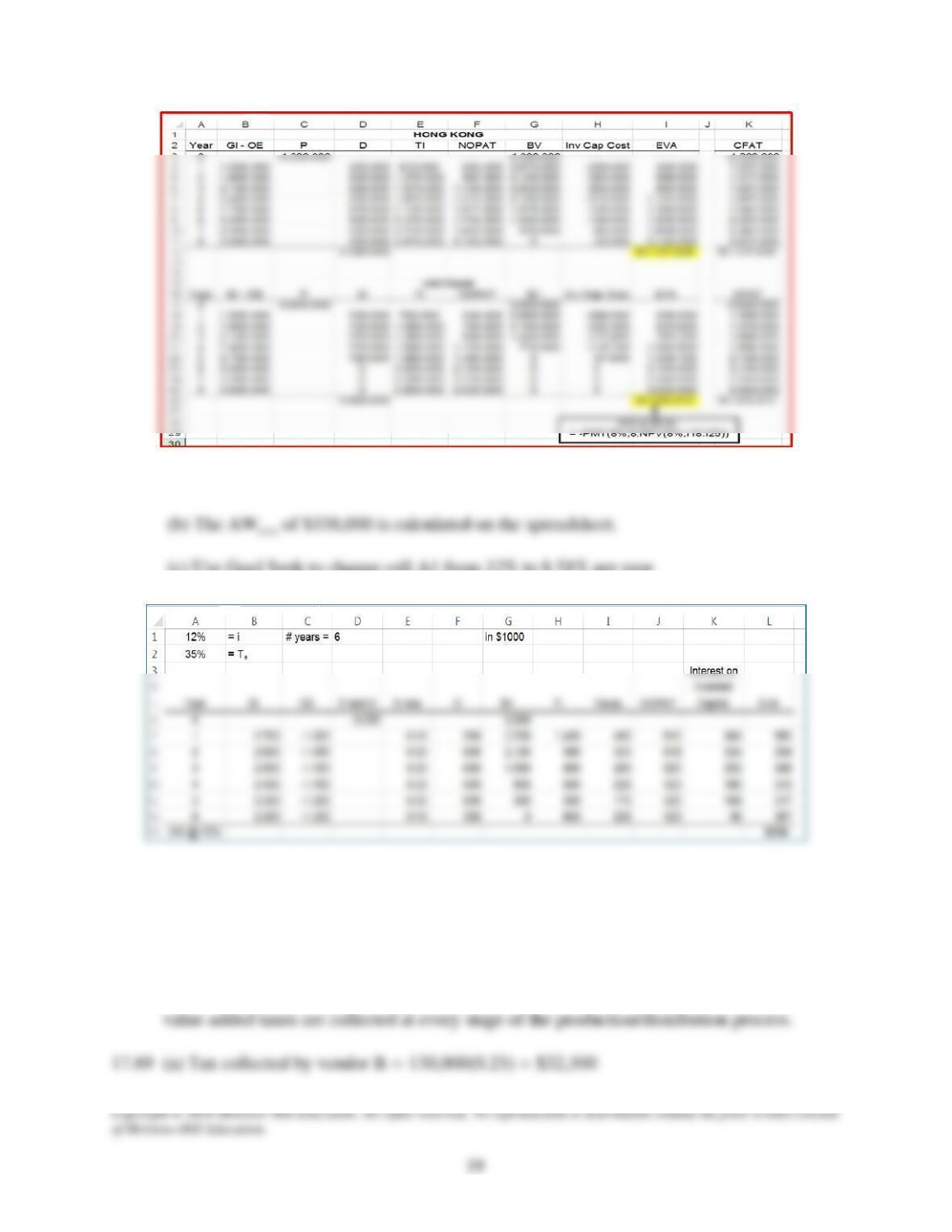

17.66 Depreciation is SL: Hong Kong: 4.2 million/8 = $525,000

17.67 (a) Column L shows the EVA each year. Use Eq. [17.23} to calculate EVA.

(c) Use Goal Seek to change cell A1 from 12% to 8.51% per year

Value–Added Tax

17.68 A sales tax is collected when the goods or services are bought by the end–user, while

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

30

(b) Tax sent by vendor B = amount collected – amount paid to vendor A

= 32,500 – 60,000(0.25) = $17,500

(c) Amount collected by Treasury = 250,000(0.25) = $62,500

17.70 VAT by supplier C = 620,000(0.125) = $77,500

17.74 Taxes sent = amount collected – amount paid

17.75 VAT collected = sent by suppliers + sent by Ajinkya

ADDITIONAL PROBLEMS AND FE EXAM PRACTICE PROBLEMS

17.76 Before–tax ROR = After–tax ROR/(1– Te)

17.77 Te = 0.07 + (1 – 0.07)(0.36) = 0.4048 (40.5%)

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

31

17.81 Answer is (a)

17.82 Answer is (d)

17.83 Tax difference = (160,000,000 – 120,000,000)(0.50) = $20,000,000

17.85 The sale results in DR = $16,000, which is an increase in TI.

17.87 CFAT = GI – OE – TI(Te)

26,000 = 30,000 – TI(0.40)

17.88 BV5 = 100,000(0.0576) = $5760

Solution to Case Study, Chapter 17

There is not always a definitive answer to case study exercises. Here are example responses.

AFTER–TAX ANALYSIS FOR BUSINESS EXPANSION

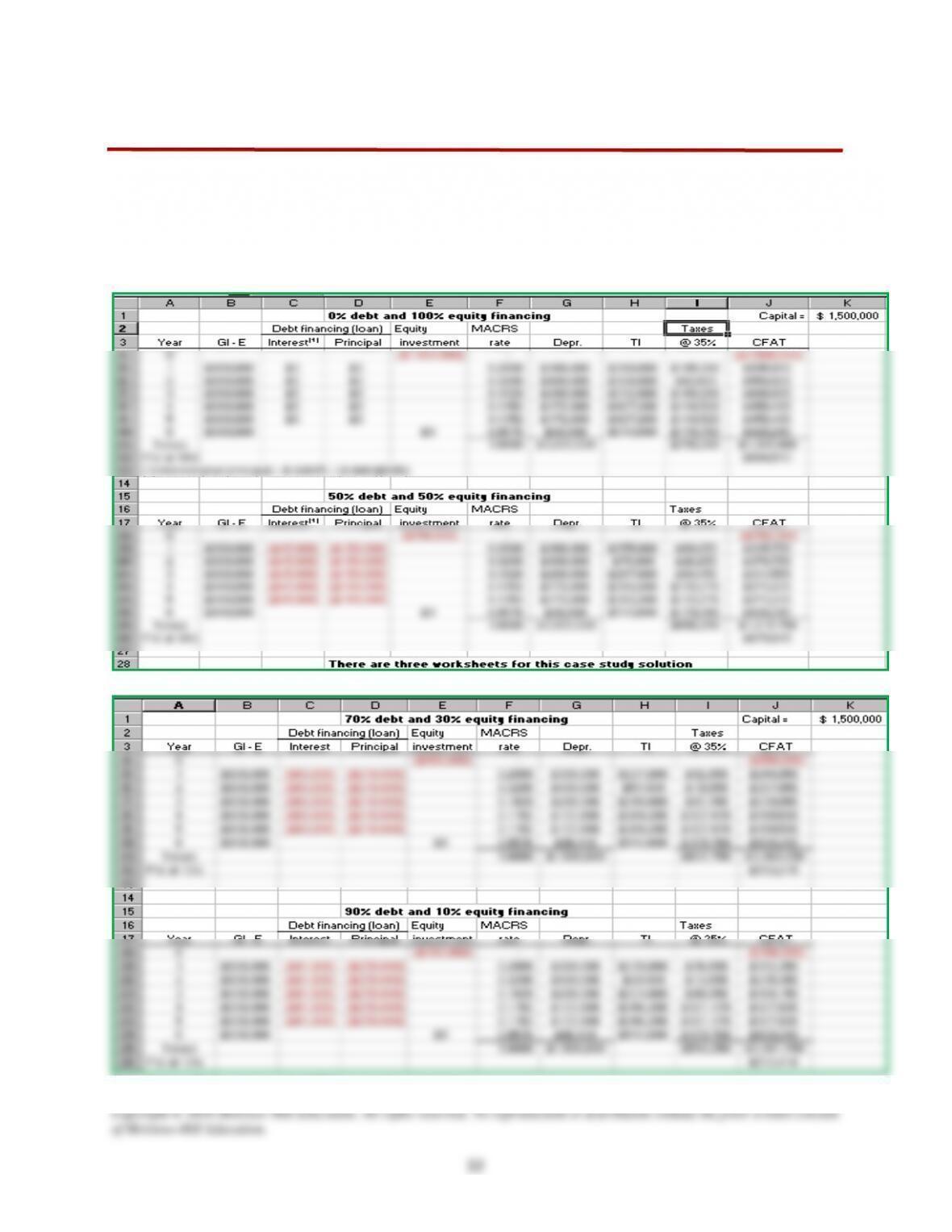

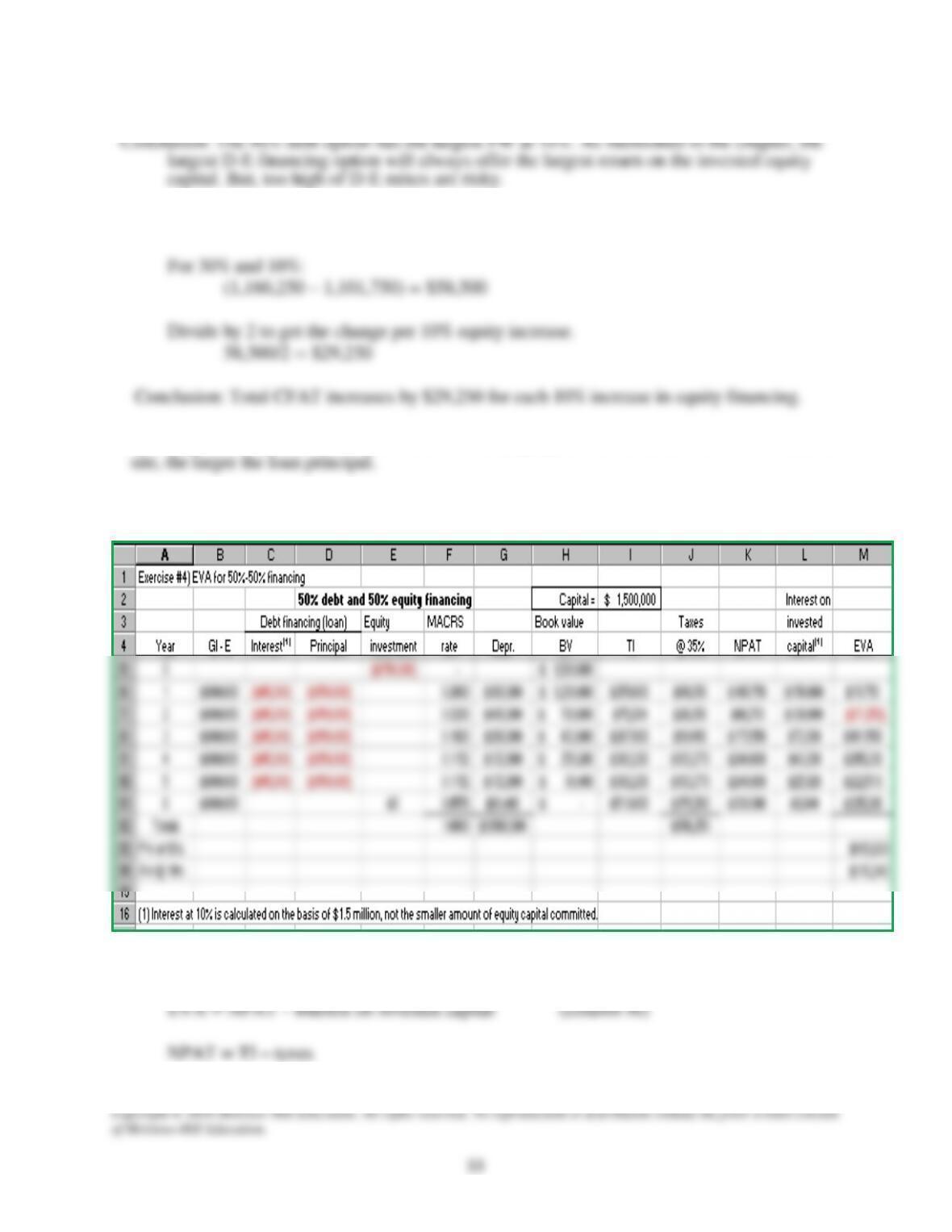

1. The next two spreadsheets perform an analysis of the four D-E mix scenarios

Note: Column B, E used instead of OE for operating expenses.

2. Subtract 2 different equity CFAT totals.

3. This happens because as less of Pro–Fence’s own (equity) funds are committed to the Victoria

4. Use the EVA series as an estimate of contribution to Pro-Fence’s bottom line through time.

Equations used to determine the EVA use NOPAT (or NPAT) and interest on invested capital.

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

34

(Interest on invested capital)t = i(BV in the previous year)

= 0.10(BVt–1)

Note: BV on the entire $1.5 million in depreciable assets is used to determine the interest on