Engineering Economy, 8th edition

Leland Blank and Anthony Tarquin

Chapter 17

After-Tax Economic Analysis

Terminology and Basic Tax Computations

17.1 NOI = Net Operating Income; GI = Gross Income; Te = Effective Tax Rate: NOPAT = Net

17.2 (a) From Table 17.1, marginal tax rate = 39%

(b) Taxes = 0.15(50,000) + 0.25(75,000 – 50,000) + 0.34(100,000 – 75,000) +

17.3 (a) Net operating profit after taxes; (b) Taxable income; (c) Depreciation;

17.4 (a) In $1 million units,

(b) EBIT = NOI

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

2

72,000 = 22,250 + 0.39(TI – 100,000)

0.39TI = 88,750

TI = $227,564

(b) Average tax rate = T = 72,000/227,564 = 0.316 (31.6%)

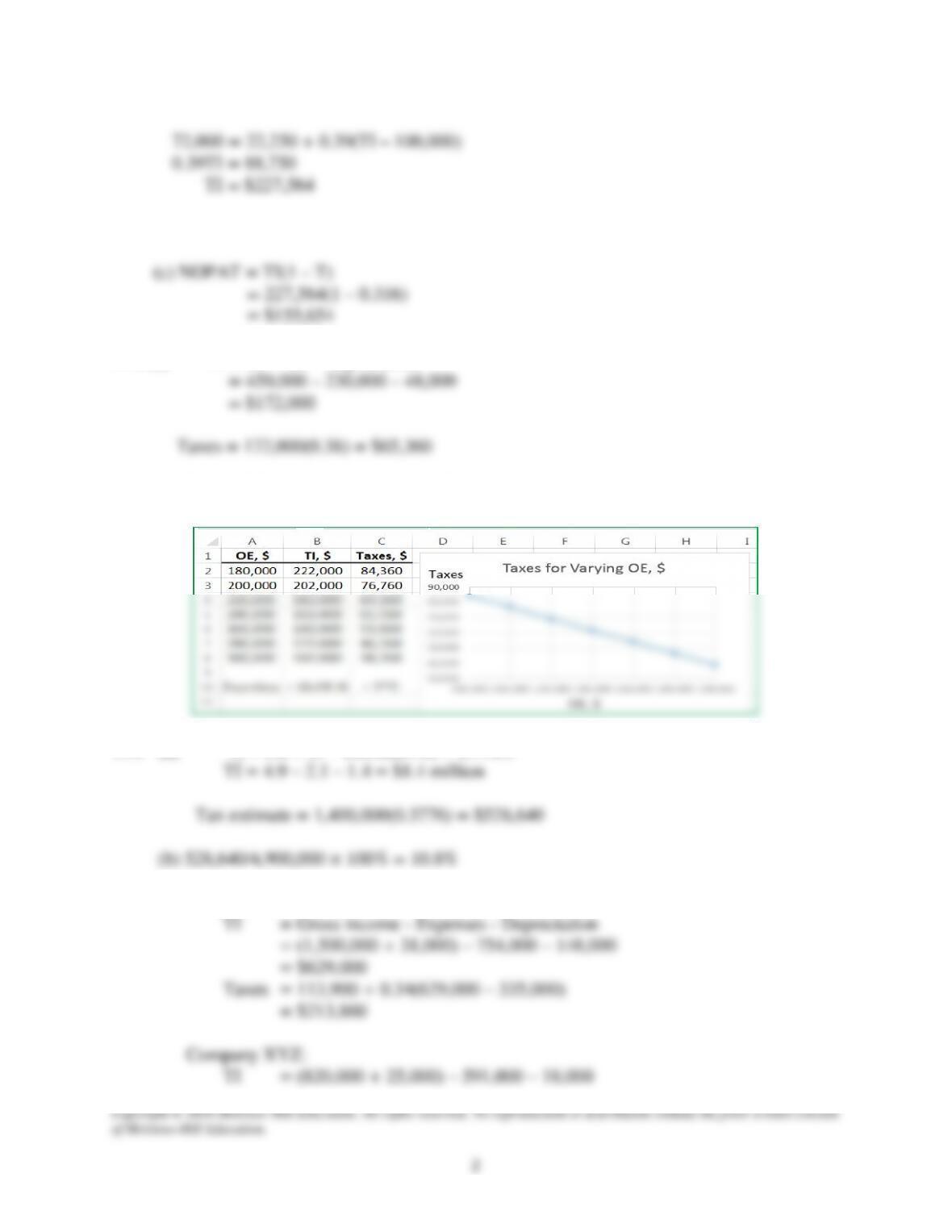

17.8 (a) TI = GI – OE – depreciation

(b) Use the TI relation with varying OE amounts to plot taxes. It is linear.

17.9 (a) Te = 9.8 + (1 – 0.098)(31%) = 37.76%

17.10 (a) Company ABC:

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

3

= $236,000

Taxes = 22,250 + 0.39(236,000 – 100,000)

= $75,290

(b) ABC: (213,860/1,500,000)*100% = 14.26%

(c) ABC:

Taxes = (TI)(Te) = 629,000(0.34) = $213,860

XYZ:

17.11 (a) Te = 0.076 + (1 – 0.076)(0.34) = 0.3902

(b) NOPAT = TI(1–Te) = 2,400,000(0.6098) = $1,463,520

17.12 (a) Federal taxes = 13,750 + 0.34(5000) = $15,450 (using Table 17-1 rates)

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

4

Federal: 80,000[0.1931(1 – 0.06)] = 80,000(0.1815)

= $14,520

17.13 (a) Te = 0.06 + (1 – 0.06)(0.23)

(c) Since Te = 22% is lower than the current federal rate of 23%, no provincial tax could

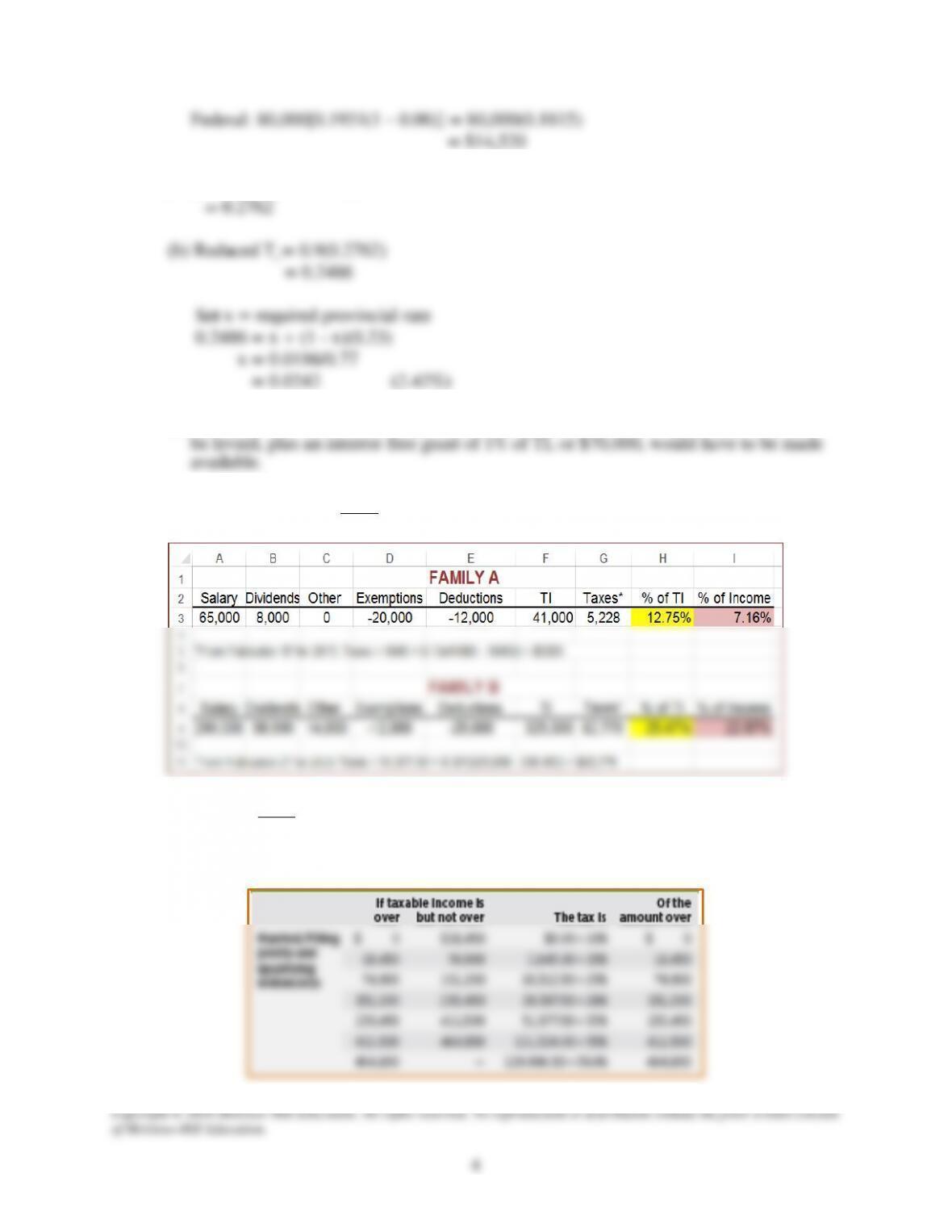

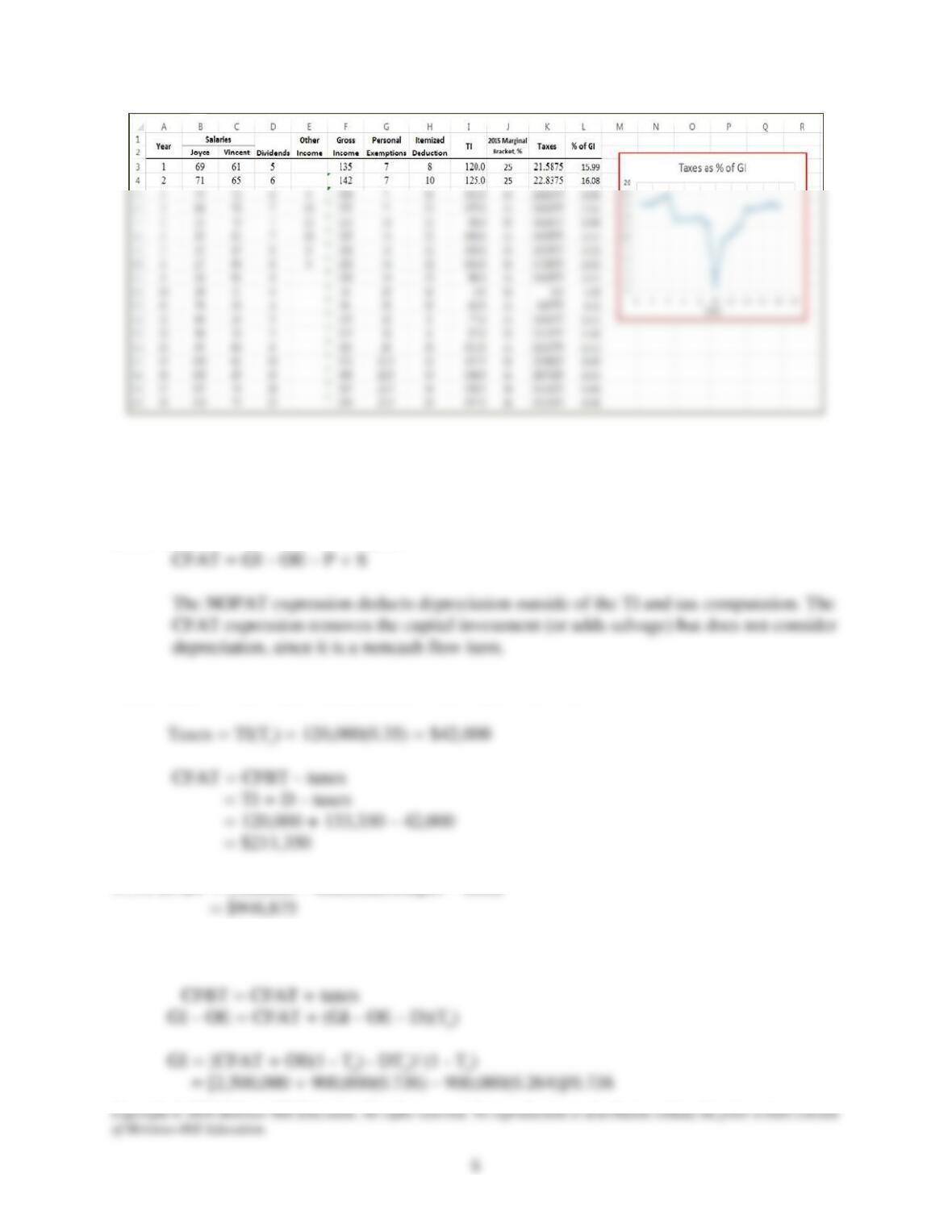

17.14 IRS Publication 17 for 2015 is used for this solution.

17.15 Tax rates for 2015 from IRS Publication 17 are below. Your tax amounts and plot will

vary when the current tax rates are applied. The percentage of GI spent on taxes has varied

widely as shown in the plot.

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

5

CFBT and CFAT

17.16 CFBT does not include life of asset, depreciation, and tax rate

17.17 NOPAT = GI – OE – D – Taxes

17.18 Use TI = GI – OE – D and CFBT = GI – OE = TI + D

17.19 CFBT = [750,000 – 400,000(0.36)]/(1 – 0.36)

17.20 Solve for GI

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

6

= $3,973,913

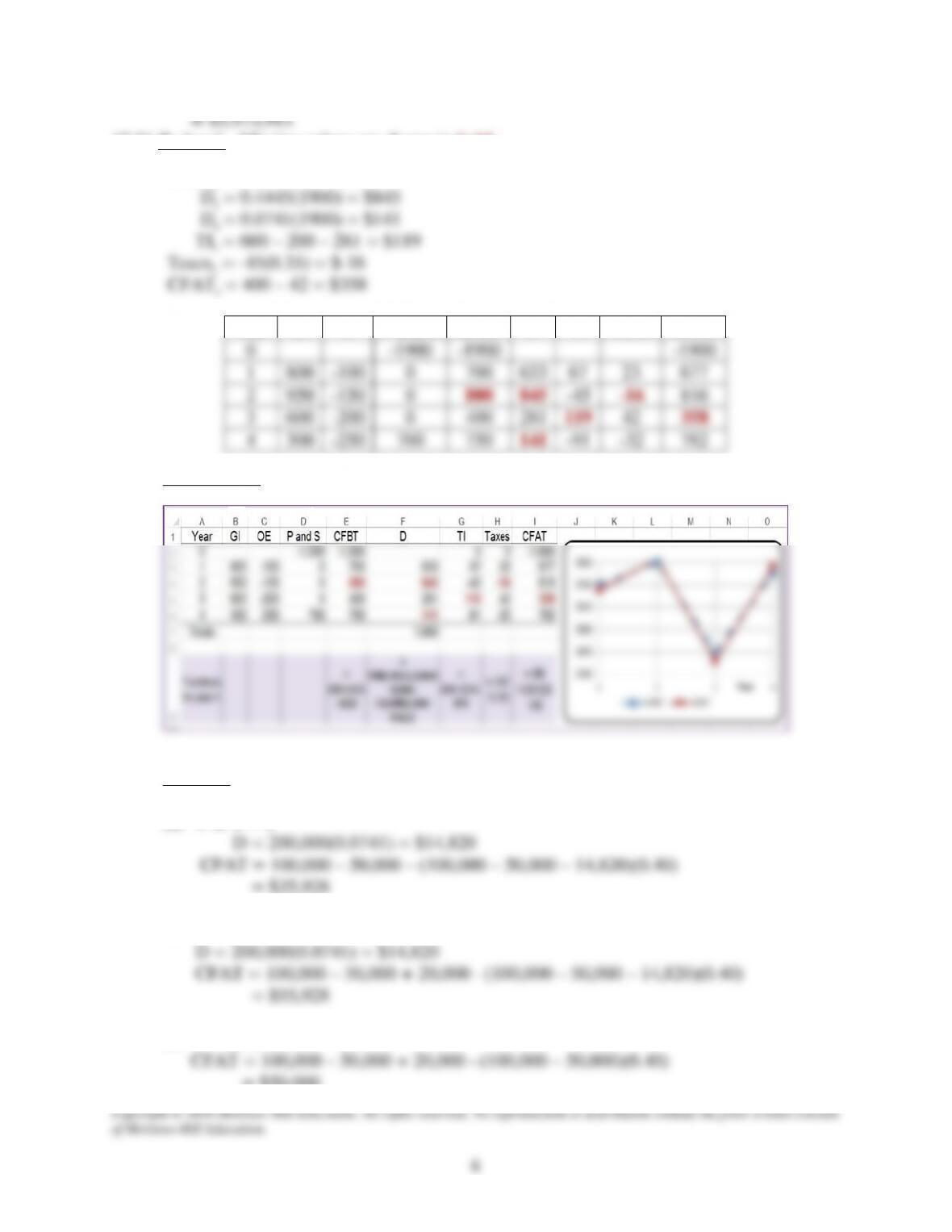

17.21 By hand: Missing values are shown in bold.

CFBT2 = 950 – 150 = $800

-1900

-200

281

300

-250

Spreadsheet: Missing values are shown in bold. Functions for year 4 are detailed.

17.22 By hand: CFAT = GI – OE – P + S – (GI – OE –D)Te

(a) P & S = 0

(b) S = $20,000

(c) S = $20,000 D = 0

= $50,000

Year

GI

E

P and S

CFBT

D

TI

Taxes

CFAT

Spreadsheet: MACRS d4 = 0.0741 SL d4 = 0

Same answers as above using Table 17–2 template

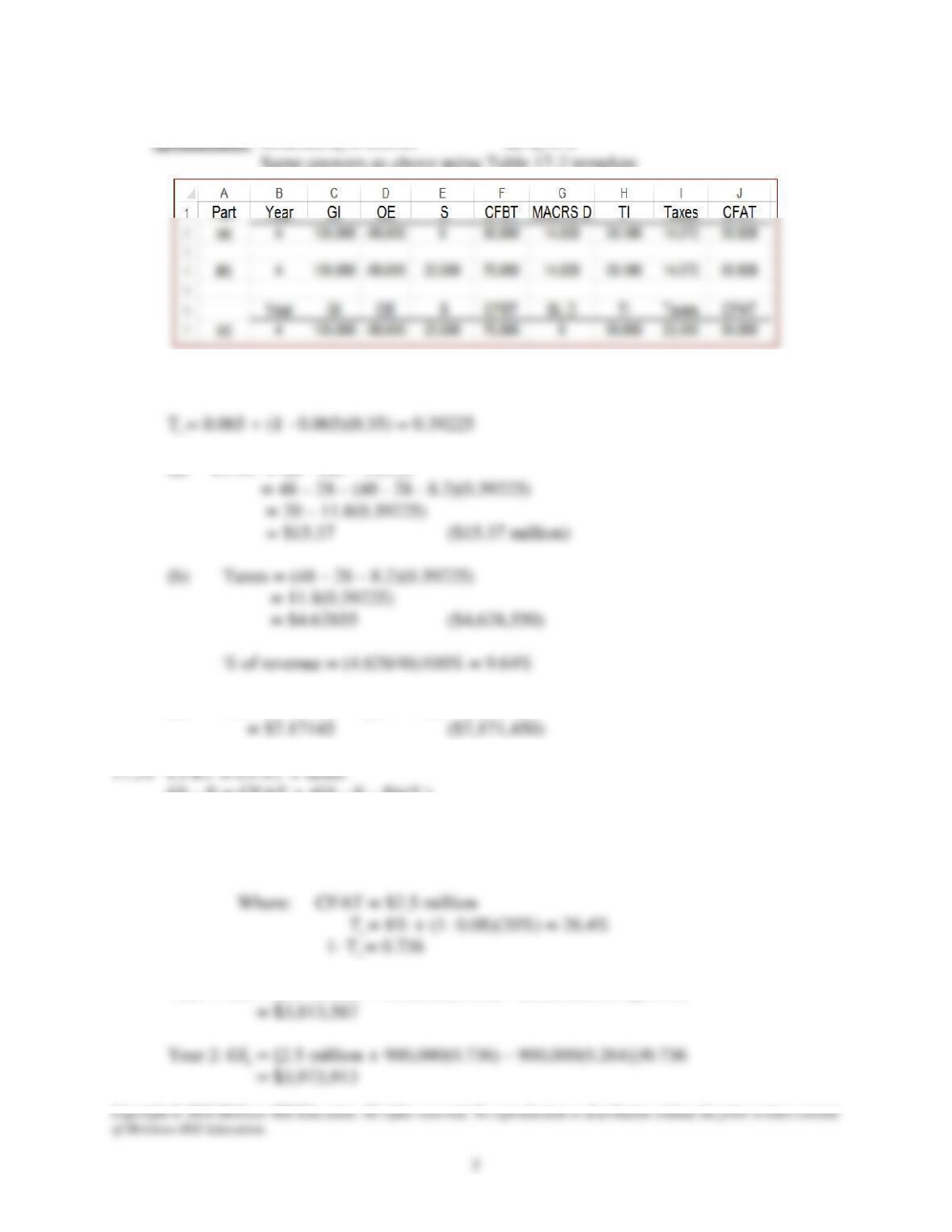

17.23 All monetary units are in $1 million

(a) CFAT = GI – OE – TI(Te )

(c) NOPAT = TI(1 – Te ) = 11.8(1 – 0.39225)

GI – E = CFAT + (GI – E – D)(Te)

Solve for GI to obtain a general relation for each year t:

GIt = [CFAT + E(1– Te) – DTe]/ (1– Te)

Year 1: GI1 = [2.5 million + 650,000(0.736) – 650,000(0.264)]/0.736

Year 3: GI3 = [2.5 million + 1,150,000(0.736) – 1,150,000(0.264)]/0.736

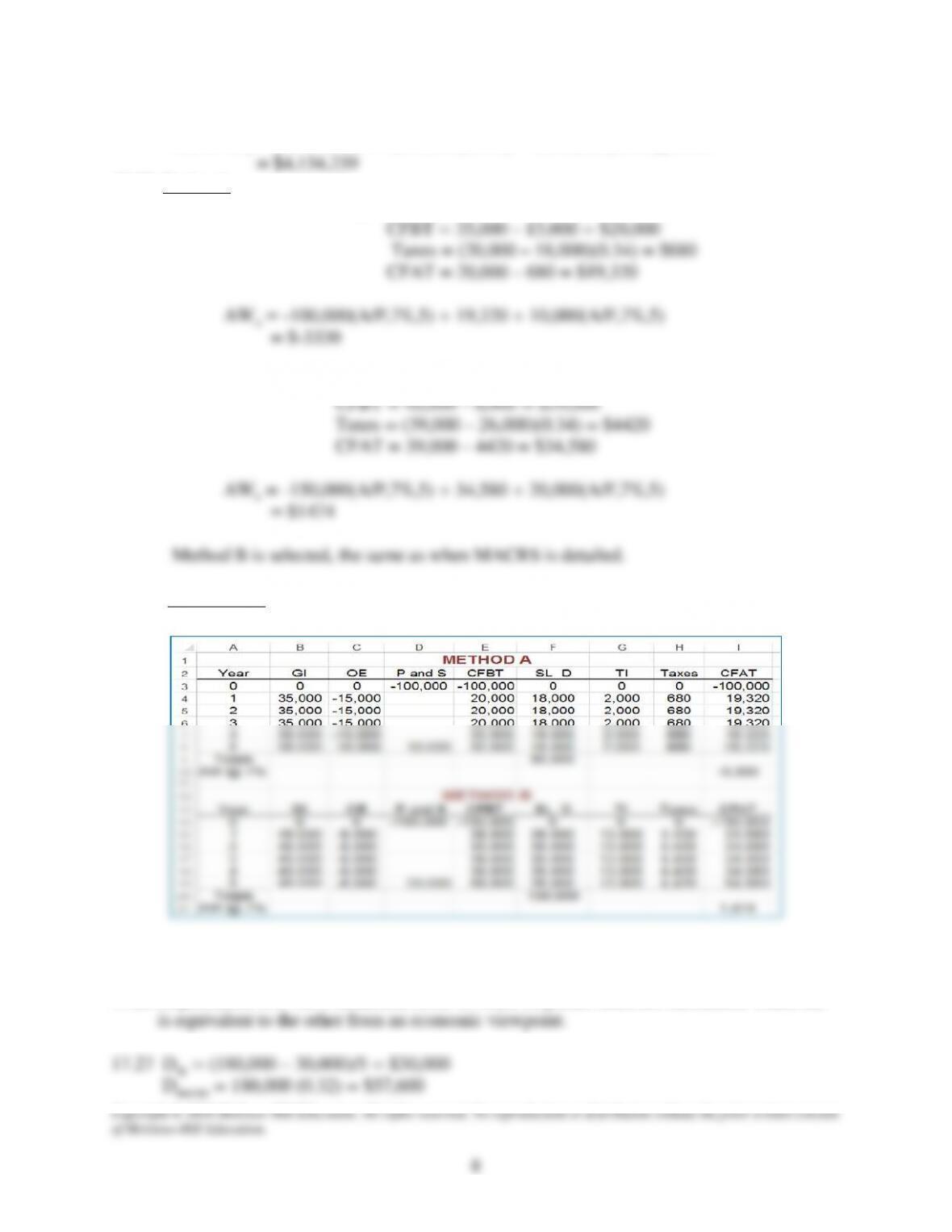

17.25 By hand:

Method A: Years 1-5, Depreciation = (100,000 – 10,000)/5 = $18,000

Method B: Years 1-5, Depreciation = (150,000 – 20,000)/5 = $26,000

Spreadsheet: Select Method B.

Depreciation Effects on Taxes

17.26 Depreciation is a 100% deduction from TI when corporate taxes are calculated. Thus, one

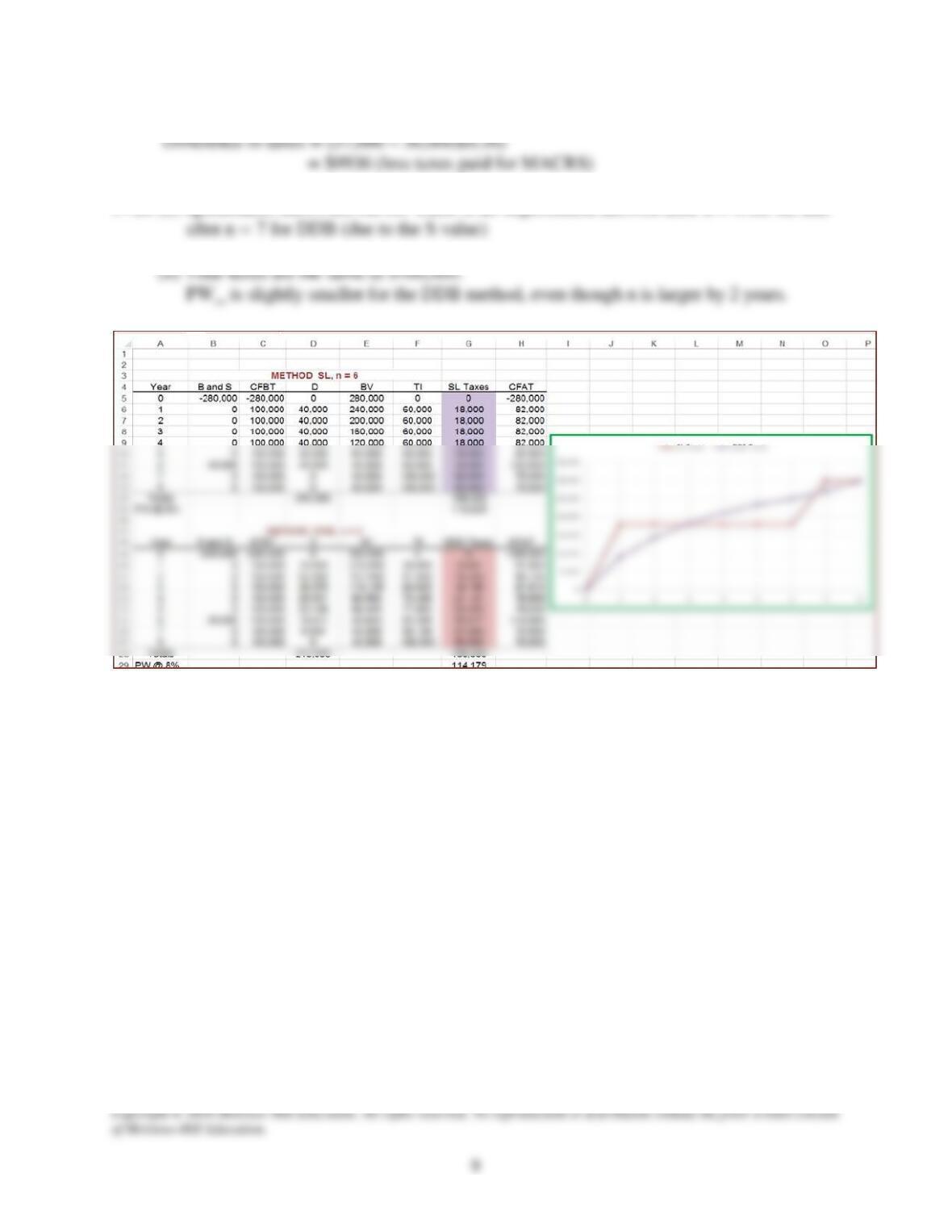

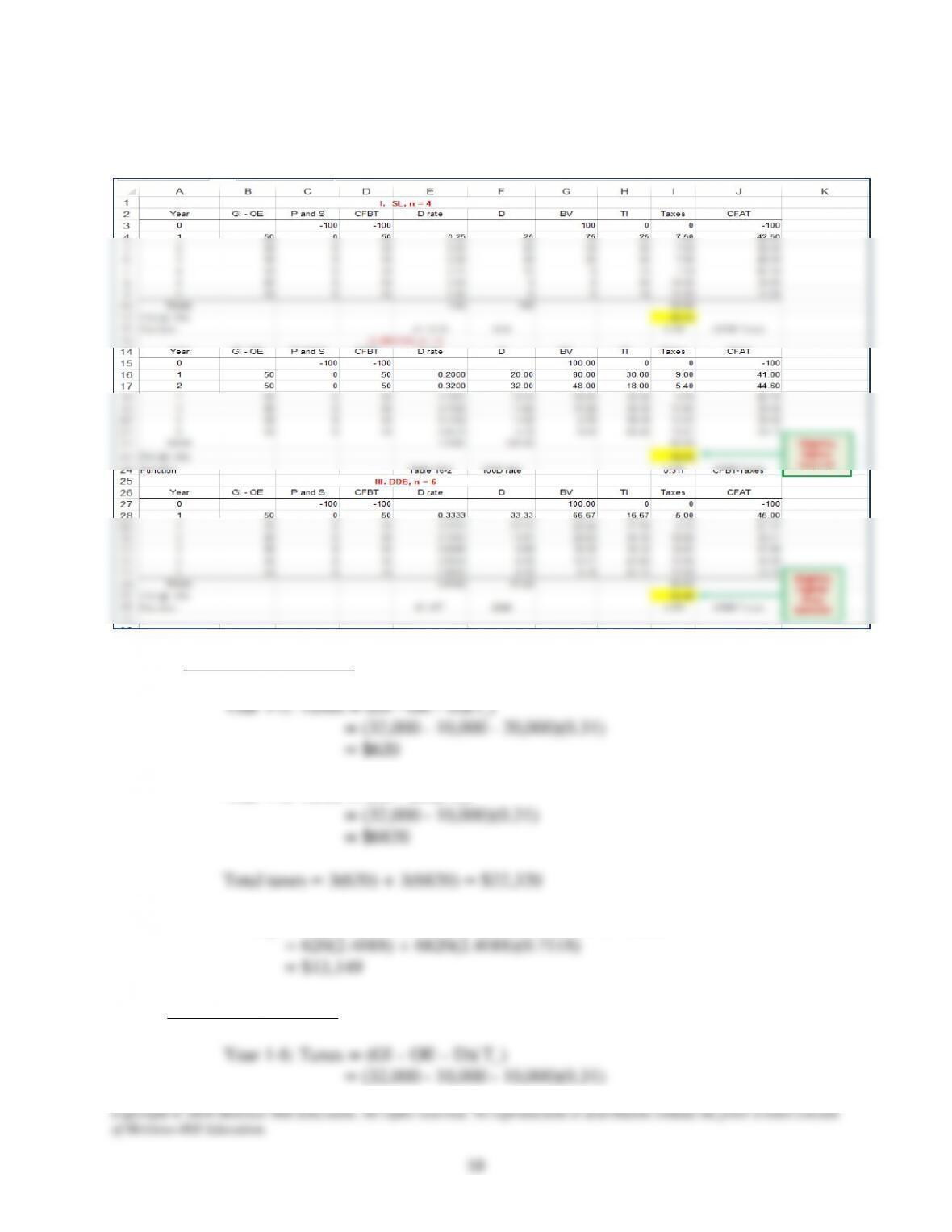

17.28 (a) Spreadsheet shows tax curves. There is no depreciation allowed after n = 6 for SL and

17.29 Did you guess correctly that SL with n = 4 years will be slightly lower in PW of taxes?

The shorter recovery period overrides the accelerated write–off in this case.

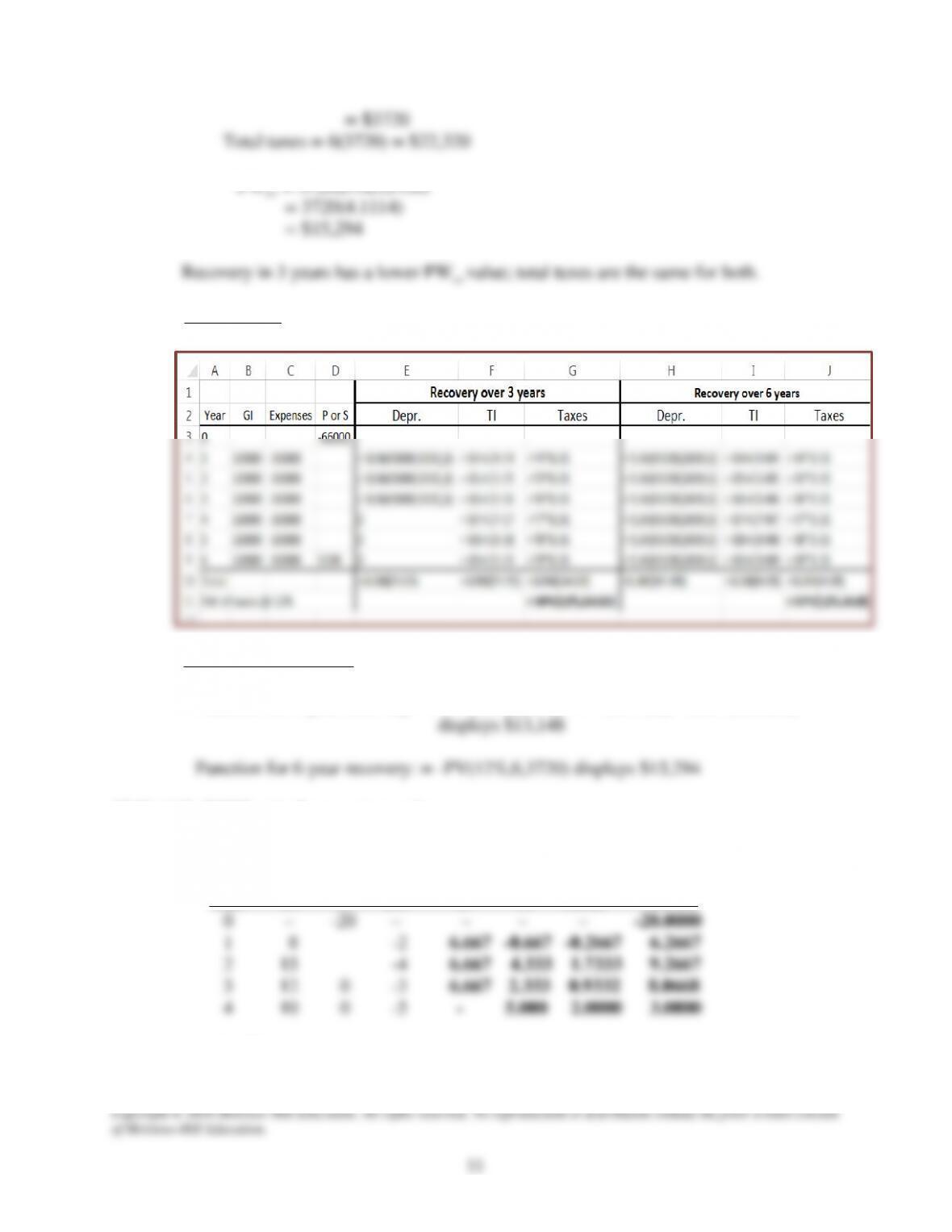

17.30 (a) Recovery over 3 years. SL depreciation is 60,000/3 = $20,000 per year

Year 4–6: Taxes = (GI – OE)( Te )

PWtax = 620(P/A,12%,3) + 6820(P/A,12%,3)(P/F,12%,3)

Recovery over 6 years. SL depreciation is 60,000/6 = $10,000 per year

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

11

= $3720

Total taxes = 6(3720) = $22,320

PWtax = 3720(P/A,12%,6)

(b) Spreadsheet: Solution follows with only the functions shown.

(c) Spreadsheet functions:

Function for 3–year recovery: = -PV(12%,3,620) + PV(12%,3,,PV(12%,3,6820))

17.31 (a) In $1000 units for monetary values.

SL: D = (20 – 0)/3 = $6.667 Te = 0.40

Year GI P OE D TI Taxes CFAT

(b) In $1000 units for monetary values.

MACRS rates Te = 0.40

Year GI P OE D TI Taxes CFAT

17.32 Find the difference between PW of CFBT and CFAT at Te = 0.40 and i = 10%

Year CFBT, $ d Depr., $ TI, $ Taxes, $ CFAT, $

17.33 All monetary terms are in $1000 units

Scenario 1: Uniform write–off

Sample for year 2: CFAT = 15 – 4 – [(15 – 4 – 6)(0.32)] = 9.40

NOPAT = 5 – 1.6 = 3.40

Year GI OE P D TI Taxes CFAT NOPAT

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

13

(a) Total NOPAT = $4.76 ($4760)

(b) PWtax = 1.6(P/F,6%,2) + 0.96(P/F,6%,3) – 0.32(P/F,6%.4)

= $1.9765 ($1977)

Scenario 2: Accelerated write–off

Year GI OE P D TI Taxes CFAT NOPAT

Total 4.205

Conclusion: A larger NOPAT and lower PWtax are better economically. Scenario 1

(accelerated depreciation) is the choice for the PWtax criterion.

Depreciation Recapture and Capital Gains (Losses)

17.34 It is important in an after-tax replacement analysis, because a ‘sacrifice’ trade-in value

17.35 BV2 = 120,000 – 120,000(0.3333 + 0.4445) = $26,664

17.36 TI will increase by DR, since MACRS BV5 = 0

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

14

Te = 0.065 + (1 – 0.065)(0.35) = 0.39225

Tax increase = 100,000(0.39225) = $39,225

17.37 (a) Land is not depreciable.

(b) SP = $10,000

(c) SP = 0.2(150,000) = $30,000

17.38 Total MACRS depreciation: 20% + 32% + 19.2% = 71.2%

Selling price of $80,000 < BV3. There is a capital loss

17.39 (a) CG = 285,000 – 240,000

(b) Taxes are shown in column I. TI for year 3 must include CG and DR as fully taxable.

17.40 Land: CG = $45,000

17.41 (a) BV2 = 28,500 – 28,500(0.3333 + 0.4445) = $6333

(b) Capital losses can only be used to offset capital gains. This will reduce taxes on the

17.42 Thomas omitted the $100,000 DR in year 4. If included, in $1000 units, the CFAT is

After–Tax Economic Evaluation

17.43 (a) Before-tax ROR: 0 = -750,000 + 260,000(P/A,i*,3) + 187,500(P/F,i*,3)

(b) Approximate after–tax ROR = (before–tax ROR) (1-Te)

17.44 Effective tax rate = 0.06 + (1 – 0.06)(0.35) = 0.38

17.45 0.08 = 0.12(1 – Te)

17.46 After-tax ROR = 24(1- 0.35) = 15.6%

17.47 Calculate taxes using Table 17-1 rates; the average tax rate Te; then after–tax ROR

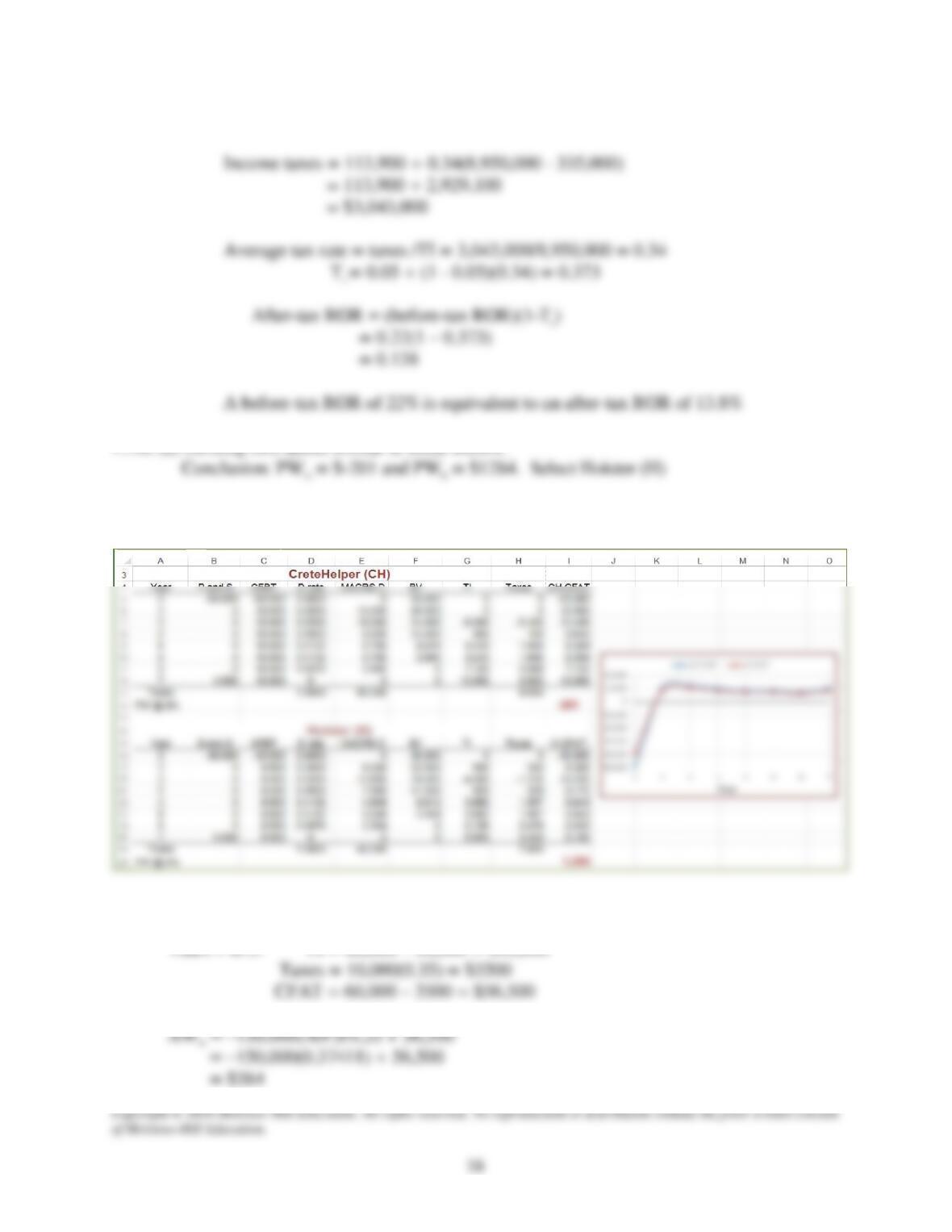

17.48 (a) Develop two tables similar to those shown.

(b) Plot of CFAT values shows they track closely.

17.49 System A: Depreciation = 150,000/3 = $50,000

Years 1 to 3: TI = 60,000 – 50,000 = $10,000

Copyright © 2018 McGraw–Hill Education. All rights reserved. No reproduction or distribution without the prior written consent

of McGraw–Hill Education.

17

System B: Depreciation = 85,000/5 = $17,000

For year 5 only, when B is sold for 10% of first cost:

Select system A

17.50 For a 12% after–tax return, find n in a PW relation.

Keep the equipment for 8.85 (or 9 rounded off) years

17.51 (a) By hand: Alternative X

Year

P and S

GI – OE

D

TI

Taxes

CFAT

0

-8000

–

–

–

–

-8000

1

3500

2666

834

333

3167

2

3500

3556

-56

-22

3522

3

3500

1185

2315

926

2574

4

0

0

593

-593

-237

237

PWX = -8000 + 3167(P/F,8%,1) + 3522(P/F,8%,2) + 2574(P/F,8%,3) + 237(P/F,8%,4)

= $169