CHAPTER 3 B-21

The common-base year answers for Question 14 are found by dividing each category value for 2009

by the same category value for 2008. For example, the cash common-base year number is found by:

$10,157 / $8,436 = 1.2040

This means the cash balance in 2009 is 1.2040 times as large as the cash balance in 2008.

The common-size, common-base year answers for Question 15 are found by dividing the common-

size percentage for 2009 by the common-size percentage for 2008. For example, the cash calculation

is found by:

3.13% / 2.86% = 1.0961

This tells us that cash, as a percentage of assets, increased by 9.61%.

16. 2008

Sources/Uses 2008

Assets

Current assets

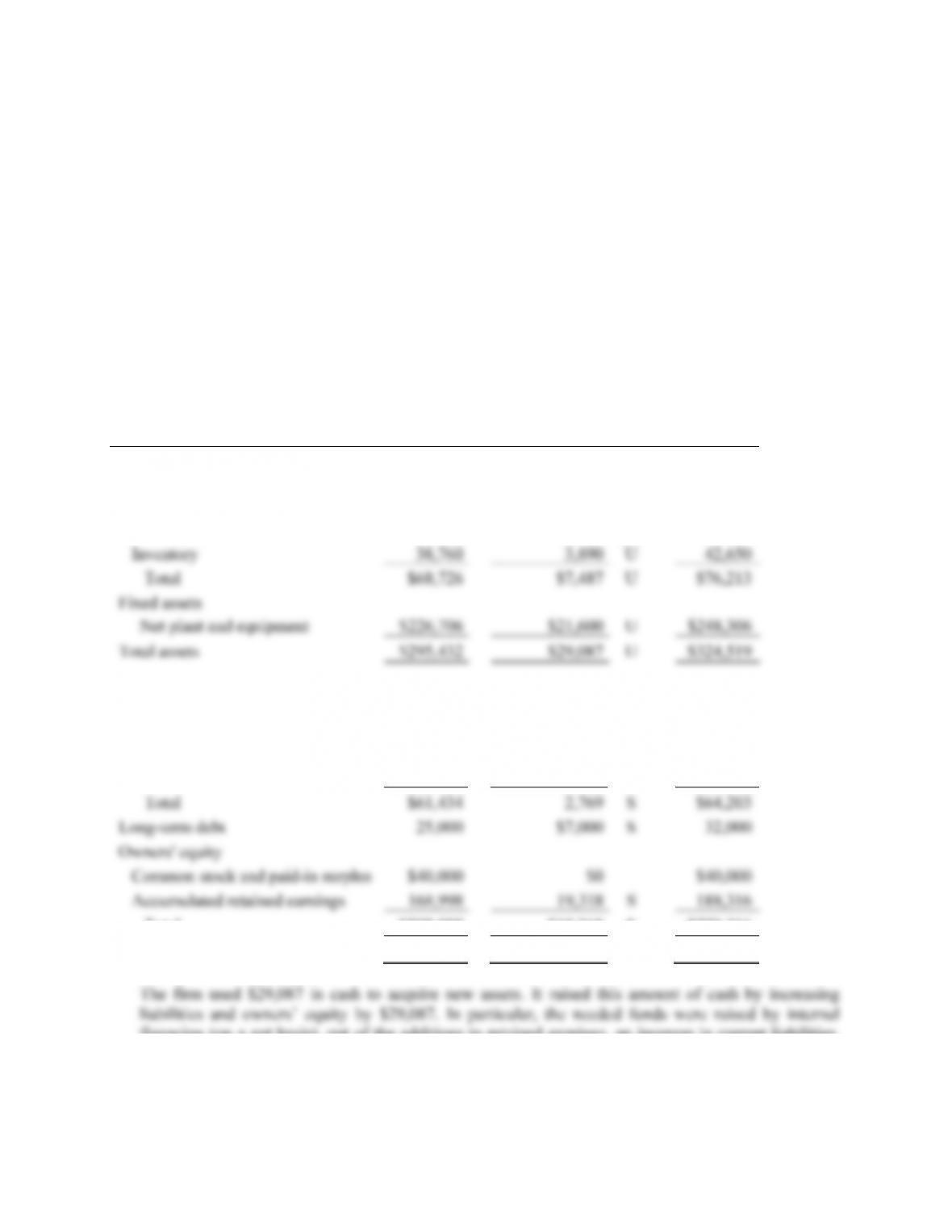

Cash $8,436 $1,721 U $10,157

Accounts receivable 21,530 1,876 U 23,406

Liabilities and Owners’ Equity

Current liabilities

Accounts payable $43,050 3,771 S $46,821

Notes payable 18,384 –1,002 U 17,382

Total $208,998 $19,318 S $228,316

Total liabilities and owners’ equity $295,432 $29,087 S $324,519

financing (on a net basis), out of the additions to retained earnings, an increase in current liabilities,

and by an issue of long-term debt.

B-22 SOLUTIONS

17. a. Current ratio = Current assets / Current liabilities

b. Quick ratio = (Current assets – Inventory) / Current liabilities

c. Cash ratio = Cash / Current liabilities

d. NWC ratio = NWC / Total assets

e. Debt-equity ratio = Total debt / Total equity

Equity multiplier = 1 + D/E

f. Total debt ratio = (Total assets – Total equity) / Total assets

Long-term debt ratio = Long-term debt / (Long-term debt + Total equity)

Intermediate

18. This is a multi-step problem involving several ratios. The ratios given are all part of the DuPont

Identity. The only DuPont Identity ratio not given is the profit margin. If we know the profit margin,

we can find the net income since sales are given. So, we begin with the DuPont Identity:

ROE = 0.15 = (PM)(TAT)(EM) = (PM)(S / TA)(1 + D/E)

Solving the DuPont Identity for profit margin, we get:

PM = [(ROE)(TA)] / [(1 + D/E)(S)]

Now that we have the profit margin, we can use this number and the given sales figure to solve for

net income:

PM = .0339 = NI / S

CHAPTER 3 B-23

19. This is a multi-step problem involving several ratios. It is often easier to look backward to determine

where to start. We need receivables turnover to find days’ sales in receivables. To calculate

receivables turnover, we need credit sales, and to find credit sales, we need total sales. Since we are

given the profit margin and net income, we can use these to calculate total sales as:

Credit sales are 70 percent of total sales, so:

Now we can find receivables turnover by:

20. The solution to this problem requires a number of steps. First, remember that CA + NFA = TA. So, if

we find the CA and the TA, we can solve for NFA. Using the numbers given for the current ratio and

the current liabilities, we solve for CA:

CR = CA / CL

To find the total assets, we must first find the total debt and equity from the information given. So,

we find the sales using the profit margin:

PM = NI / Sales

We now use the net income figure as an input into ROE to find the total equity:

ROE = NI / TE

Next, we need to find the long-term debt. The long-term debt ratio is:

Inverting both sides gives:

Substituting the total equity into the equation and solving for long-term debt gives the following:

B-24 SOLUTIONS

Now, we can find the total debt of the company:

And, with the total debt, we can find the TD&E, which is equal to TA:

And finally, we are ready to solve the balance sheet identity as:

21. Child: Profit margin = NI / S = $3.00 / $50 = .06 or 6%

The advertisement is referring to the store’s profit margin, but a more appropriate earnings measure

for the firm’s owners is the return on equity.

ROE = NI / TE = NI / (TA – TD)

22. The solution requires substituting two ratios into a third ratio. Rearranging D/TA:

Firm A Firm B

D / TA = .35 D / TA = .30

(TA – E) / TA = .35 (TA – E) / TA = .30

(TA / TA) – (E / TA) = .35 (TA / TA) – (E / TA) = .30

1 – (E / TA) = .35 1 – (E / TA) = .30

E / TA = .65 E / TA = .30

E = .65(TA) E = .70 (TA)

Rearranging ROA, we find:

NI / TA = .12 NI / TA = .11

NI = .12(TA) NI = .11(TA)

Since ROE = NI / E, we can substitute the above equations into the ROE formula, which yields:

23. This problem requires you to work backward through the income statement. First, recognize that

Net income = (1 – t)EBT. Plugging in the numbers given and solving for EBT, we get:

Now, we can add interest to EBT to get EBIT as follows:

CHAPTER 3 B-25

To get EBITD (earnings before interest, taxes, and depreciation), the numerator in the cash coverage

ratio, add depreciation to EBIT:

Now, simply plug the numbers into the cash coverage ratio and calculate:

24. The only ratio given which includes cost of goods sold is the inventory turnover ratio, so it is the last

ratio used. Since current liabilities is given, we start with the current ratio:

Using the quick ratio, we solve for inventory:

Inventory = CA – (Quick ratio × CL)

25. PM = NI / S = –£13,482,000 / £138,793 = –0.0971 or –9.71%

As long as both net income and sales are measured in the same currency, there is no problem; in fact,

except for some market value ratios like EPS and BVPS, none of the financial ratios discussed in the

NI = PM × Sales

26. Short-term solvency ratios:

Current ratio = Current assets / Current liabilities

Quick ratio = (Current assets – Inventory) / Current liabilities

Cash ratio = Cash / Current liabilities

B-26 SOLUTIONS

Asset utilization ratios:

Total asset turnover = Sales / Total assets

Receivables turnover = Sales / Accounts receivable

Long-term solvency ratios:

Total debt ratio = (Total assets – Total equity) / Total assets

Debt-equity ratio = Total debt / Total equity

Equity multiplier = 1 + D/E

Times interest earned = EBIT / Interest

Cash coverage ratio = (EBIT + Depreciation) / Interest

Profitability ratios:

Profit margin = Net income / Sales

Return on assets = Net income / Total assets

Return on equity = Net income / Total equity

27. The DuPont identity is:

ROE = (PM)(TAT)(EM)