CHAPTER 2 B-5

9. If a company raises more money from selling stock than it pays in dividends in a particular period,

its cash flow to stockholders will be negative. If a company borrows more than it pays in interest, its

cash flow to creditors will be negative.

10. The adjustments discussed were purely accounting changes; they had no cash flow or market value

consequences unless the new accounting information caused stockholders to revalue the derivatives.

11. Enterprise value is the theoretical takeover price. In the event of a takeover, an acquirer would have

to take on the company’s debt, but would pocket its cash. Enterprise value differs significantly from

simple market capitalization in several ways, and it may be a more accurate representation of a firm’s

value. In a takeover, the value of a firm’s debt would need to be paid by the buyer when taking over

a company. This enterprise value provides a much more accurate takeover valuation because it

includes debt in its value calculation.

12. In general, it appears that investors prefer companies that have a steady earnings stream. If true, this

encourages companies to manage earnings. Under GAAP, there are numerous choices for the way a

company reports its financial statements. Although not the reason for the choices under GAAP, one

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple

steps. Due to space and readability constraints, when these intermediate steps are included in this

solutions manual, rounding may appear to have occurred. However, the final answer for each problem is

found without rounding during any step in the problem.

Basic

1. To find owner’s equity, we must construct a balance sheet as follows:

Balance Sheet

CA $5,100 CL $4,300

NFA 23,800 LTD 7,400

OE ??

TA $28,900 TL & OE $28,900

We know that total liabilities and owner’s equity (TL & OE) must equal total assets of $28,900.

We also know that TL & OE is equal to current liabilities plus long-term debt plus owner’s

equity, so owner’s equity is:

B-6 SOLUTIONS

2. The income statement for the company is:

Income Statement

Sales $586,000

Costs 247,000

Depreciation 43,000

3. One equation for net income is:

Net income = Dividends + Addition to retained earnings

Rearranging, we get:

4. EPS = Net income / Shares = $171,600 / 85,000 = $2.02 per share

5. To find the book value of current assets, we use: NWC = CA – CL. Rearranging to solve for

current assets, we get:

CA = NWC + CL = $380,000 + 1,400,000 = $1,480,000

The market value of current assets and fixed assets is given, so:

6. Taxes = 0.15($50K) + 0.25($25K) + 0.34($25K) + 0.39($236K – 100K) = $75,290

7. The average tax rate is the total tax paid divided by net income, so:

CHAPTER 2 B-7

8. To calculate OCF, we first need the income statement:

Income Statement

Sales $27,500

Costs 13,280

Depreciation 2,300

EBIT $11,920

Interest 1,105

Taxable income $10,815

Taxes (35%) 3,785

9. Net capital spending = NFAend – NFAbeg + Depreciation

10. Change in NWC = NWCend – NWCbeg

Change in NWC = (CAend – CLend) – (CAbeg – CLbeg)

Change in NWC = ($2,250 – 1,710) – ($2,100 – 1,380)

11. Cash flow to creditors = Interest paid – Net new borrowing

Cash flow to creditors = Interest paid – (LTDend – LTDbeg)

Cash flow to creditors = $170,000 – ($2,900,000 – 2,600,000)

12. Cash flow to stockholders = Dividends paid – Net new equity

Note, APIS is the additional paid-in surplus.

13. Cash flow from assets = Cash flow to creditors + Cash flow to stockholders

= –$130,000 + 115,000 = –$15,000

B-8 SOLUTIONS

Intermediate

14. To find the OCF, we first calculate net income.

Income Statement

Sales $196,000

Costs 104,000

Other expenses 6,800

Depreciation 9,100

EBIT $76,100

Interest 14,800

Taxable income $61,300

Taxes 21,455

Net income $39,845

Dividends $10,400

Additions to RE $29,445

a. OCF = EBIT + Depreciation – Taxes = $76,100 + 9,100 – 21,455 = $63,745

Note that the net new long-term debt is negative because the company repaid part of its long-

term debt.

d. We know that CFA = CFC + CFS, so:

CFA is also equal to OCF – Net capital spending – Change in NWC. We already know OCF.

Net capital spending is equal to:

Now we can use:

CFA = OCF – Net capital spending – Change in NWC

15. The solution to this question works the income statement backwards. Starting at the bottom:

CHAPTER 2 B-9

Now, looking at the income statement:

EBT – EBT × Tax rate = Net income

Recognize that EBT × Tax rate is simply the calculation for taxes. Solving this for EBT yields:

Now you can calculate:

The last step is to use:

EBIT = Sales – Costs – Depreciation

Solving for depreciation, we find that depreciation = $6,846

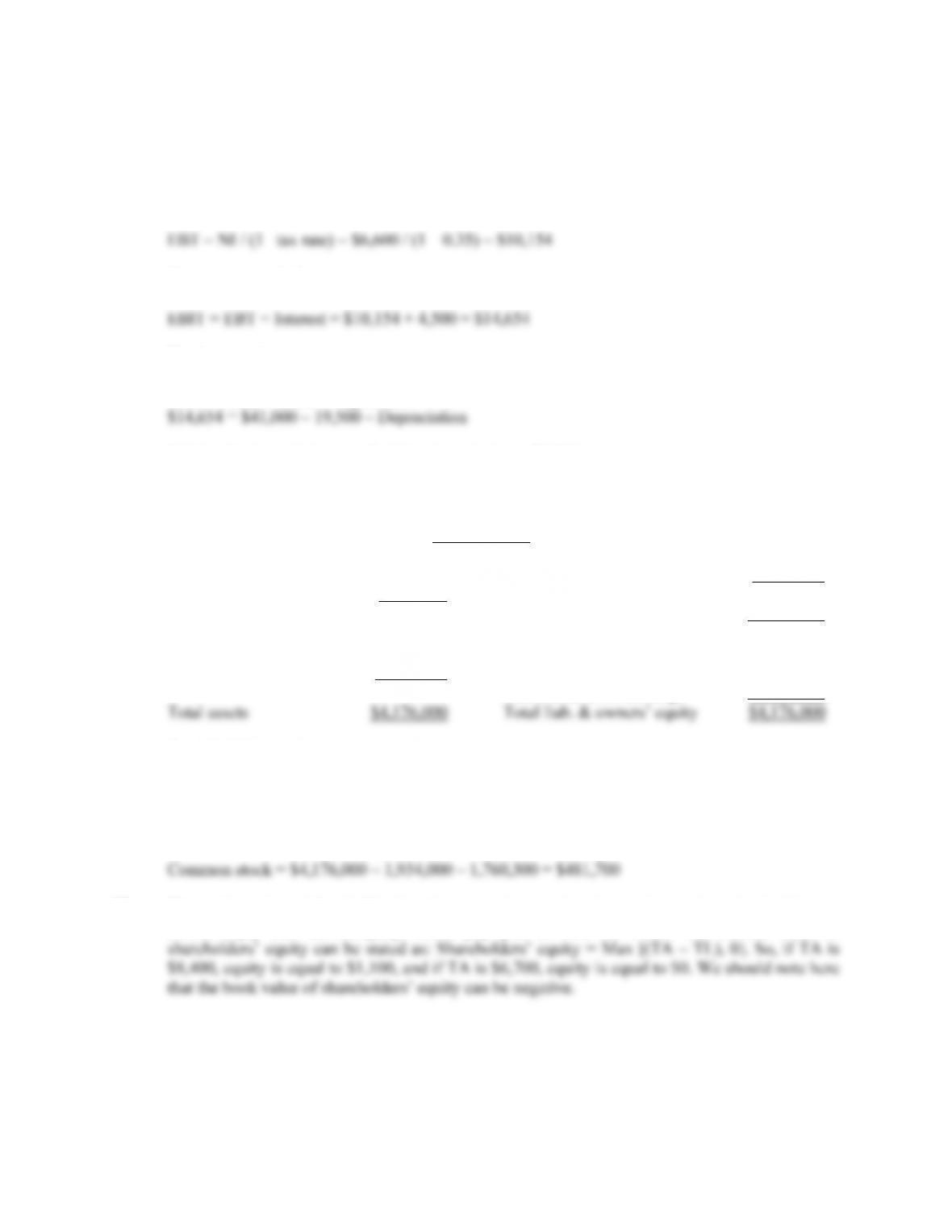

16. The balance sheet for the company looks like this:

Balance Sheet

Cash $195,000 Accounts payable $405,000

Accounts receivable 137,000 Notes payable 160,000

Inventory 264,000 Current liabilities $565,000

Current assets $596,000 Long-term debt 1,195,300

Total liabilities $1,760,300

Tangible net fixed assets 2,800,000

Intangible net fixed assets 780,000 Common stock ??

Accumulated ret. earnings 1,934,000

Total liabilities and owners’ equity is:

TL & OE = CL + LTD + Common stock + Retained earnings

Solving for this equation for equity gives us:

17. The market value of shareholders’ equity cannot be negative. A negative market value in this case

would imply that the company would pay you to own the stock. The market value of

B-10 SOLUTIONS

b. Each firm has a marginal tax rate of 34% on the next $10,000 of taxable income, despite their

different average tax rates, so both firms will pay an additional $3,400 in taxes.

19. Income Statement

Sales $730,000

COGS 580,000

A&S expenses 105,000

Depreciation 135,000

EBIT –$90,000

c. Net income was negative because of the tax deductibility of depreciation and interest

20. A firm can still pay out dividends if net income is negative; it just has to be sure there is sufficient

cash flow to make the dividend payments.

Change in NWC = Net capital spending = Net new equity = 0. (Given)

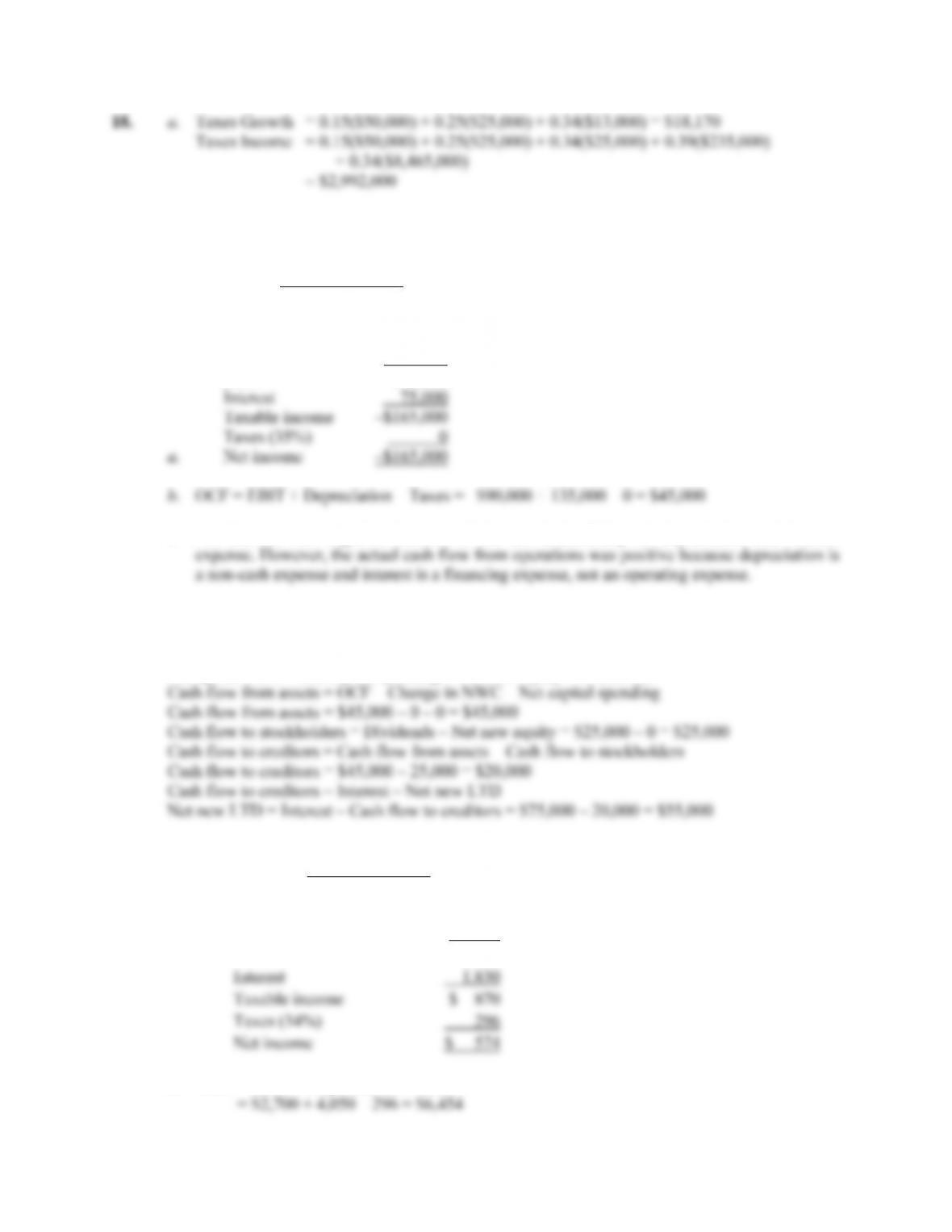

21. a.

Income Statement

Sales $22,800

Cost of goods sold 16,050

Depreciation 4,050

EBIT $ 2,700

b. OCF = EBIT + Depreciation – Taxes

= (CA

end – CLend) – (CAbeg – CLbeg)

Net capital spending = NFAend – NFAbeg + Depreciation

= $16,800 – 13,650 + 4,050 = $7,200

CFA = OCF – Change in NWC – Net capital spending

The cash flow from assets can be positive or negative, since it represents whether the firm

raised funds or distributed funds on a net basis. In this problem, even though net income and

d. Cash flow to creditors = Interest – Net new LTD = $1,830 – 0 = $1,830

We can also calculate the cash flow to stockholders as:

The firm had positive earnings in an accounting sense (NI > 0) and had positive cash flow

from operations. The firm invested $680 in new net working capital and $7,200 in new fixed

assets. The firm had to raise $1,426 from its stakeholders to support this new investment. It

22. a. Total assets 2008 = $653 + 2,691 = $3,344

b. NWC 2008 = CA08 – CL08 = $653 – 261 = $392

B-12 SOLUTIONS

c. We can calculate net capital spending as:

Net capital spending = Net fixed assets 2009 – Net fixed assets 2008 + Depreciation

So, the company had a net capital spending cash flow of $1,287. We also know that net

capital spending is:

Net capital spending = Fixed assets bought – Fixed assets sold

To calculate the cash flow from assets, we must first calculate the operating cash flow. The

income statement is:

Income Statement

Sales $ 8,280.00

Costs 3,861.00

Depreciation expense 738 .00

EBIT $3,681.00

Interest expense 211 .00

EBT $3,470.00

Taxes (35%) 1,215.50

Net income $2,256.50

So, the operating cash flow is:

And the cash flow from assets is:

Cash flow from assets = OCF – Change in NWC – Net capital spending.

d. Net new borrowing = LTD09 – LTD08 = $1,512 – 1,422 = $90

Challenge

23. Net capital spending = NFAend – NFAbeg + Depreciation

= (NFAend – NFAbeg) + (Depreciation + ADbeg) – ADbeg

CHAPTER 2 B-13

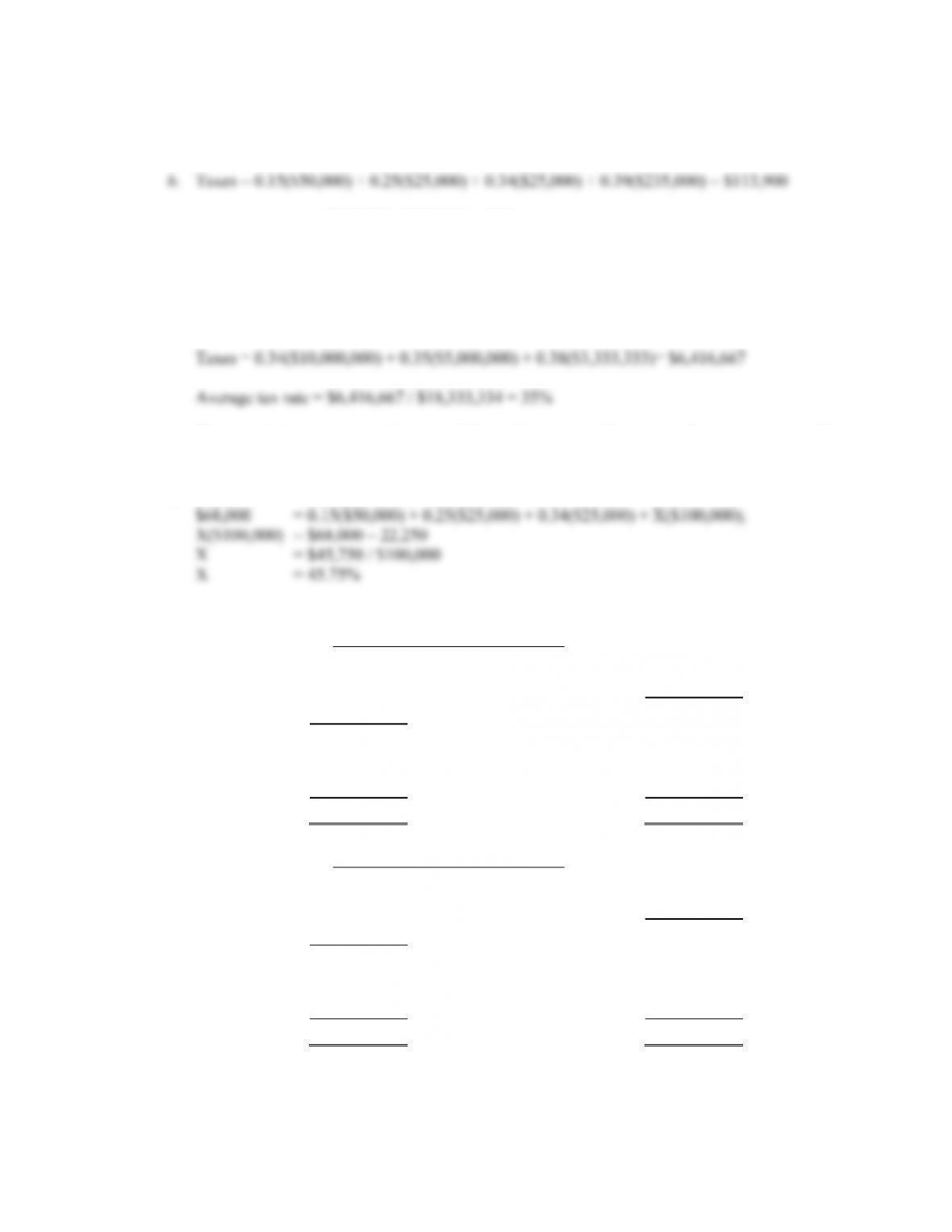

24. a. The tax bubble causes average tax rates to catch up to marginal tax rates, thus eliminating the

tax advantage of low marginal rates for high income corporations.

Average tax rate = $113,900 / $335,000 = 34%

The marginal tax rate on the next dollar of income is 34 percent.

For corporate taxable income levels of $335,000 to $10 million, average tax rates are equal to

marginal tax rates.

The marginal tax rate on the next dollar of income is 35 percent. For corporate taxable

income levels over $18,333,334, average tax rates are again equal to marginal tax rates.

c. Taxes = 0.34($200,000) = $68,000

25.

Balance sheet as of Dec. 31, 2008

Cash $3,792 Accounts payable $3,984

Accounts receivable 5,021 Notes payable 732

Inventory 8,927 Current liabilities $4,716

Current assets $17,740

Long-term debt $12,700

Net fixed assets $31,805 Owners’ equity 32,129

Total assets $49,545 Total liab. & equity $49,545

Balance sheet as of Dec. 31, 2009

Cash $4,041 Accounts payable $4,025

Accounts receivable 5,892 Notes payable 717

Inventory 9,555 Current liabilities $4,742

Current assets $19,488

Long-term debt $15,435

Net fixed assets $33,921 Owners’ equity 33,232

Total assets $53,409 Total liab. & equity $53,409

B-14 SOLUTIONS

2008 Income Statement 2009 Income Statement

Sales $7,233.00 Sales $8,085.00

COGS 2,487.00 COGS 2,942.00

Other expenses 591.00 Other expenses 515.00

Depreciation 1,038.00 Depreciation 1,085.00

EBIT $3,117.00 EBIT $3,543.00

Interest 485.00 Interest 579.00

EBT $2,632.00 EBT $2,964.00

Taxes (34%) 894.88 Taxes (34%) 1,007.76

N

et income $1,737.12 Net income $1,956.24

Dividends $882.00 Dividends $1,011.00

Additions to RE 855.12 Additions to RE 945.24

26. OCF = EBIT + Depreciation – Taxes = $3,543 + 1,085 – 1,007.76 = $3,620.24

Change in NWC = NWCend – NWCbeg = (CA – CL) end – (CA – CL) beg

= ($19,488 – 4,742) – ($17,740 – 4,716)

= $1,722

Net capital spending = NFAend – NFAbeg + Depreciation

= $33,921 – 31,805 + 1,085 = $3,201

Cash flow from assets = OCF – Change in NWC – Net capital spending

= $3,620.24 – 1,722 – 3,201 = –$1,302.76

Cash flow to creditors = Interest – Net new LTD

Net new LTD = LTDend – LTDbeg

Cash flow to creditors = $579 – ($15,435 – 12,700) = –$2,156

Net new equity = Common stockend – Common stockbeg

Common stock + Retained earnings = Total owners’ equity

Net new equity = (OE – RE) end – (OE – RE) beg

= OEend – OEbeg + REbeg – REend

REend = REbeg + Additions to RE08

Net new equity = OEend – OEbeg + REbeg – (REbeg + Additions to RE08)

= OEend – OEbeg – Additions to RE

Net new equity = $33,232 – 32,129 – 945.24 = $157.76

CFS = Dividends – Net new equity

CFS = $1,011 – 157.76 = $853.24

As a check, cash flow from assets is –$1,302.76.

CFA = Cash flow from creditors + Cash flow to stockholders

CFA = –$2,156 + 853.24 = –$1,302.76