B-304 SOLUTIONS

10. BlueSky will need less financing because it is essentially borrowing more from its suppliers. Among

other things, BlueSky will likely need less short-term borrowing from other sources, so it will save on

interest expense.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple steps.

Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

1. a. No change. A dividend paid for by the sale of debt will not change cash since the cash raised from

b. No change. The real estate is paid for by the cash raised from the debt, so this will not change the

c. No change. Inventory and accounts payable will increase, but neither will impact the cash account.

d. Decrease. The short-term bank loan is repaid with cash, which will reduce the cash balance.

e. Decrease. The payment of taxes is a cash transaction.

f. Decrease. The preferred stock will be repurchased with cash.

g. No change. Accounts receivable will increase, but cash will not increase until the sales are paid

off.

j. Decrease. The accounts payable are reduced through cash payments to suppliers.

k. Decrease. Here the dividend payments are made with cash, which is generally the case. This is

l. No change. The short-term note will not change the cash balance.

m. Decrease. The utility bills must be paid in cash.

n. Decrease. A cash payment will reduce cash.

o. Increase. If marketable securities are sold, the company will receive cash from the sale.

CHAPTER 18 B-305

2. The total liabilities and equity of the company are the net book worth, or market value of equity, plus

current liabilities and long-term debt, so:

Total liabilities and equity = $10,380 + 1,450 + 7,500

Total liabilities and equity = $19,330

This is also equal to the total assets of the company. Since total assets are the sum of all assets, and cash

is an asset, the cash account must be equal to total assets minus all other assets, so:

3. a. Increase. If receivables go up, the time to collect the receivables would increase, which increases

b. Increase. If credit repayment times are increased, customers will take longer to pay their bills,

c. Decrease. If the inventory turnover increases, the inventory period decreases.

d. No change. The accounts payable period is part of the cash cycle, not the operating cycle.

e. Decrease. If the receivables turnover increases, the receivables period decreases.

f. No change. Payments to suppliers affects the accounts payable period, which is part of the cash

4. a. Increase; Increase. If the terms of the cash discount are made less favorable to customers, the

b. Increase; No change. This will shorten the accounts payable period, which will increase the cash

B-306 SOLUTIONS

c. Decrease; Decrease. If more customers pay in cash, the accounts receivable period will decrease.

d. Decrease; Decrease. Assume the accounts payable period does not change. Fewer raw materials

e. Decrease; No change. If more raw materials are purchased on credit, the accounts payable period

will tend to increase, which would decrease the cash cycle. We should say that this may not be the

case. The accounts payable period is a decision made by the company’s management. The

f. Increase; Increase. If more goods are produced for inventory, the inventory period will increase.

5. a. A 45-day collection period implies all receivables outstanding from the previous quarter are

collected in the current quarter, and:

(90 – 45)/90 = 1/2 of current sales are collected. So:

Q1 Q2 Q3 Q4

b. A 60-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and:

(90-60)/90 = 1/3 of current sales are collected. So:

Q1 Q2 Q3 Q4

CHAPTER 18 B-307

c. A 30-day collection period implies all receivables outstanding from previous quarter are collected

in the current quarter, and:

(90-30)/90 = 2/3 of current sales are collected. So:

Q1 Q2 Q3 Q4

6. The operating cycle is the inventory period plus the receivables period. The inventory turnover and

inventory period are:

Inventory turnover = COGS/Average inventory

Inventory turnover = $56,384/{[$9,780 + 11,380]/2}

Inventory turnover = 5.3293 times

Inventory period = 365 days/Inventory turnover

Inventory period = 365 days/5.3293

Inventory period = 68.49 days

And the receivables turnover and receivables period are:

Receivables turnover = Credit sales/Average receivables

Receivables turnover = $89,804/{[$4,108 + 4,938]/2}

Receivables turnover = 19.8550 times

7. If we factor immediately, we receive cash on an average of 32 days sooner. The number of periods in a

year are:

Number of periods = 365/32

Number of periods = 11.4063

8. a. The payables period is zero since the company pays immediately. The payment in each period is

30 percent of next period’s sales, so:

b. Since the payables period is 90 days, the payment in each period is 30 percent of the last period’s

sales, so:

c. Since the payables period is 60 days, the payment in each period is 2/3 of last quarter’s orders, plus

1/3 of this quarter’s orders, or:

CHAPTER 18 B-309

9. Since the payables period is 60 days, the payables in each period will be:

Payables each period = 2/3 of last quarter’s orders + 1/3 of this quarter’s orders

Payables each period = 2/3(.75) times current sales + 1/3(.75) next period sales

10. a. The November sales must have been the total uncollected sales minus the uncollected sales from

December, divided by the collection rate two months after the sale, so:

b. The December sales are the uncollected sales from December divided by the collection rate of the

previous months’ sales, so:

c. The collections each month for this company are:

Collections = .15(Sales from 2 months ago) + .20(Last month’s sales) + .65 (Current sales)

January collections = .15($246,666.67) + .20($388,571.43) + .65($235,000)

January collections = $267,464.29

B-310 SOLUTIONS

11. The sales collections each month will be:

Sales collections = .35(current month sales) + .60(previous month sales)

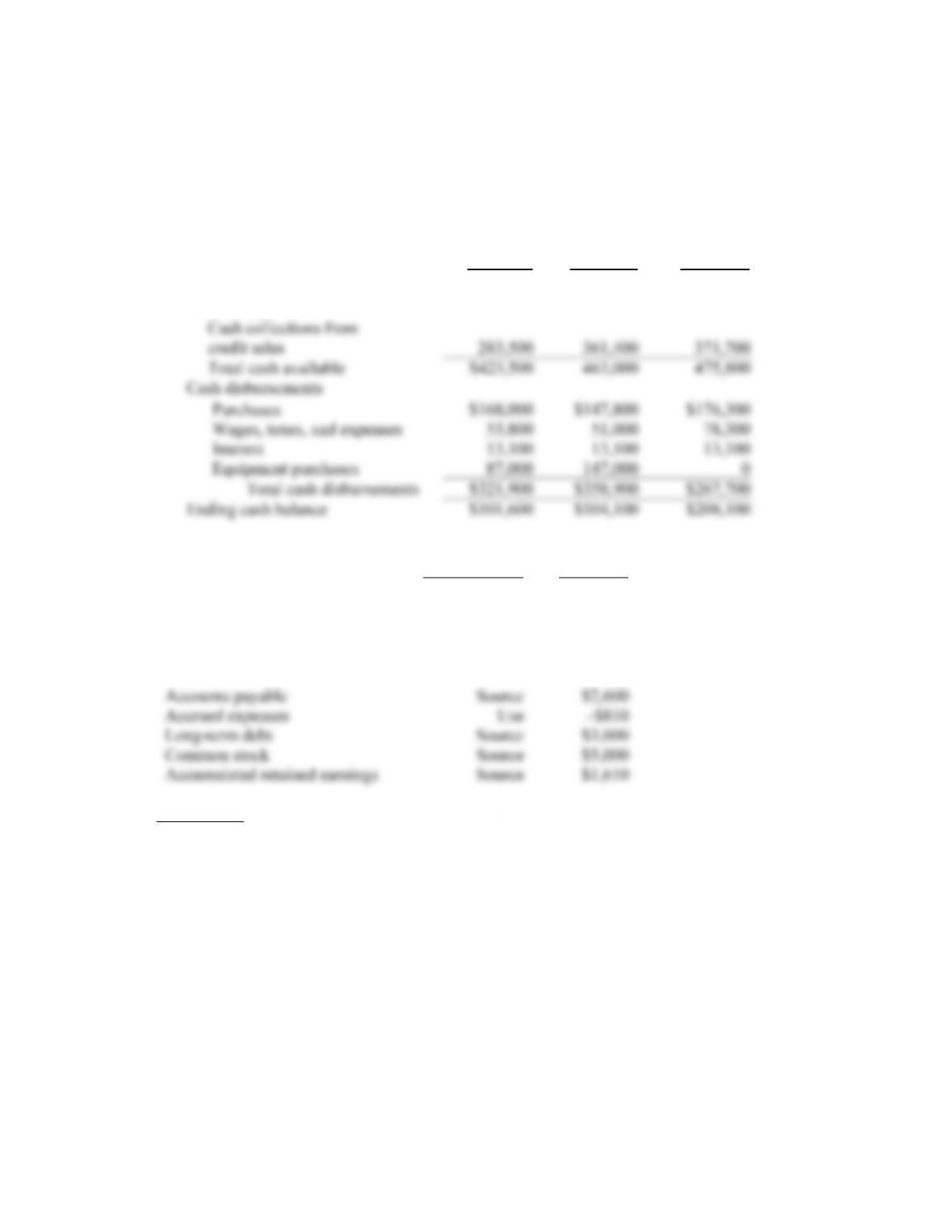

Given this collection, the cash budget will be:

April May June

Beginning cash balance $140,000 $101,600 $104,100

Cash receipts

12. Item

Source/Use Amount

Cash Source $1,100

Accounts receivable Use –$4,300

Inventories Use –$3,670

Property, plant, and equipment Use –$12,720

Intermediate

13. a. If you borrow $50,000,000 for one month, you will pay interest of:

Interest = $50,000,000(.0064)

Interest = $320,000

However, with the compensating balance, you will only get the use of:

Amount received = $50,000,000 – 50,000,000(.05)

Amount received = $47,500,000

This means the periodic interest rate is:

Periodic interest = $320,000/$47,500,000

Periodic interest = .006737 or 0.674%