CHAPTER 16 B-277

9. One side is that Continental was going to go bankrupt because its costs made it uncompetitive. The

bankruptcy filing enabled Continental to restructure and keep flying. The other side is that Continental

abused the bankruptcy code. Rather than renegotiate labor agreements, Continental simply abrogated

them to the detriment of its employees. In this, and the last several, questions, an important thing to

keep in mind is that the bankruptcy code is a creation of law, not economics. A strong argument can

always be made that making the best use of the bankruptcy code is no different from, for example,

minimizing taxes by making best use of the tax code. Indeed, a strong case can be made that it is the

financial manager’s duty to do so. As the case of Continental illustrates, the code can be changed if

socially undesirable outcomes are a problem.

10. The basic goal is to minimize the value of non-marketed claims.

Solutions to Questions and Problems

NOTE: All end of chapter problems were solved using a spreadsheet. Many problems require multiple steps.

Due to space and readability constraints, when these intermediate steps are included in this solutions

manual, rounding may appear to have occurred. However, the final answer for each problem is found

without rounding during any step in the problem.

Basic

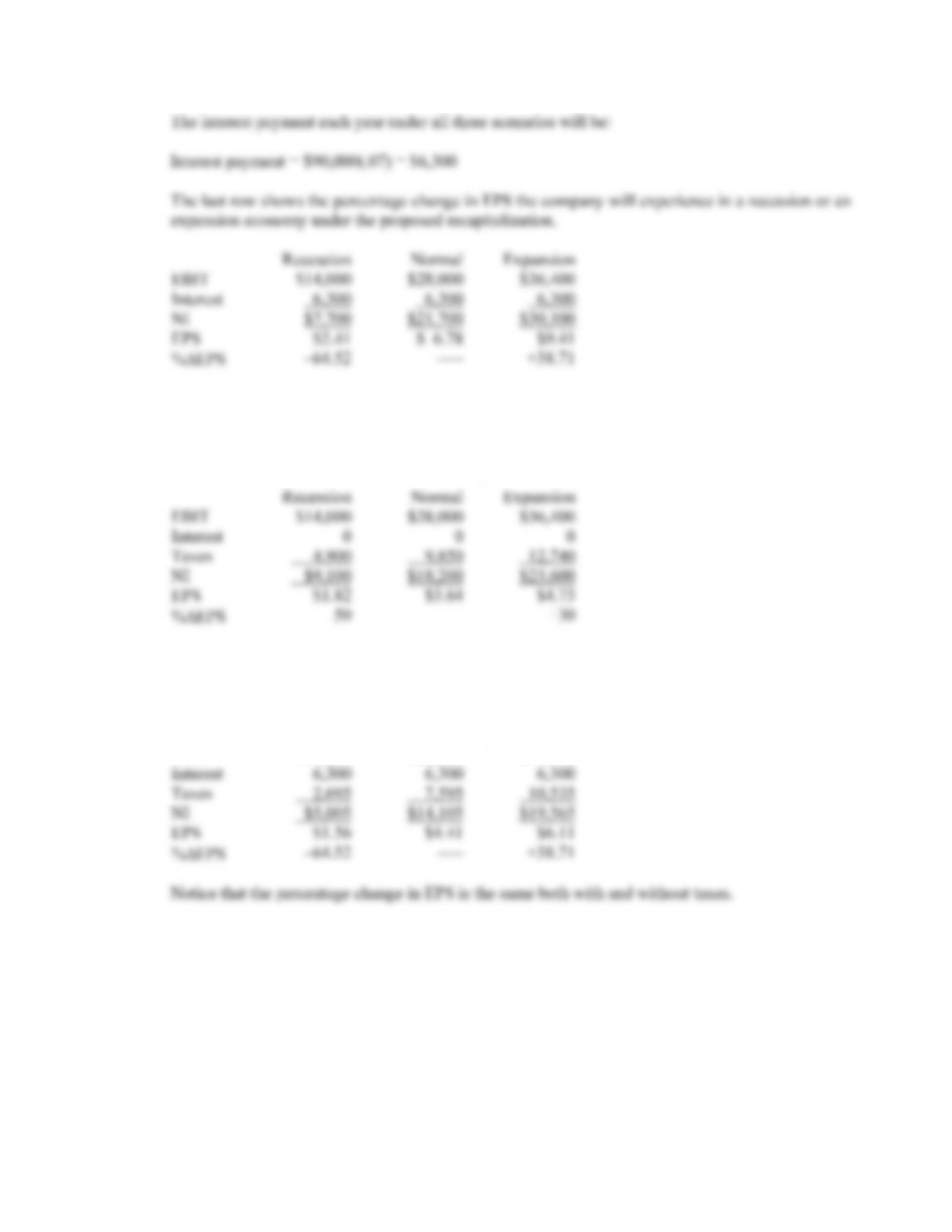

1. a. A table outlining the income statement for the three possible states of the economy is shown

below. The EPS is the net income divided by the 5,000 shares outstanding. The last row shows the

percentage change in EPS the company will experience in a recession or an expansion economy.

Recession Normal Expansion

b. If the company undergoes the proposed recapitalization, it will repurchase:

Share price = Equity / Shares outstanding

Share price = $250,000/5,000

Share price = $50

Shares repurchased = Debt issued / Share price

Shares repurchased =$90,000/$50

Shares repurchased = 1,800

B-278 SOLUTIONS

2. a. A table outlining the income statement with taxes for the three possible states of the economy is

shown below. The share price is still $50, and there are still 5,000 shares outstanding. The last row

shows the percentage change in EPS the company will experience in a recession or an expansion

economy.

b. A table outlining the income statement with taxes for the three possible states of the economy and

assuming the company undertakes the proposed capitalization is shown below. The interest

payment and shares repurchased are the same as in part b of Problem 1.

Recession Normal Expansion

EBIT $14,000 $28,000 $36,400

CHAPTER 16 B-279

3. a. Since the company has a market-to-book ratio of 1.0, the total equity of the firm is equal to the

market value of equity. Using the equation for ROE:

ROE = NI/$250,000

The ROE for each state of the economy under the current capital structure and no taxes is:

b. If the company undertakes the proposed recapitalization, the new equity value will be:

Equity = $250,000 – 90,000

Equity = $160,000

So, the ROE for each state of the economy is:

c. If there are corporate taxes and the company maintains its current capital structure, the ROE is:

ROE .0364 .0728 .0946

%ROE –50 ––– +30

If the company undertakes the proposed recapitalization, and there are corporate taxes, the ROE

4. a. Under Plan I, the unlevered company, net income is the same as EBIT with no corporate tax. The

EPS under this capitalization will be:

EPS = $350,000/160,000 shares

EPS = $2.19

B-280 SOLUTIONS

Under Plan II, the levered company, EBIT will be reduced by the interest payment. The interest

b. Under Plan I, the net income is $500,000 and the EPS is:

EPS = $500,000/160,000 shares

EPS = $3.13

Under Plan II, the net income is:

NI = $500,000 – .08($2,800,000)

c. To find the breakeven EBIT for two different capital structures, we simply set the equations for

EPS equal to each other and solve for EBIT. The breakeven EBIT is:

5. We can find the price per share by dividing the amount of debt used to repurchase shares by the number

of shares repurchased. Doing so, we find the share price is:

Share price = $2,800,000/(160,000 – 80,000)

Share price = $35.00 per share

CHAPTER 16 B-281

6. a. The income statement for each capitalization plan is:

I

I

I

All-equity

EBIT $39,000 $39,000 $39,000

Interest 16,000 24,000 0

b. The breakeven level of EBIT occurs when the capitalization plans result in the same EPS. The EPS

is calculated as:

EPS = (EBIT – RDD)/Shares outstanding

This equation calculates the interest payment (RDD) and subtracts it from the EBIT, which results

in the net income. Dividing by the shares outstanding gives us the EPS. For the all-equity capital

structure, the interest term is zero. To find the breakeven EBIT for two different capital structures,

we simply set the equations equal to each other and solve for EBIT. The breakeven EBIT between

c. Setting the equations for EPS from Plan I and Plan II equal to each other and solving for EBIT, we

get:

[EBIT – .10($160,000)]/7,000 = [EBIT – .10($240,000)]/5,000

B-282 SOLUTIONS

d. The income statement for each capitalization plan with corporate income taxes is:

I

I

I

All-equity

EBIT $39,000 $39,000 $39,000

Interest 16,000 24,000 0

Taxes 9,200 6,000 15,600

NI $ 13,800 $ 9,000 $ 23,400

EPS $ 1.97 $ 1.80 $ 2.13

The all-equity plan still has the highest EPS; Plan II still has the lowest EPS.

We can calculate the EPS as:

EPS = [(EBIT – RDD)(1 – tC)]/Shares outstanding

This is similar to the equation we used before, except now we need to account for taxes. Again, the

interest expense term is zero in the all-equity capital structure. So, the breakeven EBIT between

7. To find the value per share of the stock under each capitalization plan, we can calculate the price as the

value of shares repurchased divided by the number of shares repurchased. So, under Plan I, the value

per share is:

P = $160,000/(11,000 – 7,000 shares)

P = $40 per share

CHAPTER 16 B-283

8. a. The earnings per share are:

EPS = $32,000/8,000 shares

EPS = $4.00

b. To determine the cash flow to the shareholder, we need to determine the EPS of the firm under the

proposed capital structure. The market value of the firm is:

V = $55(8,000)

V = $440,000

Under the proposed capital structure, the firm will raise new debt in the amount of:

D = 0.35($440,000)

D = $154,000

in debt. This means the number of shares repurchased will be:

Shares repurchased = $154,000/$55

Shares repurchased = 2,800

Under the new capital structure, the company will have to make an interest payment on the new

debt. The net income with the interest payment will be:

c. To replicate the proposed capital structure, the shareholder should sell 35 percent of their shares, or

35 shares, and lend the proceeds at 8 percent. The shareholder will have an interest cash flow of:

Interest cash flow = 35($55)(.08)

Interest cash flow = $154

B-284 SOLUTIONS

The shareholder will receive dividend payments on the remaining 65 shares, so the dividends

d. The capital structure is irrelevant because shareholders can create their own leverage or unlever the

9. a. The rate of return earned will be the dividend yield. The company has debt, so it must make an

interest payment. The net income for the company is:

NI = $80,000 – .08($300,000)

NI = $56,000

The investor will receive dividends in proportion to the percentage of the company’s share they

b. To generate exactly the same cash flows in the other company, the shareholder needs to match the

capital structure of ABC. The shareholder should sell all shares in XYZ. This will net $30,000.

The shareholder should then borrow $30,000. This will create an interest cash flow of:

Interest cash flow = .08(–$30,000)

Interest cash flow = –$2,400

The investor should then use the proceeds of the stock sale and the loan to buy shares in ABC. The

investor will receive dividends in proportion to the percentage of the company’s share they own.

The total dividends received by the shareholder will be:

Dividends received = $80,000($60,000/$600,000)

c. ABC is an all equity company, so:

R

E = RA = $80,000/$600,000

R

E = .1333 or 13.33%

d. To find the WACC for each company we need to use the WACC equation:

WACC = (E/V)RE + (D/V)RD(1 – tC)

So, for ABC, the WACC is:

WACC = (1)(.1333) + (0)(.08)

10. With no taxes, the value of an unlevered firm is the interest rate divided by the unlevered cost of equity,

so:

V = EBIT/WACC

$23,000,000 = EBIT/.09