B-192 SOLUTIONS

30. Surprise! You should definitely upgrade the truck. Here’s why. At 10 mpg, the truck burns 12,000 / 10 =

1,200

Challenge

31. We will begin by calculating the aftertax salvage value of the equipment at the end of the project’s life.

The aftertax salvage value is the market value of the equipment minus any taxes paid (or refunded), so

the aftertax salvage value in four years will be:

Taxes on salvage value = (BV – MV)tC

Taxes on salvage value = ($0 – 400,000)(.38)

Taxes on salvage value = –$152,000

Market price $400,000

Tax on sale –152,000

Aftertax salvage value $248,000

Now we need to calculate the operating cash flow each year. Using the bottom up approach to

calculating operating cash flow, we find:

Year 0 Year 1 Year 2 Year 3 Year 4

Revenues $2,496,000 $3,354,000 $3,042,000 $2,184,000

Fixed costs 425,000 425,000 425,000 425,000

Variable costs 374,400 503,100 456,300 327,600

Depreciation 1,399,860 1,866,900 622,020 311,220

EBT $296,740 $559,000 $1,538,680 $1,120,180

Taxes 112,761 212,420 584,698 425,668

Net income $183,979 $346,580 $953,982 $694,512

OCF $1,583,839 $2,213,480 $1,576,002 $1,005,732

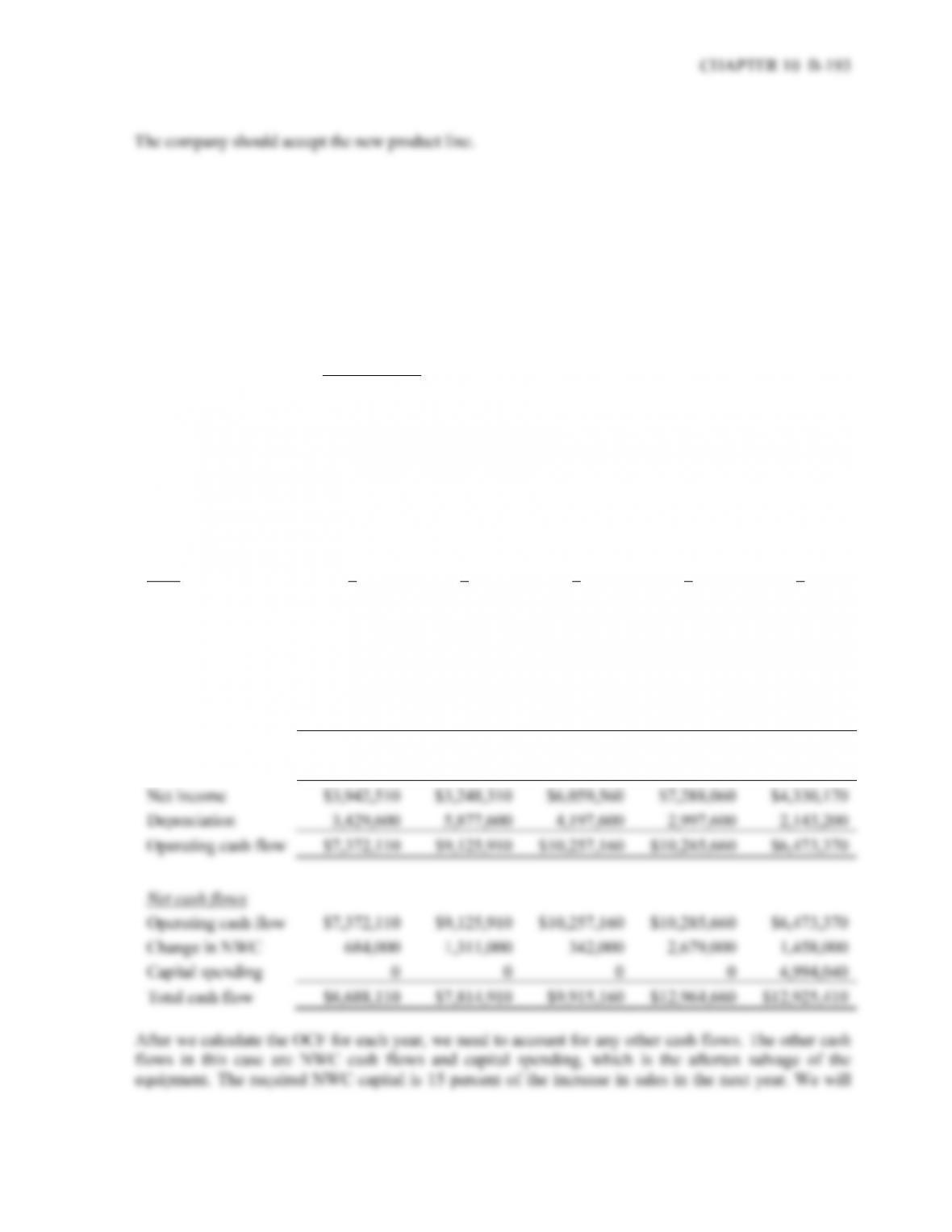

32. This is an in-depth capital budgeting problem. Probably the easiest OCF calculation for this problem is

the bottom up approach, so we will construct an income statement for each year. Beginning with the

initial cash flow at time zero, the project will require an investment in equipment. The project will also

require an investment in NWC. The initial NWC investment is given, and the subsequent NWC

investment will be 15 percent of the next year’s sales. In this case, it will be Year 1 sales. Realizing we

need Year 1 sales to calculate the required NWC capital at time 0, we find that Year 1 sales will be

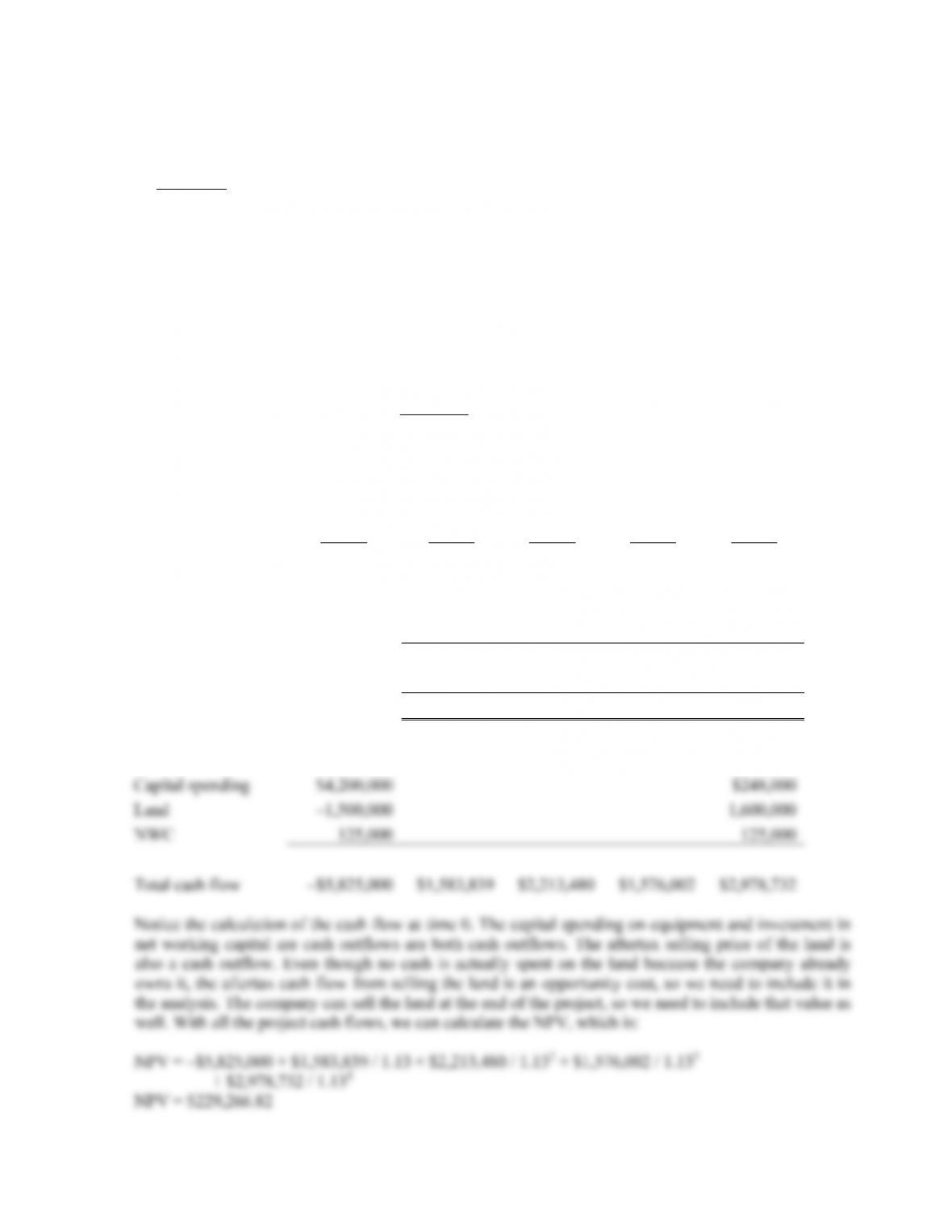

$35,340,000. So, the cash flow required for the project today will be:

Capital spending –$24,000,000

Initial NWC –1,800,000

Total cash flow –$25,800,000

Now we can begin the remaining calculations. Sales figures are given for each year, along with the price

per unit. The variable costs per unit are used to calculate total variable costs, and fixed costs are given at

$1,200,000 per year. To calculate depreciation each year, we use the initial equipment cost of $24

million, times the appropriate MACRS depreciation each year. The remainder of each income statement

is calculated below. Notice at the bottom of the income statement we added back depreciation to get the

OCF for each year. The section labeled “Net cash flows” will be discussed below:

Year 1 2 3 4 5

Ending book value $20,570,400 $14,692,800 $10,495,200 $7,497,600 $5,354,400

Sales $35,340,000 $39,900,000 $48,640,000 $50,920,000 $33,060,000

Variable costs 24,645,000 27,825,000 33,920,000 35,510,000 23,055,000

Fixed costs 1,200,000 1,200,000 1,200,000 1,200,000 1,200,000

Depreciation 3,429,600 5,877,600 4,197,600 2,997,600 2,143,200

EBIT $6,065,400 $4,997,400 $9,322,400 $11,212,400 $6,661,800

Taxes 2,122,890 1,749,090 3,262,840 3,924,340 2,331,630

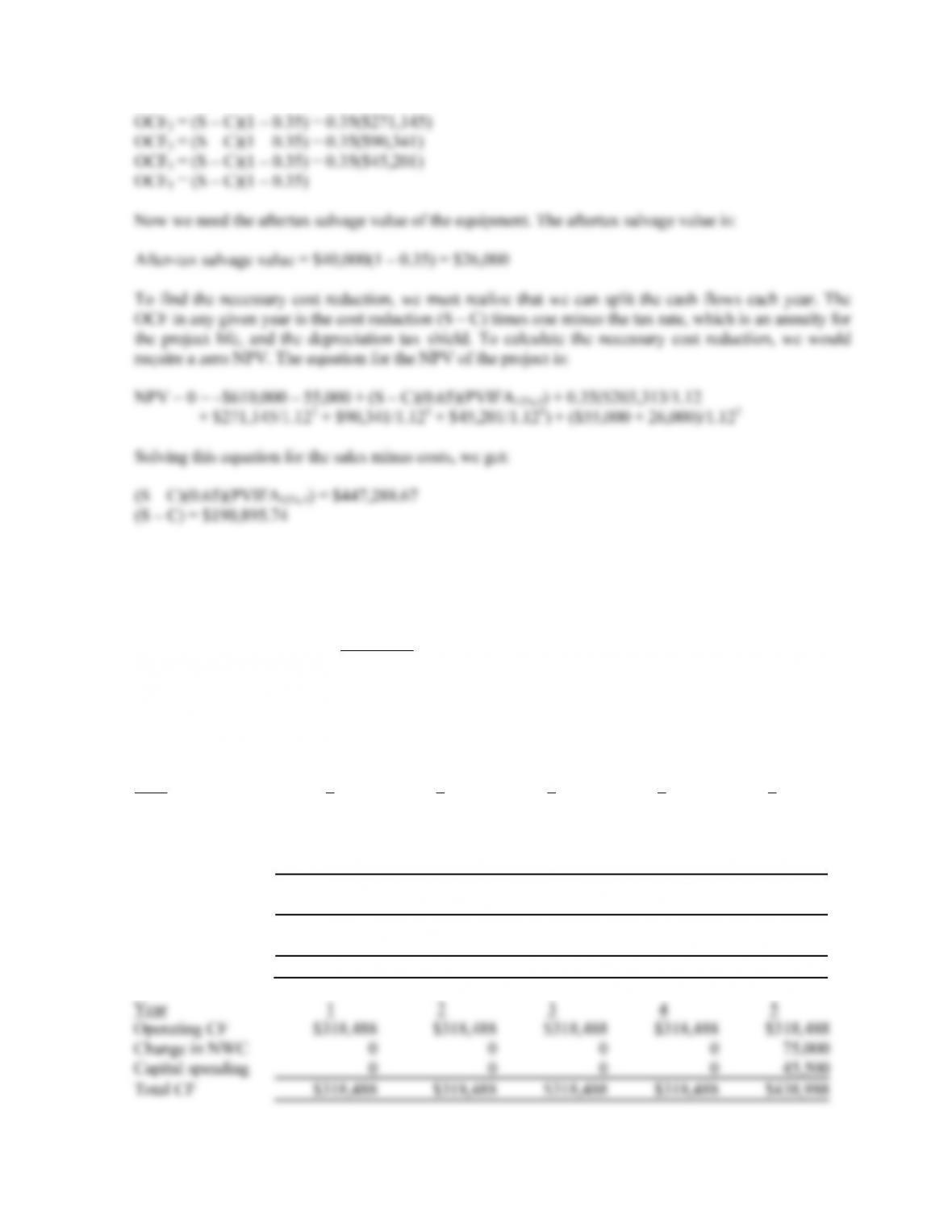

33. To find the initial pretax cost savings necessary to buy the new machine, we should use the tax shield

approach to find the OCF. We begin by calculating the depreciation each year using the MACRS

depreciation schedule. The depreciation each year is:

D

1 = $610,000(0.3333) = $203,313

D

2 = $610,000(0.4444) = $271,145

D

3 = $610,000(0.1482) = $90,341

D

4 = $610,000(0.0741) = $45,201

Using the tax shield approach, the OCF each year is:

OCF1 = (S – C)(1 – 0.35) + 0.35($203,313)

CHAPTER 10 B-195

34. a. This problem is basically the same as Problem 18, except we are given a sales price. The cash

flow at Time 0 for all three parts of this question will be:

Capital spending –$940,000

Change in NWC –75,000

Total cash flow –$1,015,000

We will use the initial cash flow and the salvage value we already found in that problem. Using the

bottom up approach to calculating the OCF, we get:

Assume price per unit = $13 and units/year = 185,000

Year 1 2 3 4 5

Sales $2,405,000 $2,405,000 $2,405,000 $2,405,000 $2,405,000

Variable costs 1,711,250 1,711,250 1,711,250 1,711,250 1,711,250

Fixed costs 305,000 305,000 305,000 305,000 305,000

Depreciation 188,000 188,000 188,000 188,000 188,000

EBIT 200,750 200,750 200,750 200,750 200,750

Taxes (35%) 70,263 70,263 70,263 70,263 70,263

Net Income 130,488 130,488 130,488 130,488 130,488

Depreciation 188,000 188,000 188,000 188,000 188,000

Operating CF $318,488 $318,488 $318,488 $318,488 $318,488

b. To find the minimum number of cartons sold to still breakeven, we need to use the tax shield approach

to calculating OCF, and solve the problem similar to finding a bid price. Using the initial cash flow and

salvage value we already calculated, the equation for a zero NPV of the project is:

NPV = 0 = –$940,000 – 75,000 + OCF(PVIFA12%,5) + [($75,000 + 45,500) / 1.125]

So, the necessary OCF for a zero NPV is:

OCF = $946,625.06 / PVIFA12%,5 = $262,603.01

Now we can use the tax shield approach to solve for the minimum quantity as follows:

CHAPTER 10 B-197

c. To find the highest level of fixed costs and still breakeven, we need to use the tax shield approach to

calculating OCF, and solve the problem similar to finding a bid price. Using the initial cash flow and

salvage value we already calculated, the equation for a zero NPV of the project is:

NPV = 0 = –$940,000 – 75,000 + OCF(PVIFA12%,5) + [($75,000 + 45,500) / 1.125]

OCF = $946,625.06 / PVIFA12%,5 = $262,603.01

Notice this is the same OCF we calculated in part b. Now we can use the tax shield approach to solve

for the maximum level of fixed costs as follows:

OCF = $262,603.01 = [(P–v)Q – FC ](1 – tC) + tCD

$262,603.01 = [($13.00 – 9.25)(185,000) – FC](1 – 0.35) + 0.35($940,000/5)

FC = $390,976.15

35. We need to find the bid price for a project, but the project has extra cash flows. Since we don’t already

produce the keyboard, the sales of the keyboard outside the contract are relevant cash flows. Since we

know the extra sales number and price, we can calculate the cash flows generated by these sales. The

cash flow generated from the sale of the keyboard outside the contract is:

1 2 3 4

Sales $855,000 $1,710,000 $2,280,000 $1,425,000

Variable costs 525,000 1,050,000 1,400,000 875,000

EBT $330,000 $660,000 $880,000 $550,000

Tax 132,000 264,000 352,000 220,000

Net income (and OCF) $198,000 $396,000 $528,000 $330,000

B-198 SOLUTIONS

36. a. Since the two computers have unequal lives, the correct method to analyze the decision is the

EAC. We will begin with the EAC of the new computer. Using the depreciation tax shield

approach, the OCF for the new computer system is:

OCF = ($145,000)(1 – .38) + ($780,000 / 5)(.38) = $149,180

Notice that the costs are positive, which represents a cash inflow. The costs are positive in this

case since the new computer will generate a cost savings. The only initial cash flow for the new

computer is cost of $780,000. We next need to calculate the aftertax salvage value, which is:

Aftertax salvage value = $150,000(1 – .38) = $93,000

Now we can calculate the NPV of the new computer as:

NPV = –$780,000 + $149,180(PVIFA12%,5) + $93,000 / 1.125

CHAPTER 10 B-199

NPV = –$189,468.79

And the EAC of the new computer is:

EAC = –$189,468.79 / (PVIFA12%,5) = –$52,560.49

Analyzing the old computer, the only OCF is the depreciation tax shield, so:

OCF = $130,000(.38) = $49,400

B-200 SOLUTIONS

b. If we are only concerned with whether or not to replace the machine now, and are not worrying

about what will happen in two years, the correct analysis is NPV. To calculate the NPV of the

decision on the computer system now, we need the difference in the total cash flows of the old

computer system and the new computer system. From our previous calculations, we can say the

cash flows for each computer system are:

t New computer Old computer Difference

0 –$780,000 –$377,200 –$402,800

1 149,180 49,400 99,780

2 149,180 136,000 13,180

3 149,180 0 149,180

4 149,180 0 149,180

5 242,180 0 242,180