Solutions to end–of–chapter problems

Engineering Economy, 7th edition

Leland Blank and Anthony Tarquin

Chapter 15

Cost Estimation

15.2 Supplies: AOC Installation: FC

15.3 Calculate taxes (A), make bids (E), pay bonuses (A), determine profit or loss (A),

15.5 Project staff (D), Audit and legal (I), Utilities (I), Rent (I), Raw materials (D), Equipment

15.6 License plate (indirect), Drivers license (indirect), Gasoline (direct), Highway

toll fee (indirect, since it is usually an option to choose a non-toll route), Oil change

2

15.15 (a) Crew cost per day = 8[25.85 + 28.60 + 5(23.25) + 31.45] = $1617.20

15.16 (a) Cost = 120(21.31 + 5.00) = $3157

15.17 Cost in Texas = 10,500(800)(0.769)

15.18 From Table 15-3, index value in 2001 = 6343; index value in mid-2010 = 8837

15.19 To have index value of 100 in year 2000, must divide by 62.21.

15.20 (a) First find the compounded percentage increase p between 1995 and 2005.

7446 = 5471 (F/P,p,10)

3

15.21 At 1% per month, annual increase = (1 + 0.01)12 -1 = 12.68%

15.22 Let f = inflation rate

(a) f = (8837.38 – 8563.35)/8563.35 = 0.032

15.23 Cost = 194(1461.3/789.6)

15.26 96.55 = (Cost in 1913)(2708.51/100)

15.27 (a) 40,000 = 21,771(F/P,2.68%,n)

15.29 (a) Cost = 28,000[(125/200)0.69

4

15.30 C2 = 13,000(500/4)0.37

15.32 Use the six-tenths model; exponent = 0.60

15.33 1.52C1 = C1(68/30)x

15.34 Area of 12” pipe = π(1)2/4

15.35 Use Equation [15.4] and Table 15-3

15.37 Let C1 = cost in 1998; From Table 15-3, M & S index values are 1061.9 in

15.38 C2 = 0.942C1 = C1(2)x

5

15.42 First find direct cost; then multiply by indirect cost factor:

h = 1 + 1.28 + 0.23 = 2.51

15.44 CT = [400,000(1 + 3.1)][1 + 0.38]

15.45 (a) h = 1 + 0.30 + 0.30 = 1.60

Let x be the indirect cost factor

CT = 430,000 = [250,000 (1.60)] (1 + x)

15.46 Total direct labor hours = 2000 + 8000 + 5000

6

15.47 (a) North: Miles basis; rate = 300,000/350,000 = 0.857 per mile

South: Labor basis; rate = 200,000/20,000 = $10 per hour

15.48 Rate for CC100 = 25,000/800 = $31.25 per hour

15.49 (a) From Equation [15.8], estimated basis level = total costs allocated/rate

Month Basis Level Basis__________

February 2800/1.40 = 2000 Space

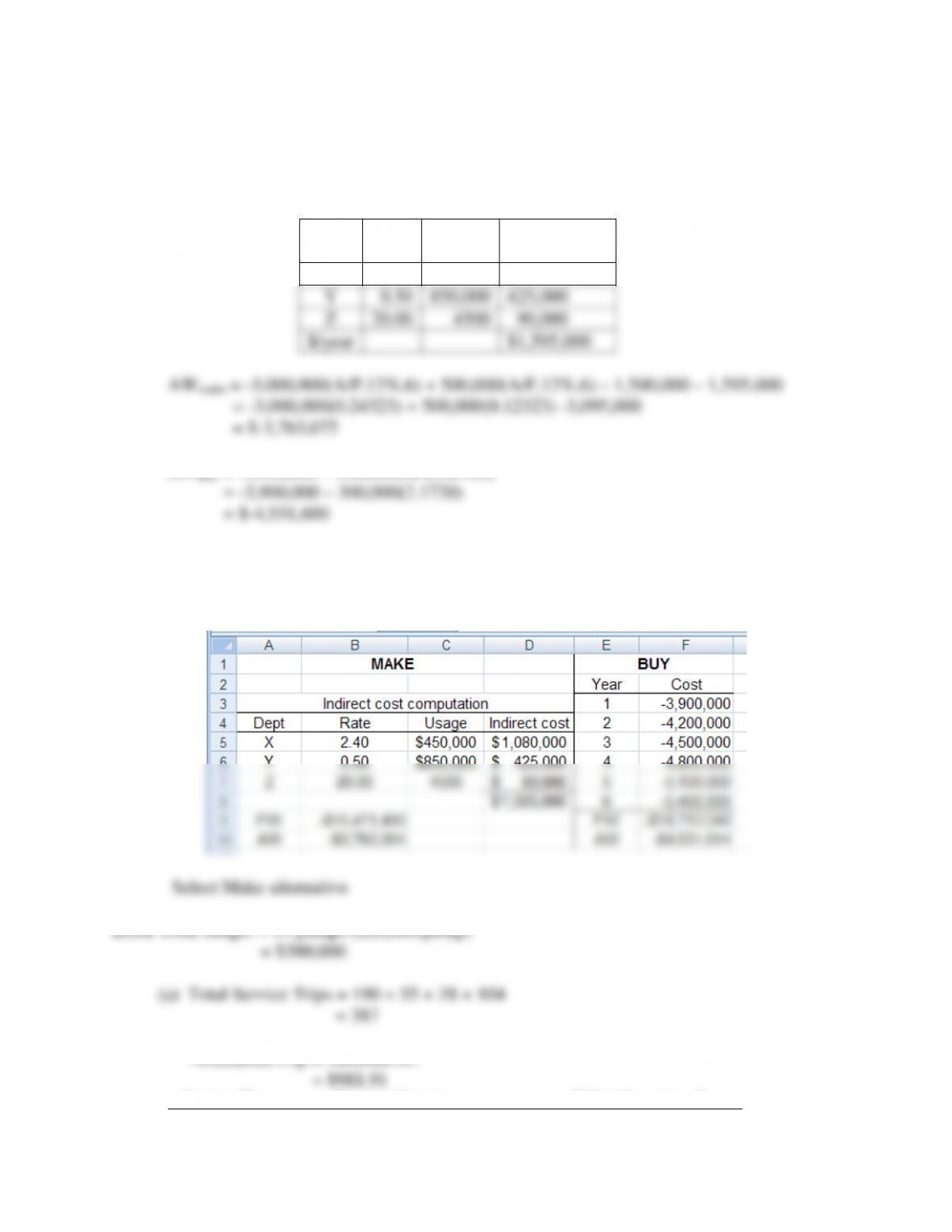

15.50 Determine AW for Make and Buy alternatives. Make has annual indirect costs.

7

Hand solution:

Make: Indirect cost computation

Dept

Rate

(1)

Usage

(2)

Annual cost

(3) = (1)(2)

X

$2.40

450,000

$1.08 million

Y

0.50

850,000

425,000

Z

20.00

4500

90,000

$/year

$1,595,000

AWbuy = -3,900,000 – 300,000(A/G,12%,6)

Select Make alternative

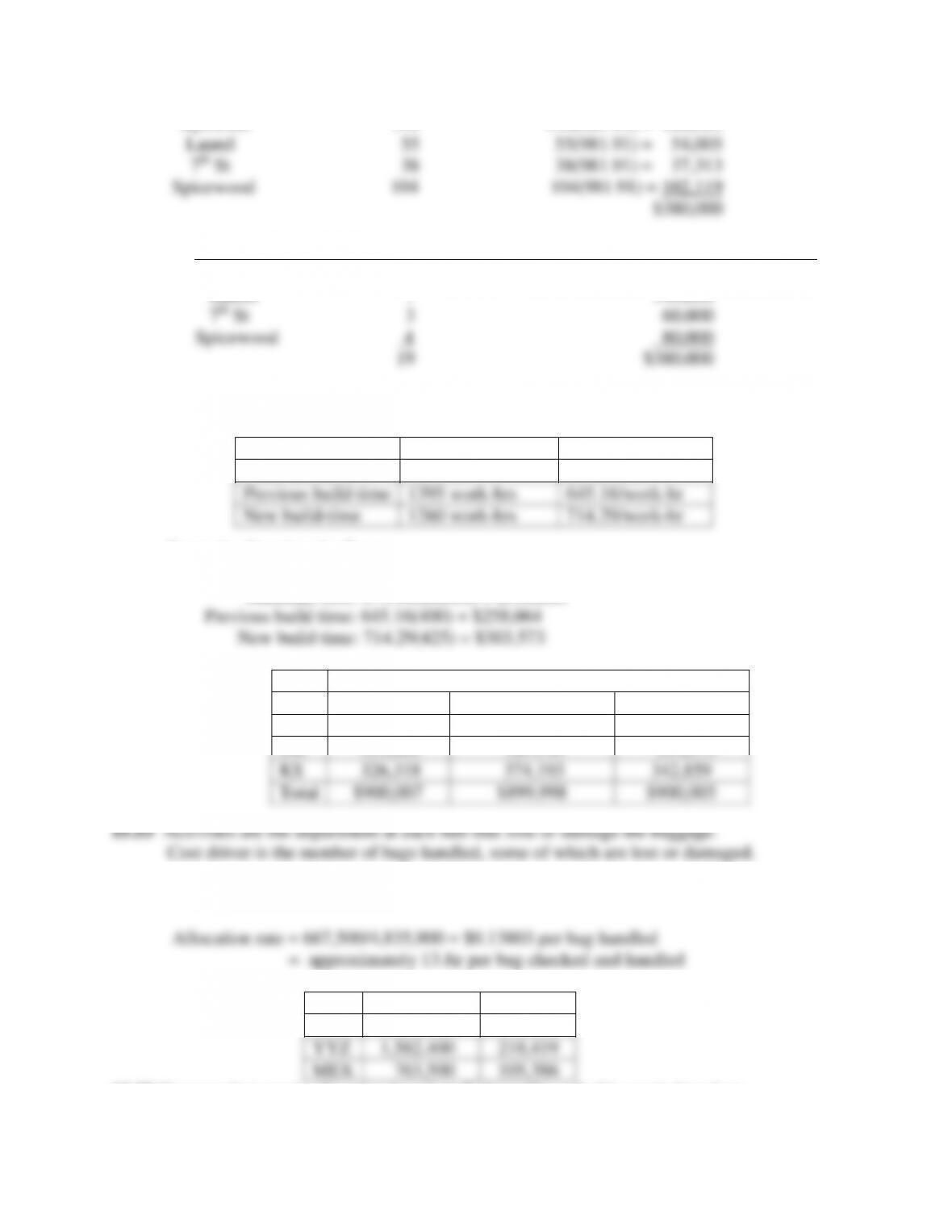

Spreadsheet solution:

Station ID Service Trips/year IDC Allocation, $____

8

Sylvester 190 190(981.91) = 186,563

(b) Station ID Number of pumps Allocation at $20,000/pump____

Sylvester 5 100,000

Laurel 7 140,000

15.52 Determine the rates by basis, then distribute the $900,000.

Previous build-time

1395 work-hrs

645.16/work-hr

New build–time

1260 work-hrs

714.29/work-hr

Example allocation for Texas:

Materials cost: 17.544(20,000) = $350,880

Allocation by each basis

Materials cost

Previous build-time

New build–time

TX

$350,880

$258,064

$303,573

OK

222,809

267,741

253,573

KS

326,318

374,193

342,859

Total

$900,007

$899,998

$900,005

15.54 Total bags handled = 4,835,900

Bags handled

Allocation

DFW

2,490,000

$343,695

YYZ

1,582,400

218,419

MEX

763,500

105,386

15.55 Compare last year’s allocation based on flight traffic with this year’s based on

Total usage

Rate

Materials cost

$51,300

$17.544/$

9

baggage traffic. Significant change took place, especially at MEX.

15.56 (a) Rate = $1 million/16,500 guests = $60.61 per guest

Charge = number of guests × rate

Site_____________

A B C D

Guests 3500 4000 8000 1000

Site_________________

A B C D__

15.60 Cost = 2100(200/50)0.76

15.61 Cost = 500,000(5542.16/3378.17)

15.62 Cost = 3000(500/250)0.32(1449.3/1061.9)

Last year;

flight basis

This year;

baggage basis

Percent

change

DFW

$330,000

$343,695

+ 4.15%

YYZ

187,500

218,419

+16.5

150,000

105,386

-29.7

10

15.63 3,000,000 = 550,000(100,000/6000)x

15.64 CT = 2.96(390,000) = $1,154,400

15.65 CT = (1 + 1.82 + 0.31)(650,000)

15.67 Allocation = (900 + 1300)(2000) = $4.4 million

11

Solution to First Case Study, Chapter 15

There is not always a definitive answer to case study exercises. Here are example responses

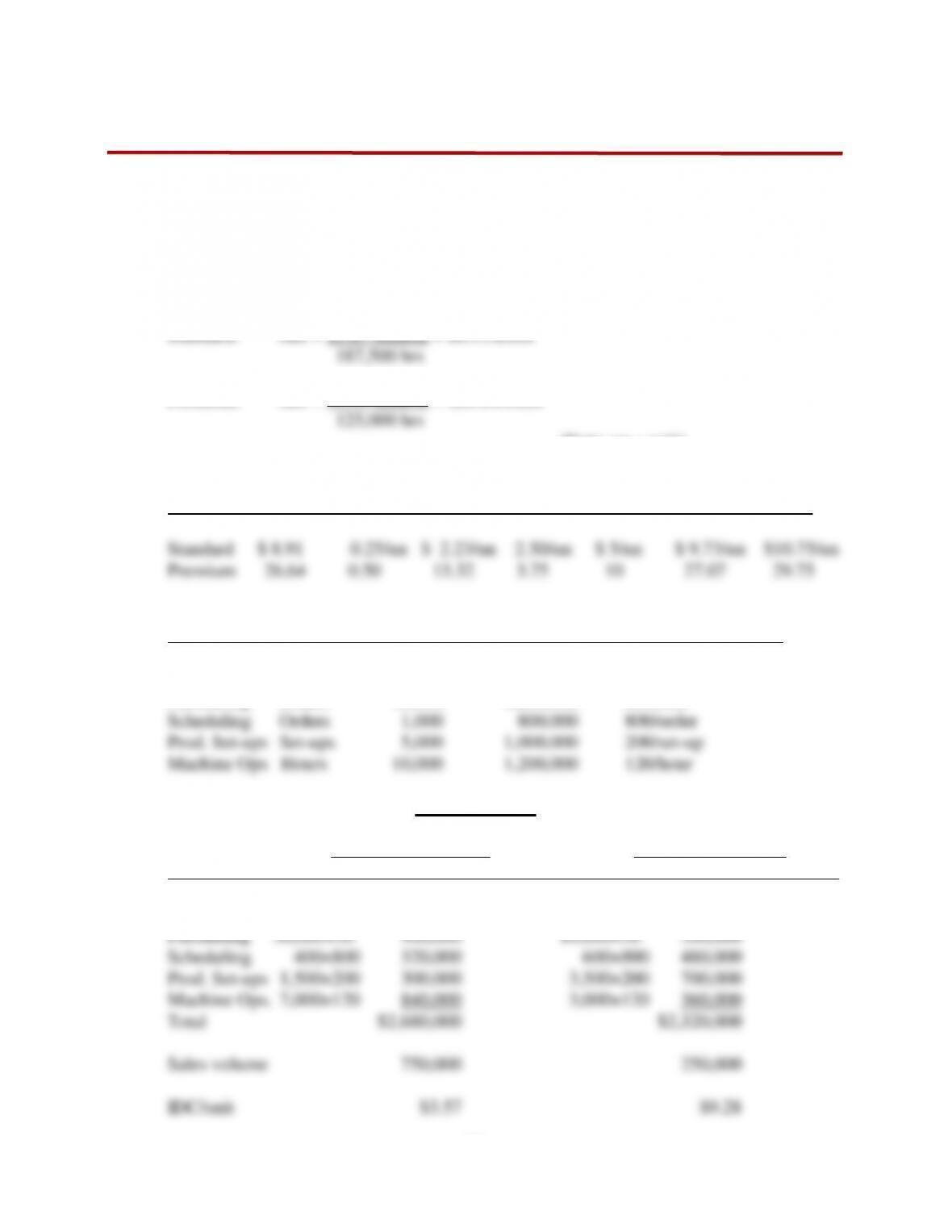

INDIRECT COST ANALYSIS OF MEDICAL EQUIPMENT

MANUFACTURING COSTS

1. DLH basis

Standard: rate = $1.67 million = $8.91/DLH

Premium: rate = $3.33 million = $26.64/DLH

(Note: un = unit)

Price,

IDC DLH IDC Direct Direct Total ~1.10 ×

Model rate hours allocation material Labor cost cost__

2. Cost Volume Total ABC

Activity Driver of driver cost/year IDC rate

Quality Inspections 20,000 $800,000 $40/inspection

Purchasing Orders 40,000 1,200,000 30/order

ABC allocation

_____Standard__________ ________Premium_________

Driver Volume×rate IDC allocation Volume×rate IDC allocation

Quality 8,000×40 $320,000 12,000×40 $480,000

12

Direct Direct IDC Total

Model material labor allocation cost

3. Traditional

Model Profit/unit Volume Profit__

Standard 10.75 – 9.73 = $1.02 750,000 $765,000

ABC

4. Price at Cost + 10%

Model Cost Price Profit/unit Volume Profit___

5. a) Prediction about IDC allocation – The manager was right on IDC allocation under

ABC, but totally wrong on traditional where the cost is ~ 1/3 and IDC is ~1/6.

_______Allocation__________

Model Traditional ABC___

13

c) Premium require more activities and operations comment

Wrong : Premium model is lower in cost driver volume for purchase orders and