The primary function of external auditors is to:

A. Express an opinion on the fairness of the company’s financial statements.

B. Determine the accuracy of the management reports.

C. Evaluate the efficiency of operations and the degree of compliance with

management’s policies in all departments within a large organization.

D. Determine that financial statements and all special reports to management are

prepared in conformity with generally accepted accounting principles.

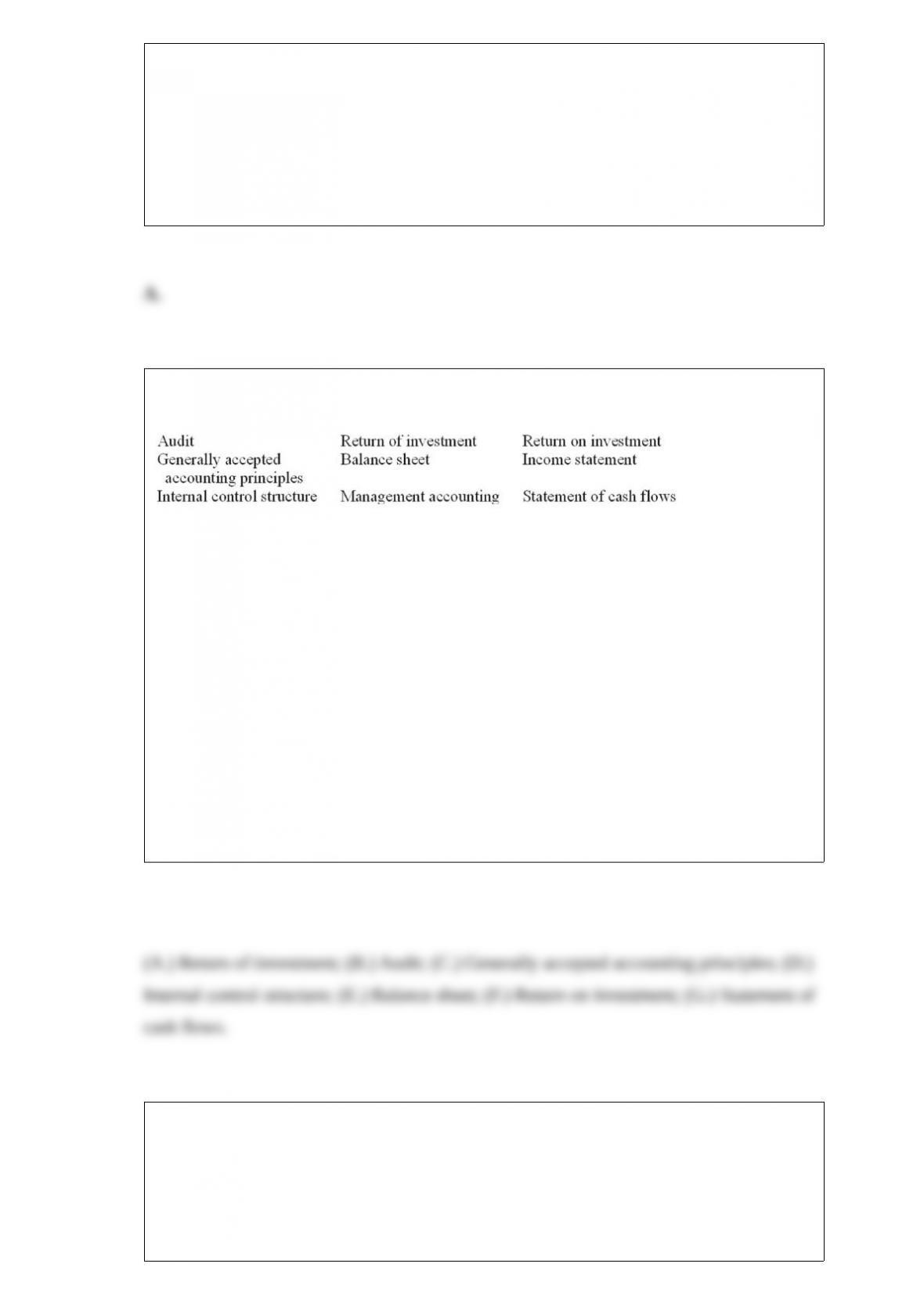

Accounting terminology

Listed below are nine accounting terms introduced in this chapter:

Each of the following statements may (or may not) describe one of these terms. In the

space provided below each statement, indicate the accounting term described, or answer

“None” if the statement does not correctly describe any of the terms. More than one

statement may describe a single term.

(A.) The repayment to an investor of the amount originally invested in an enterprise.

(B.) An examination of financial statements designed to determine their fairness in

relation to generally accepted accounting principles.

(C.) The accounting standards and concepts used in the preparation of financial

statements.

(D.) A system of measures designed to assure management that all aspects of the

business are operating according to plan.

(E.) A listing of assets, liabilities, and stockholders’ equity as of a specific date.

(F.) The payment of an amount for using another’s money.

(G.) An activity statement that shows the details of the company’s activities involving

cash during a period of time.

In the phrase “generally accepted accounting principles,” the words generally accepted

mean that the principles:

A. Have been adopted by Congress or approved by the voters in a general election.

B. Are acceptable to the Internal Revenue Service.

C. Are understood and observed by all the participants in the financial reporting

process.

D. Have been approved by a majority of the members of the Financial Accounting

Standards Board.

In a statement of cash flows, cash transactions are classified into three major categories.

Which of the following is not one of these three categories?

A. Managing activities.

B. Operating activities.

C. Financing activities.

D. Investing activities.

Refer to the information above. Assume that the Equipment shown above was acquired

by the business five years ago and has a book value of $156,000, but has a current

appraised value of $200,000. Hercules Manufacturing’s Retained Earnings at December

31, 2014, amounts to:

A. $533,000.

B. $345,000.

C. $198,000.

D. $356,000.

Cash ($7,000) + A/R ($30,000) + Land ($90,000) + Building ($250,000) + Equipment

($156,000) = $533,000

A/P ($12,000) + N/P ($135,000) + Capital Stock ($188,000) + R.E.(?) = $533,000

Cumberland, Inc. has applied to its bank for a loan. The bank asks Cumberland’s

controller about the total amount of the company’s accounts receivable. Assuming that

all accounting records are up-to-date, the controller can best answer this question by

referring to:

A. The Income Statement.

B. The Accounts Receivable control account.

C. The Accounts Receivable subsidiary ledger.

D. Last year’s Balance Sheet.

To arrive at net sales:

A. Add sales discounts to sales.

B. Subtract the cost of goods sold from the sales price.

C. Subtract sales returns and sales discounts from sales.

D. Subtract accounts receivable from sales.

Characteristics of internal accounting information include all of the following except:

A. It is audited by a CPA.

B. It must be timely.

C. It is oriented toward the future.

D. It measures efficiency and effectiveness.

Standard costs:

A. May be used in job order cost systems but not in process cost accounting systems.

B. Should be revised upward when actual costs are higher than expected because of

waste and inefficiency.

C. Are the same for all companies in a given industry.

D. Are the costs that should be incurred to produce a product under normal conditions.

The set of linked activities and resources needed to create and deliver a product or

service to the customer is referred to as:

A. The budget.

B. The value chain.

C. The operating cycle.

D. The production process.

Pet Foods Plus purchased bagged dog food at an invoice price of $6,000 and terms of

2/10, n/30. Half of the bags had been damaged in shipment and delivery was refused. If

Pet Foods Plus pays the remaining amount of the invoice within the discount period, the

amount paid should be:

A. $2,940.

B. $3,000.

C. $5,880.

D. $6,000.

The Social Security tax paid by an employer is:

A. Greater than the amount paid by the employee.

B. Less than the amount paid by the employee.

C. Equal to the amount paid by the employee.

D. The employer does not pay Social Security tax, only the employee pays the tax.

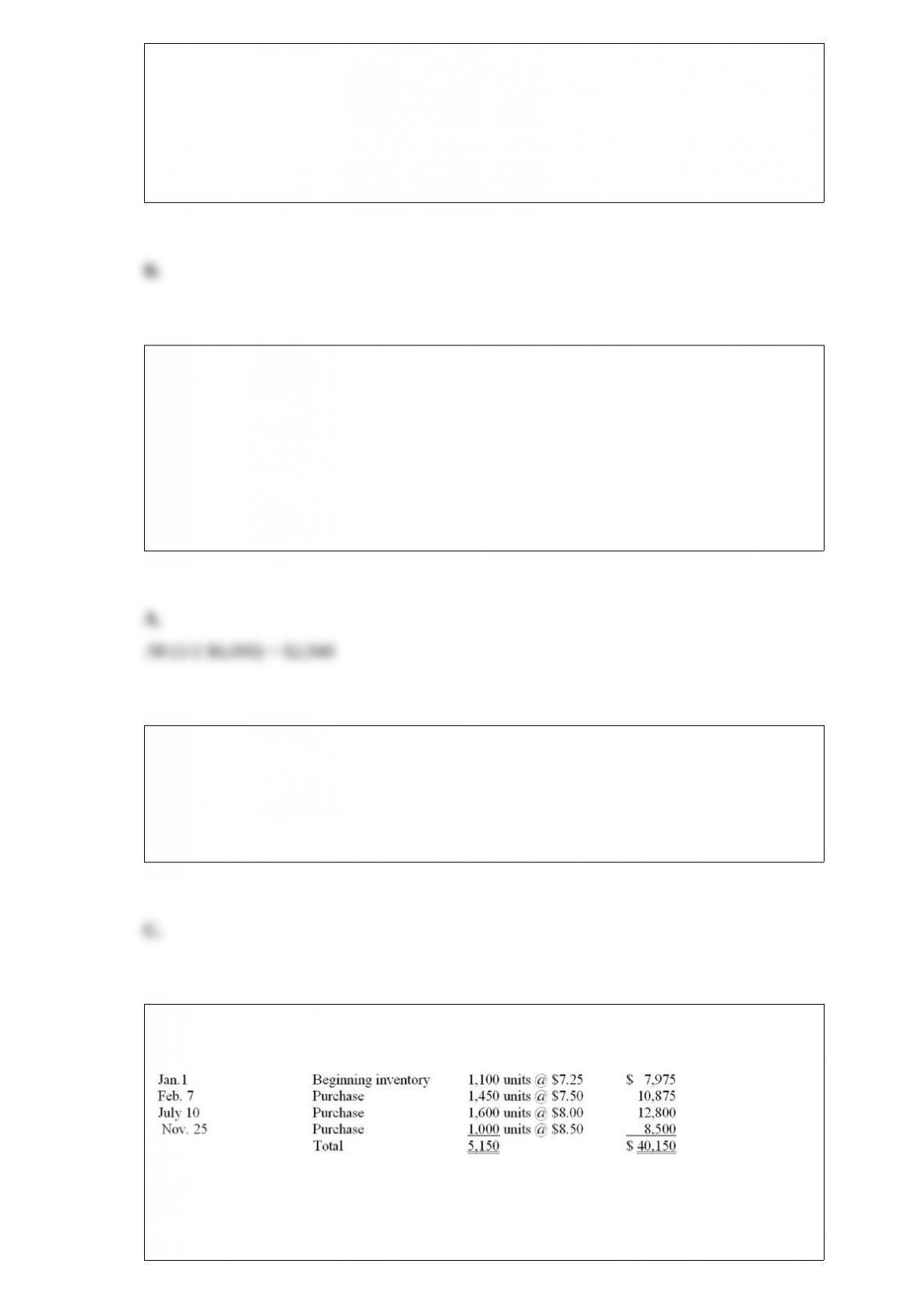

Harding Systems, Inc. uses a periodic inventory system. The purchases of a particular

product during the year are shown below:

At December 31 the ending inventory consisted of 1,500 units.

Refer to the information above. Compute the cost of the ending inventory based on the

average-cost method of inventory valuation. (Round your final answer to the nearest

dollar value.)

A. $14,512.

B. $11,694.

C. $29,560.

D. $28,450.

On October 1, 2015, Master’s Co. borrows $500,000 from its bank for five years at an

annual interest rate of 10%. According to the terms of the loan, the principal amount

will not be due for five years. Interest is to be paid monthly on the first day of each

month, beginning November 1, 2015. With respect to this borrowing, Master’s

December 31, 2015, balance sheet included only a long-term note payable of $500,000.

As a result:

A. The December 31, 2015, financial statements are accurate.

B. Liabilities are understated by $12,500 accrued interest payable.

C. Liabilities are understated by $4,167 accrued interest payable.

D. Liabilities are understated by the amount of interest for the five-year term of the note

that has not yet been paid.

In establishing standard costs for labor, management must look at all of the following

except:

A. Time allowed to produce each product.

B. Direct labor requirements for each product.

C. The wage rate of a direct laborer.

D. The quantity of materials for each product.

The amortization of a bond premium:

A. Decreases the carrying value of a bond and increases interest expense.

B. Decreases the carrying value of a bond and decreases interest expense.

C. Increases the carrying value of a bond and increases interest expense.

D. Increases the carrying value of a bond and decreases interest expense.

At the beginning of 2015, England Dresses has an inventory of $140,000. However,

management wants to reduce the amount of inventory on hand to $80,000 at December

31. If net sales for 2015 are forecast at $400,000 and the gross profit rate is expected to

be 40%, compute the cost of the merchandise which management should expect to

purchase during 2015. (Hint: First compute the expected cost of goods sold.)

A. $240,000.

B. $180,000.

C. $320,000.

D. $220,000.

All of the following statements are true regarding the Income Statement except?

A. The Income Statement may also be called the Earnings Statement.

B. The measurement of income is not absolutely accurate or precise due to assumptions

and estimates.

C. The Income Statement only includes those events that have been evidenced by actual

business transactions.

D. The net income (or net loss) appears at the bottom of the Income Statement and also

in the company’s year-end balance sheet.

An investment’s annual net cash flow will always be equal to its:

A. Annual revenue less its annual expenses.

B. Annual cash receipts less its annual cash disbursements.

C. Annual revenue less its annual cash disbursements.

D. Annual net income plus its annual depreciation expense.

A large unanticipated reduction in the property taxes on a company’s factory would, all

other things equal, most likely cause:

A. A favorable overhead spending variance.

B. An unfavorable overhead spending variance.

C. A favorable overhead volume variance.

D. An unfavorable overhead volume variance.

A strong statement of cash flows indicates that significant cash is being generated by:

A. Operating activities.

B. Financing activities.

C. Investing activities.

D. Effective tax planning.

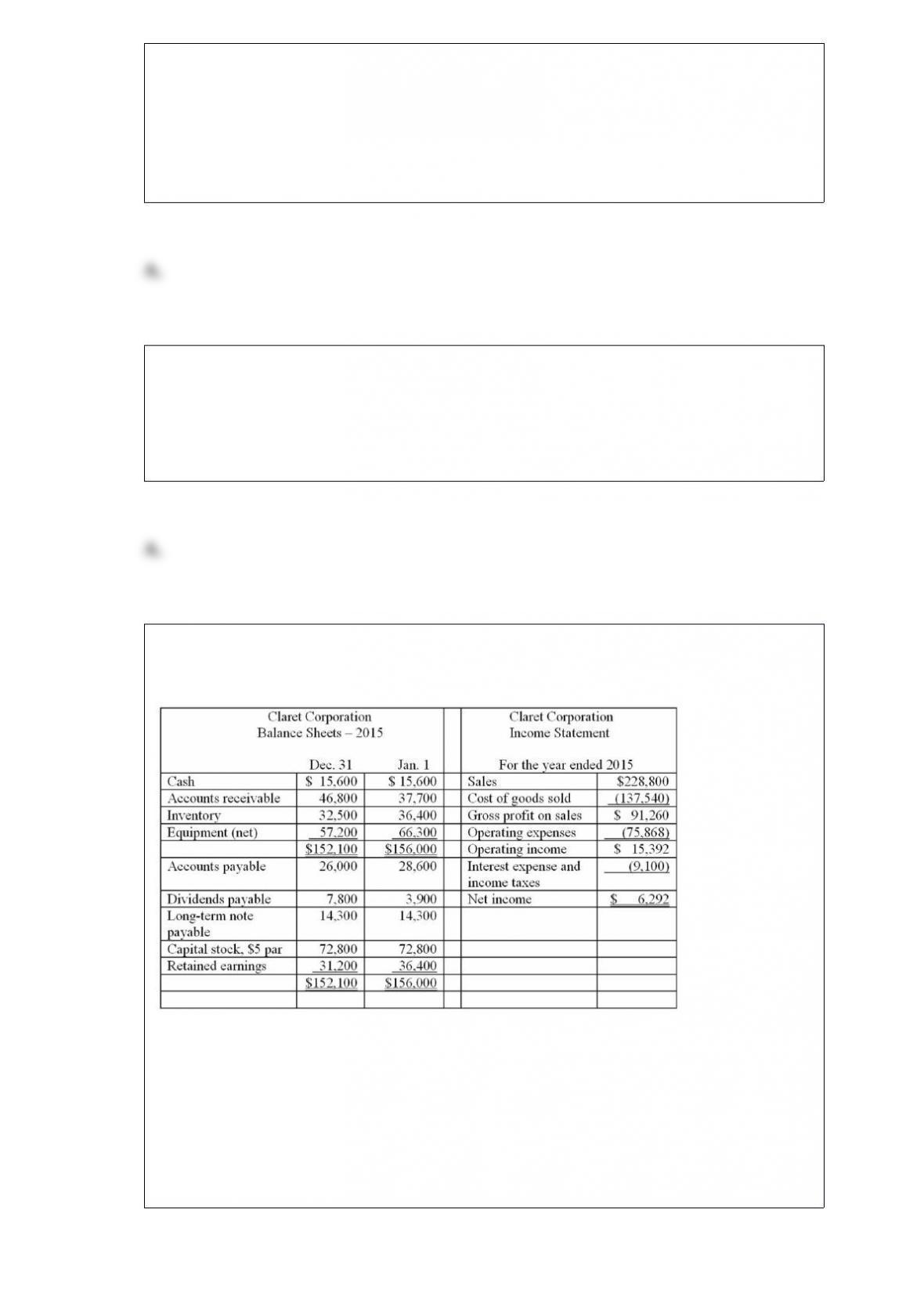

Given below are comparative balance sheets and an income statement for Claret

Corporation.

All sales were made on account. Cash dividends declared during the year totaled

$11,492.

Refer to the information above. Claret Corporation’s accounts receivable turnover for

2015 is:

A. 4.6 times.

B. 2.9 times.

C. 5.4 times.

D. 68 days.

Which of the following is not an important factor in ensuring the integrity of accounting

information?

A. Institutional factors, such as standards for preparing information.

B. Professional organizations, such as the American Institute of CPAs.

C. Competence, judgment, and ethical behavior of individual accountants.

D. The cost of preparing the financial information.

The purchase of equipment on credit is recorded by a:

A. Debit to Equipment and a credit to Accounts Payable.

B. Debit to Accounts Payable and a credit to Equipment.

C. Debit to Equipment and a debit to Accounts Payable.

D. Credit to Equipment and a credit to Accounts Payable.

The interest coverage ratio is computed by dividing:

A. Net income by interest expense.

B. Operating income by interest expense.

C. Interest expense by net income.

D. Interest expense by operating income.

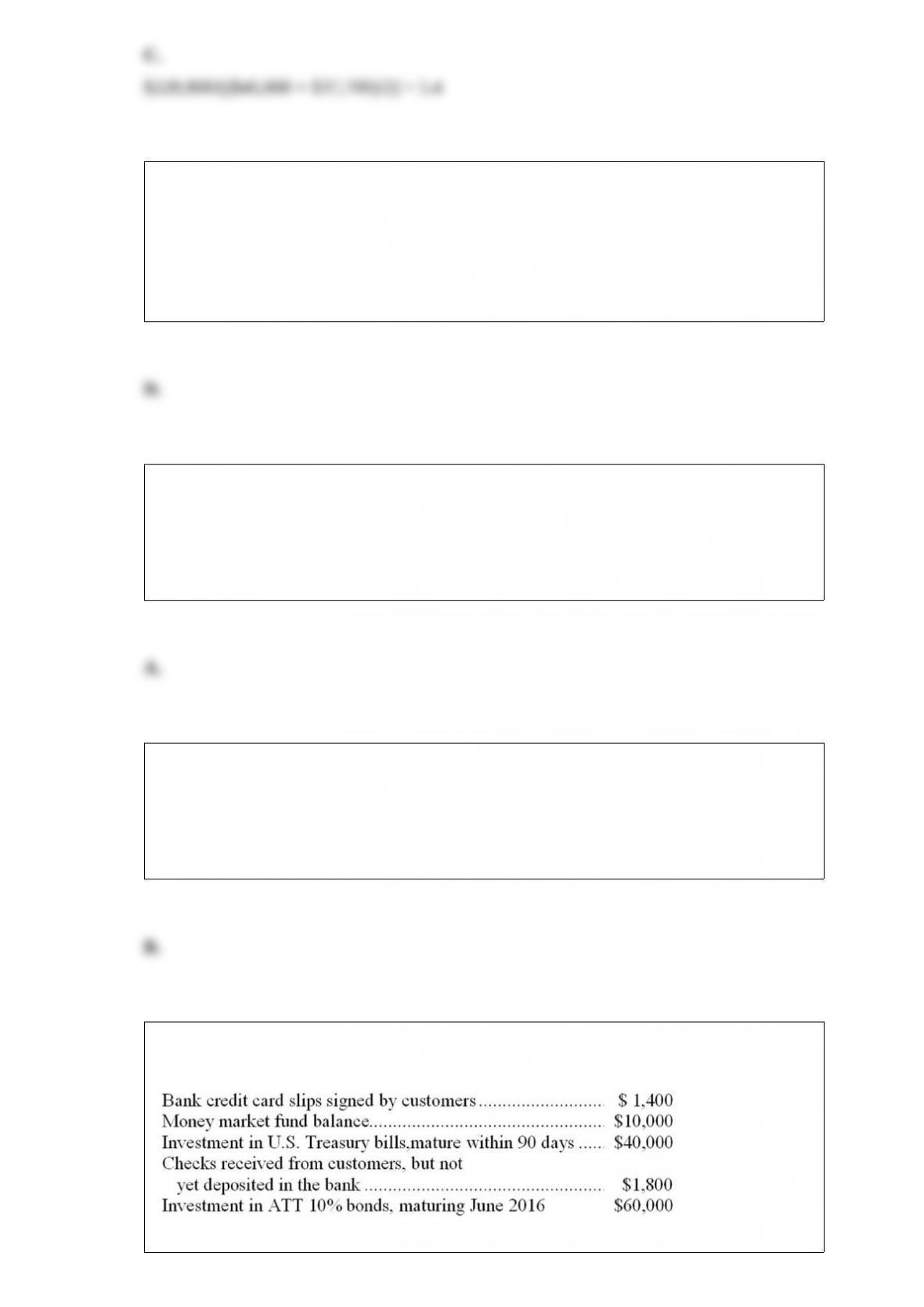

As of December 31, 2015, Valley Company has $16,920 cash in its checking account,

as well as several other items listed below:

What amount should be shown in Valley’s December 31, 2015, balance sheet as “Cash

and cash equivalents”?

A. $53,200.

B. $70,120.

C. $130,120.

D. $113,200.