An auditor vouched data for a sample of employees in a payroll register to approved

clock card/time sheet data to provide assurance that

A. payments to employees are computed at authorized rates.

B. employees worked the number of hours for which they are paid.

C. segregation of duties exists between the preparation and distribution of the payroll.

D. internal controls relating to unclaimed payroll checks are operating effectively.

The cashier of Brooke Company covered a shortage in the cash working fund with cash

obtained on December 31 from a local bank by cashing, but not recording, a check

drawn on the company’s out-of-town bank. How would the auditor discover this

manipulation?

A. Confirming all December 31 bank balances.

B. Counting the cash working fund at the close of business on December 31.

C. Preparing independent bank reconciliations as of December 31.

D. Preparing and detail testing a bank transfer schedule.

It is important for the CPA to consider the competence of the entity’s employees

because their competence bears directly and importantly upon the

A. Cost/benefit relationship of the system of internal control.

B. Achievement of the objectives of the system of internal control.

C. Comparison of recorded accountability with assets.

D. Timing of the tests to be performed.

Audit documents record the results of the auditor’s evidence-gathering procedures.

When preparing audit documents, the auditor should remember that

A. Audit documents should be kept on the client’s premises so that the client can have

access to them for reference purposes.

B. Audit documents should be the primary support for the financial statements being

examined.

C. Audit documents should be considered as a substitute for the company’s accounting

records.

D. Audit documents should be designed to facilitate the review and supervision of work

done by auditors assigned to the engagement.

During a review of a small business entity’s internal control system, the auditor

discovered that the accounts receivable clerk approves credit memos and has access to

cash. Which of the following controls would be most effective in offsetting this

weakness?

A. The owner reviews errors in billings to customers and postings to the subsidiary

ledger.

B. A controller receives the monthly bank statement directly and reconciles the

checking accounts.

C. The owner reviews credit memos before they are recorded.

D. The controller reconciles the total of the detailed accounts receivable accounts to the

amount shown in the ledger.

When examining payroll transactions, an auditor is primarily concerned with the

possibility of

A. underpayments and properly authorized payments.

B. posting of gross payroll amounts to incorrect salary expense accounts.

C. misfootings of employee time records.

D. excess withholding of amounts required to be withheld.

Which of the following best describes the role of corporate governance?

A. Management decides which accounting principles are the most appropriate.

B. Shareholders vote to decide who should be members of the board of directors.

C. Holding the management team accountable to shareholders and other constituents for

the utilization of the entity’s resources.

D. Management often is compensated based on the company’s profitability.

The documentation of an auditor’s understanding of internal controls

A. Is optional.

B. Must be exclusively in narrative, questionnaires, or flowchart form.

C. Must include flowcharts.

D. Can include any combination of narratives, questionnaires, or flowcharts.

An auditor most likely would assess control risk at high if the payroll department

supervisor is responsible for

A. examining authorization forms for new employees.

B. comparing payroll registers with original batch transmittal data.

C. authorizing payroll rate changes for all employees.

D. hiring all subordinate payroll department employees.

Which of the following might be detected by an auditor’s review of the entity’s sales

cutoff?

A. Excessive goods returned for credit.

B. Unrecorded sales discounts.

C. Lapping of year-end accounts receivable.

D. Overstated sales for the year.

An unrecorded check issued during the last week of the year would most likely be

discovered by the auditor when the

A. check register for the last month is reviewed.

B. cutoff bank statement is reconciled.

C. bank confirmation is reviewed.

D. search for unrecorded liabilities is performed.

While observing an entity’s annual physical inventory, an auditor recorded test counts

for several items and noticed that certain test counts were higher than the recorded

quantities in the entity’s perpetual records. This situation could be the result of the

entity’s failure to record

A. purchase discounts.

B. purchase returns.

C. sales.

D. sales returns.

The primary purpose of sending a standard confirmation request to financial institutions

with which the entity has done business during the year is to

A. detect kiting activities that may otherwise not be discovered.

B. corroborate information regarding deposit and loan balances.

C. provide the data necessary to prepare a proof of cash.

D. request information about contingent liabilities and secured transactions.

Under the antifraud provisions of Section 10(b) of the Securities Exchange Act of 1934,

a CPA may be liable if the CPA acted

A. negligently.

B. with independence.

C. without due diligence.

D. without good faith.

In monetary-unit sampling, population size is

A. the dollar balance in an account.

B. the number of items in an account.

C. unrelated to sample size.

D. included in the denominator of the formula to determine sample size.

Before applying substantive procedures to the details of accounts at an interim date (a

date prior to the balance sheet date), an auditor should

A. Assess control risk at high for the assertions embodied in the accounts selected for

interim testing.

B. Determine that the accounts selected for interim testing are not material to the

financial statements taken as a whole.

C. Consider the availability of information at a later date that will be necessary for the

auditor’s procedures (e.g., electronic data).

D. Obtain written representations from management that all financial records and

related data will be made available.

A procedure that would most likely be used by an auditor in performing tests of control

activities that involve segregation of functions but which leave no transaction trail is

A. Inspection.

B. Observation.

C. Reperformance.

D. Reconciliation.

Which of the following concerning the auditor’s report on internal control over financial

reporting is correct?

A. The auditor’s report contains an opinion on the effectiveness of internal control over

financial reporting based on the auditor’s independent work.

B. In the report on internal control over financial reporting, the auditor can issue only a

qualified or an unqualified opinion.

C. The auditor needs to state management’s assessment of internal control over financial

reporting, but does not necessarily need to comment on whether he or she agrees.

D. An unqualified opinion is required if a material weakness is identified.

Ford & Co., CPAs, issued an unqualified opinion on Owens Corp.’s financial

statements. Relying on these financial statements, Century Bank lent Owens $750,000.

Ford was unaware that Century would receive a copy of the financial statements or that

Owens would use them to obtain a loan. Owens defaulted on the loan. To succeed in a

common law fraud action against Ford, Century must prove, in addition to other

elements, that Century was

A. free from contributory negligence.

B. in privity of contract with Ford.

C. justified in relying on the financial statements.

D. in privity of contract with Owens.

Before issuing a report on the compilation of financial statements of a nonpublic entity,

the accountant should

A. apply analytical procedures to selected financial data to discover any material

misstatements.

B. corroborate at least a sample of the assertions management has embodied in the

financial statements.

C. inquire of the entity’s personnel whether the financial statements omit substantially

all disclosures.

D. read the financial statements to consider whether the financial statements are free

from obvious material errors.

Overall analysis of income statement accounts may bring to light errors, omissions, and

inconsistencies not disclosed in the overall analysis of balance sheet accounts. The

income statement analysis can best be accomplished by comparing monthly

A. income statement ratios to balance sheet ratios.

B. revenue and expense account balances to the monthly reported net income.

C. income statement ratios to published industry averages.

D. revenue and expense account totals to the corresponding figures of the preceding

years.

Which of the following circumstances most likely would cause an auditor to believe

that material misstatements may exist in an entity’s financial statements?

A. Accounts receivable confirmation requests yield significantly fewer responses than

expected.

B. Audit trails of computer-generated transactions exist only for a short time.

C. The chief financial officer does not sign the management representation letter until

the last day of the auditor’s fieldwork.

D. Management consults with other accountants about significant accounting matters.

In auditing long-term bonds payable, an auditor most likely would

A. perform analytical procedures on the bond premium and discount accounts.

B. examine documentation of assets purchased with bond proceeds for liens.

C. compare interest expense with the bonds payable amount for reasonableness.

D. confirm the existence of individual bond holders at year-end.

With respect to ethics, the utilitarian theory

A. suggests that auditors should always verify ownership of a client’s material tangible

assets.

B. is primarily concerned with equity and impartiality.

C. suggests that an individual’s actions should not violate the rights of any individual.

D. recognizes that decisions involve trade-offs between costs and benefits.

Which of the following should be included in an accountant’s standard report based

upon the review of a nonpublic entity’s financial statements?

A. A statement that the review was performed in accordance with generally accepted

review standards.

B. A statement that a review consists principally of inquiries and analytical procedures.

C. A statement that the accountant is independent with respect to the entity.

D. A statement that a review is substantially greater in scope than a compilation.

All of the following represent an increased opportunity for management to commit

fraud except:

A. Significant related party transactions.

B. The auditor’s relationship with management is strained.

C. Management is dominated by a single person.

D. The financial statements include highly subjective estimates.

Independence is required

A. under GAAS but not attestation standards.

B. under both GAAS and attestation standards.

C. under attestation standards but not GAAS.

D. is preferred but not required under both GAAS and attestation standards.

An example of a Type I subsequent event is

A. a tornado that destroys an entity’s factory after the balance sheet date.

B. an event after the balance sheet date that confirms the auditor’s belief (documented

prior to the end of the entity’s fiscal year) that a large portion of the entity’s inventory is

obsolete.

C. notification of an IRS audit after the balance sheet date.

D. the entity’s Board of Directors unexpectedly resigns after the balance sheet date.

The Securities Exchange Act of 1934

A. established a voluntary disclosure mechanism for issuers of publicly traded

securities.

B. primarily relates to initial sales of securities to the public.

C. regulates all sales of securities.

D. regulates trading of securities subsequent to issuance.

An auditor generally tests physical security controls over inventory by

A. test counts and cutoff procedures.

B. examination and reconciliation.

C. inspection and recomputation.

D. inquiry and observation.

In order to achieve effective quality control, a firm of independent auditors should

establish policies and procedures for

A. determining the minimum procedures necessary for unaudited financial statements.

B. setting the scope of audit work.

C. deciding whether to accept or continue a client.

D. setting the scope of internal control study and evaluation.

Assessing control risk at a lower level most likely would involve

A. Changing the timing of substantive procedures by omitting interim testing and

performing the tests at year-end.

B. Identifying specific internal controls relevant to specific assertions.

C. Performing more extensive substantive procedures with larger sample sizes than

originally planned.

D. Reducing inherent risk for most of the assertions relevant to significant account

balances.

Common law

A. requires that the CPA guarantee their work.

B. requires that the auditor performs work with due care.

C. requires that the auditor performs work with due diligence.

D. does not recognize the concept of constructive fraud.

AAA & Associates recently finished auditing LinktheEarth Corporation’s internal

control over financial reporting. AAA found a number of material weaknesses in the

entity’s internal control. LinktheEarth’s management remediated all of the weaknesses

that AAA found. However, the auditors did not have sufficient time to retest the

controls. What report should AAA issue with regards to internal control over financial

reporting at year-end?

A. Unqualified report.

B. Adverse report.

C. Qualified report.

D. Disclaimer on opinion.

Define sampling risk and nonsampling risk.

Identify the types of substantive procedures used by the auditor to test accounts payable

and accrued expenses. Provide an example of how the auditor may use each substantive

procedure. Identify if any of the substantive procedures can be used as a test of controls

or a dual-purpose test.

Name the three types of analytical procedures and provide a definition and example for

each.

During the course of the audit of FF Financial, you find that some accounting entries

have been altered. You believe this may be the result of management fraud and you

have determined that the effect of this could be material to the financial statements.

What steps should you take in response to the accounting entries and your concern

about management fraud?

Identify four of the seven primary functions in the revenue cycle and describe each

function.

Define Type I and Type II errors.

What inherent risk factors should an auditor consider when auditing the revenue

process of a computer manufacturer?

Listed below are the major functions of the purchasing process.

1) Purchasing function.

2) General ledger function.

3) Invoice-processing function.

4) Disbursement function.

5) Accounts payable function.

6) Requisition and receiving function.

Name four pairs of functions that should be segregated from each other and explain

why the segregation is important.

Discuss the differences between a control deficiency, a significant deficiency, a material

weakness, and the two dimensions of the control deficiency – likelihood and magnitude.

Identify the types of audit evidence that are tested using audit sampling techniques.

Pretty People Incorporated, is the defendant in a pending discrimination lawsuit. What

information about the lawsuit would you, as an auditor, need to know to decide whether

to disclose the litigation in the financial statements?

What information is typically requested in a legal letter to an entity’s attorney?

According to the Association of Certified Fraud Examiners, there are eight common

methods for committing financial statement fraud. List 4 of the 8 methods.

How has the advancement in technology led to the creation of the Trust Services?

The audit of inventory is often the most involved aspect of an audit. Describe at least

three inherent risk factors that affect the audit of inventory.

“Computer assisted audit techniques and big data analysis have steadily reduced the

number of situations in which audit sampling is necessary and, in the future, will

probably eliminate the need for auditors to rely on sampling.” Defend or refute the

preceding statement.

With respect to an entity’s financial statements, describe both the responsibility of

management and that of the auditor.

What are the differences between document flowcharts, system flowcharts, and

program flowcharts?

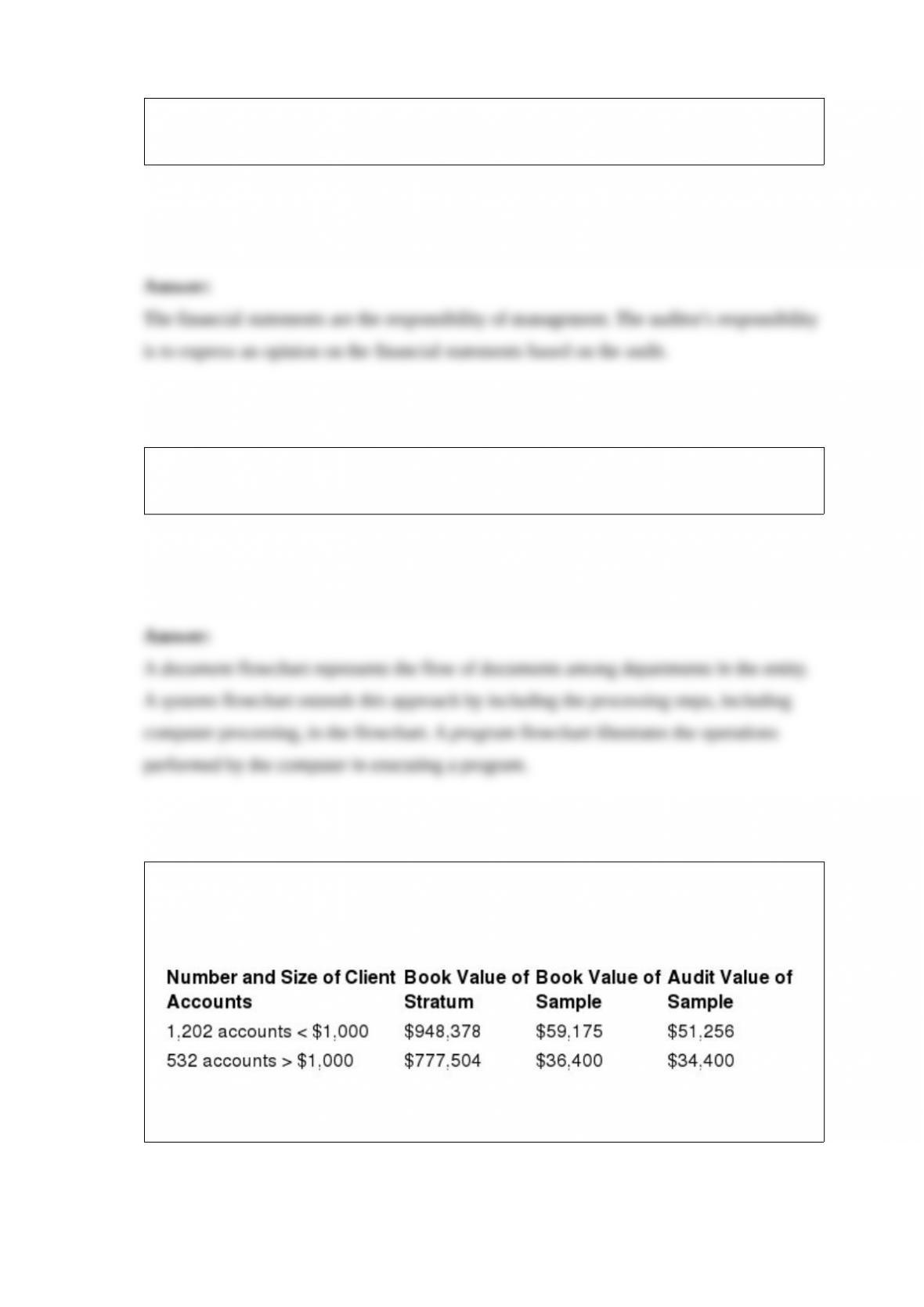

You are auditing accounts receivable for a small company and have found the following

results:

Use ratio projection to project your results.