OldSchool Corp. is reviewing its method of evaluating capital expenditure proposals

using the accounting rate of return method. A recent proposal involved a $200,000

investment in a machine that had an estimated useful life of five years and an estimated

salvage value of $20,000. The cash flow from the new machine was expected to

increase net income before depreciation expense by $56,000 per year. OldSchool’s

current policy for approving a new investment is that it have a rate of return of 12% and

a payback period of three years or less.

(a) Calculate the accounting rate of return on this investment for the first year. Assume

straight-line depreciation. Based on this analysis, would the investment be made?

Explain.

(b) Calculate the payback period for this investment. Based on this analysis, would the

investment be made? Explain.

(c) Comment on OldSchool’s current policy for capital expenditure proposals

XYZ Company has a variable cost ratio of 40%, fixed expenses of $200,000, and

desires to earn operating income of $100,000. Total sales revenue required to achieve

XYZ Company’s desired operating income is:

A. $340,000.

B. $380,000.

C. $420,000.

D. $500,000.

Which of the following is not a right or attribute of common stock ownership?

A. Electing directors.

B. Liability limited to amount invested.

C. Approving changes in corporate charter.

D. Determining dividend policy.

A cost is considered relevant if:

A. it is positive.

B. it is sunk.

C. it makes a difference.

D. if it can’t be changed.

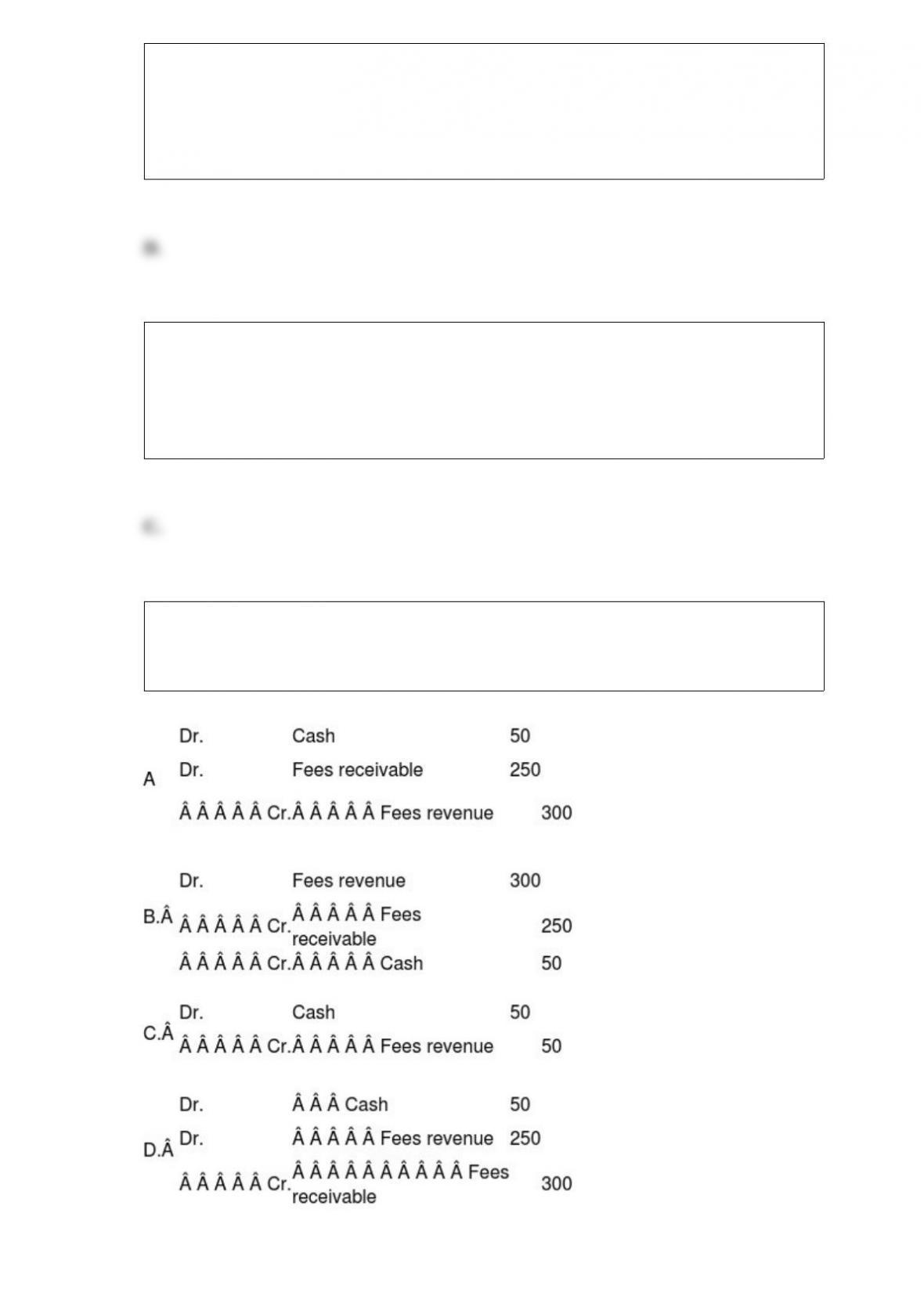

An engineering consultant provided $300 of services to a client; the client paid $50

when the bill was submitted and will pay the balance within a week. The consultant will

record this transaction by:

The accounting rate of return method for evaluating proposed investments:

A. is based on cash receipts and disbursements related to the investment.

B. uses accounting net income from the operating budget.

C. does not recognize the time value of money.

D. is easier to use than the net present value method.

The balance in the Wages Payable account increased from $24,400 at the beginning of

the month to $30,000 at the end of the month. Wages accrued during the month totaled

$122,000.

A. Wages paid during the month totaled $116,400.

B. Wages paid during the month totaled $129,600.

C. Wages expense for the month totaled $116,400.

D. Wages expense for the month totaled $152,000.

Costs may be allocated to a product or activity for many purposes, but care must be

exercised when using allocated costs because:

A. direct costs identified with the product or activity may not be accurately assigned.

B. fixed costs will change in total if the volume of activity changes.

C. all costs may not have been allocated to the product or activity.

D. arbitrarily allocated costs may not behave in the way assumed in the allocation

method.

Which of the following is true about the International Accounting Standards Board

(IASB)?

A. The IASB has been working with the FASB in recent years to achieve convergence

of International Financial Reporting Standards (IFRS) and U.S. GAAP.

B. The goal of the IASB is to develop a single set of high quality, understandable,

enforceable, and globally accepted financial reporting standards based upon clearly

articulated principles.

C. The SEC has delegated full authority to the IASB to be the accounting standards

setting body in the United States.

D. All of the above are correct.

E. Only A and B are correct.

Calculate the cash dividends required to be paid for each of the following preferred

stock issuances:

(a.) The semiannual dividend on 11.5% cumulative preferred, $100 par value;

6,000 shares authorized, issued, and outstanding.

(b.) The total dividends owed to preferred shareholders on $1.50 annual cumulative

preferred, 100,000 shares authorized, 85,000 shares issued, and 81,350 shares

outstanding. The company did not pay dividends during the prior two years or during

the current year.

(c.) The quarterly dividend on 9.6% cumulative preferred, $70 stated value, $72

liquidating value, 20,000 shares authorized, 15,000 shares issued and outstanding. No

dividends in arrears.

Transactions are summarized in:

A. The notes for the financial statements.

B. The independent auditor’s opinion letter.

C. The entity’s accounts.

D. None of the above.

A firm’s current products have sales of $100,000 and an average contribution margin

ratio of 40%. If the firm add a new product with sales of $40,000 and variable costs of

$20,000, the firm’s new average contribution margin ration will be:

A. 37.8%.

B. 42.9%.

C. 45.0%.

D. 48.7%.

When a firm purchases its own shares as treasury stock:

A. total stockholders’ equity is decreased.

B. total stockholders’ equity is increased.

C. retained earnings is decreased.

D. paid-in capital is decreased.

The key difference between a controllable cost and a noncontrollable cost is:

A. the large amount of the cost.

B. the frequency of cost incurrence.

C. the short term ability to influence the cost by the manager.

D. whether the cost is fixed or variable.

“Accumulated other comprehensive income (loss)” includes each of the following items

except:

A. cumulative foreign currency translation adjustments.

B. amounts received from the sale of additional common stock during the year.

C. unrealized gains or losses on available-for-sale investments.

D. gains on certain derivative instruments.

If an organization purchases $2,100 of supplies on account, with terms of 2/15, n50:

A. $1,950 must be paid within 15 days of the invoice date.

B. $2,094 must be paid within 50 days of the invoice date.

C. $2,058 can be paid within 15 days of the invoice date, or $2,100 must be paid within

50 days of the invoice date.

D. $2,058 can be paid within 15 days of the invoice date, or $2,142 must be paid within

50 days of the invoice date. $2,100 * 98% = $2,058

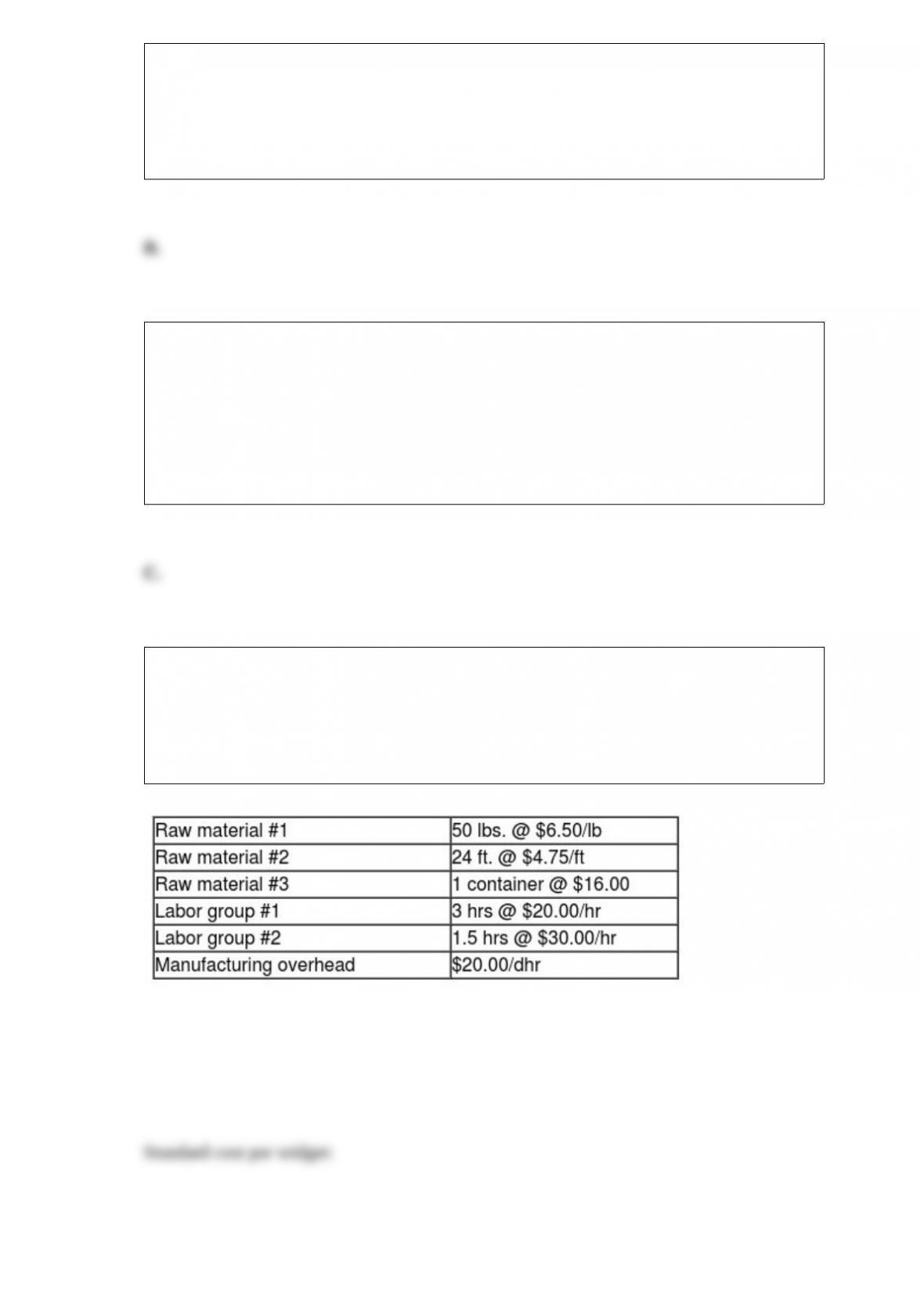

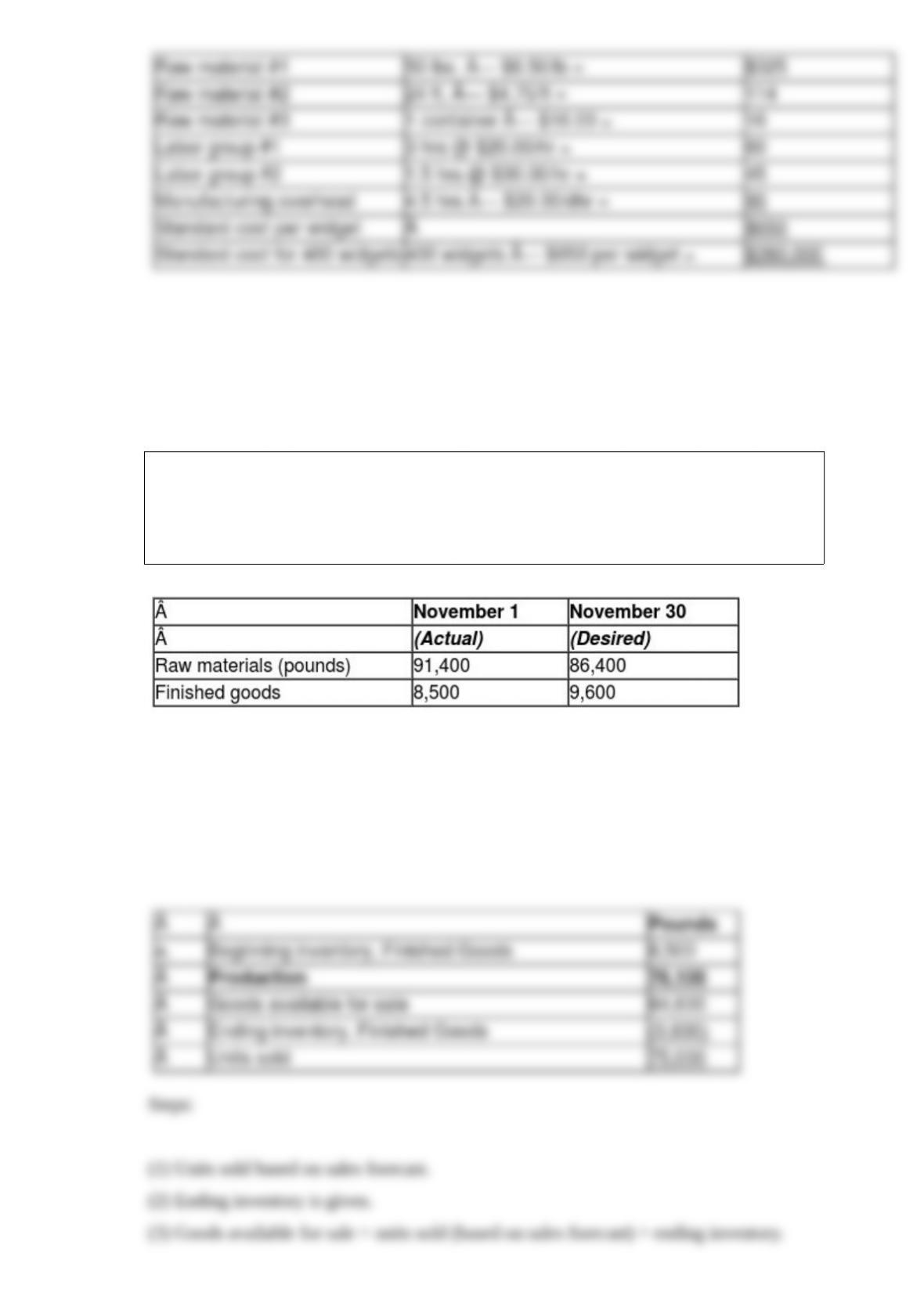

XYZ Company produces high quality widgets. Three raw materials are converted into

the finished product by two labor groups. Manufacturing overhead is applied to finished

units based on direct labor hours. The following standards have been established for

each widget produced:

a) Calculate the standard cost of producing 400 high quality widgets.

Aborkian Co. is forecasting sales of 75,000 units of product for November. To make

one unit of finished product, seven pounds of raw materials are required. Actual

beginning and desired ending inventories of raw materials and finished goods are:

(a.) Calculate the number of units of product to be produced during November.

(b.) Calculate the number of pounds of raw materials to be purchased during November.

Paid-in Capital represents:

A. earnings retained for use in the business.

B. the amount invested in the entity by the stockholders.

C. fair value of the entity’s common stock.

D. net assets of the entity at the date of the statement.

Wisdom Co. has a note payable to its bank. An adjustment is likely to be required on

Wisdom’s books at the end of every month that the loan is outstanding to record the:

A. amount of interest paid during the month.

B. amount of total interest to be paid when the note is paid off.

C. amount of principal payable at the maturity date of the note.

D. accrued interest expense for the month.

The balance sheet of an entity:

A. shows the fair value of the assets at the date of the balance sheet.

B. reflects the impact of inflation on the replacement cost of the assets.

C. reports plant and equipment at its opportunity cost.

D. shows amounts that are not adjusted for changes in the purchasing power of the

dollar.

On January 31, an entity’s balance sheet showed net assets of $3,075 and liabilities of

$675. Stockholders’ equity on January 31 was:

A. $2,400

B. $3,075

C. $3,750

D. $675

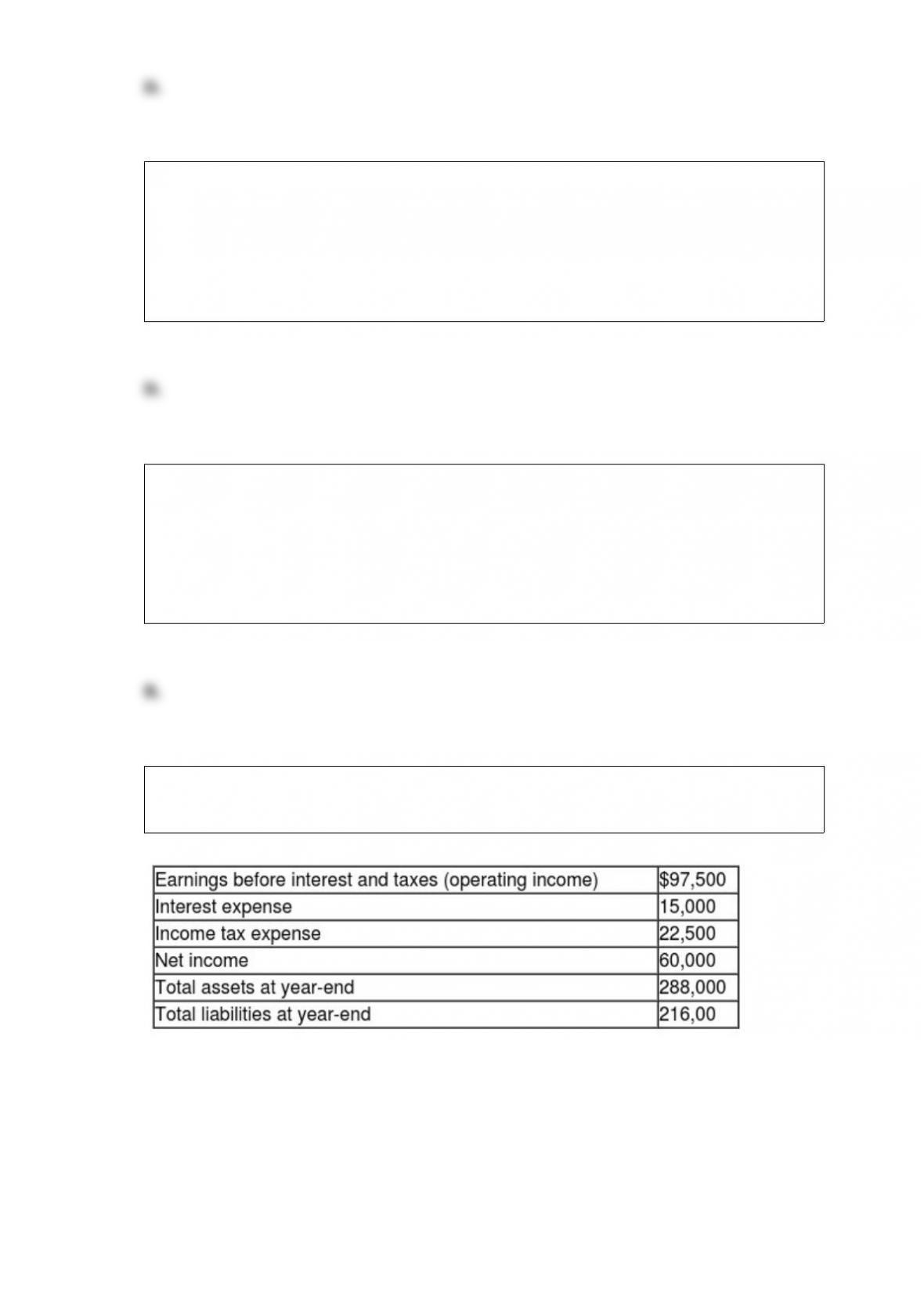

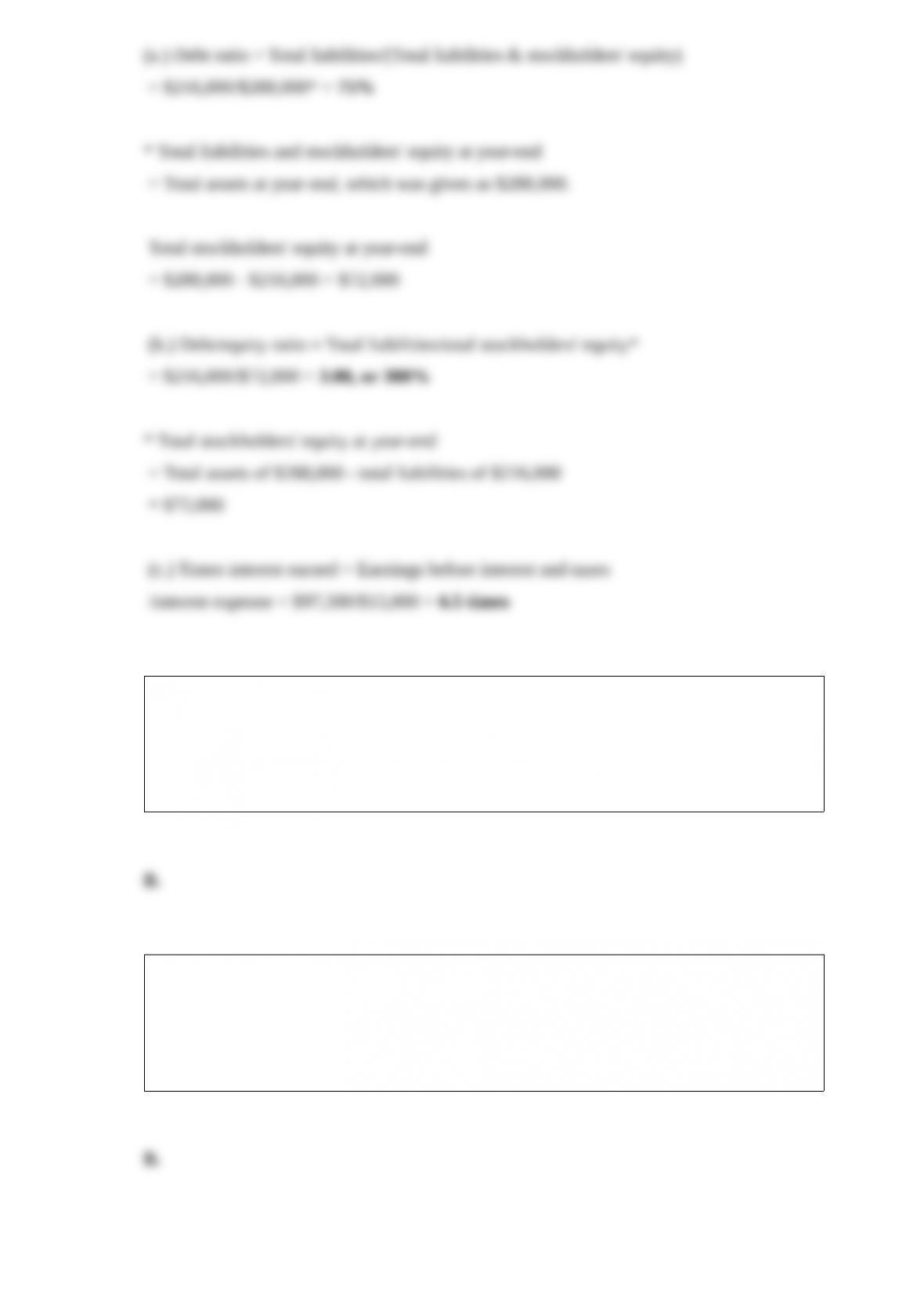

The following information was available for the year ended December 31, 2016:

Required:

(a.) Calculate the debt ratio at December 31, 2016.

(b.) Calculate the debt/equity ratio at December 31, 2016.

(c.) Calculate the times interest earned for the year ended December 31, 2016.

A variance is the difference between actual costs and:

A. selling price.

B. expected costs.

C. activity-based costs.

D. historical costs.

A cost classified “for decision-making purposes” would include:

A. period cost.

B. opportunity cost.

C. controllable cost.

D. inventoriable cost.

The statement of changes in retained earnings for the year shows:

A. the retained earnings balance at the beginning of the year.

B. amounts received from the sale of additional common stock during the year.

C. gains or losses from discontinued operations during the year.

D. the effect of a stock split during the year.

For a firm that presently has a current ratio of 2.0, the effect on this ratio of paying a

current liability is that it:

A. raises the current ratio.

B. lowers the current ratio.

C. doesn’t affect the current ratio.

D. depends on the amount paid.

Capital budgeting differs from operational budgeting because:

A. depreciation calculations are required.

B. it considers the time value of money.

C. operating expenses are not relevant.

D. capital budgets don’t affect cash flow.

Which of the following costs are included in the cost classification that is based on the

relationship between total cost and volume of activity?

A. Variable cost and fixed cost.

B. Direct cost and indirect cost.

C. Product cost and period cost.

D. Committed cost and discretionary cost.

Which of the following is the last budgeted financial statement to be prepared?

A. budgeted income statement.

B. budgeted balance sheet.

C. cash budget.

D. it doesn’t matter which one is prepared last.

An audit conducted in accordance with generally accepted auditing standards includes

each of the following except:

A. examination, on a test basis, of evidence supporting the amounts and disclosures in

the financial statements.

B. evaluation of the efficiency and effectiveness of management.

C. assessment of the accounting principles used and significant estimates made by

management.

D. planning and performance of the audit to obtain reasonable assurance that the

financial statements are free of material misstatements.