Damaged goods are not counted in inventory if they cannot be sold.

When used to monitor and control operations, internal control systems are a low

priority for managers.

A work sheet can be prepared manually or with a computer spreadsheet program.

The primary qualitative characteristics of financial information are relevance and

faithful representation.

To avoid the time-consuming process of taking an inventory each month, some

companies use the gross profit method to estimate ending inventory.

The total dollar value of inventory on hand is determined by: (1) estimating the units on

hand, (2) multiplying the count by cost per unit, and (3) adding the costs for all

products.

A company’s ability to pay its short-term obligations depends on how quickly it sells its

merchandise inventory.

The monetary unit principle means that transactions are expressed using units of money

as the common denominator.

On the work sheet, a net income is entered in the Income Statement Credit column and

in the Statement of Changes in Equity or Balance Sheet Debit column.

Quality of receivables refers to the likelihood of collection without loss.

Dividends represent distributions of profits to the partners of a business.

In order, the last four steps in the accounting cycle include preparing the adjusted trial

balance, preparing financial statements, preparing adjusting entries and preparing

closing entries.

Debits to accounts are normally decreases.

Expenses are costs incurred or the using up of assets from generating revenue.

The Merchandise Inventory account balance at the end of one period is the amount of

beginning inventory in the next period.

Accrued revenues at the end of one period result in cash payments in a subsequent

period.

When expenses exceed revenues, there is a loss and the Income Summary account has a

credit balance.

The MIS is a subsystem of the accounting information system.

Unearned revenues are assets, because a service or product is owed to the customer.

Internal controls include procedures to protect assets and prevent fraud.

A service company earns net income by buying and selling merchandise.

If a customer owes interest on a bill, Accounts Receivable is debited and Interest

Expense is credited.

In accrual basis accounting, accrued revenues are recorded as liabilities.

The formula for computing interest on a note receivable is principal multiplied by

interest rate multiplied by time.

An error made by the bank should result in a reconciling item on the book side of a

bank reconciliation.

Liabilities are defined as “the residual interest in the assets of an entity that remains

after deducting its equity”.

Income Summary is a temporary account.

Correcting entries cannot involve cash.

The necessary financial statement disclosure is accomplished if the amount disclosed is

properly calculated and the costing method used is stated.

The maturity date of a note is the day the note is signed.

An understatement of beginning inventory will understate cost of goods sold and

overstate net income.

A maker who dishonours a note does not pay it at maturity.

The journal entry for petty cash reimbursement is a debit to various expenses and a

credit to Petty Cash.

Adjustments are necessary for transactions and events that extend over more than one

accounting period.

Correcting an error always requires two entries.

The first step in the accounting cycle is transaction analysis.

A bank reconciliation results in creating an adjusted bank balance as well as an adjusted

book balance.

Trekking Company has inventory with a net realizable value of $217,000 and a cost of

$241,000. According to the guidance provided by the principle of faithful

representation, the inventory should be written down to $217,000.

The accounting equation is expressed as assets = liabilities – equity.

The Sales Journal and Cash Receipts Journal may have GST payable and PST payable

columns added to them to facilitate recording. In the same manner GST receivable and

PST receivable columns may be added to the Purchases Journal and the Cash

Disbursements Journal.

A company shows an $800 balance in Prepaid Insurance in the Unadjusted Trial

Balance columns of the work sheet. The Adjustments columns show expired insurance

of $600. This adjusting entry results in:

A. $600 less net income.

B. $600 more net income.

C. $200 difference between the debit and credit columns of the unadjusted trial balance.

D. $400 in the Income Statement Debit column on the work sheet.

E. $400 in the Balance Sheet Credit column on the work sheet.

A balance column ledger account is:

A. An account entered on the balance sheet.

B. An account with debit and credit columns for recording entries and a third column

for showing the balance of the account after each entry is posted.

C. Another name for the withdrawals account.

D. An account used to record the transfers of assets from a business to its owner.

E. A simple form of account that is widely used in accounting education to illustrate the

debits and credits required in recording a transaction.

Z-Mart plans to eliminate a $200 petty cash fund. The current balance in the account

includes $45 in receipts and $165 in currency. The entry to eliminate the fund will

include a:

A. Debit to Cash Short and Over for $10.

B. Debit to Cash for $165.

C. Debit to Miscellaneous Expenses for $35.

D. Credit to Petty Cash for $165.

E. Credit to Cash for $165.

The acid-test ratio:

A. Is also called the quick ratio.

B. Measures profitability.

C. Measures liquidity.

D. Is also called the quick ratio and measures liquidity.

E. All of these answers are correct.

The special journals under the perpetual inventory system:

A. Include an additional sales tax payable journal.

B. Include the sales journal, cash receipts journal, purchases journal, and cash

disbursements journal.

C. Include an additional inventory journal.

D. Include an additional cost of goods sold journal.

E. Include both an additional inventory journal and an additional cost of goods sold

journal.

A company paid the $1,350 premium on a three-year insurance policy on April 1, 2015.

The policy gave protection beginning on that date. How many dollars of the premium

will appear as an expense on the calendar year 2015 income statement assuming the

accrual basis of accounting? Assuming the cash basis of accounting?

A. $1,350 accrual basis; $337.50 cash basis.

B. $450 accrual basis; $450 cash basis.

C. $337.50 accrual basis; $1,350 cash basis.

D. $1,012.50 accrual basis; $1,350 cash basis.

E. $1,350 accrual basis; $1,350 cash basis.

An MIS is designed to:

A. Ensure reliable financial reports.

B. Safeguard company assets.

C. Ensure full disclosure.

D. Both ensure reliable financial reports and safeguard company assets.

E. Collect and process data.

For a merchandiser, each sales transaction involves:

A. Revenue received in the form of a liability from a customer.

B. Recognizing the cost of merchandise sold to a customer.

C. Recognizing cash discounts.

D. Recognizing purchase discounts.

E. Recording accounts payable.

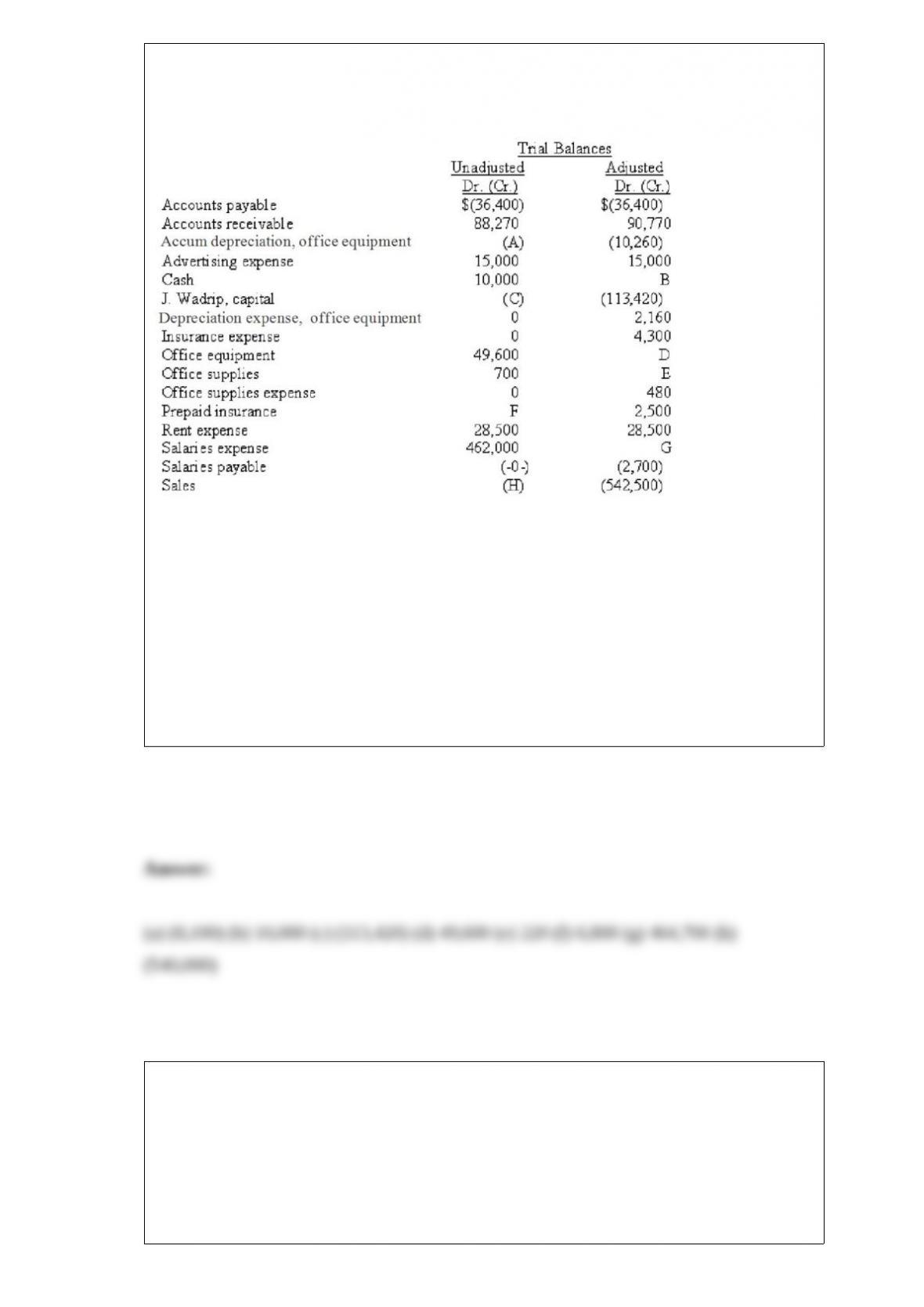

Shown below are data taken from the unadjusted and adjusted trial balances for Wallaby

Company at December 31, 2015:

The differences between the unadjusted and adjusted trial balances can be explained by

adjusting entries that were made for an unrecorded sale, depreciation, expired

insurance, office supplies expense, and accrued salaries expense. Determine the

amounts that should appear in the trial balance blanks labelled A through H and write

your answers below. (Show credit amounts in parentheses.)

A. ____________ B. ___________ C. ____________ D. ____________

E. ____________ F. ___________ G. ____________ H. ____________

A trade discount is:

A. A term used by a purchaser to describe a cash discount given to customers for

prompt payment.

B. A reduction below a list price.

C. A term used by a seller to describe a cash discount granted to customers for prompt

payment.

D. A reduction in price for prompt payment.

E. Also called a rebate.

The broad principle that requires expenses to be reported in the same period as the

revenues that were earned as a result of the expenses is the:

A. Revenue recognition principle.

B. Cost principle.

C. Cash basis of accounting.

D. Matching principle.

E. Timeliness principle.

A $15 credit to Sales was posted as a $150 credit. By what amount is Sales out of

balance?

A. $150 understated.

B. $135 overstated.

C. $150 overstated.

D. $15 understated.

E. $135 understated.

The person who signs a note receivable and promises to pay is the:

A. Maker.

B. Payee.

C. Holder.

D. Receiver.

E. Owner.

Financial statements are prepared in the following order:

A. Balance sheet, statement of changes in equity, income statement.

B. Statement of changes in equity, balance sheet, income statement.

C. Income statement, balance sheet, statement of changes in equity.

D. Income statement, statement of changes in equity, balance sheet.

E. Balance sheet, income statement, statement of changes in equity.

The materiality principle:

A. States that an amount can be ignored if its effect on financial statements is

unimportant to the user and permits use of the direct write-off method.

B. Permits use of the direct write-off method.

C. Prohibits use of the direct write-off method.

D. States that an amount can be ignored if its effect on financial statements is

unimportant to the user.

E. Both permits and prohibits use of the direct write-off method.

The days’ sales uncollected ratio:

A. Is used to evaluate the liquidity of receivables.

B. Is calculated by dividing accounts receivable by sales.

C. Measures a company’s ability to pay its bills on time.

D. Measures a company’s debt to income.

E. Is calculated by dividing sales by accounts receivable.

In the process of adjusting inventory, how can the lower of cost and net realizable value

be applied to the ending inventory?

A. The inventory as a whole.

B. Current replacement cost.

C. Current sales price.

D. To groups of similar or related items.

E. Purchase price.

A credit entry:

A. Increases asset and expense accounts, or decreases liability, equity, and revenue

accounts.

B. Is recorded on the left side of a T-account.

C. Decreases asset and expense accounts, or increases liability, equity, and revenue

accounts.

D. Decreases asset, expense and revenue accounts.

E. Increases the withdrawals account.

Properties or economic resources owned by a business, also described as probable

future economic benefits, are called:

A. Assets.

B. Revenues.

C. Liabilities.

D. Equity.

E. Expenses.

A 10-column spreadsheet used to draft a company’s unadjusted trial balance, adjusting

entries, adjusted trial balance, and financial statements, and which is an optional step in

the accounting process, is a(n):

A. Adjusted trial balance.

B. Work sheet.

C. Post-closing trial balance.

D. Unadjusted trial balance.

E. Book of final entry.

The accrual basis of accounting:

A. Is generally accepted for external reporting because it gives more useful information.

B. Is not acceptable because it gives incomplete information about cash flows.

C. Recognizes revenues when received.

D. Recognizes expenses when paid.

E. Eliminates the need for adjusting entries.

An unconditional written promise to pay a definite sum of money on demand or on a

defined future date (or dates) is a(n):

A. Unearned revenue.

B. Prepaid expense.

C. Account payable.

D. Promissory note.

E. Account receivable.

Financial information that is verifiable means that:

A. Information is clear and concise.

B. Knowledgeable users agree that the financial information is faithfully represented.

C. The information is useful to users with reasonable knowledge of accounting as well

as business and economic activities.

D. Users are able to compare different companies, if all the companies use similar

accounting practices.

E. The financial statements have not been prepared according to GAAP.

J.C. Penny’s total quick assets were $5,888 million. Its current assets were $11,700. Its

current liabilities were $8,000. The acid-test ratio is:

A. .74.

B. .50.

C. 1.5.

D. .68.

E. 2.2.

The ledger that contains the financial statement accounts of a business is the:

A. General Ledger.

B. General Journal.

C. Special Ledger.

D. Special Journal.

E. Column balance ledger.

Closing the temporary accounts at the end of each accounting period:

A. Serves to transfer the effects of these accounts to the proper equity account on the

balance sheet.

B. Prepares the withdrawals account for use in the next period.

C. Gives the revenue and expense accounts zero balances.

D. Gives the withdrawals account a zero balance.

E. All of these answers are correct.

Incidental costs of inventory:

A. Can be assigned to every unit.

B. May be immaterial.

C. Can be allocated to cost of goods sold.

D. Are subject to the materiality principle.

E. All of these answers are correct.

The account sometimes referred to as the owner’s personal account or drawing account

is called a(n):

A. Revenue account.

B. Withdrawals account.

C. Capital account.

D. Expense account.

E. Liability account.

Trekking Company markets a climbing kit and uses a perpetual inventory system to

account for its merchandise. The beginning balance of the inventory and transactions

during January were as follows:

If the ending inventory is valued at $357, what inventory cost flow assumption was

used?

A. Average costing.

B. FIFO.

C. Weighted-average.

D. Specific identification.

E. Retail.

If an inventory amount is reported in error, it can cause a misstatement in:

A. Cost of goods sold.

B. Gross profit.

C. Net income.

D. Current assets.

E. All of these answers are correct.

Net income appears on which of the following statement(s)?

A. Balance sheet.

B. Income statement.

C. Statement of changes in equity.

D. Statement of cash flows.

E. Both an income statement and statement of changes in equity.

Before recording adjusting entries on December 31, the Store Supplies account had a

$900 debit balance, while a physical count of the supplies showed $325 of unused

supplies on hand. Prepare the required adjusting entry.

When a count of merchandise inventory is taken for the purpose of reconciling goods

actually on hand to the inventory control account in the general ledger it is known as

taking a(n) ________________.

Identify whether each of the following items affects the bank side or the book side of a

bank statement reconciliation.

_____ (1)Bank service charges

_____ (2)Outstanding cheques

_____ (3)Deposits in transit

_____ (4)NSF cheque

_____ (5)Interest on a chequing account

_____ (6)The bank recorded a cheque for $958. The company wrote the cheque for

$9,580

_____ (7)The bank printed cheques for the depositor.

_____ (8)Debit memo

_____ (9)Credit memo

_____ (10)The bank collected a $1,000 note for the depositor.

An overstatement of beginning inventory will __________________ cost of goods sold,

and _________________ net income.

Companies experiencing seasonal variations in sales often choose a fiscal year

corresponding to their ________________________.

Trekking Company uses a perpetual inventory system and four special journals:

Purchases, Sales, Cash Receipts, and Cash Disbursements. The following transactions

were incurred during August:

Explain how inventory management is evaluated using the merchandise turnover and

days’ sales in inventory ratios.

Caps Lock has liabilities of $150,000 and $100,000 in equity. What is the value of its

assets?

Explain why ethics and social responsibility are an integral part of accounting.

Explain the accounting equation, also called the balance sheet equation.