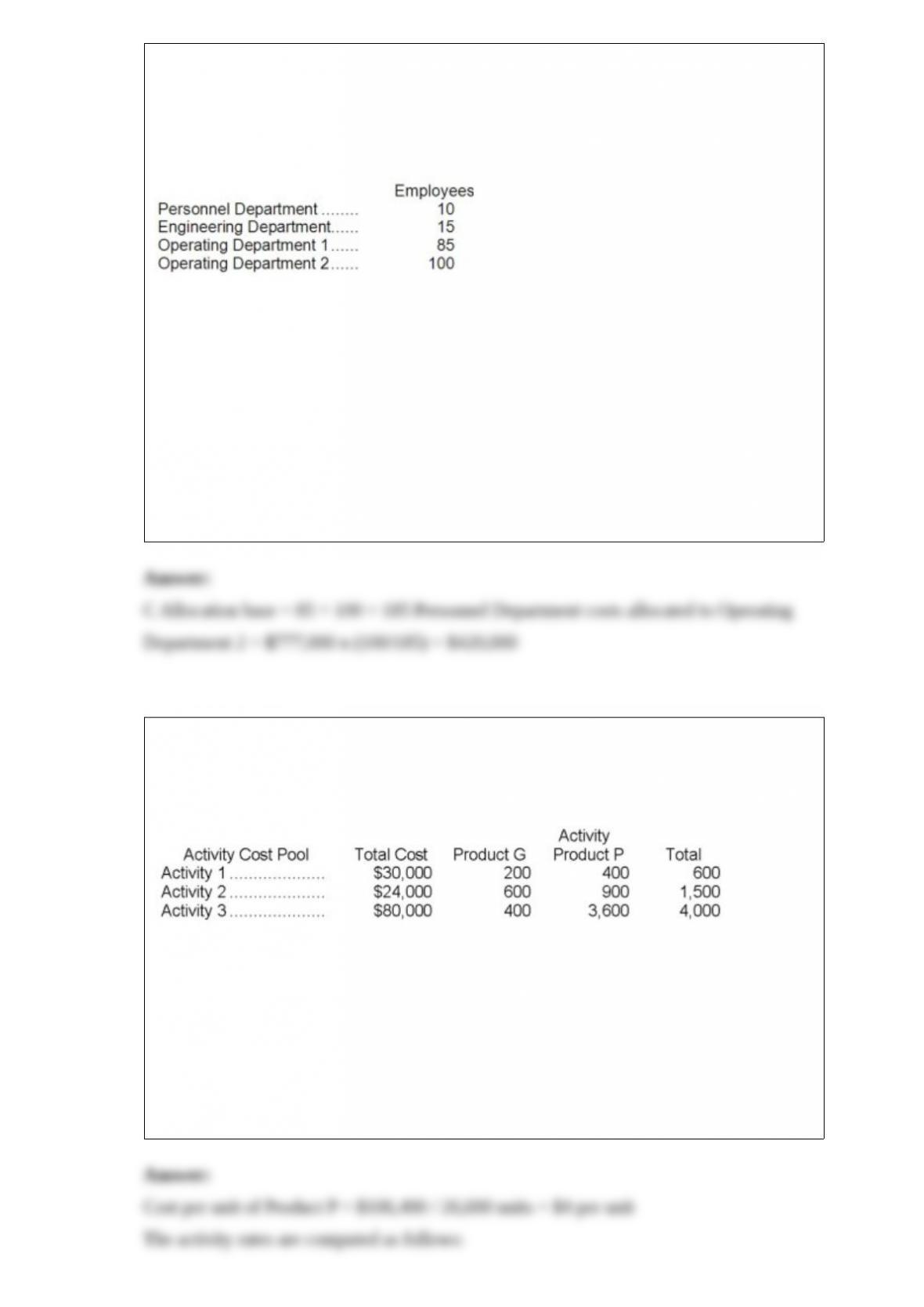

1) Apex Corporation has two service departments and two operating departments. The

costs of the Personnel department (a service department) are allocated to other

departments on the basis of the number of employees in the other departments.

Departments and number of employees are as follows:

Costs in the Personnel Department total $777,000 for the year.

The amount of Personnel Department cost that would be allocated to Operating

Department 2 under the direct method would be:

A.$0

B.$388,500

C.$420,000

D.$370,000

2) Monson Corporation has two products: G and P. The company uses activity-based

costing and has prepared the following analysis showing the total cost and activity for

each of its three activity cost pools:

The annual production and sales of Product G is 10,640 units. The annual production

and sales of Product P is 26,600.

The cost per unit of Product P under activity-based costing is closest to:

A.$4.00

B.$30.16

C.$10.00

D.$6.88

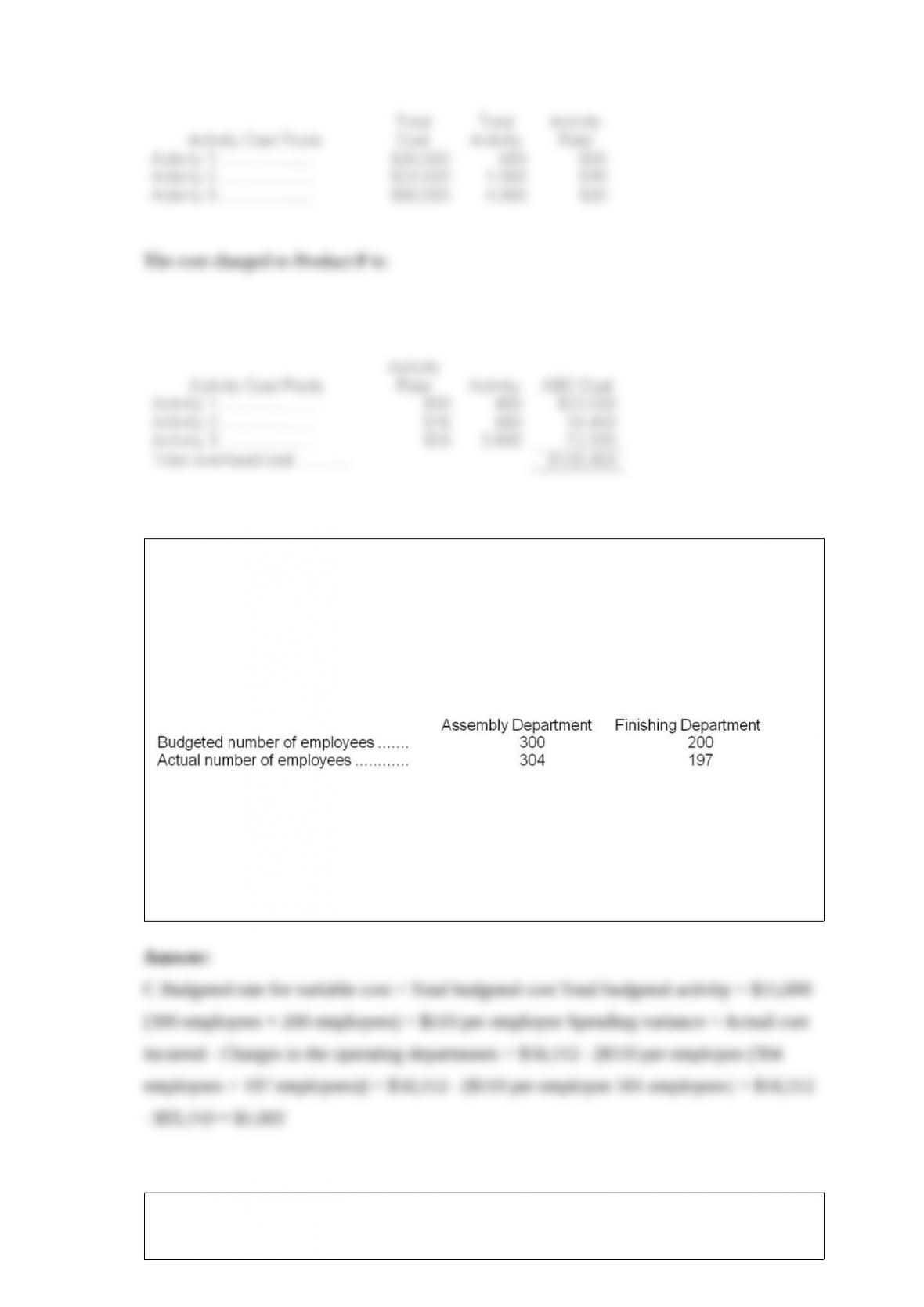

3) The Bolton Company operates a Health Care service department for its employees.

The variable costs of this department are charged to the company’s two operating

departments, Assembly and Finishing, based on the number of employees in each

department. The Health Care Department’s total variable cost was budgeted at $55,000

for the past year; its actual total variable cost was $56,112. Additional data for the past

year follow:

For performance evaluation purposes, how much of the actual Health Care variable cost

should not be charged to the operating departments at the end of the year?

A.$55,000

B.$56,112

C.$1,002

D.$1,112

4) The ________________________ is the amount remaining from sales revenue after

all variable expenses have been deducted.

A) cost structure

B) gross margin

C) contribution margin

D) committed fixed cost

5) The Murray Corporation uses a standard cost system in which it applies

manufacturing overhead on the basis of standard direct labor-hours (DLHs). The

company recorded the following activity and cost data for May:

The amount of fixed manufacturing overhead cost that was used to compute the fixed

component of the predetermined overhead rate was:

A.$54,135

B.$60,150

C.$59,465

D.$57,600

6) The journal entry to record the allocation of any underapplied or overapplied

manufacturing overhead for July would include the following:

A.debit to Finished Goods of $29,800

B.credit to Finished Goods of $600

C.debit to Finished Goods of $600

D.credit to Finished Goods of $29,800

7) At the beginning of the year, manufacturing overhead for the year was estimated to

be $477,590. At the end of the year, actual direct labor-hours for the year were 29,000

hours, the actual manufacturing overhead for the year was $472,590, and manufacturing

overhead for the year was overapplied by $110. If the predetermined overhead rate is

based on direct labor-hours, then the estimated direct labor-hours at the beginning of the

year used in the predetermined overhead rate must have been:

A.29,300 direct labor-hours

B.28,987 direct labor-hours

C.28,993 direct labor-hours

D.29,000 direct labor-hours

8) Sales in North Corporation increased from $60,000 per year to $63,000 per year

while net operating income increased from $10,000 to $12,000. Given this data, the

company’s degree of operating leverage must have been:

A.4.0

B.1.5

C.5.0

D.21.0

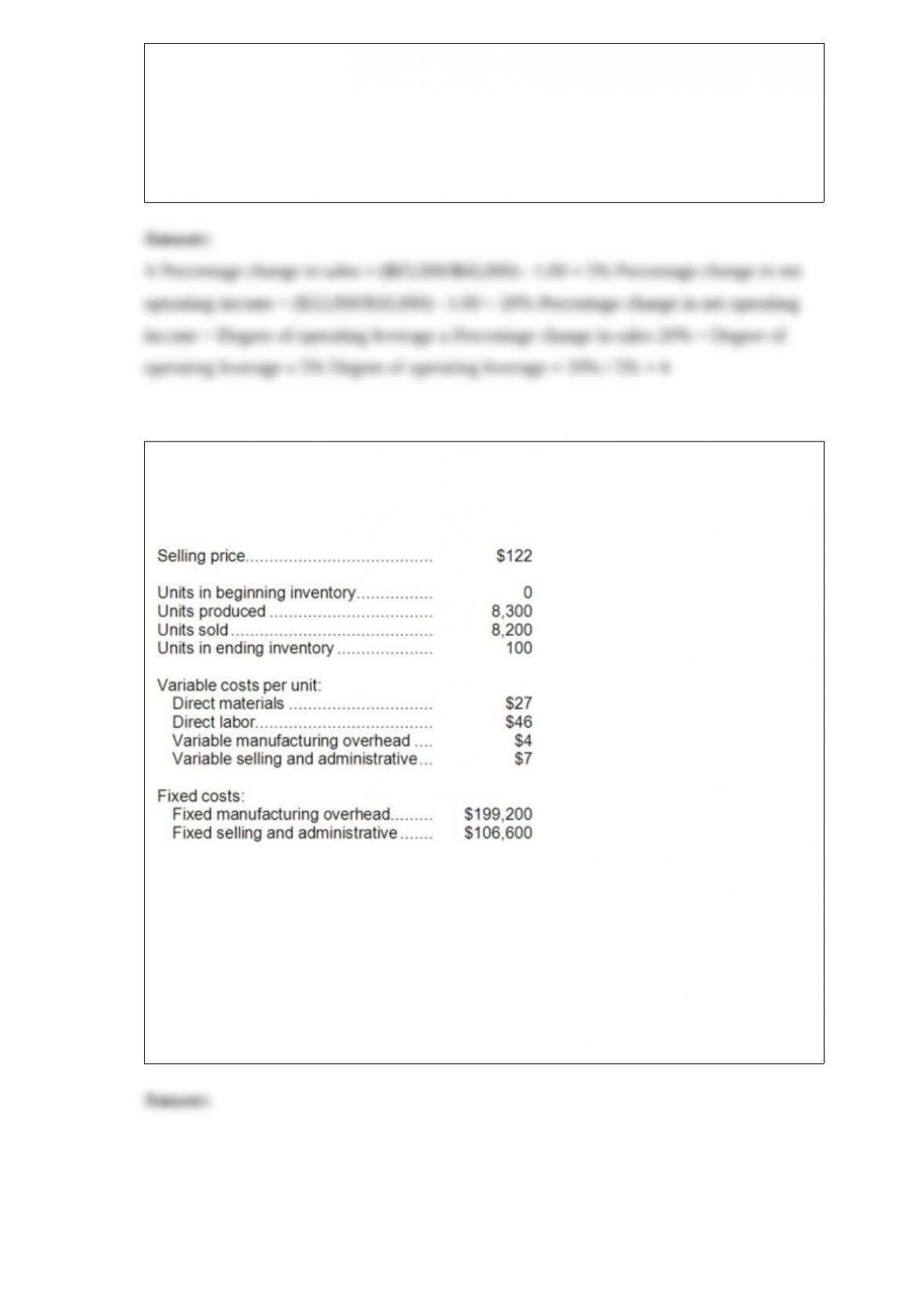

9) Mahugh Corporation, which has only one product, has provided the following data

concerning its most recent month of operations:

Required:

a. What is the unit product cost for the month under variable costing?

b. What is the unit product cost for the month under absorption costing?

c. Prepare a contribution format income statement for the month using variable costing.

d. Prepare an income statement for the month using absorption costing.

e. Reconcile the variable costing and absorption costing net operating incomes for the

month.

10) Coblentz Fabrication Corporation has a standard cost system in which it applies

manufacturing overhead to products on the basis of standard machine-hours (MHs) at

$6.20 per MH. The company had budgeted its fixed manufacturing overhead cost at

$40,000 for the month. During the month, the actual total variable manufacturing

overhead was $48,970 and the actual total fixed manufacturing overhead was $43,000.

The actual level of activity for the period was 8,300 MHs. What was the total of the

variable overhead rate and fixed manufacturing overhead budget variances for the

month?

A.$2,490 Favorable

B.$510 Favorable

C.$510 Unfavorable

D.$2,490 Unfavorable

11) A study has been conducted to determine if one of the departments in Barry

Corporation should be discontinued. The contribution margin in the department is

$60,000 per year. Fixed expenses charged to the department are $75,000 per year. It is

estimated that $34,000 of these fixed expenses could be eliminated if the department is

discontinued. These data indicate that if the department is discontinued, the company’s

overall net operating income would:

A.decrease by $26,000 per year

B.increase by $26,000 per year

C.decrease by $15,000 per year

D.increase by $15,000 per year

12) A major weakness of flexible budgets is that:

A.they are valid for only a single level of activity.

B.they ignore fixed costs.

C.they compare actual costs at one level of activity to budgeted costs at a different level

of activity.

D.none of these is a major weakness of flexible budgets.

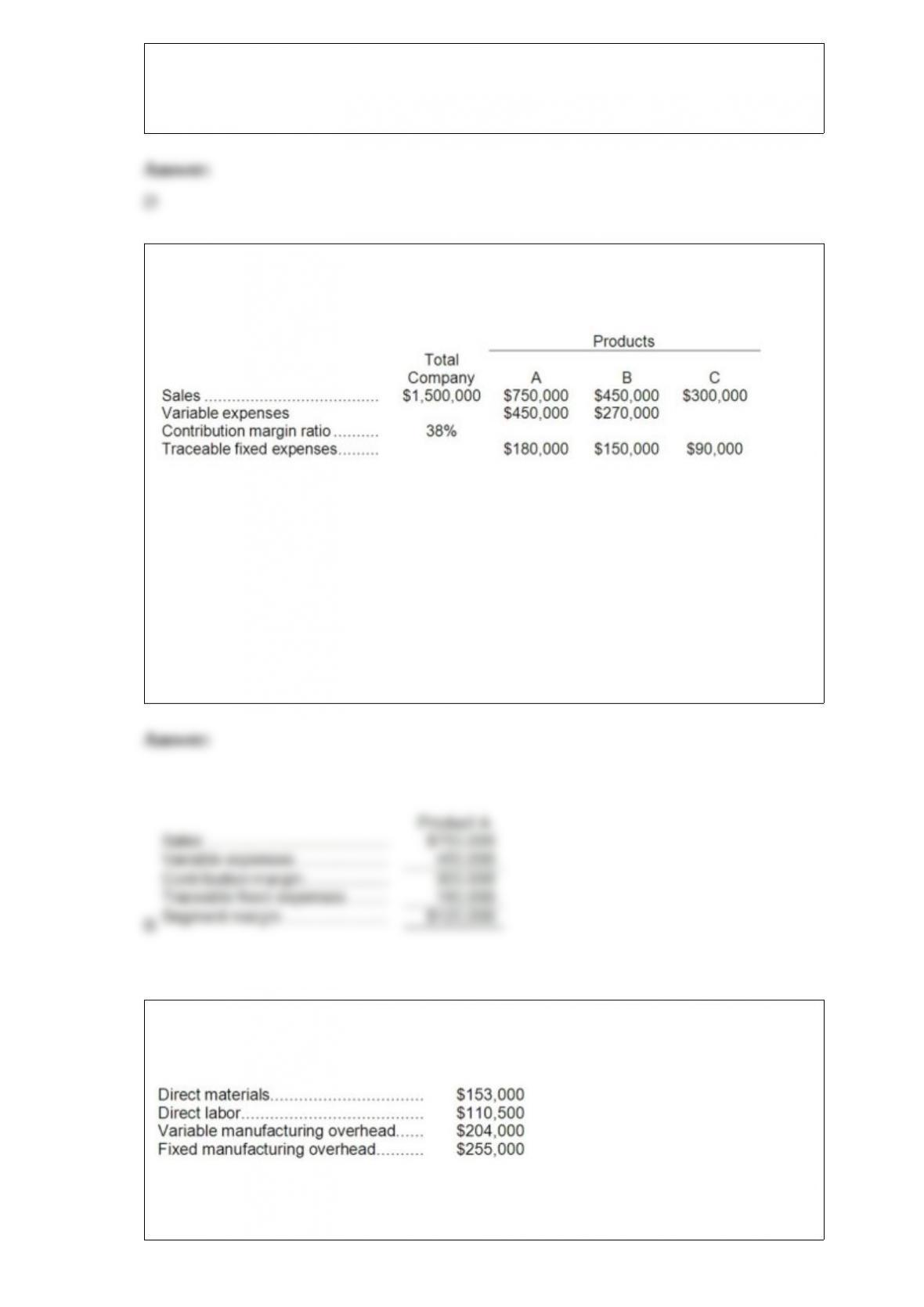

13) Higgins Corporation sells three products, Product A, Product B, and Product C.

Data concerning the company’s most recent month of operations, June, appear below:

The total fixed expense for the company was $525,000.

The product line segment margin for Product A for June was:

A.$300,000

B.$120,000

C.$65,000

D.$10,000

14) Harris Corporation produces a single product. Last year, Harris manufactured

17,000 units and sold 13,000 units. Production costs for the year were as follows:

Sales were $780,000 for the year, variable selling and administrative expenses were

$88,400, and fixed selling and administrative expenses were $170,000. There was no

beginning inventory. Assume that direct labor is a variable cost.

Under variable costing, the company’s net operating income for the year would be:

A.$60,000 higher than under absorption costing

B.$108,000 higher than under absorption costing

C.$108,000 lower than under absorption costing

D.$60,000 lower than under absorption costing

15) Last year the Uptown Division of Gorcen Enterprises had sales of $300,000 and a

net operating income of $24,000. The average operating assets at Uptown last year

amounted to $120,000.

At Uptown the turnover used to calculate ROI last year was:

A.0.4

B.2.5

C.3.2

D.5.0

16) All differences between super-variable costing and absorption costing are explained

by:

A.the accounting for direct materials and manufacturing overhead costs.

B.the accounting for direct labor and direct materials.

C.the accounting for direct labor and manufacturing overhead costs.

D.the accounting for manufacturing overhead costs.

17) Davey Corporation is preparing its Manufacturing Overhead Budget for the fourth

quarter of the year. The budgeted variable manufacturing overhead rate is $3.00 per

direct labor-hour; the budgeted fixed manufacturing overhead is $66,000 per month, of

which $10,000 is factory depreciation.

If the budgeted direct labor time for November is 9,000 hours, then the total budgeted

cash disbursements for manufacturing overhead for November must be:

A.$56,000

B.$83,000

C.$37,000

D.$93,000

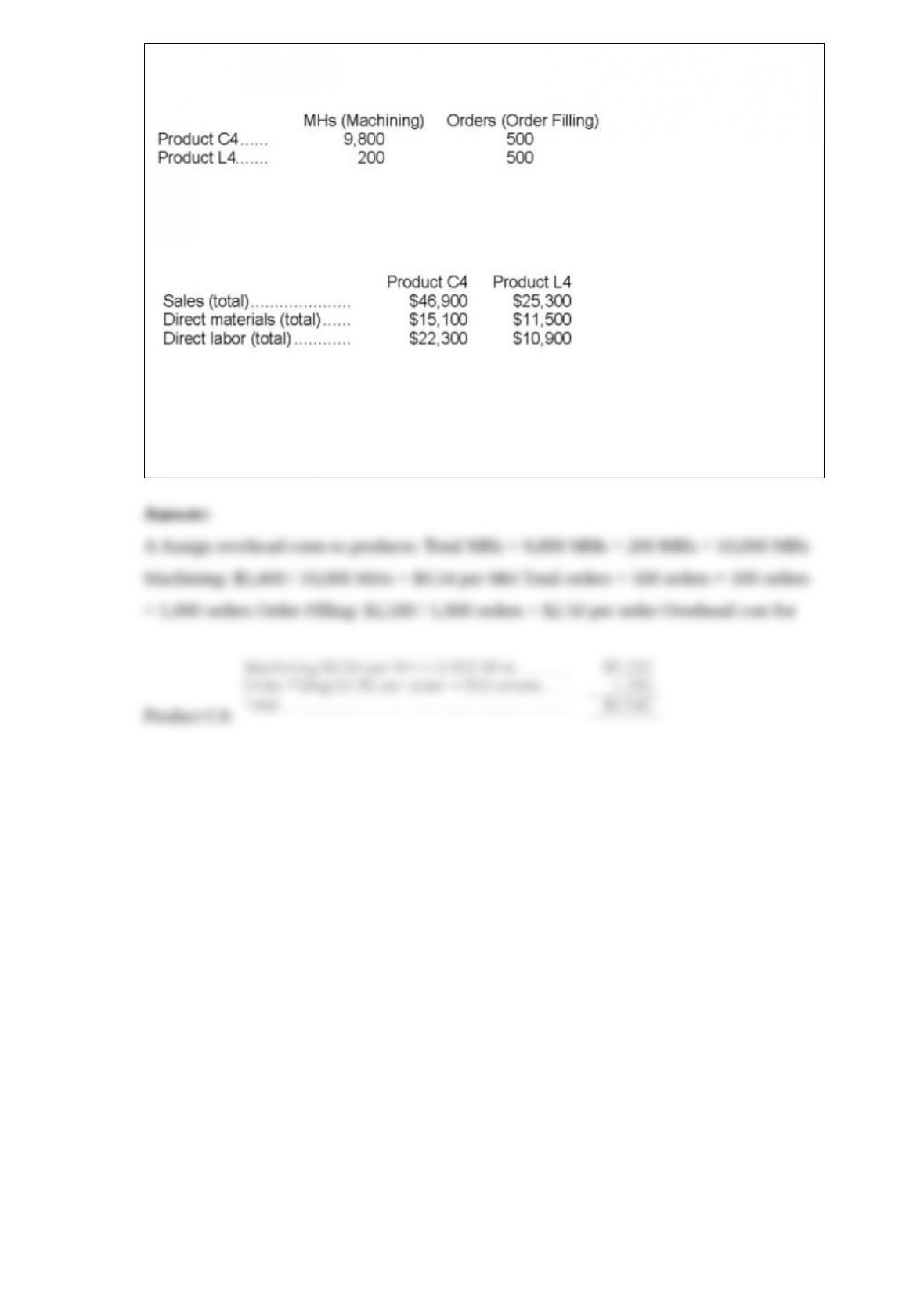

18) Stroth Corporation uses activity-based costing to compute product margins.

Overhead costs have already been allocated to the company’s three activity cost

pools-Machining, Order Filling, and Other. The costs in those activity cost pools appear

below:

Machining costs are assigned to products using machine-hours (MHs) and Order Filling

costs are assigned to products using the number of orders. The costs in the Other

activity cost pool are not assigned to products. Activity data appear below:

Finally, sales and direct cost data are combined with Machining and Order Filling costs

to determine product margins.

What is the overhead cost assigned to Product C4 under activity-based costing?

A.$6,542

B.$5,292

C.$1,250

D.$10,500