Which of the following methods provides no data for service departments to monitor

each other’s costs?

A. Direct method.

B. Reciprocal method.

C. Step method.

D. All three methods, Direct, Reciprocal, and Step, provide data for monitoring costs.

Answer:

Controllable revenue is included in a performance report of a

A. a

B. b

C. c

D. d

Answer:

The cost accountant determined $2,700,000 of the communication network’s costs were

fixed and should be allocated based on the number of calls. The remaining costs should

be allocated based on the time on the network. What is the total communication

network costs allocated to the Large Box Division assuming the company uses

dual-rates to allocate common costs?

A. $2,700,000

B. $2,520,000

C. $1,980,000

D. $1,500,000

Answer:

Wetter Co. has provided the following information for last year:

The total material cost (rounded) is:

A. $293,325

B. $582,500

C. $300,021

D. $200,000

Answer:

What is the predetermined manufacturing overhead rate per direct labor hour for the

year?

A. $15

B. $20

C. $25

D. $30

Answer:

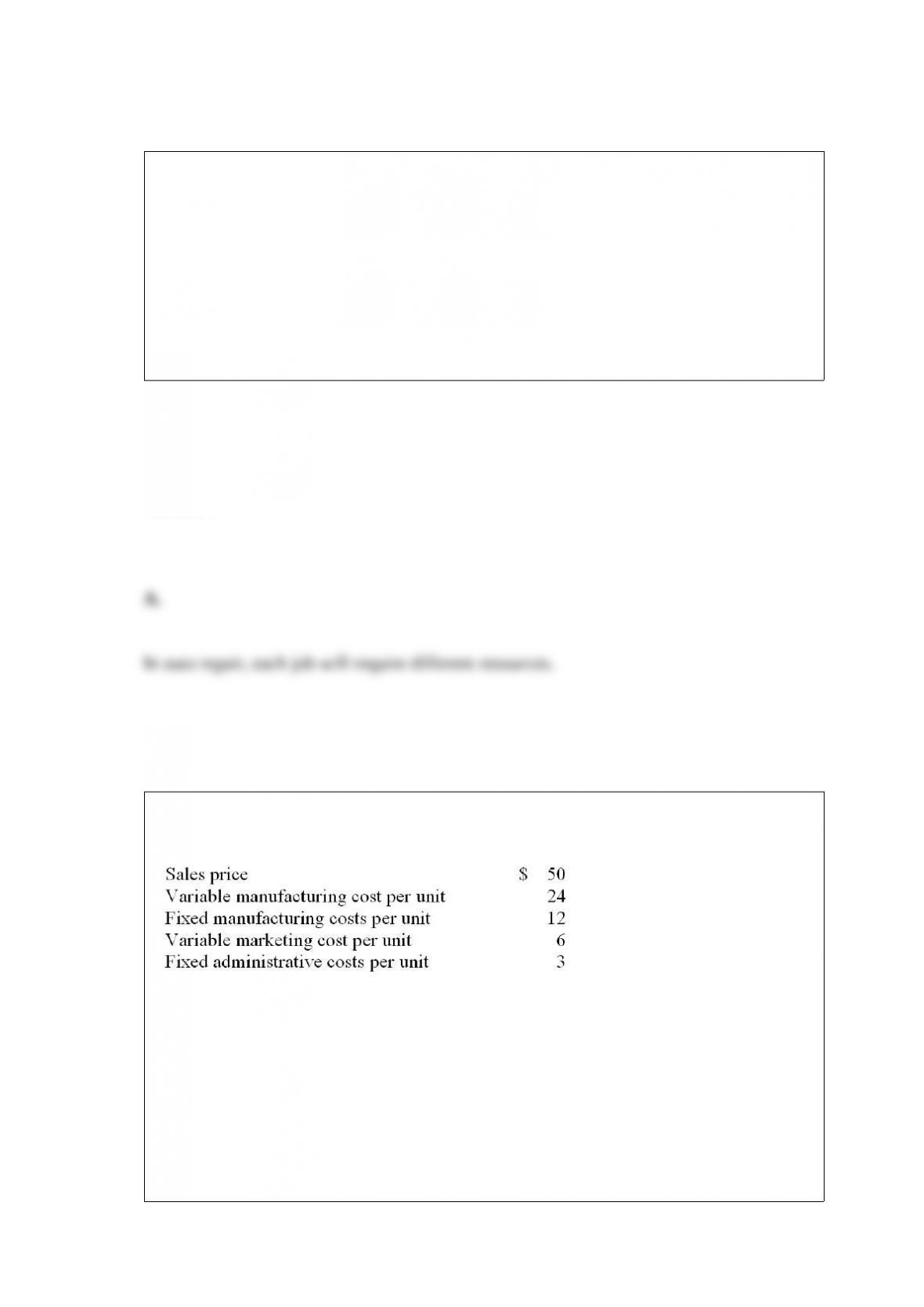

For which of the following businesses would the job order cost system be appropriate?

A. Auto repair shop

B. Crude oil refinery

C. Drug manufacturer

D. Root beer producer

Answer:

You have been provided with the following information regarding the York

Manufacturing Company

:

This information is based on forecasted sales of 33,000 units.

Required:

(a) What are the expected operating profits for the upcoming year?

(b) What is the break-even point in dollars?

(c) How much in sales dollars is required to generate an operating profit of $275,000?

Answer:

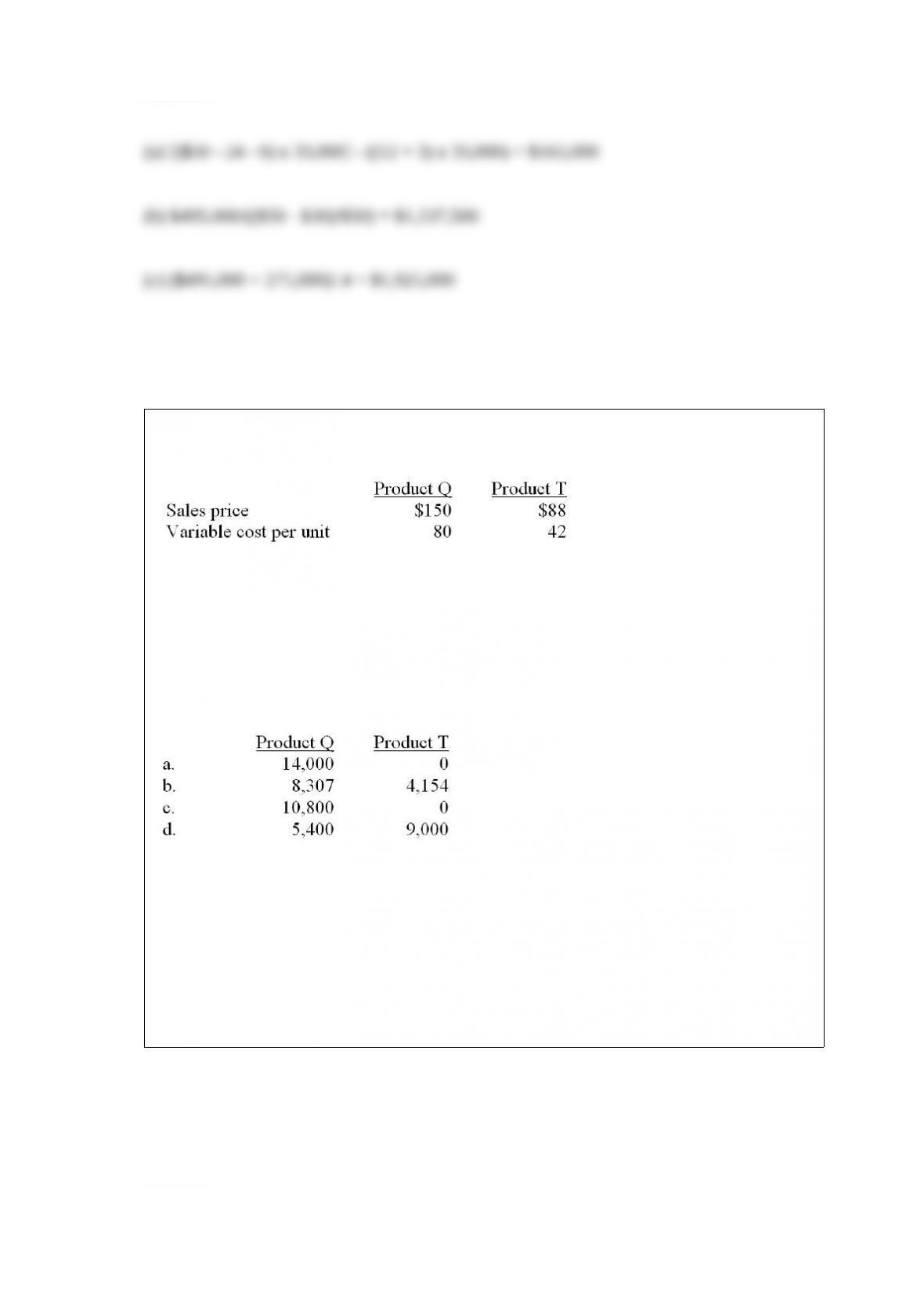

The Winwood Company manufactures two products: Q and T. The costs and revenues

are as follows:

Total demand for Product Q is 14,000 units and for Product T is 9,000 units. Machine

time is a scarce resource. During the year, 54,000 machine hours are available. Product

Q requires 5 machine hours per unit, while Product T requires 3 machine hours per unit.

How many units of Products Q and T should Winwood produce?

A. a

B. b

C. c

D. d

Answer:

Use the following information to compute residual income:

A. $12,000

B. $22,500

C. $30,000

D. $48,000

Answer:

Which of the following statements is (are) false?

(A) From an organization’s viewpoint, transfer prices have no effect on total profits

assuming the transfer occurs between the two responsibility centers.

(B) A transfer price is the value assigned to the transfer of goods or services between

divisions within the same organization.

A. Only A is false.

B. Only B is false.

C. Both A and B are false.

D. Neither A nor B is false.

Answer:

Which one of the following items would most likely not be incorporated into the

calculation of a division’s investment base when using the residual income approach for

performance measurement and evaluation? (CMA Adapted)

A. Fixed assets employed in division operations.

B. Land being held by the division as a site for a new plant.

C. Division inventories when division management exercises control over the amount

of short-term credit used.

D. Division accounts payable when division management exercises control over the

amount of short-term credit used.

Answer:

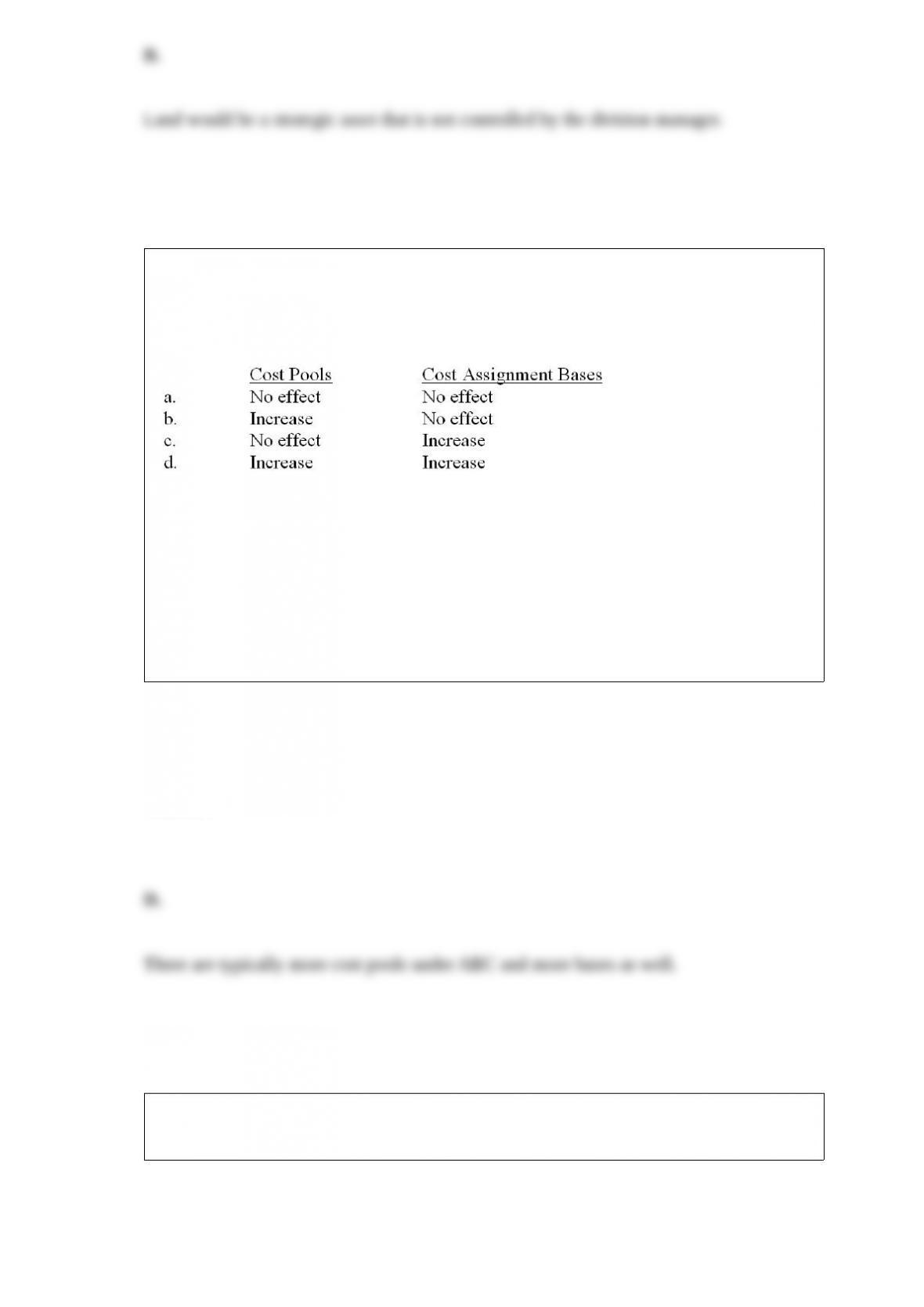

What is the typical effect on the numbers of cost pools and cost assignment bases when

an activity-based costing (ABC) system replaces a traditional costing system? (CPA

adapted)

A. a

B. b

C. c

D. d

Answer:

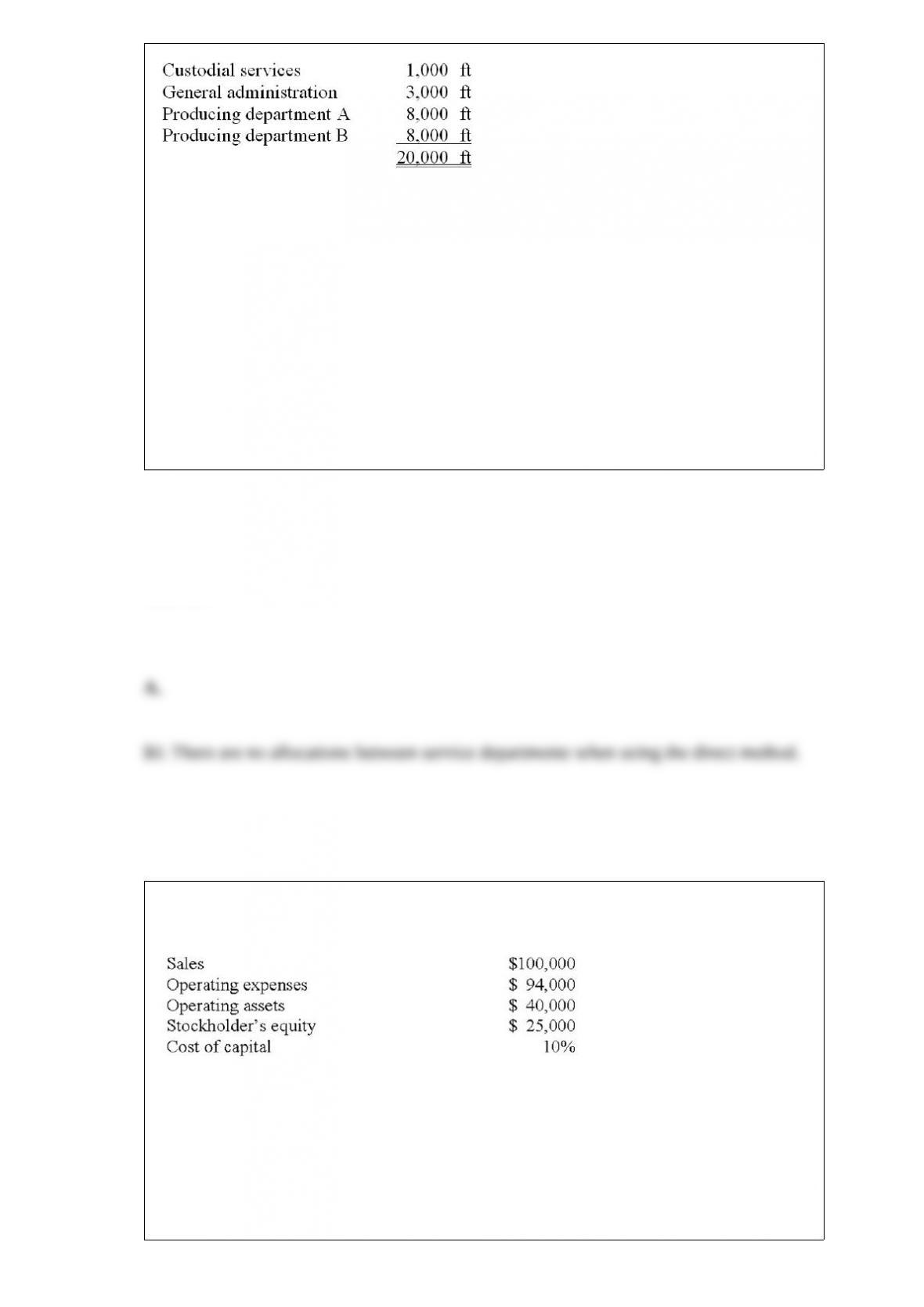

Bagley Company has two service departments and two producing departments. Square

footage of space occupied by each department follows:

The department costs of Custodial Services are allocated on a basis of square footage of

space. If Custodial Services costs are budgeted at $38,000, the amount of cost allocated

to General Administration under the direct method would be

A. $0.

B. $7,125.

C. $6,000.

D. $5,700.

Answer:

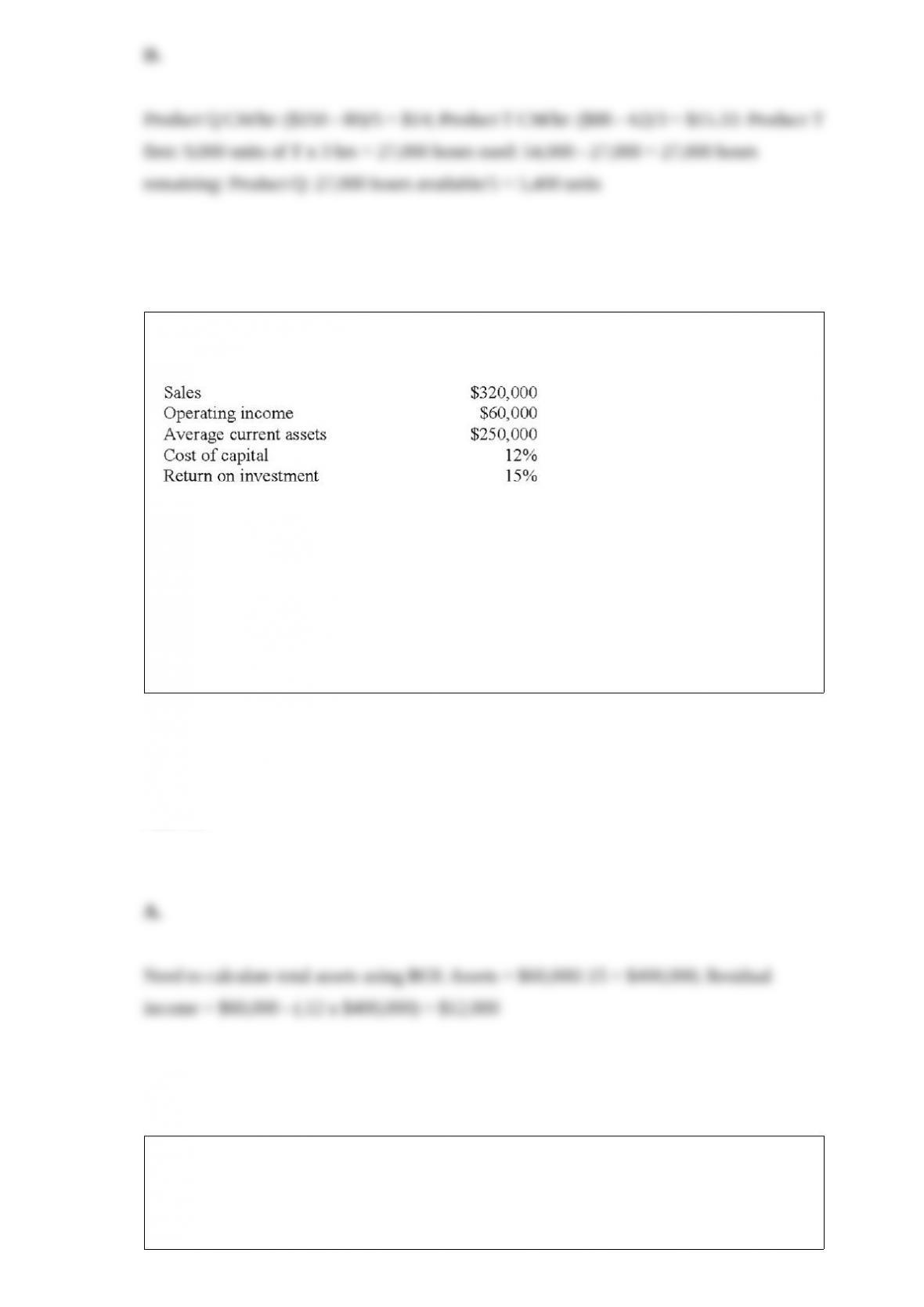

The following information is available for Company X:

What is Company X’s return on investment (ROI)?

A. 6.0%

B. 10.0%

C. 15.0%

D. 24.0%

Answer:

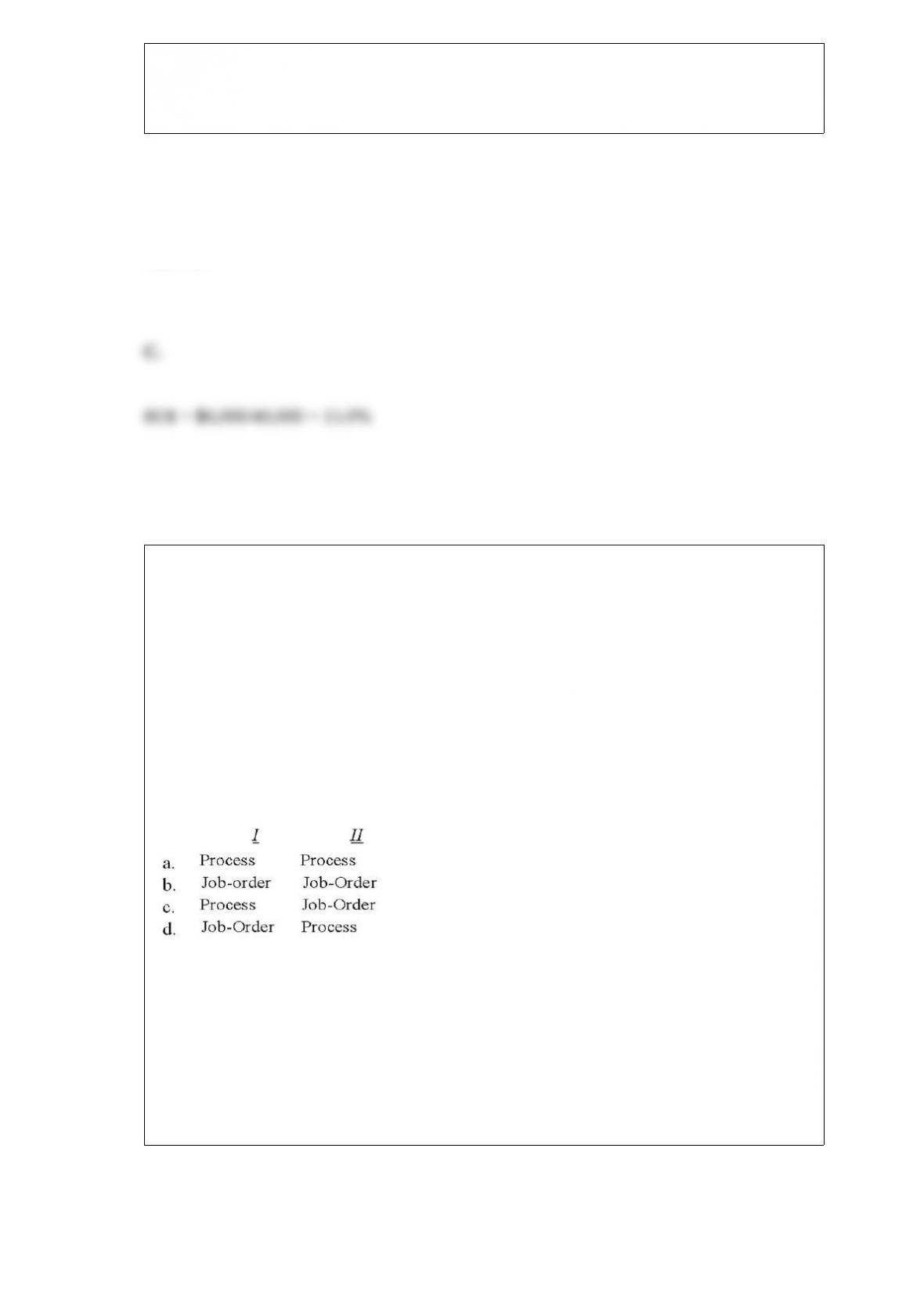

The following examples briefly describe the manufacture of two different products.

Which costing method (job-order or process) would be the best method to use for each

project?

I. Fred Puetz manufactures Fred’s Wine Cooler. Fred once made the statement, “People

can have any flavor of Fred’s Wine Cooler they want as long it’s boysenberry.”

II. Ahmad Aerondonetics is manufacturing three space shuttles for the country of

Kricherra. Each shuttle is slightly different and production will last approximately two

years.

A. a

B. b

C. c

D. d

Answer:

In the general model, an efficiency variance is calculated as

A. (SP x AQ) – (SP x SQ)

B. (AP x SQ) – (SP x SQ)

C. (AP x AQ) – (SP x SQ)

D. (AP x AQ) – (SP x AQ)

Answer:

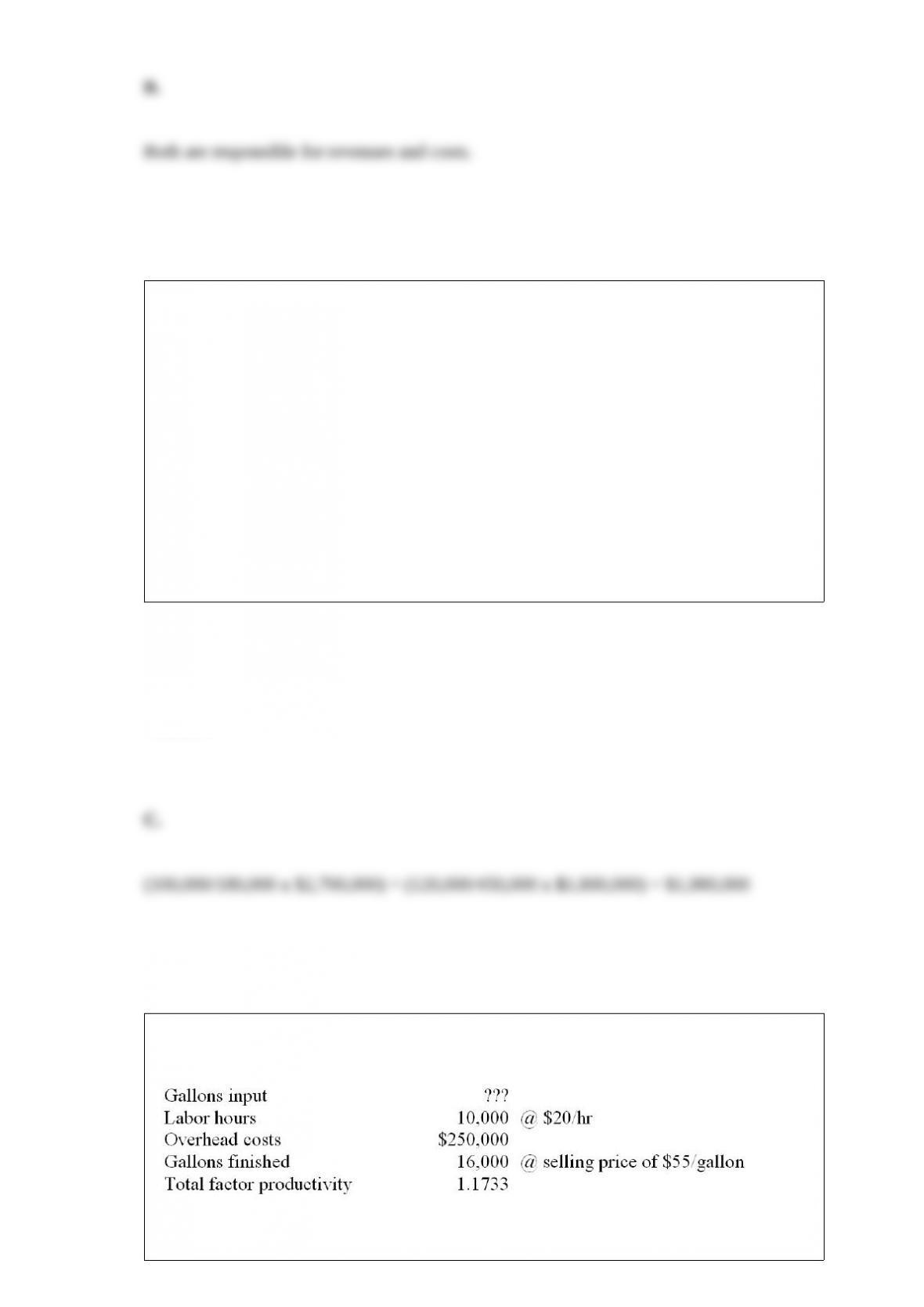

The number of services provided by an accounting firm would be classified as a(n)

A. volume-related activity.

B. batch-related activity.

C. product-related activity.

D. facility-related activity.

Answer:

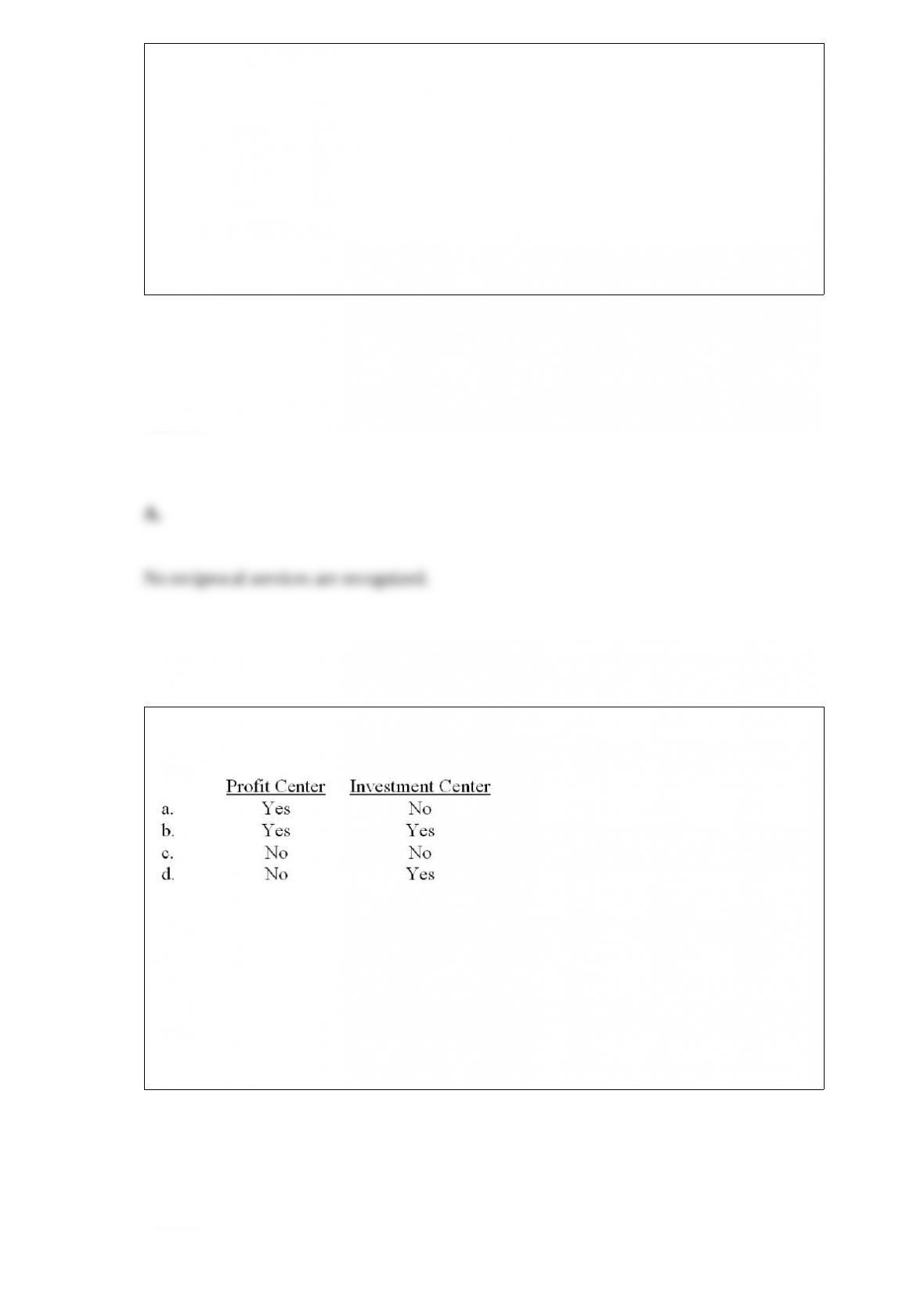

Responsibility accounting defines an operating center that is responsible for revenue

and costs as a(n) (CMA adapted)

A. profit center.

B. revenue center.

C. division.

D. operating unit.

E. investment center.

Answer:

In general, the terms favorable and unfavorable are used to describe the effect of a

variance on

A. net income.

B. sales revenue.

C. production costs.

D. operating expenses.

E. balance sheet.

Answer:

A hybrid costing system that is often used when manufacturing goods that have some

common characteristics plus some individual characteristics is called:

A. continuous flow process.

B. cost management system.

C. two-stage allocation system.

D. operations cost.

Answer:

Which of the following statements regarding differential costs is (are) false?

(A) The full cost fallacy occurs when a decision-maker fails to include fixed

manufacturing overhead in the product’s cost.

(B) When deciding whether or not to accept a special order, a decision-maker should

focus on differential costs instead of full costs.

A. Only A.

B. Only B.

C. Neither A nor B is false.

D. Both A and B are true.

Answer:

Which of the following performance measures would be used to evaluate the personnel

department performance?

A. Number of product recalls

B. Percentage of late deliveries

C. Number of requests for transfers

D. Length of time to fill vacant positions

Answer:

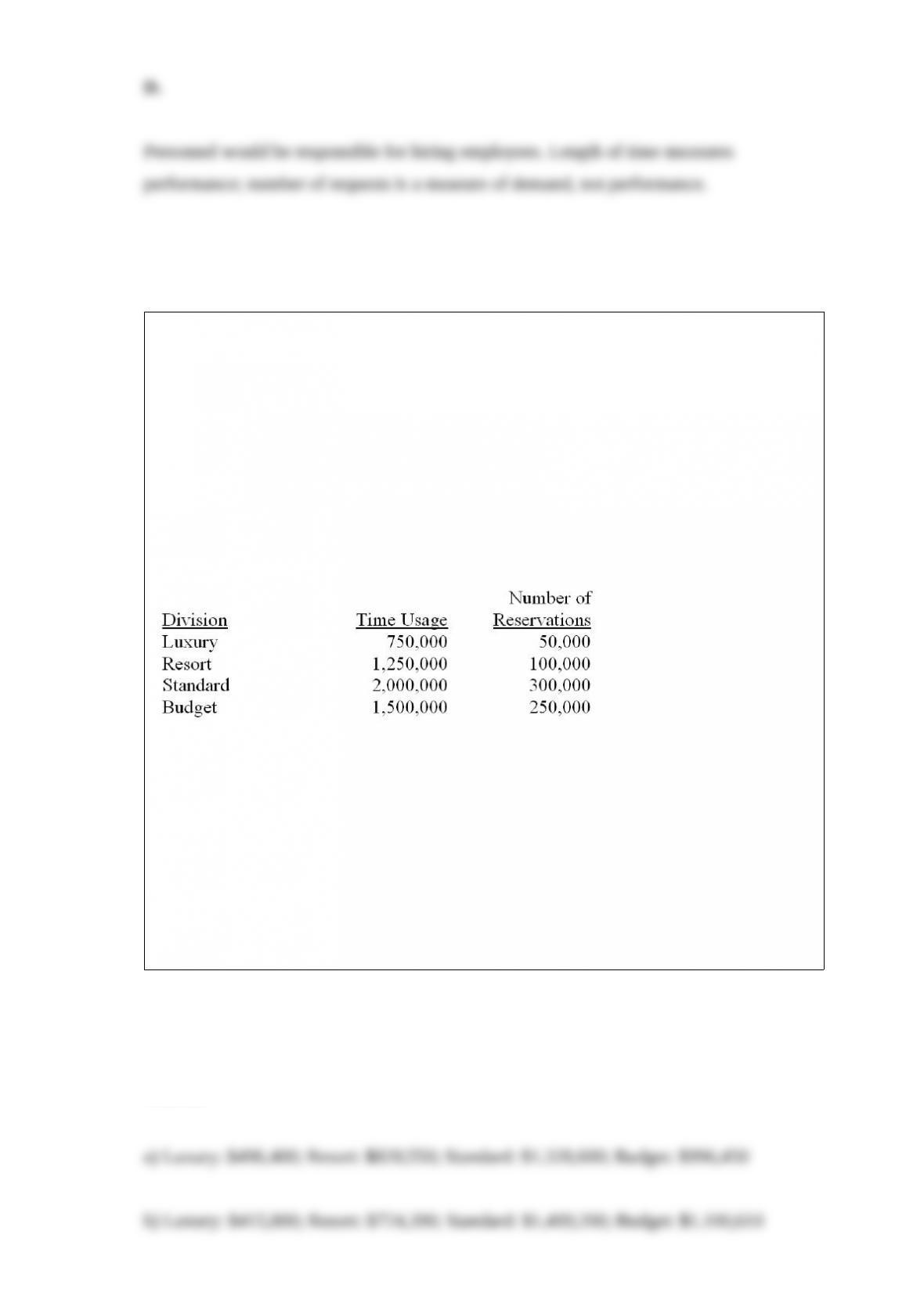

Atlantic Hotels operates a centralized call center for the reservation needs of its

time-share units. Costs associated with use of the center are charged to the time-share

group (Luxury, Resort, Standard, and Budget) where a reservation is made on the basis

of time on a call. Idle time of the reservation agents, time spent on calls where no

reservation is made, and the fixed cost of the equipment are allocated on the number of

reservations made in each group. Due to recent increased competition in the time-share,

the company has decided that it is necessary to more accurately allocate its costs to

price its services competitively and profitably. During the current period, the use of the

call center for each group was as follows (in thousands of seconds for time usage and in

number of reservations):

During this period, the cost of the computer center amounted to $2,410,000 for

personnel and $1,240,000 for equipment and other costs.

Required Determine the allocation to each of the divisions using (you may round all

decimals to three places):

a) A single rate based on time used.

b) Multiple rates based on time used (for personnel costs) and number of reservations

(for equipment and other cost).

Answer:

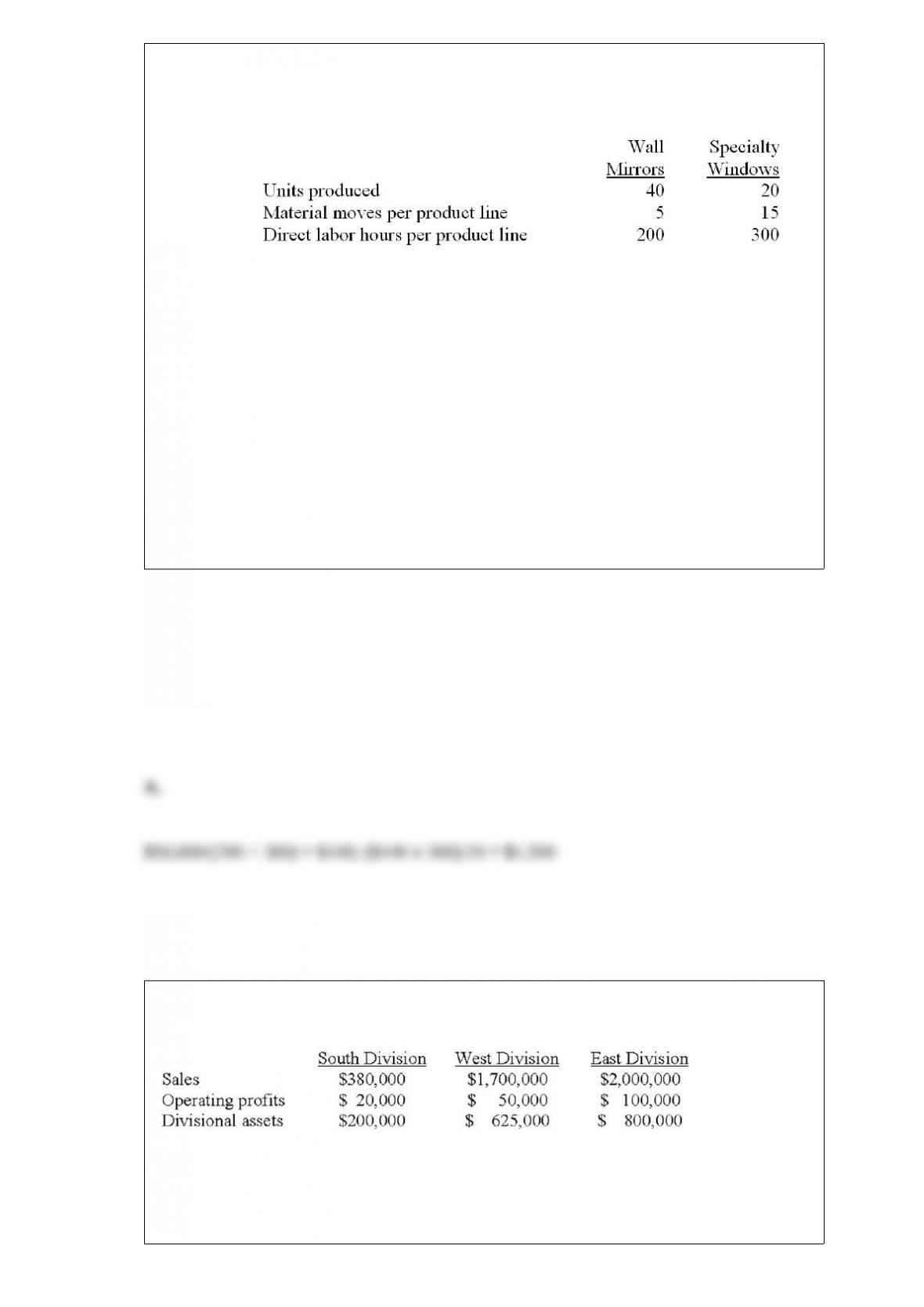

Zela Company is preparing its annual profit plan. As part of its analysis of the

profitability of individual products, the controller estimates the amount of overhead that

should be allocated to the individual product lines from the information provided below.

(CMA based)

Budgeted material handling costs: $50,000

Under a traditional costing system that allocates overhead on the basis of direct labor

hours, the materials handling costs allocated to one unit of specialty windows would be

A. $1,500

B. $500

C. $2,000

D. $5,000

Answer:

The Multidivision Corporation reported the following operating results for its three

divisions: South, West, and East.

Which division’s profit margin is the highest?

A. South

B. West

C. East

D. All three divisions are the same

Answer:

If both the variable cost per unit and the selling price per unit decrease, the new

contribution margin ratio in relation to the old contribution margin ratio will be:

A. Lower.

B. Higher.

C. Unchanged.

D. Not enough information to tell.

Answer:

Acme Sales has two store locations. Store A has fixed costs of $125,000 per month and

a variable cost ratio of 60%. Store B has fixed costs of $200,000 per month and a

variable cost ratio of 30%. What is the break-even sales volume for Store A?

A. $208,333

B. $312,500

C. $325,000

D. Cannot determine with the information given.

Answer:

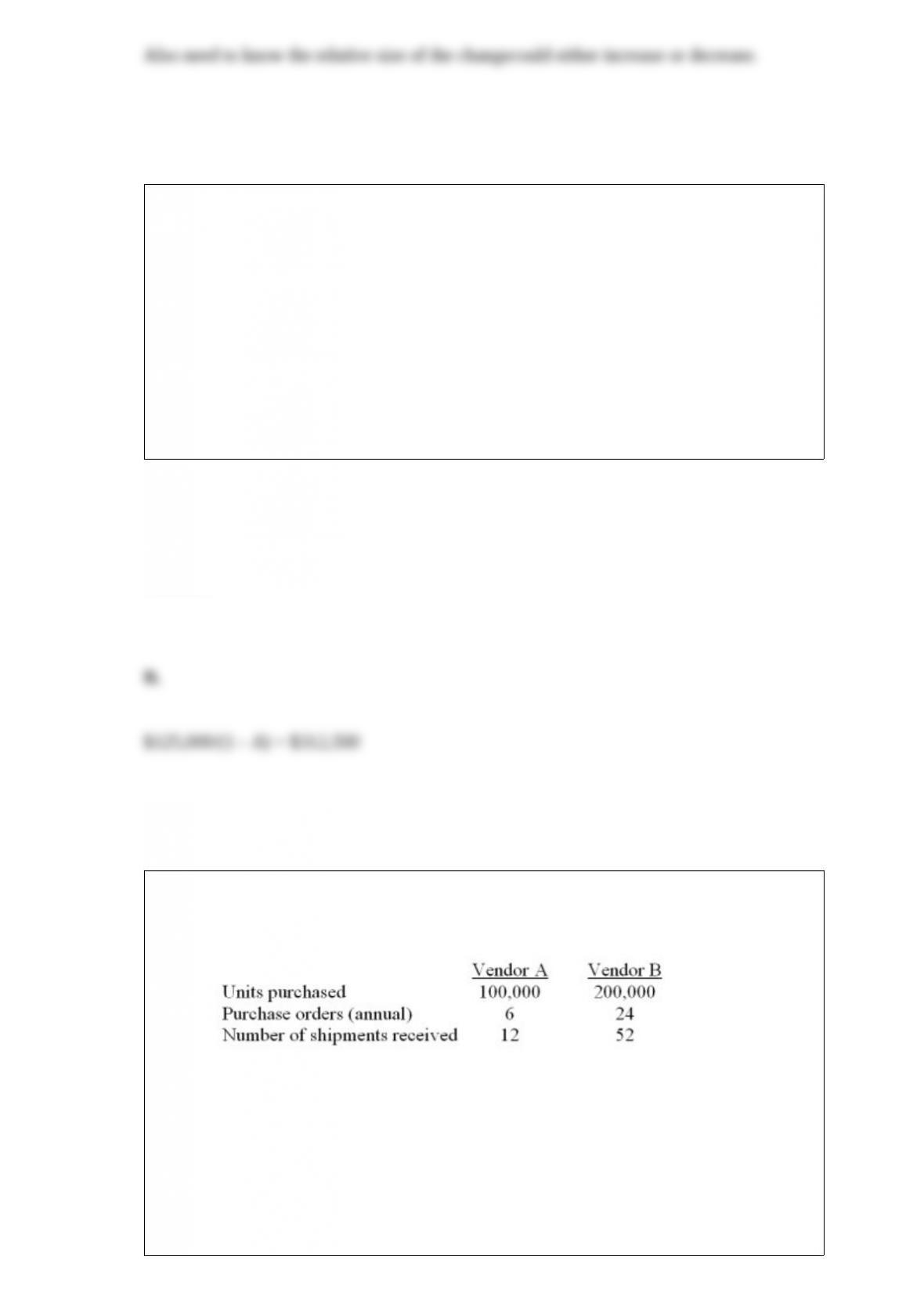

Rogers Company is preparing its annual profit plan. As part of its analysis of the cost

of its purchasing activity, management estimates that the $48,000 for purchasing

support should be assigned to the individual vendors from the information given as

follows:

What is the amount of the purchasing costs that should be allocated to Vendor A

assuming Rogers uses number of shipments received to compute activity-based costs?

A. $9,000

B. $16,000

C. $32,000

D. $39,000

Answer:

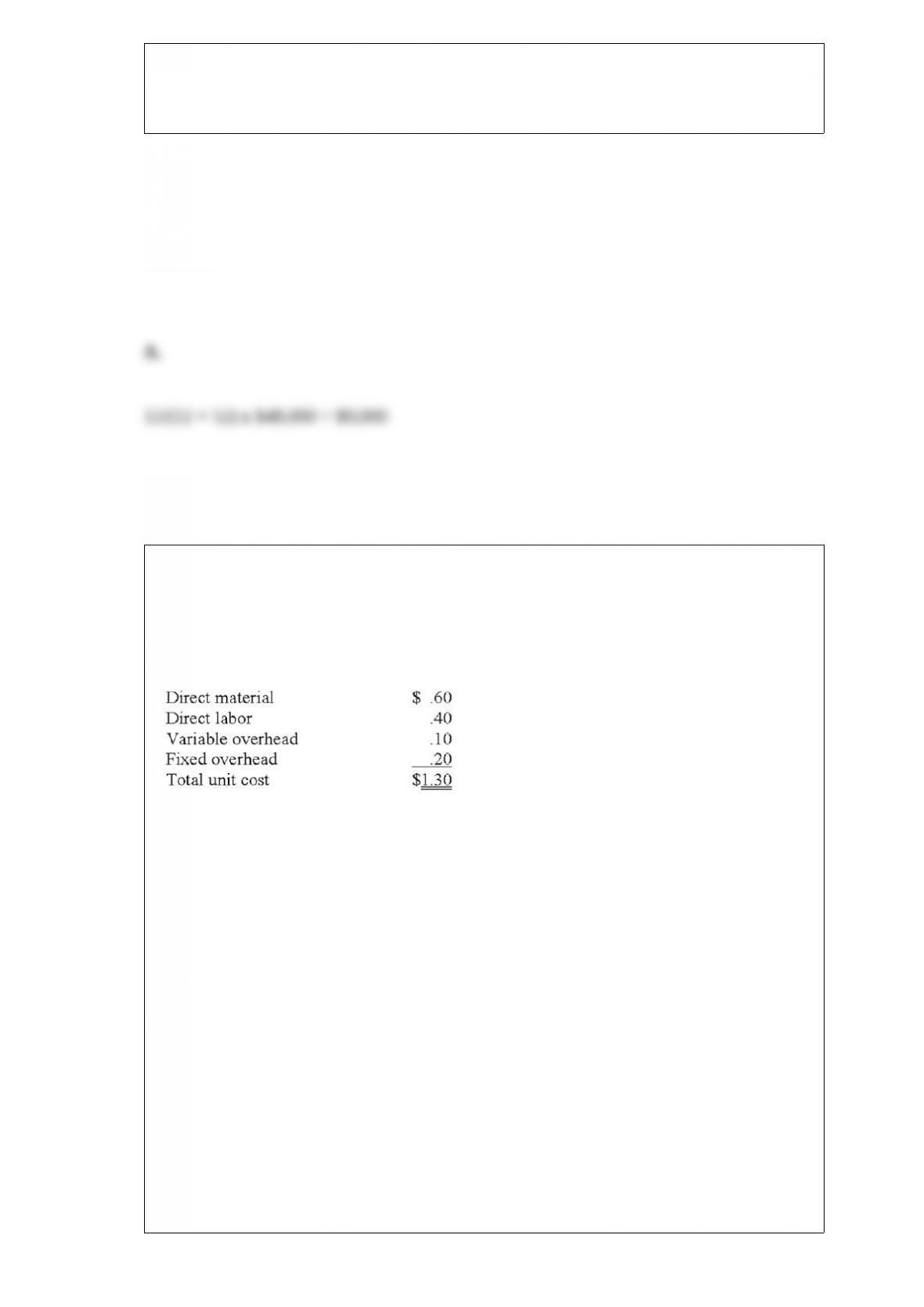

Cohasset Company currently manufactures all component parts used in the

manufacture of various hand tools. Hurley Division produces a steel handle used in

three different tools. The budget for these handles is 120,000 units with the following

unit cost.

Ironwood Division purchases 20,000 handles from Hurley Division and completes the

hand tools. An outside supplier, R & M Steel, has offered to supply 20,000 units of the

handle to Ironwood Division for $1.25 per unit. Hurley currently has idle capacity that

cannot be used.

What is the cost impact to Cohasset as a whole of purchasing from R & M Steel? (CMA

adapted)

A. increase the handle unit cost by $.05.

B. increase the handle unit cost by $.15.

C. decrease the handle unit cost by $.15.

D. decrease the handle unit cost by $.25.

E. decrease the handle unit cost by $.05.

Answer:

The Muskego National Bank is considering either a bankwide overhead rate or

department overhead rates to allocate $250,000 of indirect costs. The bankwide rate

could be based on either direct labor hours (DLH) or the number of loans processed.

The departmental rates would be based on direct labor hours for Consumer Loans and a

dual rate based on direct labor hours and the number of loans processed for Commercial

Loans. The following information was gathered for the upcoming period:

If Muskego uses a bankwide rate based on direct labor hours, what would be the

indirect costs allocated to the Commercial Department?

A. $100,000

B. $150,000

C. $250,000

D. $350,000

Answer:

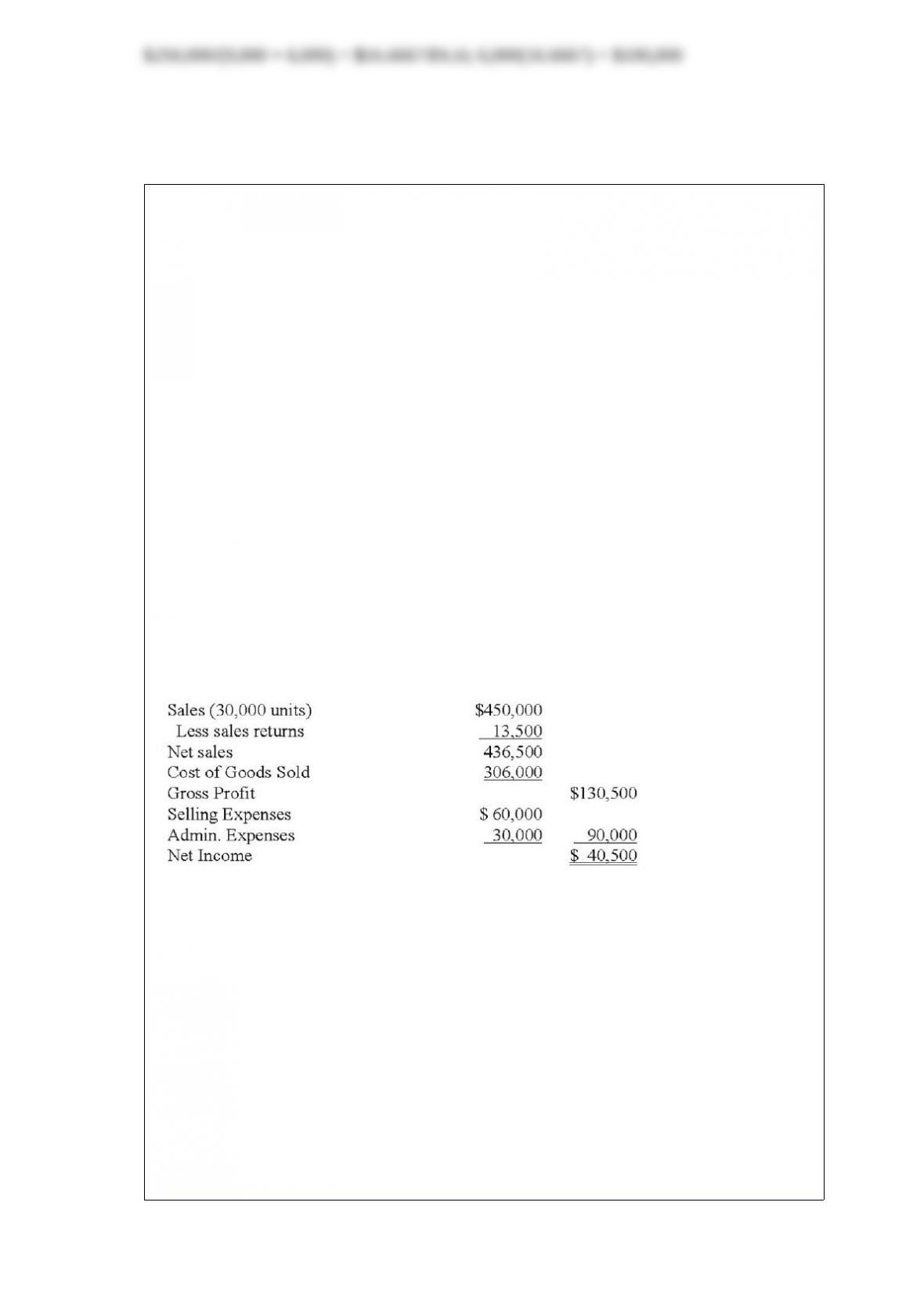

Hawle Manufacturing Company is in the process of preparing its 2010 budget and is

anticipating the following changes:

30% increase in the number of units sold

20% increase in the direct material unit cost

15% increase in the direct labor cost per unit

10% increase in the manufacturing overhead cost per unit

14% increase in the selling price

7% increase in the administrative expenses

Hawle does not keep any units in inventory.

The composition of the cost of finished products during 2010 for materials, direct labor

and factory overhead, respectively, was in the ratio of 3 to 2 to 1. The condensed

income statement for 2009 is as follows:

What are estimated net sales for 2010, assuming the sales return/gross sales relationship

remains constant?

A. $646,893

B. $585,000

C. $571,500

D. $567,450

E. $553,950

Answer:

The Work-in-Process Inventory account of a manufacturing firm has a balance of

$2,400 at the end of an accounting period. The job cost sheets of two uncompleted jobs

show charges of $400 and $200 for materials used, and charges of $300 and $500 for

direct labor used. Overhead is applied as a percentage of direct labor costs. The

predetermined rate is

A. 41.7%.

B. 80.0%.

C. 125.0%.

D. 240.0%.

Answer:

Criteria for selecting allocation bases for service department allocations should not

include

A. direct, traceable benefits from the service.

B. the extent of facilities provided.

C. the ease of making an allocation.

D. sales dollars generated during the period.

Answer: