Ethics and laws often differ.

Chuck Taylor invested $8,000 in cash in FastForward. This amount would be reported

in the statement of cash flows under financing.

The conceptual framework summarizes the qualitative characteristics and supportive

building blocks that are required to prepare financial information.

One of the most important decisions in accounting for inventory is determining the

per-unit costs assigned to inventory items.

The equity in a partnership belongs to one owner.

Quick assets include cash, inventory, and receivables.

Correcting entries are a specialized type of adjusting entry.

When businesses apply the lower of cost and net realizable value rule on an item by

item basis, they will report the lowest inventory value possible.

Financial statements are an organization’s primary means of financial communication

and are the end result of a process, or a cycle, which begins with a business transaction

like a sale.

Z-Mart did not take advantage of a supplier’s offer of 2/10, n/30, and paid the invoice at

the end of the month. By not taking the discount Z-Mart lost the equivalent of 18%

annual interest on the amount of the purchase.

The periodic inventory system is superior to the perpetual inventory system in

preventing shrinkage.

Revenue and expense accounts are permanent accounts and should not be closed at the

end of the fiscal period.

A retailer is a middleman that buys products from manufacturers and sells them to

wholesalers.

The Purchases Journal is the same in both the periodic and perpetual systems.

The natural business year for businesses is always the same as the calendar year.

If Cash Over and Short has a debit at the end of the period, the dollar amount represents

miscellaneous revenue.

If you fail to record accrued salaries at the end of the month, net income for the month

will be overstated.

Provincial sales tax (PST) is normally calculated on the original purchase price plus the

goods and services tax (GST) or Harmonized Sales Tax (HST).

The percentage of sales approach for estimating bad debts is based on the idea that a

percent of a company’s credit sales for the period are uncollectible.

If an account was incorrectly debited for $300 instead of correctly credited for $300, the

account is out of balance by $300.

The materiality principle requires that the inventory valuation method follow the flow

of goods.

The report format is considered to be the only correct format for the balance sheet.

Two common subsidiary ledgers are cash receipts and cash disbursements.

Cost of goods sold represents the cost of buying and preparing merchandise for sale.

The steps to reconcile the balance of the bank statement to the adjusted balance include

adding outstanding cheques, deposits, and bank service charges to the bank balance.

The preferred ethical path is to take a course of action that avoids casting doubt on one’s

decisions.

It is a bad business practice to accept a note receivable in exchange for an overdue

account receivable.

The days’ sales uncollected ratio measures a company’s ability to manage its debt.

A perpetual inventory system is able to directly measure shrinkage.

The closing process is a step in the accounting cycle that prepares accounts for the next

accounting period.

Omega Supply’s current ratio is 2 to 1. Its acid test ratio is .75 to 1. Omega Supply is a

good credit risk because the ratios reveal no liquidity problem.

Periodic inventory systems were historically used by companies that sold large

quantities of low-value items.

The Accounts Payable ledger is used for storing transaction data regarding individual

customers.

Assets are classified into current assets, investments, property, plant and equipment, and

intangible assets.

If a company sells products and receives from the customer a formal written promise to

pay a definite sum of money on demand or on a defined future date (or dates), the seller

should debit the promised amount to Accounts Receivable.

Source documents are a group of components that collect and process raw financial data

into timely, accurate, relevant, and cost-effective information to meet the purposes of

internal and external users.

TechCom customer RDA Electronics paid off an $8,300 balance on its account

receivable. TechCom should record the transaction as a debit to Accounts

Receivable-RDA Electronics and a credit to Cash.

An obligation of a business that represents the claims of others against the assets of the

business is called a(n):

A. Asset.

B. Expense.

C. Revenue.

D. Equity.

E. Liability.

An individual or organization entitled to receive payments from a business is known to

the business as a:

A. Debtor.

B. Shareholder.

C. Controller.

D. Creditor.

E. Bookkeeper.

Pledging receivables:

A. Allow firms to raise cash.

B. Allow firms to retain ownership of receivables.

C. Transfer risk of bad debt to the lender.

D. Allow firms to raise cash and retain ownership of receivables.

E. All of these answers are correct.

The agreed cost of an item to be purchased by a business on credit is $4,000. The

applicable cost will be debited to advertising expense. The item is subject to 5% goods

and services tax (GST) and 7% provincial sales tax (PST). When this transaction is

recorded, what amount will be debited to advertising expense?

A. $4,000

B. $4,200

C. $4,280

D. $4,480

E. None of these answers is correct.

Source documents:

A. Are input devices.

B. Provide basic information processed by an accounting system.

C. Can be electronic files.

D. Both provide basic information processed by an accounting system and can be

electronic files.

E. All of these answers are correct.

A good system of internal control:

A. Encourages adherence to prescribed managerial policies.

B. Promotes operational efficiencies.

C. Eliminates the need for an audit.

D. Both encourages adherence to prescribed managerial policies and promotes

operational efficiencies.

E. All of these answers are correct.

The total amount of depreciation recorded for an asset during the entire time the asset

has been owned:

A. Is not shown on the balance sheet.

B. Is referred to as accumulated depreciation.

C. Is shown on the income statement.

D. Is shown on the statement of changes in equity.

E. Is recorded in a liability account.

Accounting information systems:

A. Collect and process data from events and transactions.

B. Organize data in useful forms.

C. Communicate information to decision makers.

D. Both collect and process data from events and transactions and organize data in

useful forms.

E. All of these answers are correct.

Limitations of internal control include:

A. Human error.

B. Human fraud.

C. Cost-benefit standard.

D. Human error and fraud.

E. All of these answers are correct.

Net income is:

A. Assets minus liabilities.

B. The excess of revenues over expenses.

C. The excess of expenses over revenues.

D. A revenue.

E. The same as equity.

Incurred but unpaid expenses that are recorded during the adjusting process with a debit

to an expense and a credit to a liability are called

A. Operating expenses.

B. Prepaid expenses.

C. Unearned expenses.

D. Accounts payable.

E. Accrued expenses.

The fees charged businesses by banks on credit card transactions can be shown on the

income statement as:

A. A discount from revenue used in determining net sales.

B. A selling expense.

C. An administrative expense

D. All of these answers are correct.

E. None of these answers is correct.

A company uses a Sales Journal, a Purchases Journal, a Cash Receipts Journal, a Cash

Disbursements Journal, and a General Journal. A sales return for credit on account

would be recorded in the:

A. Sales Journal.

B. General Journal.

C. Cash Receipts Journal.

D. Accounts Receivable Ledger.

E. Cash Disbursements Journal.

The matching principle requires:

A. That bad debt expenses be reported in the same accounting period as the sales they

helped generate.

B. That bad debt expenses be reported in the same accounting period as the sales they

helped generate and requires the use of the allowance method of accounting for bad

debts.

C. The use of the allowance method of accounting for bad debts.

D. That bad debt expenses be reported in the same accounting period as the sales they

helped generate and requires the use of the direct write-off method for bad debts.

E. The use of the direct write-off method for bad debts.

The right side of a T-account is a(n):

A. Debit.

B. Increase.

C. Credit.

D. Decrease.

E. Account balance.

The accounting equation can be stated as:

A. Assets = non-owner equity + equity.

B. Liabilities = assets – equity.

C. Assets = liabilities + equity.

D. Equity = assets – liabilities.

E. All of these answers are correct.

The eight recurring steps performed each accounting period, starting with recording

transactions in the journal and continuing through the post-closing trial balance, is

called the:

A. Accounting period.

B. Operating cycle.

C. Accounting cycle.

D. Closing cycle.

E. Natural business year.

Accounting information system components include:

A. People.

B. Input data.

C. Software.

D. Hardware.

E. All of these answers are correct.

A perpetual inventory system:

A. Gives a continuous record of the amount of inventory on hand.

B. Uses a Purchases account for the cost of new merchandise purchased.

C. Was historically used by companies that sold large quantities of low-value items.

D. Is not widely used in practice.

E. All of these answers are correct.

2/10, n/30 is interpreted as:

A. 2% cash discount if the whole amount is paid within 10 days, the balance is due in

30 days.

B. 10% cash discount if the whole amount is paid within 2 days, the balance is due in

30 days.

C. 30% discount if paid within 2 days.

D. 30% discount if paid within 10 days.

E. 2% discount if paid within 30 days.

If assets are $144,000 and liabilities are $37,000, then equity equals:

A. $37,000.

B. $74,000.

C. $107,000.

D. $144,000.

E. $181,000.

The days’ sales uncollected ratio is used to:

A. Measure how many days of sales remain until the end of the year.

B. Determine the number of days that have passed without collecting on accounts

receivable.

C. Identify the likelihood of collecting sales on account.

D. Estimate how much time is likely to pass before cash receipts from credit sales equal

the current amount of accounts receivable.

E. Measure the amount of layaway sales for a period.

Payments of cash by a corporation to its shareholders are called:

A. Dividends.

B. Cheques.

C. Shareholders equity.

D. Withdrawals.

E. Expenses.

Reversing entries:

A. Are optional.

B. Are mandatory.

C. Fix errors in journal entries.

D. Are required by CRA.

E. Are not posted to the ledger.

Internal controls are procedures set up to:

A. Protect assets.

B. Ensure accounting reports are free from error, neutral and complete.

C. Promote efficiency.

D. Ensure company policies are followed.

E. All of these answers are correct.

The impact of technology on internal controls includes:

A. Reduced processing errors.

B. Elimination of the need for regular audits.

C. Fewer hard copies of source documents.

D. More efficient separation of duties.

E. Reduced processing errors and fewer hard copies of source documents.

Source documents:

A. Do not provide objective evidence about transactions.

B. Are a source of accounting information.

C. Can only be in electronic form.

D. Are only used for audit purposes.

E. Are acceptable as a substitute for financial statements.

Accounts that are used to describe revenues, expenses, and owner’s withdrawals, and

are closed at the end of the reporting period, are:

A. Real accounts.

B. Temporary accounts.

C. Closing accounts.

D. Permanent accounts.

E. Ledger accounts.

Revenues are:

A. Profits.

B. The amount a business earns after subtracting all expenses from sales.

C. Business events.

D. Net assets.

E. The value of assets exchanged for goods or services provided to the customer.

The expense created by allocating the cost of plant and equipment to the periods in

which they are used, representing the expense of using the assets, is called:

A. Accumulated depreciation.

B. The cash basis of accounting.

C. The matching principle.

D. Depreciation.

E. Allowance for depreciation.

Discuss the importance of periodic reporting and the timeliness principle.

The amount that an asset can be sold for is called its _________________.

Using the information from Lucie Accounting (Ref 4-1), calculate the current ratio.

The following accounts appear on either the Income Statement (IS) or Balance Sheet

(BS). In the space provided next to each account write the letters, IS or BS, that identify

the statement on which the account appears.

__________________________ consist of people, records, methods, and equipment.

TechCom had net sales of $315,000 and average accounts receivable of $75,600. Its

competitor, ZCom, had net sales of $299,000 and average accounts receivable of

$81,350. Calculate the accounts receivable turnover ratio for both companies. Which

company is doing a better job of managing its accounts receivable (all other things

assumed to be equal)?

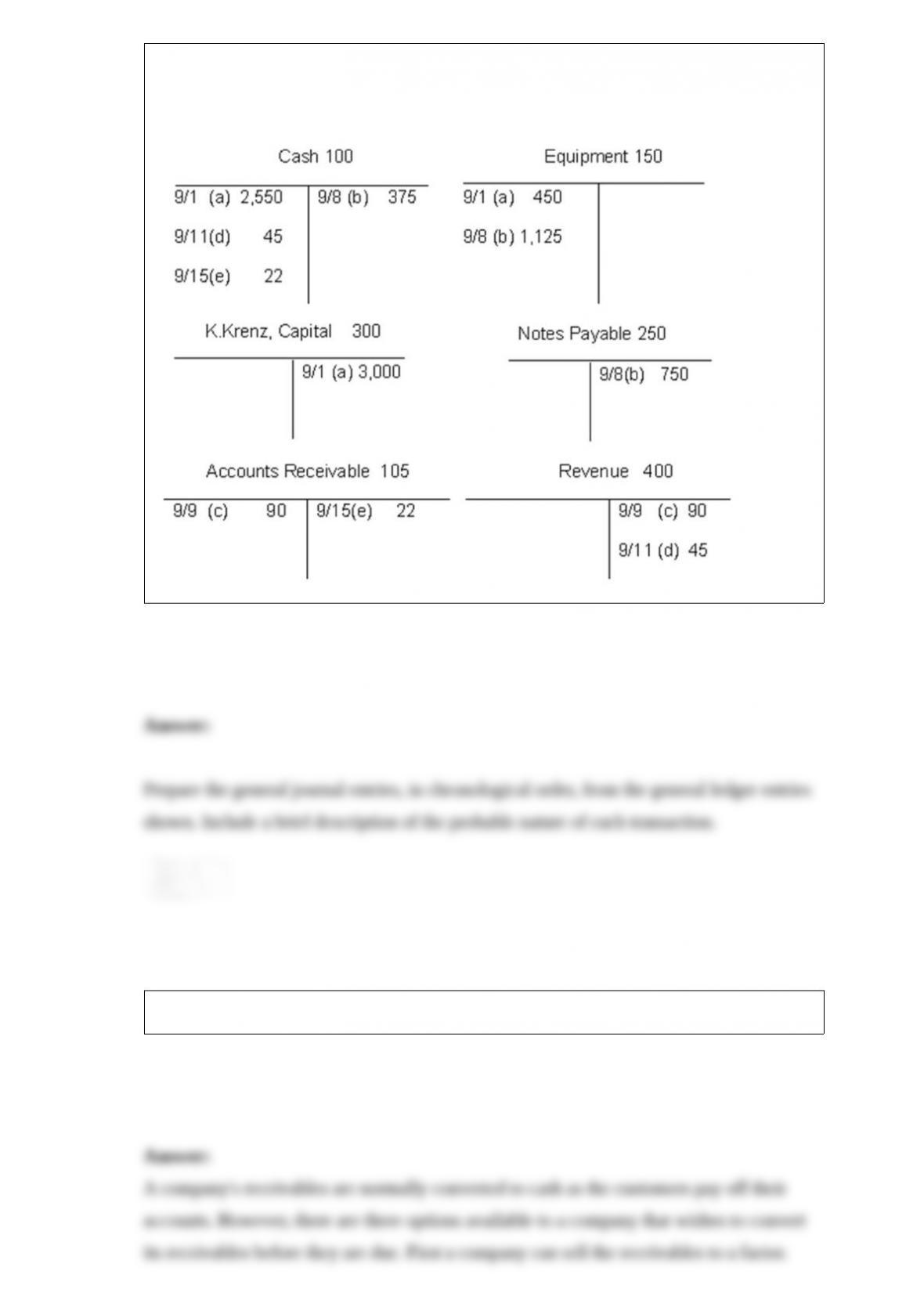

Krenz Kar Kare, owned and operated by Karl Krenz, began business in September of

the current year. Karl, a master mechanic, had no experience with keeping a set of

books. As a result, Karl entered all of September’s transactions directly to the General

Ledger accounts. When he tried to locate a particular entry originally made on

September 8, he found it confusing and time-consuming. He has hired you to improve

his bookkeeping procedures. The accounts in his General Ledger follow:

How can a company convert its receivables to cash?