On January 1, 2016, Glanville Company sold goods to Otter Corporation. Otter signed

an installment note requiring payment of $15,000 annually for six years. The first

payment was made on January 1, 2016. The prevailing rate of interest for this type of

note at date of issuance was 8%. Glanville should record sales revenue in January 2016

of:

a. $90,000.

b. $69,343.

c. $74,891.

d. None of these answer choices is correct.

Which of the following is most true regarding consignment arrangements?

a. Revenue is recognized at the point in time when the consignment arrangement is

made.

b. Revenue is recognized when goods are transferred to the consignee.

c. Revenue is recognized upon sale by the consignee to an end customer.

d. Revenue is never recognized because GAAP does not allow such arrangements.

Ireland Corporation obtained a $40,000 note receivable from a customer on June 30,

2016. The note, along with interest at 6%, is due on June 30, 2017. On September 30,

2016, Ireland discounted the note at Cloverdale bank. The bank’s discount rate is 10%.

What amount of cash did Ireland receive from Cloverdale Bank?

a. $40,600.

b. $36,000.

c. $39,220.

d. $36,820.

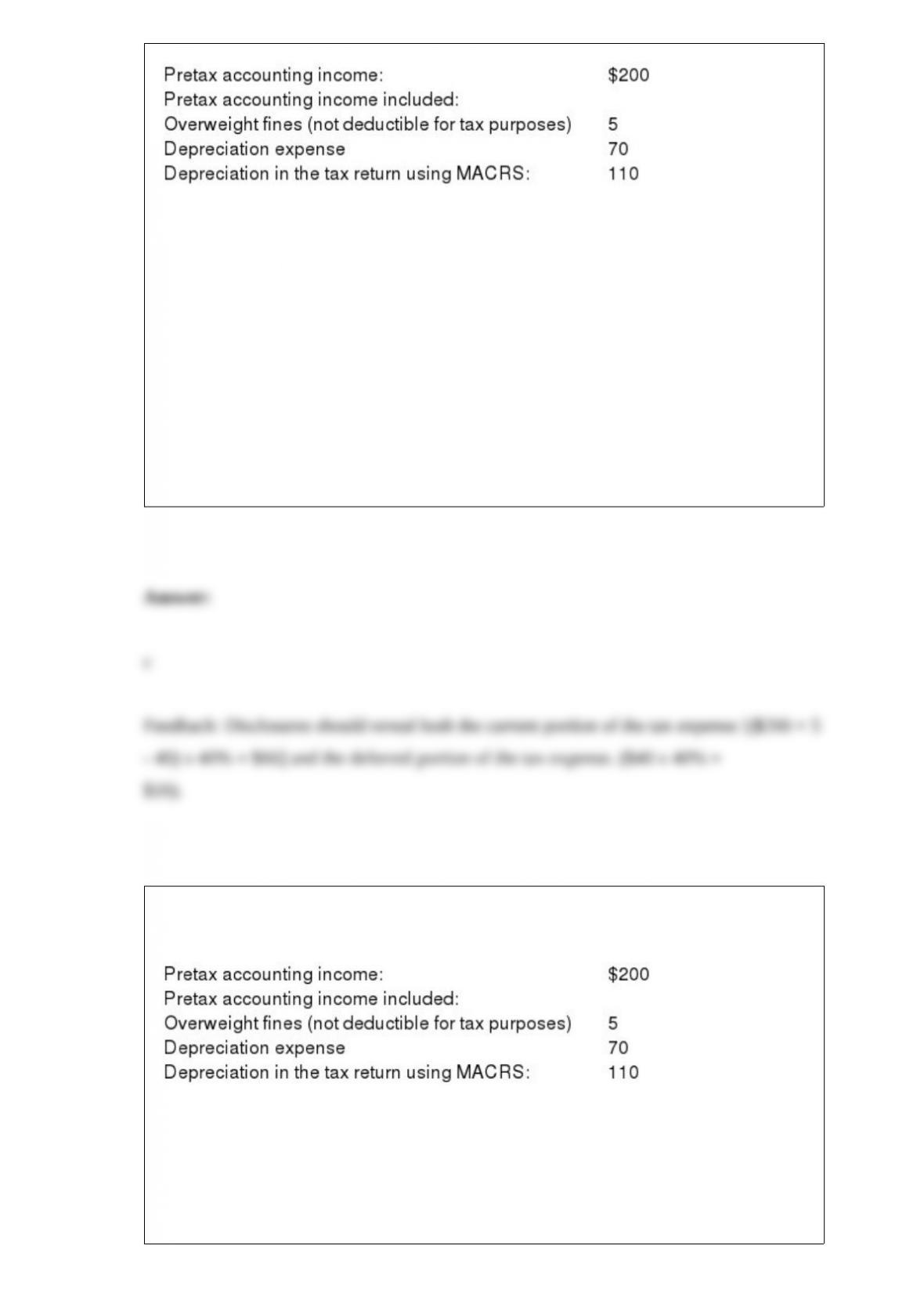

The following information relates to Franklin Freightways for its first year of

operations (data in millions of dollars):

The applicable tax rate is 40%. There are no other temporary or permanent differences.

Which of the following must Franklin Freightways disclose related to the income tax

expense reported in the income statement ($ in millions)?

a. Only the current portion of tax expense of $66.

b. Only the total tax expense of $82.

c. Both the current portion of the tax expense of $66 and the deferred portion of the tax

expense of $16.

d. None of these answer choices are correct.

The following information relates to Franklin Freightways for its first year of

operations (data in millions of dollars):

The applicable tax rate is 40%. There are no other temporary or permanent differences.

Franklin Freightways experienced ($ in millions) a current:

a. Tax liability of $66.

b. Tax liability of $36.

c. Tax liability of $70.6.

d. Tax benefit of $10 due to the NOL.

Cash flows from financing activities include:

a. Interest received.

b. Interest paid.

c. Dividends received.

d. Dividends paid.

FIFA Footballs acquired a patent in 2013 at a cost of $150 million and amortizes the

patent on a straight-line basis. During 2016 management decided that the benefits from

the patent would be received over a total period of 8 years rather than the 20-year legal

life being used to amortize the cost. FIFA’s 2016 financial statements should include:

a. A patent balance of $150 million.

b. A patent balance of $102 million.

c. Patent amortization expense of $15 million.

d. Patent amortization expense of $7.5 million.

AMC issues a note with no stated interest rate in exchange for a machine. In accounting

for the transaction:

a. The machine should be depreciated over the note’s term to maturity.

b. If fair values of the note and machine are unavailable, the note should be recorded at

its present value, discounted at the market rate of interest.

c. Both the note and machine are recorded at the face amount of the note or the fair

value of the machine, whichever is more clearly determinable.

d. The note is recorded at its face amount unless the fair value of the machine is readily

available.

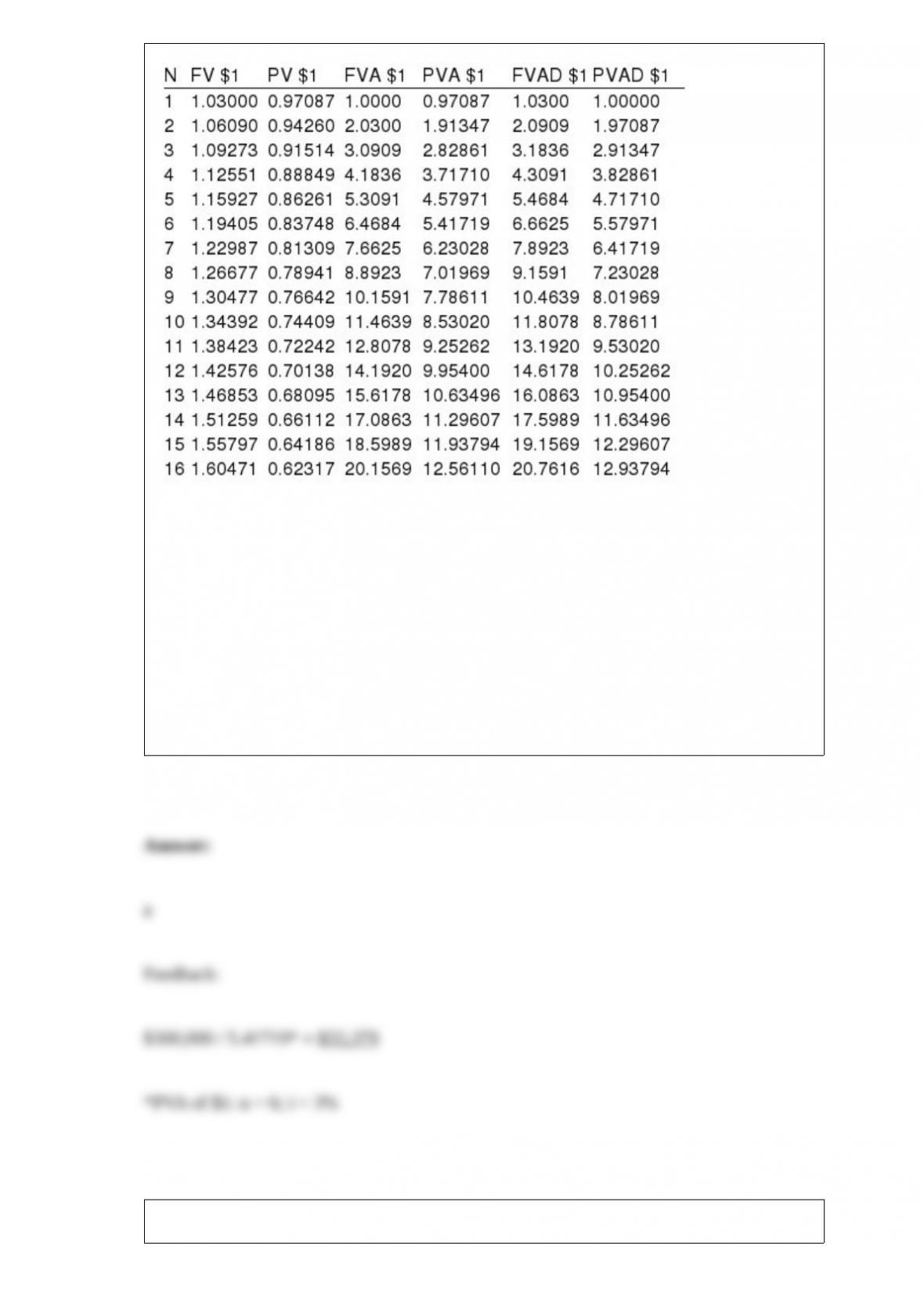

Present and future value tables of $1 at 3% are presented below:

Micro Brewery borrows $300,000 to be paid off in three years. The loan payments are

semiannual with the first payment due in six months, and interest is at 6%. What is the

amount of each payment?

a. $ 55,379.

b. $106,059.

c. $ 30,138.

d. $ 60,276.

Which of the following is not an identified valuation technique in GAAP regarding fair

value measurement?

a. Cost approach.

b. Market approach.

c. Cost-benefit approach.

d. Income approach.

When the service method is used for amortizing prior service costs, the amount

recognized each year is:

a. In proportion to the fraction of the total remaining service years worked during the

year.

b. A constant amount or fixed amount.

c. Prior service cost divided by the average remaining service life of the active

employee group.

d. Prior service cost divided by the average estimated retirement age of the currently

enrolled employee group.

Companies recognize revenue only when

a. A contract is reasonably likely to exist

b. A performance obligation is designated in a written contract

c. A written contract is in place and payment is variable

d. Control over goods or services has been transferred from the seller to the customer

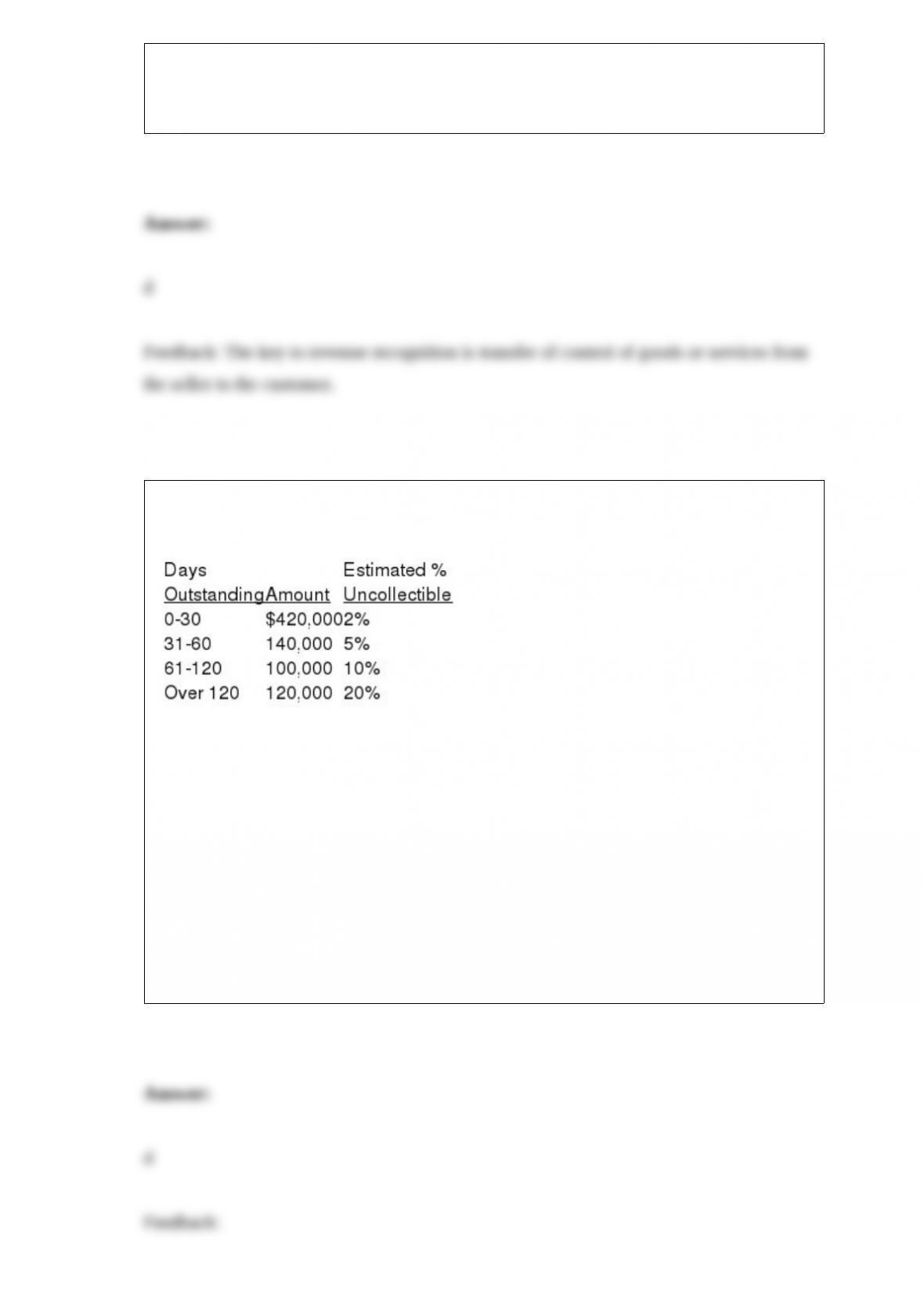

The following information pertains to Jacobsen Co.’s accounts receivable at December

31, 2016:

During 2016, Jacobsen wrote off $18,000 in receivables and recovered $6,000 that had

been written off in prior years. Jacobsen’s December 31, 2015, allowance for

uncollectible accounts was $40,000. Under the aging method, what amount of

allowance for uncollectible accounts should Jacobsen report at December 31, 2016?

a. $28,000.

b. $31,400.

c. $55,400.

d. $49,400.

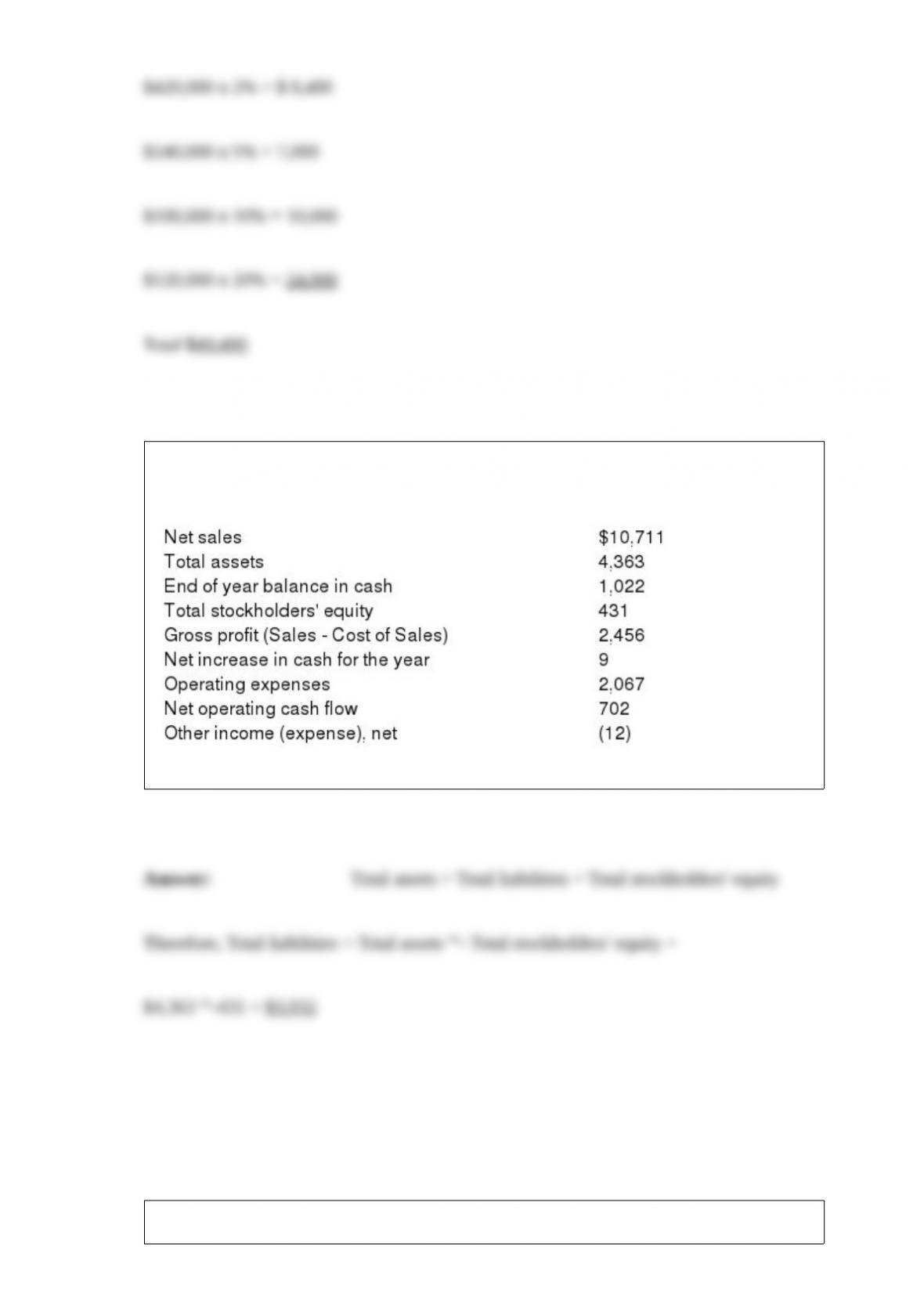

The following information ($ in millions) comes from a recent annual report of

Amazon.com, Inc.:

Compute Amazon’s total liabilities at the end of the year.

Briefly explain the disclosures that are required relative to depreciable assets.

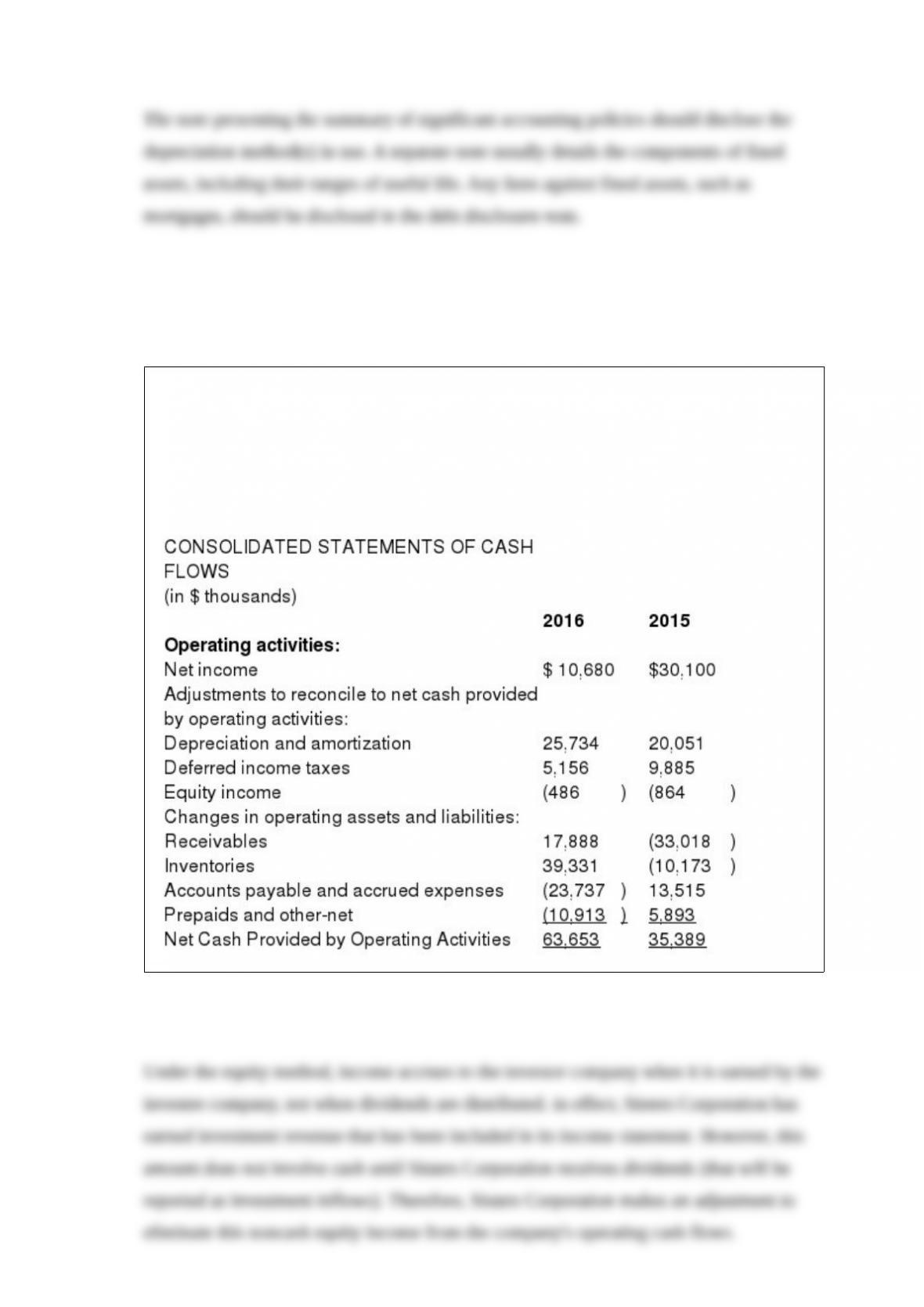

Explain why Sisters Corporation subtracts equity income from its net income in its

measurement of cash flows.

In its 2016 Annual Report to Shareholders, Sisters Corporation included the following

information on cash flows from operations:

On December 31, 2015, Witherspoon Services had 800,000 shares of common stock

and 200,000 shares of 5.5%, noncumulative, nonconvertible $10 par preferred stock

issued and outstanding.

On March 2, 2016, Witherspoon sold 120,000 common shares. In keeping with its

long-term share repurchase plan, 30,000 shares were retired on August 31. Witherspoon

distributed a 10% common stock dividend on June 3. Witherspoon’s net income for the

year ended December 31, 2014, was $600,000. The company paid cash dividends of

$110,000 to preferred shareholders on December 20, 2016. The income tax rate is 40%.

Required:

Compute Witherspoon’s earnings per share for the year ended December 31, 2016.

On the last day of its fiscal year ending December 31, 2016, the Boatright Ship Builders

completed two financing arrangements. The funds provided by these initiatives will

allow the company to expand its operations.

1> Boatright issued 6% stated rate bonds with a face amount of $200 million. The

bonds mature on December 31, 2036 (20 years). The market rate of interest for similar

bond issues was 8% (4% semiannual rate). Interest is paid semiannually (3%) on June

30 and December 31, beginning on June 30, 2017.

2> The company leased two manufacturing facilities. Lease A requires 10 annual lease

payments of $50,000 beginning on January 1, 2017. Lease B also is for 10 years,

beginning January 1, 2017. Terms of the lease require seven annual lease payments of

$60,000 beginning on January 1, 2020. Accounting standards require both leases to be

recorded as liabilities for the present value of the scheduled payments. Assume that an

8% interest rate properly reflects the time value of money for the lease obligations.

Required:

What amounts will appear in Boatright’s December 31, 2016, balance sheet for the

bonds and for the leases?

Briefly describe the differences between an ordinary annuity, an annuity due, and a

deferred annuity.

Using an example, discuss the techniques that analysts use to transform accounting

numbers into more useful forms.