1) When auditors evaluate sales returns and allowances, a primary emphasis is on the

objective of occurrence.

A) True

B) False

2) The underlying reason for a code of professional conduct for any profession is:

A) the need for public confidence in the quality of service of the profession

B) that it provides a safeguard to keep unscrupulous people out

C) that it is required by federal legislation

D) that it allows licensing agencies to have a yardstick to measure deficient behavior

3) Several states have statutes that permit privileged communication between the client

and auditor, allowing a CPA to refuse to testify in state and federal courts.

A) True

B) False

4) A benefit obtained from comparing the client’s data with industry averages is that it

provides a(n):

A) benchmark to compare the company against industry averages

B) indication where errors exist in the statements

C) benchmark to be used in evaluating a client’s budgets

D) comparison of “what is” with “what should be”

5) Responsibility for the issuance of new notes payable would normally be vested in

the:

A) board of directors

B) purchasing department

C) accounting department

D) accounts payable department

6) Which of the following errors gives the auditor the least concern in auditing payroll

transactions?

A) An error that indicates possible fraud

B) Computational errors in formulas when a computerized system is used

C) Classification errors in charging labor to inventory and job cost accounts

D) Each of the above gives the auditor significant concern

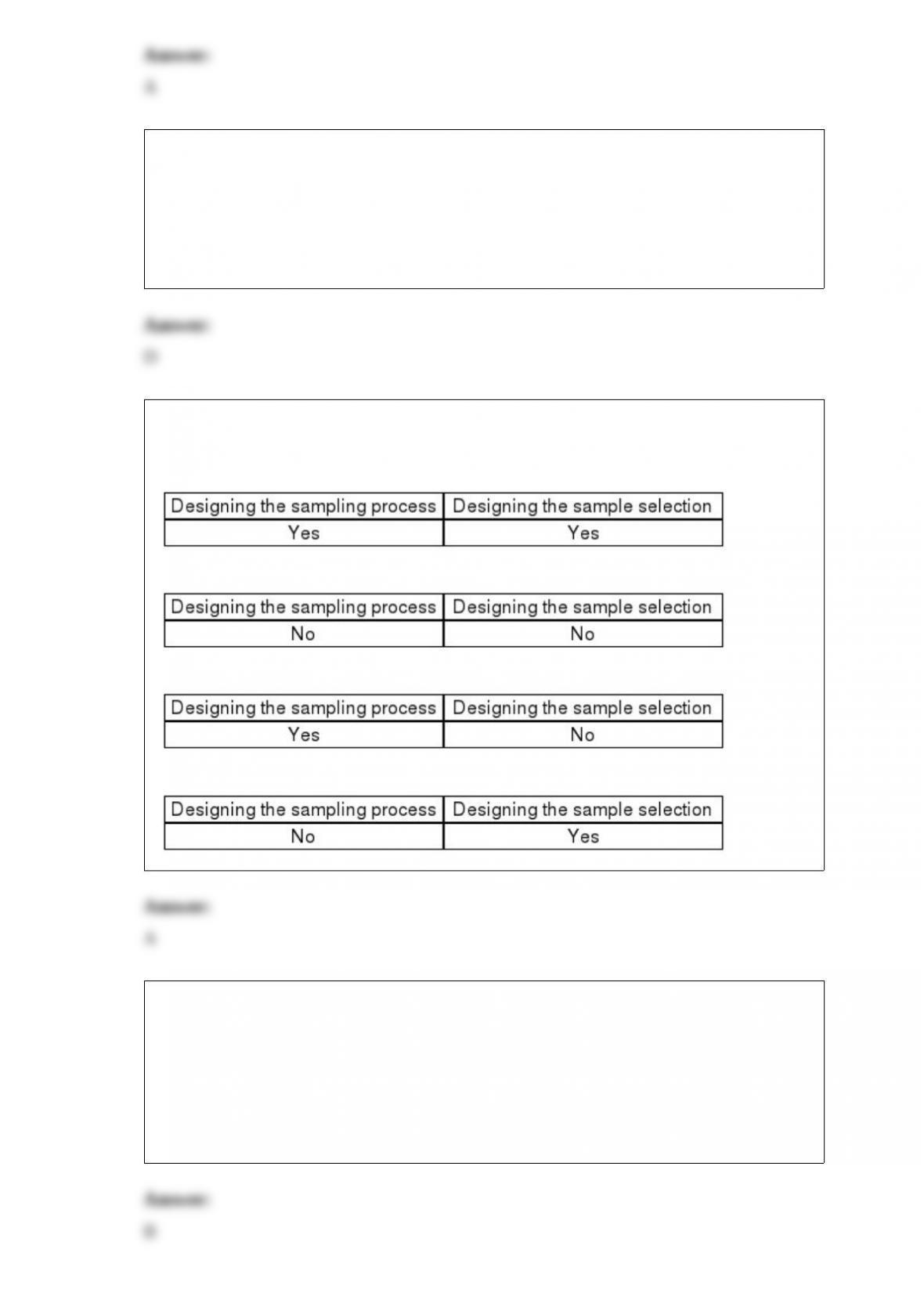

7) An auditor can increase the likelihood that a sample is representative by using care

in:

A)

B)

C)

D)

8) You are auditing Nelson and Company and determined that the sample results

support a conclusion that the account is materially misstated, when in fact it was not

misstated. This illustrates the risk of:

A) incorrect acceptance

B) incorrect rejection

C) control risk too low

D) control risk too high

9) The major considerations in evaluating the reasonableness of cost allocations are

compliance with GAAP and consistency with prior years.

A) True

B) False

10) Which one of the following analytical procedures would be most useful in alerting

the auditor to the possibility of obsolete inventory?

A) Compare gross margin percentage with previous years’

B) Compare unit costs of inventory with previous years’

C) Compare inventory turnover ratio with previous years’

D) Compare current year manufacturing costs with previous years’

11) The primary purpose of performing analytical procedures in the planning phase of

an audit is to:

A) help the auditor obtain an understanding of the client’s industry and business

B) assess the going concern assumption

C) indicate possible misstatements

D) reduce detailed tests

12) When planning an audit, the auditor’s assessed level of control risk is:

A) determined by using actuarial tables

B) calculated by using the audit risk model

C) a judgment issue, based on auditor knowledge

D) calculated by using the formulas provided in the

13) The failure to capitalize a permanent asset, or the recording of an asset acquisition

at the improper amount, affects the balance sheet:

A) forever

B) for the current period

C) for the depreciable life of the asset

D) until the firm disposes of the asset

14) The auditor, in auditing payroll, wants to determine that the individuals included in

her sample were employees of the company for the period under review. What is the

auditor’s best source of evidence?

A) Examination of Human Resource Records

B) Examination of the Payroll Master File

C) Examination of the Payroll Transaction File

D) Examination of the Payroll Tax Records

15) In the

A) True

B) False

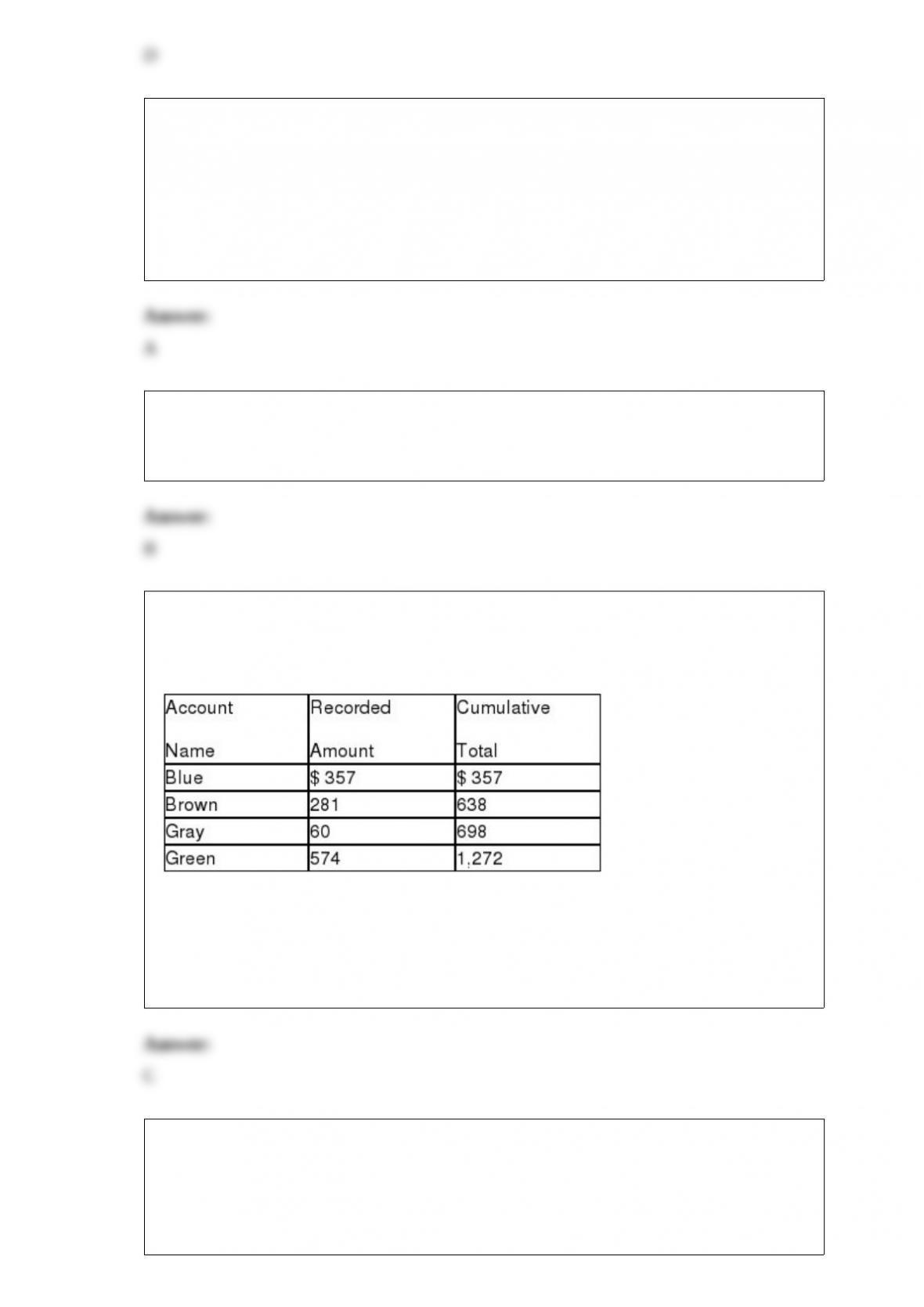

16) An accounts receivable population contains a total of four customers. The accounts,

the amounts, and the cumulative total are shown below. Monetary-unit sampling is to be

used.

Based on the information above, the population size is:

A) 4

B) 574

C) 1,272

D) $2,684

17) Which of the following activities would be least likely to strengthen a company’s

internal control?

A) separating accounting from other financial operations

B) maintaining insurance for fire and theft

C) fixing responsibility for the performance of employee duties

D) carefully selecting and training employees

18) Which of the following normally signs the engagement letter for an audit of a

private company?

A) Management

B) Board of directors representative

C) Audit committee representative

D) Corporate treasurer

19) Which of the following statements related to application controls is correct?

A) Application controls relate to various aspects of the IT function including software

acquisition and the processing of transactions

B) Application controls relate to various aspects of the IT function including physical

security and the processing of transactions in various cycles

C) Application controls relate to all aspects of the IT function

D) Application controls relate to the processing of individual transactions

20) In any company involved in manufacturing, an adequate cost accounting internal

control system is necessary to indicate the relative profitability of the various products

for management planning and control and to:

A) determine variances from standards

B) determine variances from budgets

C) value inventories for financial statement purposes

D) value inventories for audit verification

21) Match six of the terms (a-i) used in the capital acquisitions and repayment cycle

with the descriptions provided below (1-6):

a.Capital acquisition and repayment cycle

b.Capital stock certificate book

c.Closely held corporation

d.Independent registrar

e.Note payable

f.Publicly held corporation

g.Stock transfer agent

h.Schedule of notes payable and accrued interest

i.Stock maintenance agent

________ 1> An outside person engaged by a corporation to make sure that its stock is

issued in accordance with capital stock provisions in the corporate charter and

authorizations by the board of directors.

________ 2> The normal starting point for the audit of notes payable; includes detailed

information of all transactions related to notes payable that took place during the year.

________ 3> A record of the issuance and repurchase of capital stock for the life of the

corporation.

________ 4> An outside person engaged by a corporation to maintain the stockholder

records, and often to disburse cash dividends.

________ 5> An entity that is required to engage an independent registrar.

________ 6> The cycle that concerns the acquisition of capital resources through

interest-bearing debt and owners’ equity and repayment of the capital.

22) Audit fraud occurs when:

A) a misstatement is made and there is both knowledge of its falsity and the intent to

deceive

B) a misstatement is made and there is knowledge of its falsity but no intent to deceive

C) the auditor lacks even slight care in the performance in performing the audit

D) the auditor has an absence of reasonable care in the performance of the audit

23) A company has changed its method of inventory valuation from an unacceptable

one to one in conformity with generally accepted accounting principles. The auditor’s

report on the financial statements of the year of the change should include:

A) no reference to consistency

B) a reference to a prior period adjustment in the opinion paragraph

C) an explanatory paragraph that justifies the change and explains the impact of the

change on reported net income

D) an explanatory paragraph explaining the change

24) Whenever practical and reasonable, the confirmation of accounts receivable is

required of CPAs.

A) True

B) False

25) In which of the following situations would the auditor most likely issue an

unqualified report?

A) The client valued ending inventory by using the replacement cost method

B) The client valued ending inventory by using the Next-In-First-Out (NIFO) method

C) The client valued ending inventory at selling price rather than historical cost

D) The client valued ending inventory by using the First-In-First-Out (FIFO) method,

but showed the replacement cost of inventory in the Notes to the Financial Statements

26) If planned detection risk is reduced, the amount of evidence the auditor accumulates

will:

A) increase

B) decrease

C) remain unchanged

D) be indeterminate

27) Internal Auditors are expected to add value to the organization through improved

operational effectiveness. In addition, their responsibilities include all the following

except:

A) reviewing the reliability and integrity of information

B) ensuring compliance with the company’s accounting policies

C) verifying accounting information for external users

D) ensuring compliance with applicable governmental regulations

28) Which of the following statements is correct?

A) The overhead charged to inventory at the balance sheet date can be understated if the

salaries of administrative personnel are inadvertently or intentionally charged to indirect

manufacturing overhead

B) When jobs are billed on a cost-plus basis, revenue and total expenses are both

affected by charging labor to incorrect jobs

C) Payroll is a significant portion of inventory for retail and service industry companies

D) The valuation of inventory is affected if the direct labor cost of individual employees

is improperly charged to the wrong job or process

29) The standard of due care to which the auditor is expected to adhere to in the

performance of the audit is referred to as the:

A) prudent person concept

B) common law doctrine

C) due care concept

D) vigilant person concept

30) When a company prepares multi-copy, prenumbered sales invoices at the time

customer orders are received, there is a higher likelihood of failure to bill the customers

than when sales invoices are prepared only after goods have been shipped.

A) True

B) False

31) There are seven types of audit evidence: physical examination, confirmation,

documentation, observation, inquiries of the client, reperformance, and analytical

procedures. For each of the following types of audit tests, indicate the type(s) of

evidence that can be obtained through the test: (1) tests of controls, (2) substantive tests

of transactions, (3) analytical procedures, and (4) tests of details of balances.

32) List and describe the six elements of quality control. Who establishes the standards

for quality control?

33) Describe the audit procedures typically used to test for out-of-period liabilities (also

referred to as the search for unrecorded accounts payable).

34) Discuss the required communications between predecessor and successor auditors.

35) Explain acceptable risk of incorrect acceptance and acceptable risk of incorrect

rejection within the context of variables sampling.

36) You are the audit manager for a new audit client. Your staff auditors are unsure of

what constitutes a control deficiency. Discuss the definition of control deficiency. In

your response include at least two examples of control deficiencies.

37) Briefly explain each management assertion related to account balances at period

end.

38) The auditing standards of the Yellow Book are consistent with the ten generally

accepted auditing standards of the

39) In accumulating final evidence upon which to base an audit opinion, the auditor

should perform four activities. List the activities below.