On January 1, 2015, Edward Corporation had 10,000 shares of $6 par value common

stock and 10,000 shares of 8%, $100 par value convertible preferred stock outstanding.

The preferred shares carried a 3 for 1 conversion privilege. On October 1, 2015, all of

the preferred shares were converted to common. What number of shares must Edward

use in computing basic earnings per share at December 31, 2015?

A. 17,500.

B. 40,000.

C. 7,500.

D. 10,000.

Establishing budgeted amounts

(a) The text discusses two basic philosophies as to the levels at which budgeted

amounts should be set. Identify and describe briefly each of these two philosophies.

(b) Which of the two management philosophies would be more likely to elicit the

following comment?

“At our company, budgeted revenue is set so high and budgeted costs so low that no

department can ever meet the budget. This way, department managers can never relax;

they are motivated to keep working harder no matter how well they are already doing.”

The operating cycle:

A. Is repeated once per year for manufacturers and merchandisers.

B. Has seven steps.

C. Starts with using cash to purchase merchandise and ends with collecting the cash

back from customers.

D. Is longer for a retailer than for a manufacturer.

Wanda Company sold an asset for $10,000 on September 6, 2015. The historical cost of

the asset was $22,000, and the asset’s accumulated depreciation at the date of sale was

$14,500. Which of the following statements is correct?

A. Wanda will record a cash inflow from operating activities of $10,000 in its 2015

financial statements.

B. Wanda will record a cash inflow from investing activities of $10,000 in its 2015

financial statements.

C. Wanda will record a cash inflow from investing activities of $2,500 in its 2015

financial statements.

D. Wanda will record no cash flows related to this asset on its 2015 statement of cash

flows.

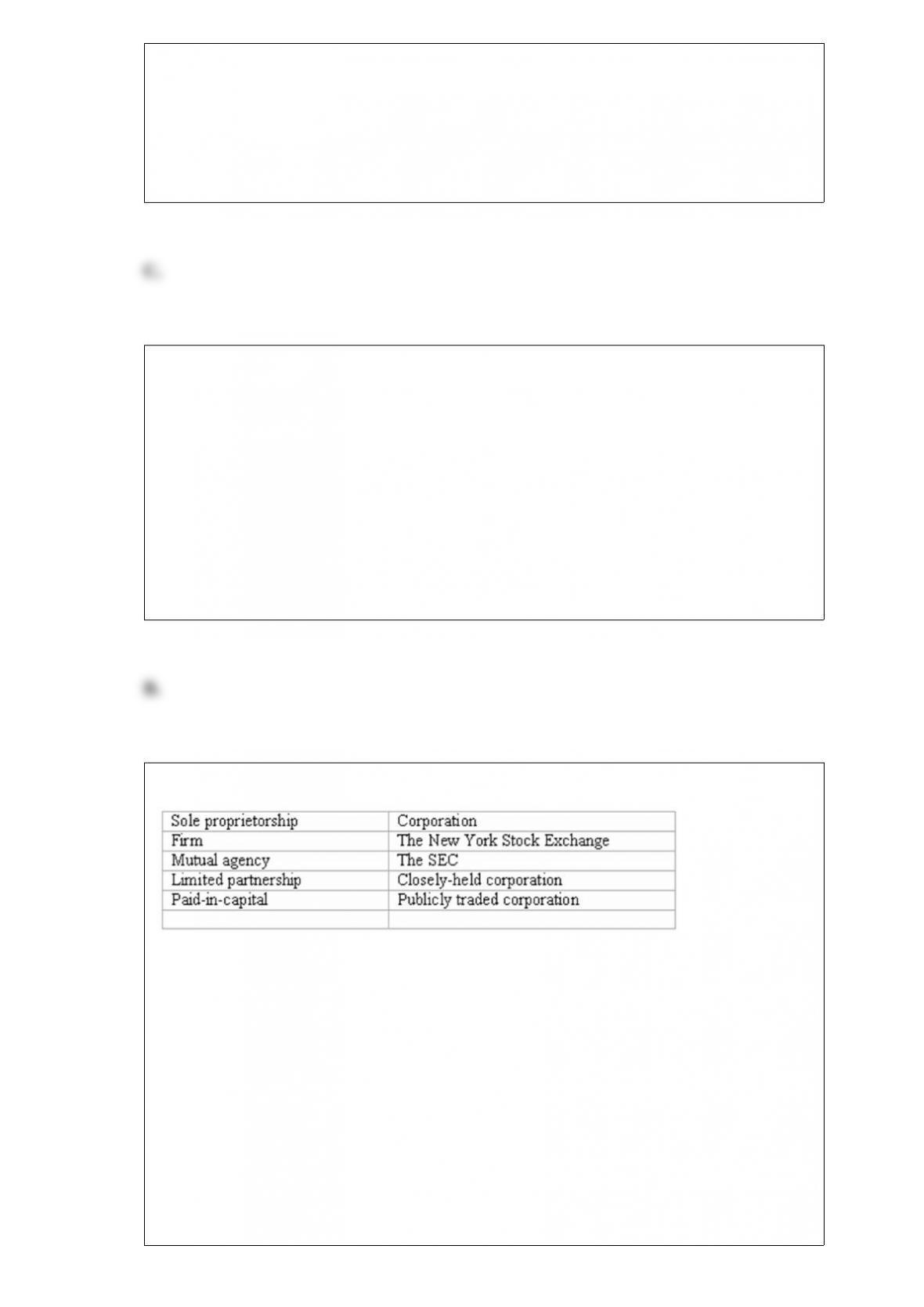

Listed below are several accounting terms introduced in this section.

Each of the following statements may (or may not) describe one of these accounting

terms. In the space provided, indicate the term described, or enter “none” if the

statement does not correctly describe any of the terms.

_________(A.) An unincorporated business owned by one person.

_________(B.) An example of an organized securities market.

_________(C.) The right of each partner to negotiate binding contracts.

_________(D.) The total earnings of a corporation less dividends paid out.

_________(E.) Investments by the owners of a corporation.

_________(F.) A partnership where one or more partners are not personally liable for

the debts of the partnership.

_________(G.) An organization that serves the professional needs of a CPA.

_________(H.) A business that is responsible for its own debts and which pays income

taxes on its earnings.

_________(I.) An unincorporated business owned by two or more people.

_________(J.) A corporation whose shares are not publicly traded.

Unearned revenue is:

A. An asset.

B. Income.

C. A liability.

D. An expense.

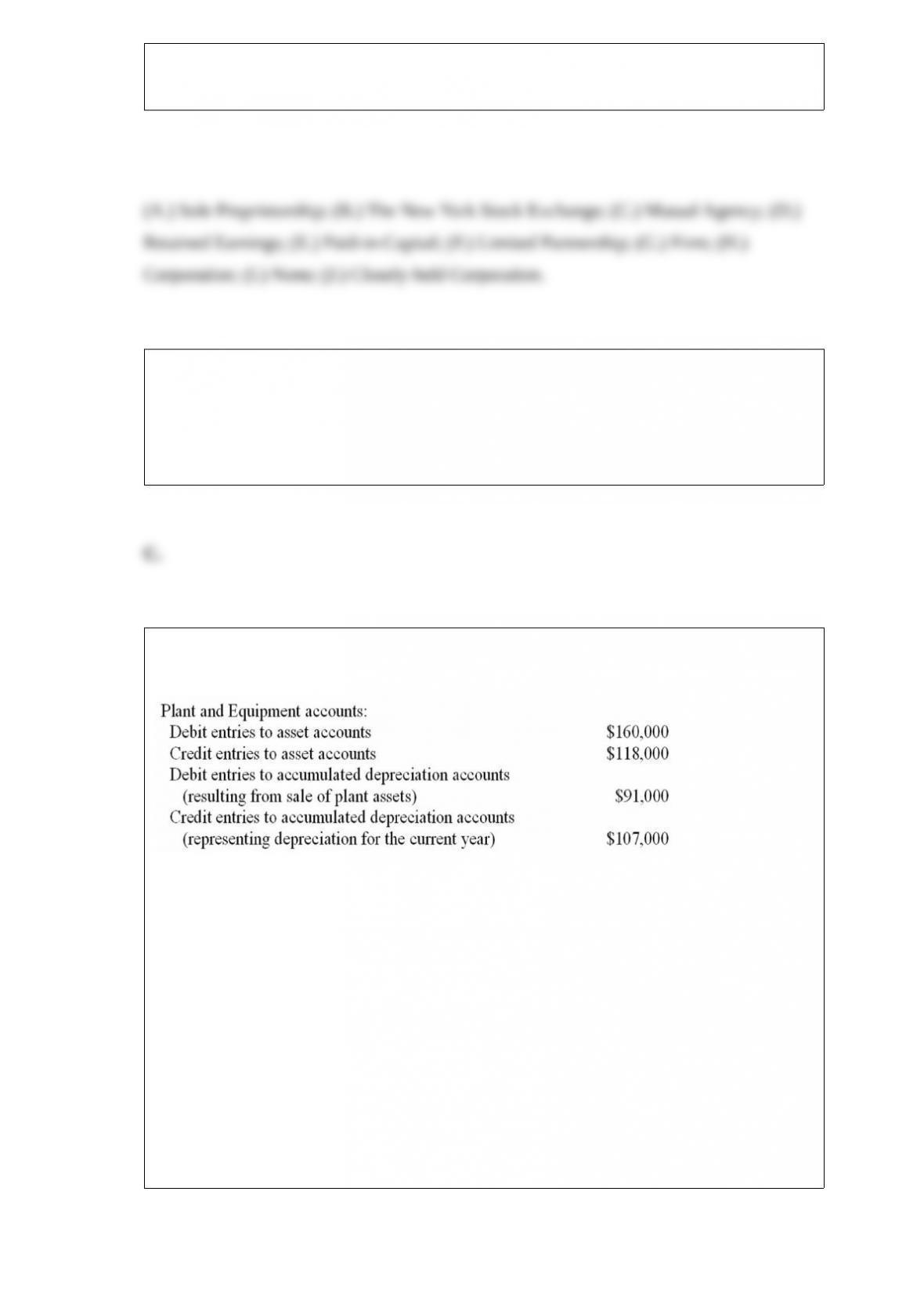

An analysis of changes in selected balance sheet accounts of Johnson Corporation

shows the following for the current year:

Johnson’s income statement for the current year includes a $14,000 loss on disposal of

plant assets. All payments and proceeds relating to purchase or sale of plant assets were

in cash.

Refer to the information above. How should purchases, sales, and depreciation of plant

assets be classified in Johnson’s statement of cash flows for the current year? (Assume

the direct method is used by Johnson.)

A. Purchases of plant assets are classified as investing activities; sales of plant assets

are classified as financing activities; depreciation is classified as an operating activity.

B. Purchases of plant assets and depreciation are classified as investing activities; sales

of plant assets are classified as financing activities.

C. Purchases and sales of plant assets are classified as investing activities; depreciation

does not appear as an operating, financing, or investing activity.

D. Since plant assets are used to generate income from operations, purchases, sales, and

depreciation of plant assets are all classified as operating activities.

Using more direct labor hours for units produced than the amount allowed by the

standard results in:

A. An unfavorable total labor variance.

B. An unfavorable labor efficiency variance, regardless of the wage rate paid to

employees.

C. An unfavorable labor efficiency variance only if the wage rate is higher than

standard cost allowed.

D. A favorable labor rate variance, because the hourly wage rate is automatically

reduced when workers operate less efficiently.

Operating and capital leases

Berkeley Corporation wants to expand operations and is considering various leasing

arrangements for additional equipment. Berkeley’s management has heard the terms

capital lease and operating lease mentioned by the accounting department and wants

clarification of these terms before signing any lease contracts.

(a) Briefly explain the difference between a capital lease and an operating lease from a

lessee’s (Berkeley’s) point of view. Your answer should include the financial statement

impact of each type of lease.

(b) How does a lessee determine whether a specific lease contract is an operating lease

or a capital lease? Include at least two of the criteria specified by the FASB in your

answer.

(c) Which of the above two types of leases is sometimes referred to as

“off-balance-sheet financing?” Briefly explain.

Yale Company purchased equipment having an invoice price of $21,500. The terms of

sale were 2/10, n/30, and Yale paid within the discount period. In addition, Yale paid a

$320 delivery charge, $350 installation charge, and $1,183 sales tax. The amount

recorded as the cost of this equipment is:

A. $21,070.

B. $21,500.

C. $21,740.

D. $22,923.

Comparison of LIFO and FIFO

Both Company X and Company Y sell the same product. The cost of this product has

been rising steadily throughout the year. Both companies reported the same net income

for the year, although Company X used the first-in, first-out method of pricing

inventory, while Company Y used the last-in, first-out method.

(a) Which company’s valuation of ending inventory in the balance sheet is more likely

to approximate replacement cost?

Company ______________________________

(b) Which company reports a cost of goods sold figure in the current year income

statement that is more likely to reflect the replacement cost of the units sold?

Company ______________________________

(c) Which company is minimizing income taxes it must pay?

Company ______________________________

(d) Which company would have reported the higher net income if both companies had

used the same method of pricing inventory?

Company ______________________________

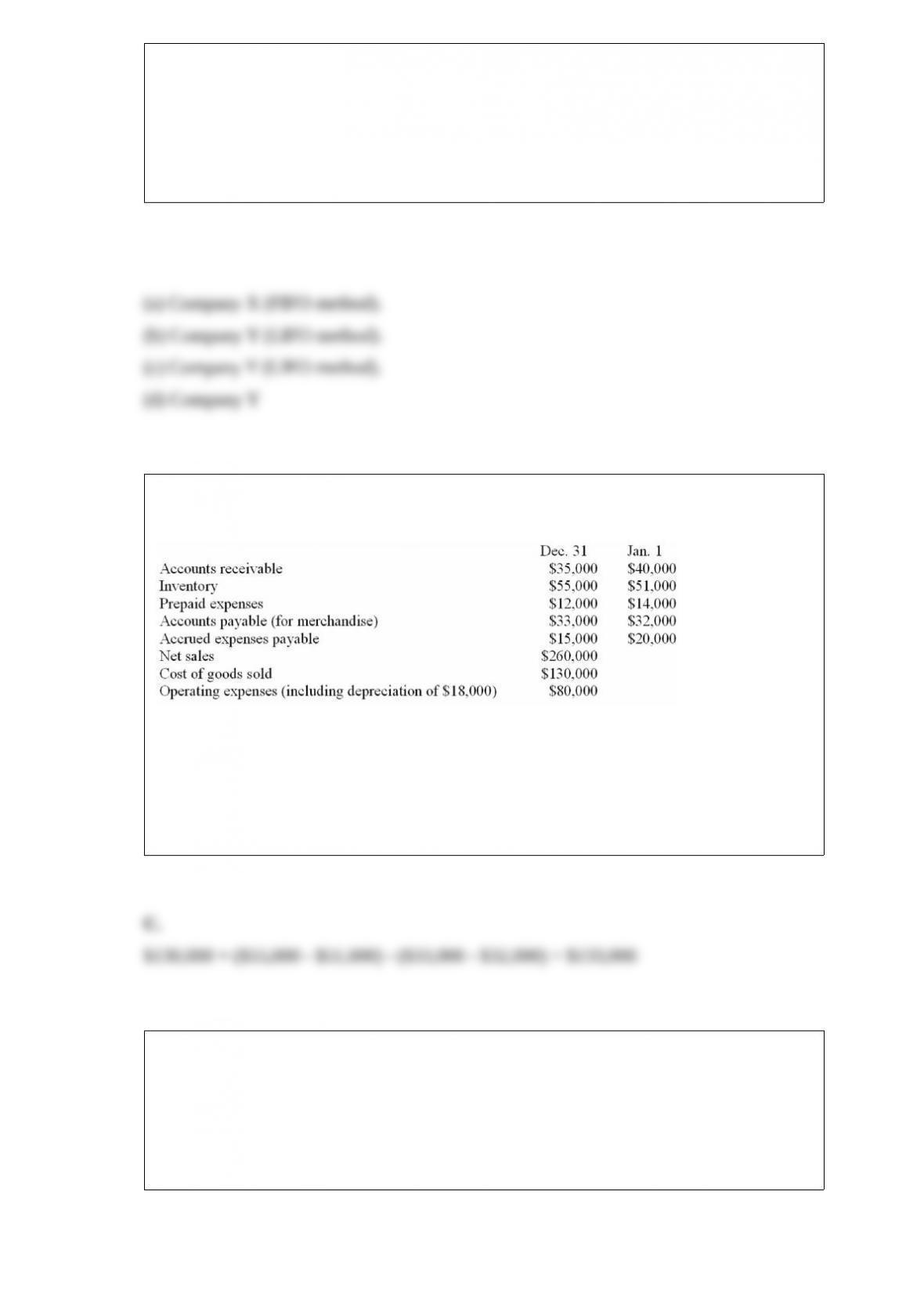

The financial statements of Seldin, Inc., provide the following information for the

current year:

Refer to the information above. Compute the amount of Seldin’s cash payments for

purchases of merchandise during the current year.

A. $130,000.

B. $125,000.

C. $133,000.

D. $127,000.

Which of the following entries causes an immediate decrease in assets and in net

income?

A. The entry to record depreciation expense.

B. The entry to record revenue earned but not yet received.

C. The entry to record the earned portion of rent received in advance.

D. The entry to record accrued wages payable.

On December 1, Year 1, Bradley Corporation incurs a 15-year $200,000 mortgage

liability in conjunction with the acquisition of an office building. This mortgage is

payable in monthly installments of $2,400, which include interest computed at the rate

of 12% per year. The first monthly payment is made on December 31, Year 1.

Refer to the information above. Compute the total amount to be paid by Bradley over

the 15-year life of the mortgage.

A. $200,000.

B. $562,000.

C. $432,000.

D. $474,000.

During the month of May, Henderson Company had the following transactions:

* Revenues of $60,000 were earned and received in cash.

* Bank loans of $9,000 were paid off.

* Equipment of $20,000 was purchased.

* Expenses of $36,800 were paid.

* Stockholders purchased additional shares for $22,000 cash.

A statement of cash flows for May would report net cash flows from operating activities

of:

A. $60,000.

B. $16,200.

C. $23,200.

D. $20,000.

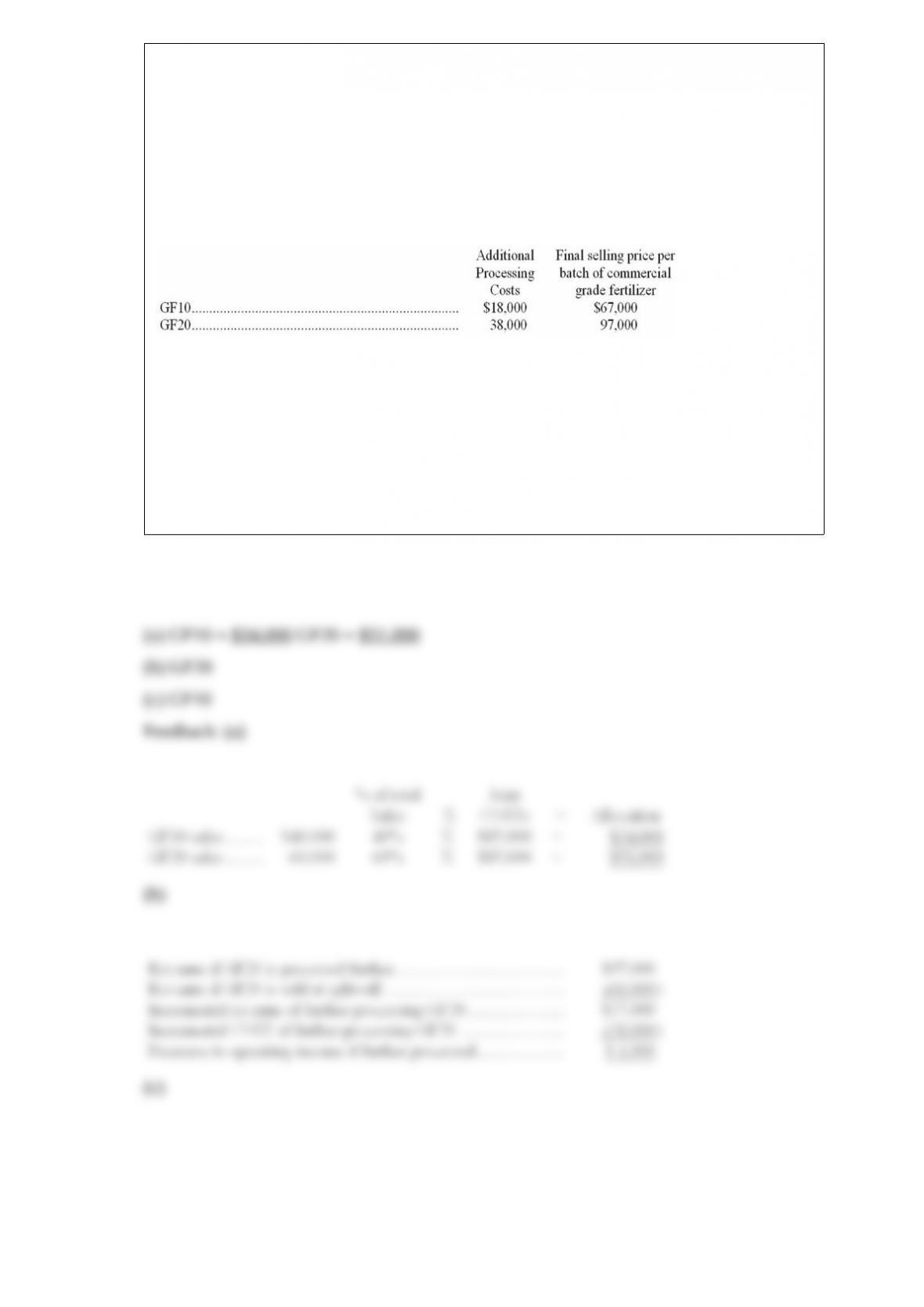

Joint production decisions

Grassy Fertilizer manufactures two lines of garden grade fertilizer as part of a joint

production process: GF10 and GF20. Joint costs up to the split-off point total $85,000

per batch. These joint costs are allocated to GF10 and GF20 in proportion to their

relative sales values at the split-off point of $40,000 and $60,000, respectively.

Both lines of garden grade fertilizer can be further processed into commercial grade

fertilizer. The following table summarizes the costs and revenue associated with

additional processing of GF10 and GF20:

(a) The $85,000 in joint costs should be allocated to each product as follows:

GF10 $____________, GF20 $____________

(b) Which product (GF10 or GF20) would result in a net decrease in operating income

if processed into a commercial grade fertilizer?

____________

(c) Which product (GF10 or GF20) would result in a net increase in operating income if

processed into a commercial grade fertilizer?

____________

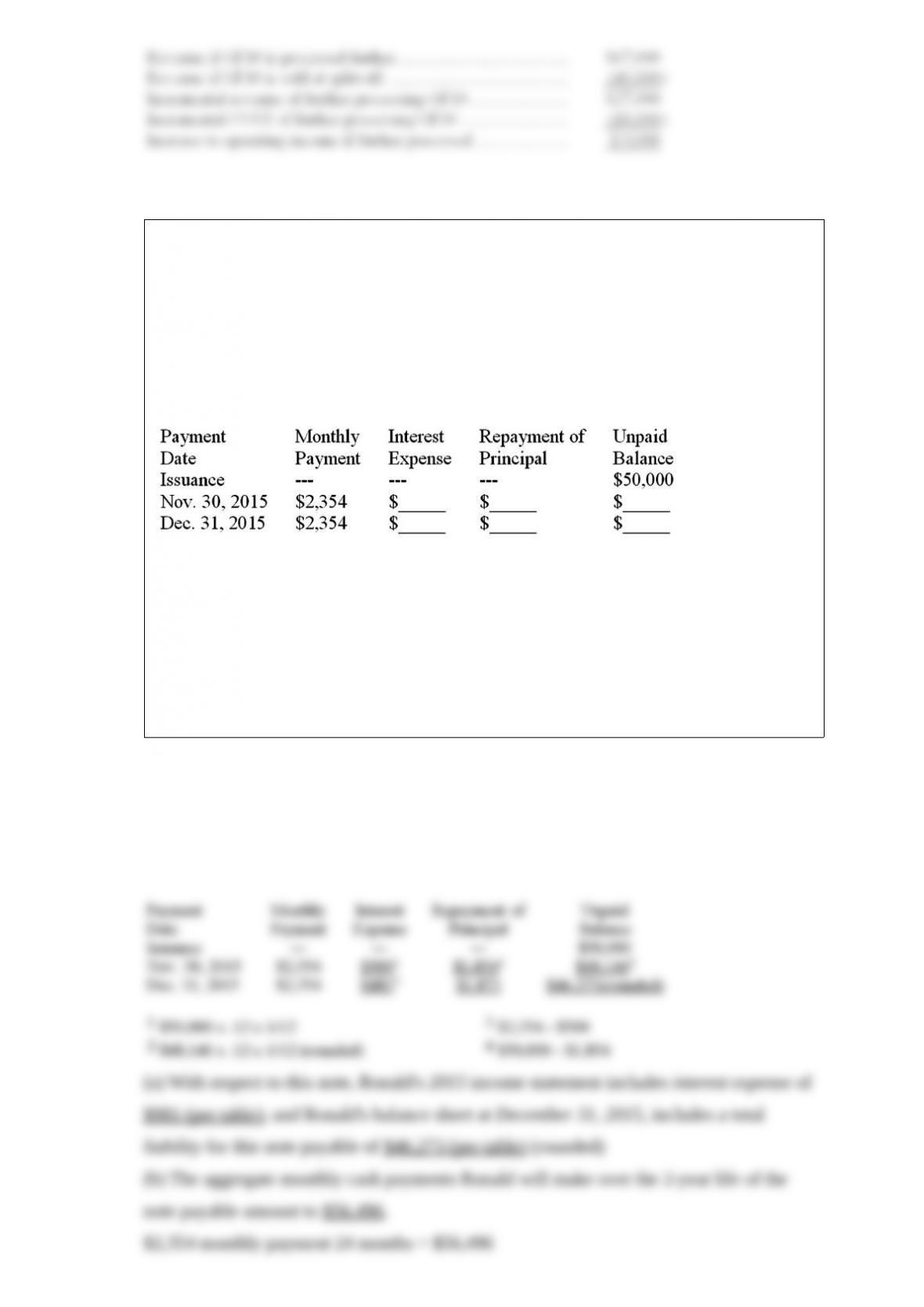

Fully amortizing installment note payable

On October 31, 2015 Ronald signed a 2-year installment note in the amount of $50,000

in conjunction with the purchase of equipment. This note is payable in equal monthly

installments of $2,354, which include interest computed at an annual rate of 12%. The

first monthly payment is made on November 30, 2015. This note is fully amortizing

over 24 months.

Complete the amortization table for the first two payments by entering the correct dollar

amounts in the blank spaces provided. In addition, answer the questions that follow.

(a) With respect to this note, Ronald’s 2015 income statement includes interest expense

of $_______________, and Ronald’s balance sheet at December 31, 2015, includes a

total liability for this note payable of ______________. (Do not separate into current

and long-term portions.)

(b) The aggregate monthly cash payments Ronald will make over the 2-year life of the

note payable amount to $_______________.

(c) Over the 2-year life of the note, the amount Ronald will pay for interest amounts to

$_______________.

Goods that are still in the production process would be in which account?

A. Raw Materials Inventory.

B. Work in Process Inventory.

C. Finished Goods Inventory.

D. Cost of Goods Sold.

World of Sound is a small retail business that specializes in the sale of top-of-the-line

sound systems. This year, the store has begun to carry the Surround Sound

manufactured by Carp Co. Thus far, World of Sound has recorded the following

transactions involving the Surround Sound

May 5 Purchased 18 units at a unit cost of $2,400

May 18 Purchased 15 additional units at $2,550 each

June 12 Sold 19 units to the Davies Theater

Refer to the information above. If World of Sound uses a perpetual inventory system,

the journal entry to record the purchase on May 18th would include which of the

following?

A. A debit to the Purchases account for $38,250.

B. A debit to the Cost of Goods Sold for $38,250.

C. A credit to Inventory for $38,250.

D. A debit to Inventory for $38,250.

VanRoy Supplies reports net sales of $1,750,000, net income of $175,000, and gross

profit of $300,000. The company’s cost of goods sold is:

A. $1,400,000.

B. $475,000.

C. $1,575,000.

D. $1,450,000.

Refer to the information above. What is the return on sales for Brookes, Inc. (round

your answer to the nearest full percentage point)?

A. 13%.

B. 19%.

C. 9%.

D. 70%.

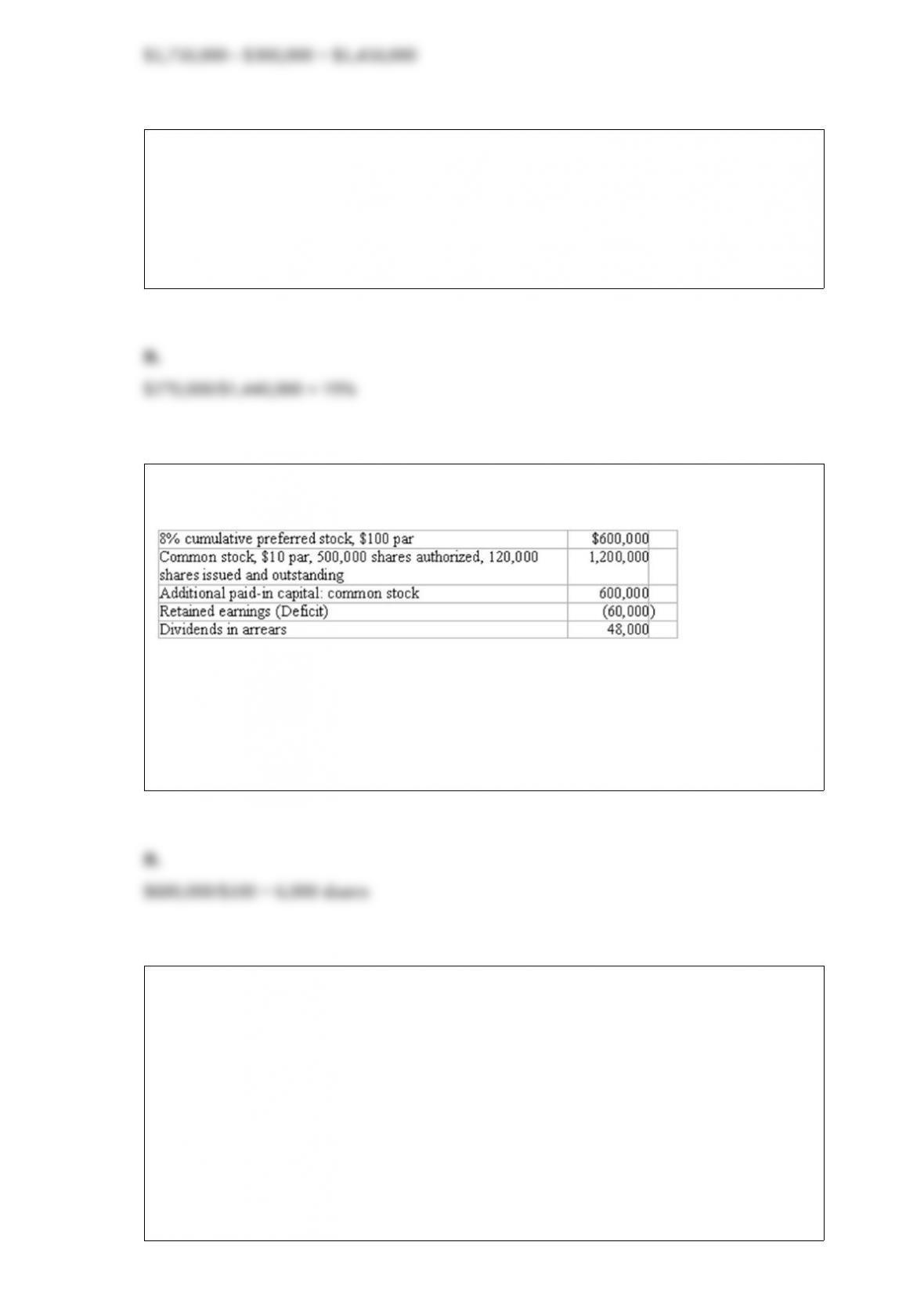

Shown below is information relating to the stockholders’ equity of Reeve Corporation

as of December 31, 2015:

Refer to the information above. How many shares of preferred stock are issued and

outstanding?

A. 75,000 shares.

B. 6,000 shares.

C. 60,000 shares.

D. 120,000 shares.

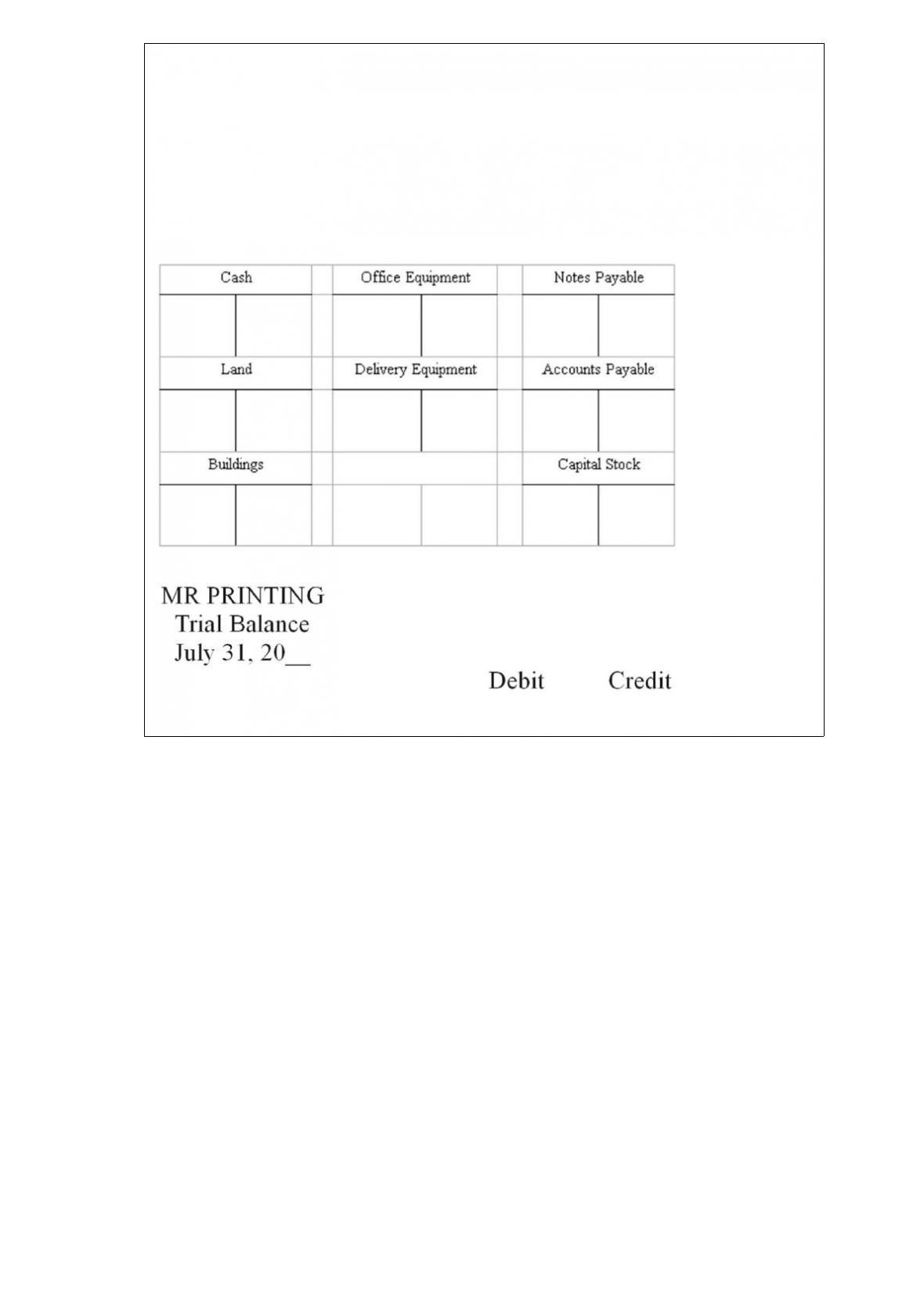

Recording transactions directly in T accounts; trial balance

On July 20, Mollie Rose began a new business called MR Printing, which provides

typing, duplicating, and printing services. The following six transactions were

completed by the business during July.

(A.) Issued to Rose 1,000 shares of capital stock in exchange for her investment of

$200,000 cash.

(B.) Purchased land and a small building for $450,000, paying $165,000 cash and

signing a note payable for the balance. The land was considered to be worth $240,000

and the building $210,000.

(C.) Purchased office equipment for $30,000 from Quality Interiors, Inc. Paid $17,000

cash and agreed to pay the balance within 60 days.

(D.) Purchased a motorcycle on credit for $3,400 to be used for making deliveries to

customers. Mollie agreed to make payment to Spokes, Inc. within 10 days.

(E.) Paid in full the account payable to Spokes, Inc.

(F.) Borrowed $30,000 from a bank and signed a note payable due in six months.

Instructions

(A.) Record the above transactions directly in the T accounts below. Identify each entry

in a T account with the letter shown for the transaction. This exercise does not call for

the use of a journal.

(B.) Prepare a trial balance at July 31 by completing the form provided.

(A)

The net income of a sole proprietorship should compensate the owner for all of the

following except:

A. Personal service.

B. The income taxes paid by the owner.

C. Capital invested by the owner.

D. The risk taken by the owner.

Which of the following should not be classified as inventory in the balance sheet of a

large automobile dealership?

A. Pickup trucks offered for sale.

B. Used cars taken in trade and offered for sale on the company’s used-car lot.

C. Spark plugs, oil filters, and other parts which are intended for use by the service

department in repairing and servicing customers’ cars.

D. “Company cars” provided to specific company executives for their personal use.

Sterling Corporation has borrowed $75,000 that must be repaid in two years. This

$75,000 is to be invested in an eight-year project with an estimated annual net cash

flow of $15,000. The payback period for this investment is:

A. Two years.

B. Five years.

C. Eight years.

D. Indeterminable with the given information.

Tuliptime, Inc. sold American fashions to a Japanese company at a price of 4 million

yen. On the sale date, the exchange rate was $0.0100 per Japanese yen, but when

Tuliptime received payment from its customer, the exchange rate was $0.0103 per yen.

When the foreign receivable was collected, Tuliptime:

A. Credited Sales for $1,200.

B. Debited Cash for $40,000.

C. Credited Gain on Fluctuation of Foreign Currency for $1,200.

D. Debited Loss on Fluctuation of Foreign Currency for $1,200.

In cost-volume-profit analysis, income tax expense:

A. Is included among the monthly operating expenses as a variable cost.

B. Is considered a fixed cost of doing business.

C. Is treated as a semi-variable cost that is partially dependent upon sales volume.

D. Is generally ignored.

Assume the exchange rate for the Canadian dollar is rising relative to the U.S. dollar.

An American company will incur losses from this rising exchange rate if it is making:

A. Credit sales to Canadian companies at prices stated in Canadian dollars.

B. Credit purchases from Canadian companies at prices stated in U.S. dollars.

C. Credit sales to Canadian companies at prices stated in U.S. dollars.

D. Credit purchases from Canadian companies at prices stated in Canadian dollars.

Which of the following results in the cost of goods sold being stated at the most current

acquisition costs?

A. Average cost.

B. Specific identification.

C. FIFO.

D. LIFO.

Bonds, with the same face value, issued at a premium will:

A. Have a greater maturity value than a bond issued at a discount.

B. Have a lesser maturity value than a bond issued at a discount.

C. Have the same maturity value as a bond issued at a discount.

D. Have a different maturity value than a bond issued at a discount, depending upon the

interest rate and maturity date.

Accounts receivable are classified as current assets:

A. Only if convertible into cash within 60 days or sooner.

B. Only if the allowance method is used to estimate the uncollectible accounts.

C. Only if convertible into cash within one year.

D. Whenever the accounts receivable arise from “normal” sales of merchandise to

customers, regardless of the credit terms.

The Financial Accounting Standards Board is:

A. Responsible for the review and audit of federal income tax returns.

B. Primarily concerned with the preparation of the annual federal budget.

C. A private group that conducts research and determines generally accepted accounting

principles.

D. A government agency with legal authority to approve or disapprove the financial

statements of corporations that sell their securities to the public.

The amount of earnings per share is usually computed:

A. For both preferred and common stock.

B. For common stock by deducting the dividends on preferred stock from net income

and dividing the remaining amount by the weighted average number of common shares

outstanding.

C. By dividing net income by the combined number of preferred and common shares.

D. On the basis of the number of shares outstanding at year-end, regardless of changes

in the number of shares during the year.